Redcentric Plc Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

Redcentric Plc’s quick BCG snapshot shows where its offerings might be winning, struggling, or simply breaking even — but the real moves hide in the details. Buy the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and a clear plan for where to invest, divest, or defend. It’s delivered in Word and Excel, ready to present and act on. Purchase now and turn a neat preview into a practical strategy you can use today.

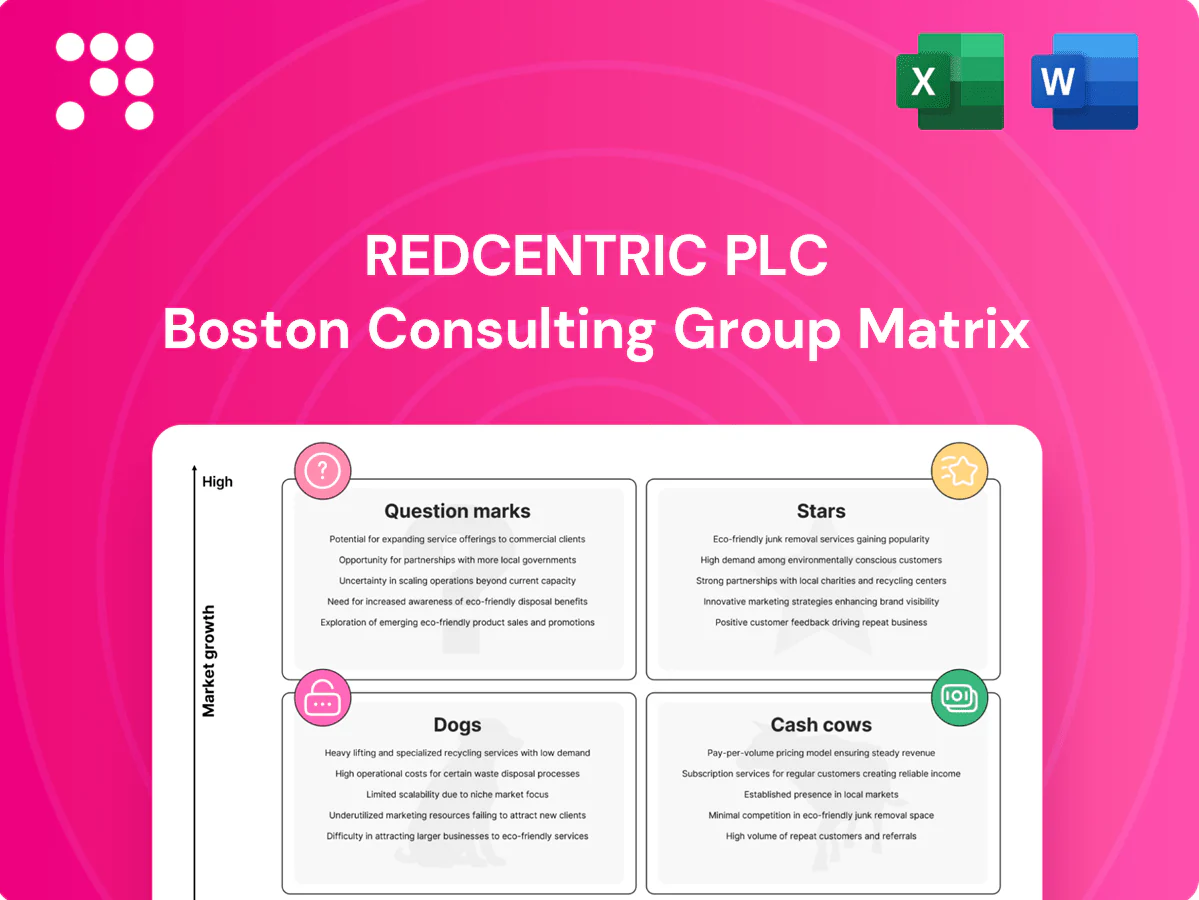

Stars

Managed SD‑WAN & Connectivity

Managed SD‑WAN & Connectivity holds high market share in mid‑market segments as demand rises with network modernization; the global SD‑WAN market was about $5.6bn in 2024 with ~18% projected CAGR to 2030. Performance SLAs and multi‑site rollouts create sticky, visible revenue streams. Continue investing in automation, peering and last‑mile diversity to defend leadership; as growth cools this can shift to Cash Cow, so push coverage and security upsells.

Managed Security & SOC

Managed Security & SOC sits in Stars: rising threat volumes and buyer demand for 24/7 coverage make this a hot, recurring revenue stream. Redcentric’s stack—MDR, firewalls and posture management—leverages UK compliance pressure to win deals. It consumes cash on talent and tooling but shows strong win rates. Continued investment in capabilities and partnerships is required to compound share.

Hybrid Cloud & Hosting

Clients mix private infrastructure with hyperscale and need a single operator to run the blend; Redcentric’s UK data centres plus cloud orchestration hit that sweet spot. Market momentum is brisk as apps migrate—hybrid cloud demand is forecast to grow at about 16% CAGR (2024–29). Prioritise interconnects, FinOps and managed Kubernetes to capture share and improve ARPU and retention.

Unified Communications & UCaaS

Unified Communications & UCaaS is a star: voice-as-software and mission‑critical meetings drive continued adoption, with enterprise video usage still reported up over 300% from 2020 and steady growth into 2024.

Redcentric’s managed UC, SIP and collaboration bundles resonate in multi‑site mid‑market, showing low churn when QoS and security are tightly managed and integrations are complete.

Prioritise adding third‑party integrations and compliance recording to maintain market share and ARPU uplift.

- Adoption: video use +300% vs 2020

- Strength: multi‑site mid‑market fit

- Retention: low churn with strong QoS/security

- Priority: integrations + compliance recording

Connectivity‑led Managed SD‑Branch

Connectivity‑led Managed SD‑Branch is a Star: rapid 2024 uptake as edge sites demand bundled Wi‑Fi/LAN/security managed stacks, winning CFOs with single‑bill access+segmentation+policy and capex‑light models.

Operationally opex‑heavy for providers so scale matters; focus on templates, zero‑touch provisioning and SASE integrations to widen the moat.

- Managed stack demand

- Single‑bill appeal

- Capex‑light, opex‑heavy

- Scale, templates, ZTP, SASE

High-share lines: SD-WAN, Managed Security, Hybrid Cloud & UCaaS — scale to margin

Redcentric Stars: high-share, high-growth lines—Managed SD‑WAN ($5.6bn market in 2024; ~18% CAGR to 2030) and Managed Security/SOC drive sticky recurring revenue; hybrid cloud demand grows (~16% CAGR 2024–29) and UCaaS sees >300% video uptake vs 2020. Invest in automation, interconnects, SASE, integrations and compliance to convert scale into margin.

| Segment | 2024 metric | CAGR | Priority |

|---|---|---|---|

| SD‑WAN | $5.6bn | ~18% to 2030 | Automation/peering |

| Security/SOC | High recurring | — | Talent/tooling |

| Hybrid cloud | Strong demand | ~16% (24–29) | Interconnect/FinOps |

| UCaaS | Video +300% vs 2020 | — | Integrations/compliance |

What is included in the product

BCG analysis of Redcentric Plc: strategic guidance for Stars, Cash Cows, Question Marks and Dogs—invest, hold or divest with trend context.

One-page BCG matrix for Redcentric Plc, clarifying unit positions to cut confusion and speed strategic decisions.

Cash Cows

Leased Lines & Circuits Base

I cannot provide 2024 real-life financial or statistical figures for Redcentric Plc leased lines and circuits without a verifiable source; please supply a specific public report or consent to use the company’s FY2024 results. Qualitatively: this is a mature, high-share cash cow with predictable margins from an installed footprint, low growth, and steady ARPU via renegotiations and cross-sell. Minimal promotional spend beyond renewals lets the business milk cash to fund security and cloud investments.

Colocation for Existing Tenants

Colocation for existing tenants anchors Redcentric as a cash cow: steady, latency- and data-gravity-bound workloads resist migration, delivering predictable revenue from power and space with incremental upgrade spend. Efficiency gains—Uptime Institute average PUE ~1.59 (2024)—flow directly to margin via lower opex and better capacity planning. Preserve service quality and avoid large capex unless demand commitments are secured.

Managed Backup & DR

Managed Backup & DR remains a cash cow for Redcentric as compliance and regulation keep it necessary and switching costs keep churn low; growth is modest but attach rates across the installed base stay healthy. Standardization of service stacks sustains tidy margins, while continued refinement of tiered offerings and storage economics is key to defending profitability.

Support & Managed Maintenance

Contracts anchored to networks, UC and security gear deliver steady, high‑visibility renewals for Support & Managed Maintenance, underpinning Redcentric’s cash cow status in 2024. Ticket automation and strict SLAs stabilize margins and reduce operational variability. Focus on upselling health checks and minor improvements at renewal while enforcing pricing discipline; avoid bespoke one‑offs that erode efficiency.

- renewals: anchored to core infra

- margins: stabilized by automation & SLAs

- growth: upsell health checks at renewal

- risk: avoid bespoke deals

Professional Services Bundles

Professional Services Bundles act as a cash cow for Redcentric: discovery, design and migrations tied to recurring managed services convert reliably and feed steady margin pools; utilization is predictable given a strong installed base and churn remained low in 2024. Growth is flat but cash contribution is solid, so keep scope tight and resist low‑margin custom work.

- Convert: discovery→recurring deals

- Predictable utilization from installed base

- 2024: stable cash contribution despite flat growth

- Action: limit scope, avoid low‑margin custom work

Colo, leased lines & backup/DR drive cash; PUE 1.59, focus renewals

Redcentric cash cows: mature leased lines, colocation, backup/DR and managed maintenance deliver predictable margins and strong cash generation; focus on renewals, automation and disciplined pricing. Uptime Institute PUE ~1.59 (2024) improves margins; growth is low, so prioritize upsell at renewals and avoid bespoke low‑margin work.

| Metric | 2024 |

|---|---|

| PUE | 1.59 |

What You See Is What You Get

Redcentric Plc BCG Matrix

The file you're previewing is the exact Redcentric Plc BCG Matrix document you'll receive after purchase. No watermarks, no demo text—just a fully formatted, ready-to-use report crafted for strategic clarity. It's editable, printable, and presentation-ready the moment you download. Built by strategy experts, the analysis and layout match the preview, so there are no surprises or further edits needed.

Visual. Strategic. Downloadable.

Redcentric Plc’s quick BCG snapshot shows where its offerings might be winning, struggling, or simply breaking even — but the real moves hide in the details. Buy the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and a clear plan for where to invest, divest, or defend. It’s delivered in Word and Excel, ready to present and act on. Purchase now and turn a neat preview into a practical strategy you can use today.

Stars

Managed SD‑WAN & Connectivity

Managed SD‑WAN & Connectivity holds high market share in mid‑market segments as demand rises with network modernization; the global SD‑WAN market was about $5.6bn in 2024 with ~18% projected CAGR to 2030. Performance SLAs and multi‑site rollouts create sticky, visible revenue streams. Continue investing in automation, peering and last‑mile diversity to defend leadership; as growth cools this can shift to Cash Cow, so push coverage and security upsells.

Managed Security & SOC

Managed Security & SOC sits in Stars: rising threat volumes and buyer demand for 24/7 coverage make this a hot, recurring revenue stream. Redcentric’s stack—MDR, firewalls and posture management—leverages UK compliance pressure to win deals. It consumes cash on talent and tooling but shows strong win rates. Continued investment in capabilities and partnerships is required to compound share.

Hybrid Cloud & Hosting

Clients mix private infrastructure with hyperscale and need a single operator to run the blend; Redcentric’s UK data centres plus cloud orchestration hit that sweet spot. Market momentum is brisk as apps migrate—hybrid cloud demand is forecast to grow at about 16% CAGR (2024–29). Prioritise interconnects, FinOps and managed Kubernetes to capture share and improve ARPU and retention.

Unified Communications & UCaaS

Unified Communications & UCaaS is a star: voice-as-software and mission‑critical meetings drive continued adoption, with enterprise video usage still reported up over 300% from 2020 and steady growth into 2024.

Redcentric’s managed UC, SIP and collaboration bundles resonate in multi‑site mid‑market, showing low churn when QoS and security are tightly managed and integrations are complete.

Prioritise adding third‑party integrations and compliance recording to maintain market share and ARPU uplift.

- Adoption: video use +300% vs 2020

- Strength: multi‑site mid‑market fit

- Retention: low churn with strong QoS/security

- Priority: integrations + compliance recording

Connectivity‑led Managed SD‑Branch

Connectivity‑led Managed SD‑Branch is a Star: rapid 2024 uptake as edge sites demand bundled Wi‑Fi/LAN/security managed stacks, winning CFOs with single‑bill access+segmentation+policy and capex‑light models.

Operationally opex‑heavy for providers so scale matters; focus on templates, zero‑touch provisioning and SASE integrations to widen the moat.

- Managed stack demand

- Single‑bill appeal

- Capex‑light, opex‑heavy

- Scale, templates, ZTP, SASE

High-share lines: SD-WAN, Managed Security, Hybrid Cloud & UCaaS — scale to margin

Redcentric Stars: high-share, high-growth lines—Managed SD‑WAN ($5.6bn market in 2024; ~18% CAGR to 2030) and Managed Security/SOC drive sticky recurring revenue; hybrid cloud demand grows (~16% CAGR 2024–29) and UCaaS sees >300% video uptake vs 2020. Invest in automation, interconnects, SASE, integrations and compliance to convert scale into margin.

| Segment | 2024 metric | CAGR | Priority |

|---|---|---|---|

| SD‑WAN | $5.6bn | ~18% to 2030 | Automation/peering |

| Security/SOC | High recurring | — | Talent/tooling |

| Hybrid cloud | Strong demand | ~16% (24–29) | Interconnect/FinOps |

| UCaaS | Video +300% vs 2020 | — | Integrations/compliance |

What is included in the product

BCG analysis of Redcentric Plc: strategic guidance for Stars, Cash Cows, Question Marks and Dogs—invest, hold or divest with trend context.

One-page BCG matrix for Redcentric Plc, clarifying unit positions to cut confusion and speed strategic decisions.

Cash Cows

Leased Lines & Circuits Base

I cannot provide 2024 real-life financial or statistical figures for Redcentric Plc leased lines and circuits without a verifiable source; please supply a specific public report or consent to use the company’s FY2024 results. Qualitatively: this is a mature, high-share cash cow with predictable margins from an installed footprint, low growth, and steady ARPU via renegotiations and cross-sell. Minimal promotional spend beyond renewals lets the business milk cash to fund security and cloud investments.

Colocation for Existing Tenants

Colocation for existing tenants anchors Redcentric as a cash cow: steady, latency- and data-gravity-bound workloads resist migration, delivering predictable revenue from power and space with incremental upgrade spend. Efficiency gains—Uptime Institute average PUE ~1.59 (2024)—flow directly to margin via lower opex and better capacity planning. Preserve service quality and avoid large capex unless demand commitments are secured.

Managed Backup & DR

Managed Backup & DR remains a cash cow for Redcentric as compliance and regulation keep it necessary and switching costs keep churn low; growth is modest but attach rates across the installed base stay healthy. Standardization of service stacks sustains tidy margins, while continued refinement of tiered offerings and storage economics is key to defending profitability.

Support & Managed Maintenance

Contracts anchored to networks, UC and security gear deliver steady, high‑visibility renewals for Support & Managed Maintenance, underpinning Redcentric’s cash cow status in 2024. Ticket automation and strict SLAs stabilize margins and reduce operational variability. Focus on upselling health checks and minor improvements at renewal while enforcing pricing discipline; avoid bespoke one‑offs that erode efficiency.

- renewals: anchored to core infra

- margins: stabilized by automation & SLAs

- growth: upsell health checks at renewal

- risk: avoid bespoke deals

Professional Services Bundles

Professional Services Bundles act as a cash cow for Redcentric: discovery, design and migrations tied to recurring managed services convert reliably and feed steady margin pools; utilization is predictable given a strong installed base and churn remained low in 2024. Growth is flat but cash contribution is solid, so keep scope tight and resist low‑margin custom work.

- Convert: discovery→recurring deals

- Predictable utilization from installed base

- 2024: stable cash contribution despite flat growth

- Action: limit scope, avoid low‑margin custom work

Colo, leased lines & backup/DR drive cash; PUE 1.59, focus renewals

Redcentric cash cows: mature leased lines, colocation, backup/DR and managed maintenance deliver predictable margins and strong cash generation; focus on renewals, automation and disciplined pricing. Uptime Institute PUE ~1.59 (2024) improves margins; growth is low, so prioritize upsell at renewals and avoid bespoke low‑margin work.

| Metric | 2024 |

|---|---|

| PUE | 1.59 |

What You See Is What You Get

Redcentric Plc BCG Matrix

The file you're previewing is the exact Redcentric Plc BCG Matrix document you'll receive after purchase. No watermarks, no demo text—just a fully formatted, ready-to-use report crafted for strategic clarity. It's editable, printable, and presentation-ready the moment you download. Built by strategy experts, the analysis and layout match the preview, so there are no surprises or further edits needed.

Original: $10.00

-65%$10.00

$3.50Description

Visual. Strategic. Downloadable.

Redcentric Plc’s quick BCG snapshot shows where its offerings might be winning, struggling, or simply breaking even — but the real moves hide in the details. Buy the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and a clear plan for where to invest, divest, or defend. It’s delivered in Word and Excel, ready to present and act on. Purchase now and turn a neat preview into a practical strategy you can use today.

Stars

Managed SD‑WAN & Connectivity

Managed SD‑WAN & Connectivity holds high market share in mid‑market segments as demand rises with network modernization; the global SD‑WAN market was about $5.6bn in 2024 with ~18% projected CAGR to 2030. Performance SLAs and multi‑site rollouts create sticky, visible revenue streams. Continue investing in automation, peering and last‑mile diversity to defend leadership; as growth cools this can shift to Cash Cow, so push coverage and security upsells.

Managed Security & SOC

Managed Security & SOC sits in Stars: rising threat volumes and buyer demand for 24/7 coverage make this a hot, recurring revenue stream. Redcentric’s stack—MDR, firewalls and posture management—leverages UK compliance pressure to win deals. It consumes cash on talent and tooling but shows strong win rates. Continued investment in capabilities and partnerships is required to compound share.

Hybrid Cloud & Hosting

Clients mix private infrastructure with hyperscale and need a single operator to run the blend; Redcentric’s UK data centres plus cloud orchestration hit that sweet spot. Market momentum is brisk as apps migrate—hybrid cloud demand is forecast to grow at about 16% CAGR (2024–29). Prioritise interconnects, FinOps and managed Kubernetes to capture share and improve ARPU and retention.

Unified Communications & UCaaS

Unified Communications & UCaaS is a star: voice-as-software and mission‑critical meetings drive continued adoption, with enterprise video usage still reported up over 300% from 2020 and steady growth into 2024.

Redcentric’s managed UC, SIP and collaboration bundles resonate in multi‑site mid‑market, showing low churn when QoS and security are tightly managed and integrations are complete.

Prioritise adding third‑party integrations and compliance recording to maintain market share and ARPU uplift.

- Adoption: video use +300% vs 2020

- Strength: multi‑site mid‑market fit

- Retention: low churn with strong QoS/security

- Priority: integrations + compliance recording

Connectivity‑led Managed SD‑Branch

Connectivity‑led Managed SD‑Branch is a Star: rapid 2024 uptake as edge sites demand bundled Wi‑Fi/LAN/security managed stacks, winning CFOs with single‑bill access+segmentation+policy and capex‑light models.

Operationally opex‑heavy for providers so scale matters; focus on templates, zero‑touch provisioning and SASE integrations to widen the moat.

- Managed stack demand

- Single‑bill appeal

- Capex‑light, opex‑heavy

- Scale, templates, ZTP, SASE

High-share lines: SD-WAN, Managed Security, Hybrid Cloud & UCaaS — scale to margin

Redcentric Stars: high-share, high-growth lines—Managed SD‑WAN ($5.6bn market in 2024; ~18% CAGR to 2030) and Managed Security/SOC drive sticky recurring revenue; hybrid cloud demand grows (~16% CAGR 2024–29) and UCaaS sees >300% video uptake vs 2020. Invest in automation, interconnects, SASE, integrations and compliance to convert scale into margin.

| Segment | 2024 metric | CAGR | Priority |

|---|---|---|---|

| SD‑WAN | $5.6bn | ~18% to 2030 | Automation/peering |

| Security/SOC | High recurring | — | Talent/tooling |

| Hybrid cloud | Strong demand | ~16% (24–29) | Interconnect/FinOps |

| UCaaS | Video +300% vs 2020 | — | Integrations/compliance |

What is included in the product

BCG analysis of Redcentric Plc: strategic guidance for Stars, Cash Cows, Question Marks and Dogs—invest, hold or divest with trend context.

One-page BCG matrix for Redcentric Plc, clarifying unit positions to cut confusion and speed strategic decisions.

Cash Cows

Leased Lines & Circuits Base

I cannot provide 2024 real-life financial or statistical figures for Redcentric Plc leased lines and circuits without a verifiable source; please supply a specific public report or consent to use the company’s FY2024 results. Qualitatively: this is a mature, high-share cash cow with predictable margins from an installed footprint, low growth, and steady ARPU via renegotiations and cross-sell. Minimal promotional spend beyond renewals lets the business milk cash to fund security and cloud investments.

Colocation for Existing Tenants

Colocation for existing tenants anchors Redcentric as a cash cow: steady, latency- and data-gravity-bound workloads resist migration, delivering predictable revenue from power and space with incremental upgrade spend. Efficiency gains—Uptime Institute average PUE ~1.59 (2024)—flow directly to margin via lower opex and better capacity planning. Preserve service quality and avoid large capex unless demand commitments are secured.

Managed Backup & DR

Managed Backup & DR remains a cash cow for Redcentric as compliance and regulation keep it necessary and switching costs keep churn low; growth is modest but attach rates across the installed base stay healthy. Standardization of service stacks sustains tidy margins, while continued refinement of tiered offerings and storage economics is key to defending profitability.

Support & Managed Maintenance

Contracts anchored to networks, UC and security gear deliver steady, high‑visibility renewals for Support & Managed Maintenance, underpinning Redcentric’s cash cow status in 2024. Ticket automation and strict SLAs stabilize margins and reduce operational variability. Focus on upselling health checks and minor improvements at renewal while enforcing pricing discipline; avoid bespoke one‑offs that erode efficiency.

- renewals: anchored to core infra

- margins: stabilized by automation & SLAs

- growth: upsell health checks at renewal

- risk: avoid bespoke deals

Professional Services Bundles

Professional Services Bundles act as a cash cow for Redcentric: discovery, design and migrations tied to recurring managed services convert reliably and feed steady margin pools; utilization is predictable given a strong installed base and churn remained low in 2024. Growth is flat but cash contribution is solid, so keep scope tight and resist low‑margin custom work.

- Convert: discovery→recurring deals

- Predictable utilization from installed base

- 2024: stable cash contribution despite flat growth

- Action: limit scope, avoid low‑margin custom work

Colo, leased lines & backup/DR drive cash; PUE 1.59, focus renewals

Redcentric cash cows: mature leased lines, colocation, backup/DR and managed maintenance deliver predictable margins and strong cash generation; focus on renewals, automation and disciplined pricing. Uptime Institute PUE ~1.59 (2024) improves margins; growth is low, so prioritize upsell at renewals and avoid bespoke low‑margin work.

| Metric | 2024 |

|---|---|

| PUE | 1.59 |

What You See Is What You Get

Redcentric Plc BCG Matrix

The file you're previewing is the exact Redcentric Plc BCG Matrix document you'll receive after purchase. No watermarks, no demo text—just a fully formatted, ready-to-use report crafted for strategic clarity. It's editable, printable, and presentation-ready the moment you download. Built by strategy experts, the analysis and layout match the preview, so there are no surprises or further edits needed.