Reckitt Benckiser Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Reckitt Benckiser faces intense rivalry in fast-moving consumer goods, with strong brands and scale reducing buyer power and raising switching costs; supplier power is moderate due to diversified global sourcing, while regulatory barriers and scale keep new entrants at bay and substitutes (private labels, niche innovators) a steady threat. This preview is just the starting point. Dive into a complete, consultant-grade breakdown of Reckitt Benckiser Group’s industry competitiveness—ready for immediate use.

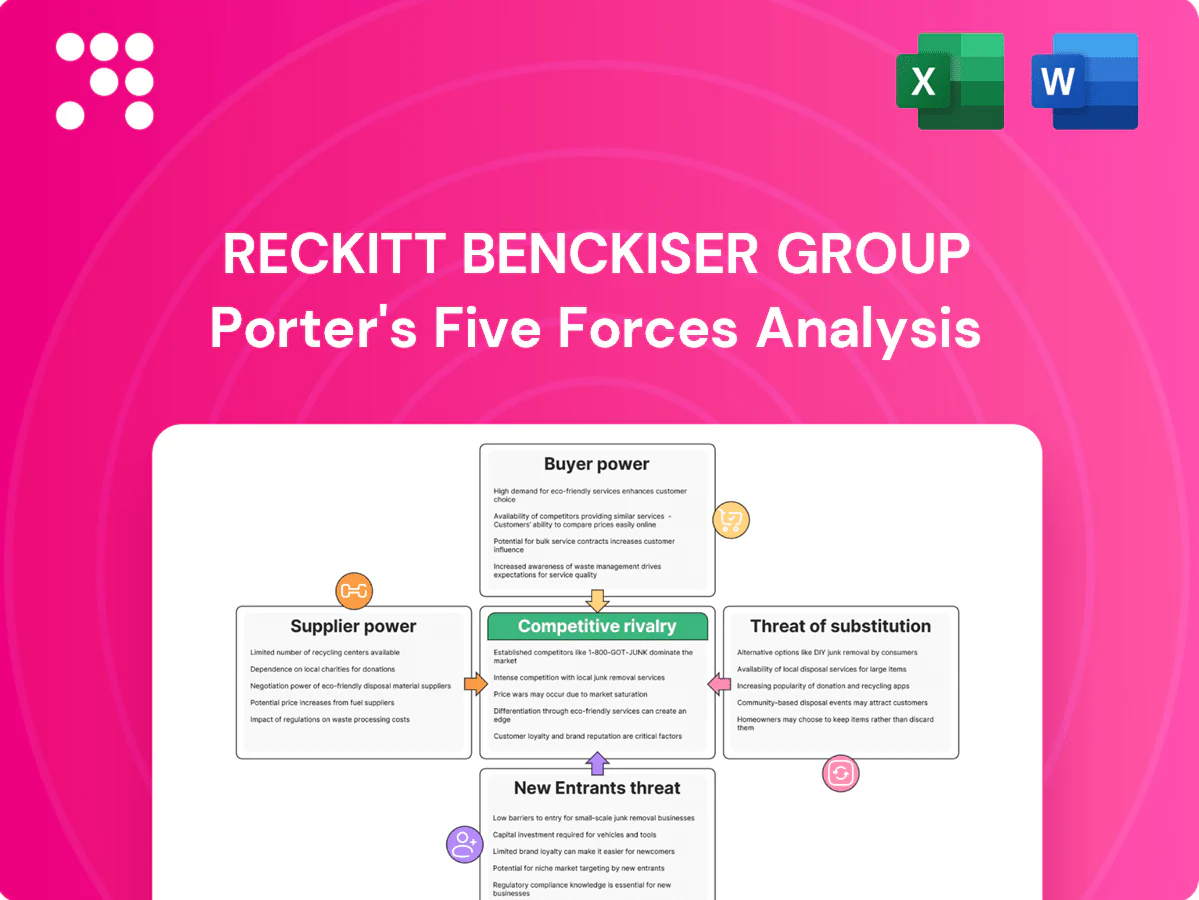

Suppliers Bargaining Power

Diversified raw material base

Reckitt sources chemicals, APIs, fragrances and packaging from a broad global pool, limiting single-supplier leverage and supporting its £12.5bn 2024 revenue base.

Multi-sourcing and dual qualification across categories reduce switching risk and supply disruption exposure, while logistics and regional hubs spread procurement geographically.

Specialized actives and pharma-grade inputs in health can narrow options, so supplier power is moderate and varies by input criticality.

Regulated and specialized inputs

Regulated OTC medicines and infant nutrition require GMP-certified, audited suppliers, raising switching costs and favoring long-term contracts; the global infant formula market was estimated at about USD 70 billion in 2024, concentrating demand on qualified dairy-protein suppliers. Strict quality, traceability and auditability concentrate supply, increasing vendor influence and price-setting power. Disruptions in specialized excipients or dairy proteins can halt production, strengthening supplier power in these tightly regulated lines.

Packaging and logistics volatility

Packaging inputs such as resins, aluminum, glass and corrugate move with energy and commodity cycles, and freight/logistics shocks can amplify supplier bargaining power during tight markets; container rates that surged over 200% versus pre‑pandemic peaks in 2021–22 had largely eased by 2024, reducing but not eliminating pressure. Long‑term contracts and hedging partially mitigate volatility, yet bargaining power shifts cyclically and spikes sharply in periods of scarcity.

Scale and procurement leverage

Reckitt’s global scale (2024 net revenue ~£13.0bn) secures volume discounts and more favorable supplier terms, shifting pricing power toward the buyer. Centralized procurement and category management concentrate spend and enhance negotiating clout across categories. Vendor performance programs and supplier relationship management raised reliability and reduced cost for non-specialty inputs.

- Scale: global spend consolidation

- Procurement: centralized category teams

- SRM: vendor KPIs/improved reliability

- Power: favors Reckitt on non-specialty goods

Sustainability and compliance demands

Sustainability and stricter ESG, recyclability and responsible sourcing standards in 2024 have narrowed Reckitt's supplier pool, raising verification and traceability needs.

Compliance-related costs—notably audit and certification spend—are increasingly passed to buyers; Reckitt's FY 2024 revenue was £12.1bn, highlighting material margin sensitivity.

Strategic supplier partnerships secure innovation and supply assurance but can lock pricing and terms, modestly elevating supplier influence.

- ESG-driven supplier narrowing

- Compliance cost pass-through

- Partnerships = security vs. flexibility

- Moderate increase in supplier power

Moderate supplier power: specialized pharma and infant-nutrition increase leverage despite scale

Reckitt faces moderate supplier power: broad multi‑sourcing and centralized procurement favor the buyer, but specialized pharma actives, GMP suppliers and ESG vetting concentrate supply for critical lines.

Infant‑nutrition and regulated OTC inputs and audit costs raise switching costs; partnerships secure supply but can lock terms.

Scale (FY2024 revenue £12.1bn) and SRM mitigate but do not eliminate cyclical supplier leverage.

| Metric | 2024 |

|---|---|

| Revenue | £12.1bn |

| Infant formula market | USD70bn |

| Container rate peak vs pre‑pandemic | +200% (2021–22) |

What is included in the product

Tailored Porter's Five Forces analysis for Reckitt Benckiser Group, uncovering competitive intensity, buyer and supplier power, substitute threats, and barriers protecting incumbents, with strategic implications for pricing and market share.

A clear one-sheet summary of all five forces for Reckitt Benckiser—customizable pressure levels and instant spider/radar chart visualization to relieve strategic uncertainty and slot directly into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated retail channels

Large retailers and wholesalers exert material shelf and pricing power—Walmart accounted for about 25% of US grocery sales in 2024 and the UK Big Four held roughly 68% of grocery market share per Kantar—forcing high trade spend, slotting fees and promotional support to secure visibility. Delist risk in mature categories raises margin pressure, and buyer power peaks where channel concentration is greatest.

E-commerce and marketplace dynamics

Online platforms increase price transparency and comparison shopping, with marketplaces typically accounting for 20%+ of CPG online sales and commission rates commonly around 15–20%, squeezing manufacturer margins.

Platforms demand fees, data sharing and rapid fulfillment standards—Amazon reported 2024 Prime delivery and seller performance KPIs tightening lead times and penalties.

Direct-to-consumer reduces reliance but raises marketing spend and logistics costs; overall digital channels shift bargaining power toward platforms and consumers.

Private label alternatives

Retailers aggressively expand private labels in commoditized cleaners and wipes, with Western Europe private-label penetration near 39% value in 2024, anchoring lower price points and eroding premium tiers. Private labels often undercut branded prices by 20–40%, forcing Reckitt to defend share through faster innovation and sustained brand equity investments. Buyer power increases when store brands reach “good enough” quality, prompting trade promotions and selective premiumization by Reckitt to protect margins.

Brand loyalty in health and hygiene

Trusted OTC, disinfectant and infant nutrition brands (eg Dettol, Nurofen, Enfamil) reduce price elasticity and dampen switching despite promotions; in 2024 Reckitt reported c.£13.0bn revenue with health & hygiene driving the majority of sales, so brand trust tempers retailer leverage in critical need-states and moderates buyer power.

- Brand trust reduces elasticity

- Perceived safety limits switching

- Retailer leverage constrained in need-states

Promotional intensity and trade terms

Frequent promotions train consumers to wait for deals, shifting purchasing power toward retailers and amplifying customer bargaining power for Reckitt Benckiser. Retailers routinely negotiate funding for features, end-caps and prominent online placement, increasing trade spend and promotional dependency. Over-reliance on such tactics can compress gross margins, forcing stricter revenue management to protect profitability.

- Promotions drive purchase timing pressure

- Retailer funding demands increase trade spend

- Margin compression risk from heavy promotions

- Requires disciplined revenue management

Retail concentration, marketplaces and private labels squeeze CPG margins

Large concentrated retailers (Walmart ~25% US grocery 2024; UK Big Four ~68% share) and marketplaces (~20%+ CPG online sales; 15–20% commissions) exert strong pricing/shelf leverage, driving high trade spend and margin pressure. Private label penetration (Western Europe ~39% value 2024) and promotions compress prices, though Reckitt’s c.£13.0bn 2024 revenue and strong brands temper switching.

| Metric | 2024 |

|---|---|

| Walmart US grocery | ~25% |

| UK Big Four | ~68% |

| Private label WE | ~39% value |

| Reckitt revenue | c.£13.0bn |

Preview the Actual Deliverable

Reckitt Benckiser Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of Reckitt Benckiser Group provides a clear assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with actionable implications for strategy and valuation. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use instantly after purchase.

Don't Miss the Bigger Picture

Reckitt Benckiser faces intense rivalry in fast-moving consumer goods, with strong brands and scale reducing buyer power and raising switching costs; supplier power is moderate due to diversified global sourcing, while regulatory barriers and scale keep new entrants at bay and substitutes (private labels, niche innovators) a steady threat. This preview is just the starting point. Dive into a complete, consultant-grade breakdown of Reckitt Benckiser Group’s industry competitiveness—ready for immediate use.

Suppliers Bargaining Power

Diversified raw material base

Reckitt sources chemicals, APIs, fragrances and packaging from a broad global pool, limiting single-supplier leverage and supporting its £12.5bn 2024 revenue base.

Multi-sourcing and dual qualification across categories reduce switching risk and supply disruption exposure, while logistics and regional hubs spread procurement geographically.

Specialized actives and pharma-grade inputs in health can narrow options, so supplier power is moderate and varies by input criticality.

Regulated and specialized inputs

Regulated OTC medicines and infant nutrition require GMP-certified, audited suppliers, raising switching costs and favoring long-term contracts; the global infant formula market was estimated at about USD 70 billion in 2024, concentrating demand on qualified dairy-protein suppliers. Strict quality, traceability and auditability concentrate supply, increasing vendor influence and price-setting power. Disruptions in specialized excipients or dairy proteins can halt production, strengthening supplier power in these tightly regulated lines.

Packaging and logistics volatility

Packaging inputs such as resins, aluminum, glass and corrugate move with energy and commodity cycles, and freight/logistics shocks can amplify supplier bargaining power during tight markets; container rates that surged over 200% versus pre‑pandemic peaks in 2021–22 had largely eased by 2024, reducing but not eliminating pressure. Long‑term contracts and hedging partially mitigate volatility, yet bargaining power shifts cyclically and spikes sharply in periods of scarcity.

Scale and procurement leverage

Reckitt’s global scale (2024 net revenue ~£13.0bn) secures volume discounts and more favorable supplier terms, shifting pricing power toward the buyer. Centralized procurement and category management concentrate spend and enhance negotiating clout across categories. Vendor performance programs and supplier relationship management raised reliability and reduced cost for non-specialty inputs.

- Scale: global spend consolidation

- Procurement: centralized category teams

- SRM: vendor KPIs/improved reliability

- Power: favors Reckitt on non-specialty goods

Sustainability and compliance demands

Sustainability and stricter ESG, recyclability and responsible sourcing standards in 2024 have narrowed Reckitt's supplier pool, raising verification and traceability needs.

Compliance-related costs—notably audit and certification spend—are increasingly passed to buyers; Reckitt's FY 2024 revenue was £12.1bn, highlighting material margin sensitivity.

Strategic supplier partnerships secure innovation and supply assurance but can lock pricing and terms, modestly elevating supplier influence.

- ESG-driven supplier narrowing

- Compliance cost pass-through

- Partnerships = security vs. flexibility

- Moderate increase in supplier power

Moderate supplier power: specialized pharma and infant-nutrition increase leverage despite scale

Reckitt faces moderate supplier power: broad multi‑sourcing and centralized procurement favor the buyer, but specialized pharma actives, GMP suppliers and ESG vetting concentrate supply for critical lines.

Infant‑nutrition and regulated OTC inputs and audit costs raise switching costs; partnerships secure supply but can lock terms.

Scale (FY2024 revenue £12.1bn) and SRM mitigate but do not eliminate cyclical supplier leverage.

| Metric | 2024 |

|---|---|

| Revenue | £12.1bn |

| Infant formula market | USD70bn |

| Container rate peak vs pre‑pandemic | +200% (2021–22) |

What is included in the product

Tailored Porter's Five Forces analysis for Reckitt Benckiser Group, uncovering competitive intensity, buyer and supplier power, substitute threats, and barriers protecting incumbents, with strategic implications for pricing and market share.

A clear one-sheet summary of all five forces for Reckitt Benckiser—customizable pressure levels and instant spider/radar chart visualization to relieve strategic uncertainty and slot directly into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated retail channels

Large retailers and wholesalers exert material shelf and pricing power—Walmart accounted for about 25% of US grocery sales in 2024 and the UK Big Four held roughly 68% of grocery market share per Kantar—forcing high trade spend, slotting fees and promotional support to secure visibility. Delist risk in mature categories raises margin pressure, and buyer power peaks where channel concentration is greatest.

E-commerce and marketplace dynamics

Online platforms increase price transparency and comparison shopping, with marketplaces typically accounting for 20%+ of CPG online sales and commission rates commonly around 15–20%, squeezing manufacturer margins.

Platforms demand fees, data sharing and rapid fulfillment standards—Amazon reported 2024 Prime delivery and seller performance KPIs tightening lead times and penalties.

Direct-to-consumer reduces reliance but raises marketing spend and logistics costs; overall digital channels shift bargaining power toward platforms and consumers.

Private label alternatives

Retailers aggressively expand private labels in commoditized cleaners and wipes, with Western Europe private-label penetration near 39% value in 2024, anchoring lower price points and eroding premium tiers. Private labels often undercut branded prices by 20–40%, forcing Reckitt to defend share through faster innovation and sustained brand equity investments. Buyer power increases when store brands reach “good enough” quality, prompting trade promotions and selective premiumization by Reckitt to protect margins.

Brand loyalty in health and hygiene

Trusted OTC, disinfectant and infant nutrition brands (eg Dettol, Nurofen, Enfamil) reduce price elasticity and dampen switching despite promotions; in 2024 Reckitt reported c.£13.0bn revenue with health & hygiene driving the majority of sales, so brand trust tempers retailer leverage in critical need-states and moderates buyer power.

- Brand trust reduces elasticity

- Perceived safety limits switching

- Retailer leverage constrained in need-states

Promotional intensity and trade terms

Frequent promotions train consumers to wait for deals, shifting purchasing power toward retailers and amplifying customer bargaining power for Reckitt Benckiser. Retailers routinely negotiate funding for features, end-caps and prominent online placement, increasing trade spend and promotional dependency. Over-reliance on such tactics can compress gross margins, forcing stricter revenue management to protect profitability.

- Promotions drive purchase timing pressure

- Retailer funding demands increase trade spend

- Margin compression risk from heavy promotions

- Requires disciplined revenue management

Retail concentration, marketplaces and private labels squeeze CPG margins

Large concentrated retailers (Walmart ~25% US grocery 2024; UK Big Four ~68% share) and marketplaces (~20%+ CPG online sales; 15–20% commissions) exert strong pricing/shelf leverage, driving high trade spend and margin pressure. Private label penetration (Western Europe ~39% value 2024) and promotions compress prices, though Reckitt’s c.£13.0bn 2024 revenue and strong brands temper switching.

| Metric | 2024 |

|---|---|

| Walmart US grocery | ~25% |

| UK Big Four | ~68% |

| Private label WE | ~39% value |

| Reckitt revenue | c.£13.0bn |

Preview the Actual Deliverable

Reckitt Benckiser Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of Reckitt Benckiser Group provides a clear assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with actionable implications for strategy and valuation. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use instantly after purchase.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Reckitt Benckiser faces intense rivalry in fast-moving consumer goods, with strong brands and scale reducing buyer power and raising switching costs; supplier power is moderate due to diversified global sourcing, while regulatory barriers and scale keep new entrants at bay and substitutes (private labels, niche innovators) a steady threat. This preview is just the starting point. Dive into a complete, consultant-grade breakdown of Reckitt Benckiser Group’s industry competitiveness—ready for immediate use.

Suppliers Bargaining Power

Diversified raw material base

Reckitt sources chemicals, APIs, fragrances and packaging from a broad global pool, limiting single-supplier leverage and supporting its £12.5bn 2024 revenue base.

Multi-sourcing and dual qualification across categories reduce switching risk and supply disruption exposure, while logistics and regional hubs spread procurement geographically.

Specialized actives and pharma-grade inputs in health can narrow options, so supplier power is moderate and varies by input criticality.

Regulated and specialized inputs

Regulated OTC medicines and infant nutrition require GMP-certified, audited suppliers, raising switching costs and favoring long-term contracts; the global infant formula market was estimated at about USD 70 billion in 2024, concentrating demand on qualified dairy-protein suppliers. Strict quality, traceability and auditability concentrate supply, increasing vendor influence and price-setting power. Disruptions in specialized excipients or dairy proteins can halt production, strengthening supplier power in these tightly regulated lines.

Packaging and logistics volatility

Packaging inputs such as resins, aluminum, glass and corrugate move with energy and commodity cycles, and freight/logistics shocks can amplify supplier bargaining power during tight markets; container rates that surged over 200% versus pre‑pandemic peaks in 2021–22 had largely eased by 2024, reducing but not eliminating pressure. Long‑term contracts and hedging partially mitigate volatility, yet bargaining power shifts cyclically and spikes sharply in periods of scarcity.

Scale and procurement leverage

Reckitt’s global scale (2024 net revenue ~£13.0bn) secures volume discounts and more favorable supplier terms, shifting pricing power toward the buyer. Centralized procurement and category management concentrate spend and enhance negotiating clout across categories. Vendor performance programs and supplier relationship management raised reliability and reduced cost for non-specialty inputs.

- Scale: global spend consolidation

- Procurement: centralized category teams

- SRM: vendor KPIs/improved reliability

- Power: favors Reckitt on non-specialty goods

Sustainability and compliance demands

Sustainability and stricter ESG, recyclability and responsible sourcing standards in 2024 have narrowed Reckitt's supplier pool, raising verification and traceability needs.

Compliance-related costs—notably audit and certification spend—are increasingly passed to buyers; Reckitt's FY 2024 revenue was £12.1bn, highlighting material margin sensitivity.

Strategic supplier partnerships secure innovation and supply assurance but can lock pricing and terms, modestly elevating supplier influence.

- ESG-driven supplier narrowing

- Compliance cost pass-through

- Partnerships = security vs. flexibility

- Moderate increase in supplier power

Moderate supplier power: specialized pharma and infant-nutrition increase leverage despite scale

Reckitt faces moderate supplier power: broad multi‑sourcing and centralized procurement favor the buyer, but specialized pharma actives, GMP suppliers and ESG vetting concentrate supply for critical lines.

Infant‑nutrition and regulated OTC inputs and audit costs raise switching costs; partnerships secure supply but can lock terms.

Scale (FY2024 revenue £12.1bn) and SRM mitigate but do not eliminate cyclical supplier leverage.

| Metric | 2024 |

|---|---|

| Revenue | £12.1bn |

| Infant formula market | USD70bn |

| Container rate peak vs pre‑pandemic | +200% (2021–22) |

What is included in the product

Tailored Porter's Five Forces analysis for Reckitt Benckiser Group, uncovering competitive intensity, buyer and supplier power, substitute threats, and barriers protecting incumbents, with strategic implications for pricing and market share.

A clear one-sheet summary of all five forces for Reckitt Benckiser—customizable pressure levels and instant spider/radar chart visualization to relieve strategic uncertainty and slot directly into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated retail channels

Large retailers and wholesalers exert material shelf and pricing power—Walmart accounted for about 25% of US grocery sales in 2024 and the UK Big Four held roughly 68% of grocery market share per Kantar—forcing high trade spend, slotting fees and promotional support to secure visibility. Delist risk in mature categories raises margin pressure, and buyer power peaks where channel concentration is greatest.

E-commerce and marketplace dynamics

Online platforms increase price transparency and comparison shopping, with marketplaces typically accounting for 20%+ of CPG online sales and commission rates commonly around 15–20%, squeezing manufacturer margins.

Platforms demand fees, data sharing and rapid fulfillment standards—Amazon reported 2024 Prime delivery and seller performance KPIs tightening lead times and penalties.

Direct-to-consumer reduces reliance but raises marketing spend and logistics costs; overall digital channels shift bargaining power toward platforms and consumers.

Private label alternatives

Retailers aggressively expand private labels in commoditized cleaners and wipes, with Western Europe private-label penetration near 39% value in 2024, anchoring lower price points and eroding premium tiers. Private labels often undercut branded prices by 20–40%, forcing Reckitt to defend share through faster innovation and sustained brand equity investments. Buyer power increases when store brands reach “good enough” quality, prompting trade promotions and selective premiumization by Reckitt to protect margins.

Brand loyalty in health and hygiene

Trusted OTC, disinfectant and infant nutrition brands (eg Dettol, Nurofen, Enfamil) reduce price elasticity and dampen switching despite promotions; in 2024 Reckitt reported c.£13.0bn revenue with health & hygiene driving the majority of sales, so brand trust tempers retailer leverage in critical need-states and moderates buyer power.

- Brand trust reduces elasticity

- Perceived safety limits switching

- Retailer leverage constrained in need-states

Promotional intensity and trade terms

Frequent promotions train consumers to wait for deals, shifting purchasing power toward retailers and amplifying customer bargaining power for Reckitt Benckiser. Retailers routinely negotiate funding for features, end-caps and prominent online placement, increasing trade spend and promotional dependency. Over-reliance on such tactics can compress gross margins, forcing stricter revenue management to protect profitability.

- Promotions drive purchase timing pressure

- Retailer funding demands increase trade spend

- Margin compression risk from heavy promotions

- Requires disciplined revenue management

Retail concentration, marketplaces and private labels squeeze CPG margins

Large concentrated retailers (Walmart ~25% US grocery 2024; UK Big Four ~68% share) and marketplaces (~20%+ CPG online sales; 15–20% commissions) exert strong pricing/shelf leverage, driving high trade spend and margin pressure. Private label penetration (Western Europe ~39% value 2024) and promotions compress prices, though Reckitt’s c.£13.0bn 2024 revenue and strong brands temper switching.

| Metric | 2024 |

|---|---|

| Walmart US grocery | ~25% |

| UK Big Four | ~68% |

| Private label WE | ~39% value |

| Reckitt revenue | c.£13.0bn |

Preview the Actual Deliverable

Reckitt Benckiser Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of Reckitt Benckiser Group provides a clear assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with actionable implications for strategy and valuation. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use instantly after purchase.