Red Robin Gourmet Burgers Porter's Five Forces Analysis

Don't Miss the Bigger Picture

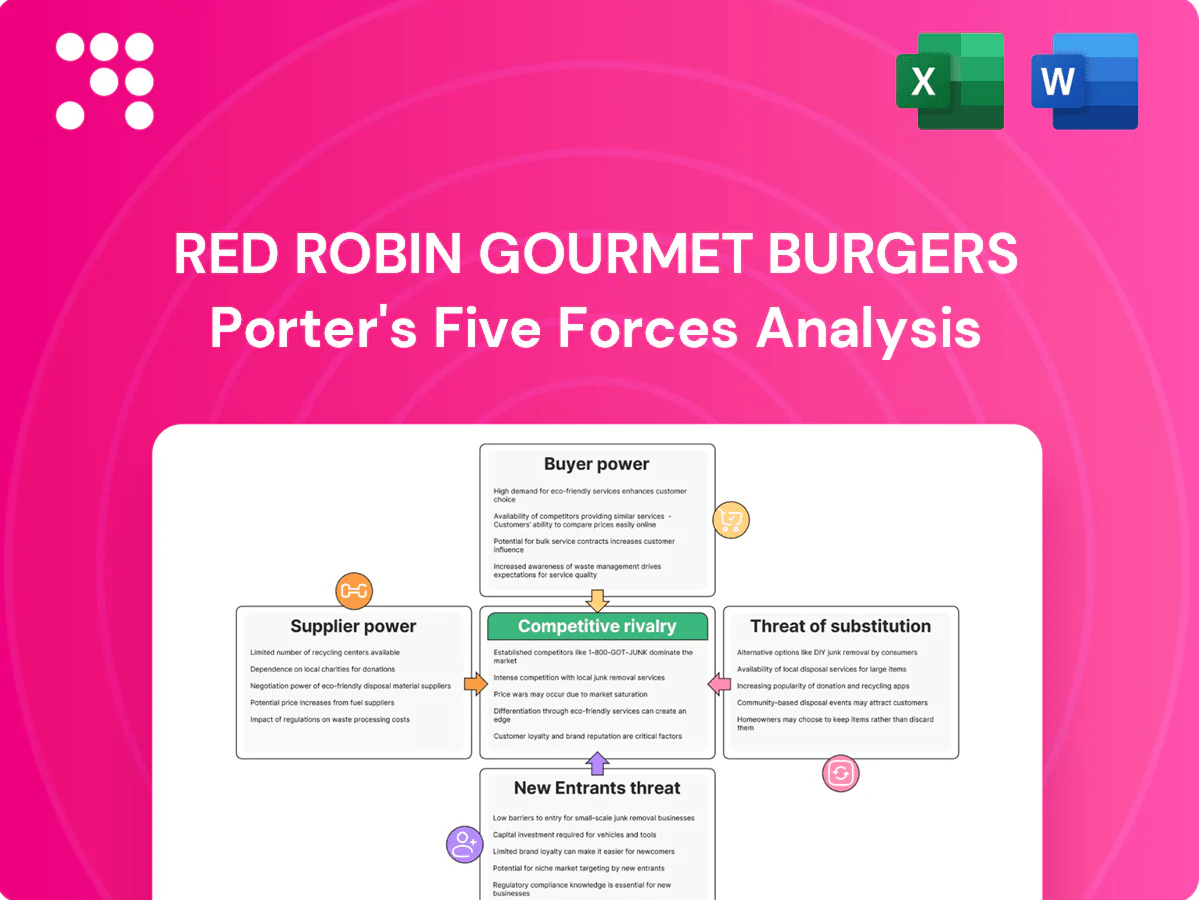

Red Robin faces intense rivalry from casual dining peers, moderate supplier leverage, growing buyer price sensitivity, and mounting threat from fast-casual substitutes and delivery platforms. Labor costs and real estate shape barriers to entry. This snapshot highlights key pressures on margins and growth. Unlock the full Porter's Five Forces Analysis to explore Red Robin Gourmet Burgers’s competitive dynamics in detail.

Suppliers Bargaining Power

Supplier Power 1

Red Robin depends on large volumes of beef, potatoes, wheat, dairy and frying oil, leaving it exposed to commodity swings; U.S. beef futures moved roughly 15% in 2024, amplifying cost risk.

Commodity volatility can compress margins quickly if menu pricing lags—food & beverage costs historically drive ~30%+ of casual-dining costs and spikes hit margins fast.

Hedging and fixed-supply contracts mitigate but rarely eliminate exposure; heavy menu reliance on burgers and fries concentrates vulnerability to a few inputs.

Supplier Power 2

National distributors provide scale and coverage for Red Robin but wield negotiating leverage on pricing, slotting and fees. Sysco and US Foods together account for roughly 50% of US foodservice broadline distribution (2024), increasing supplier concentration and bargaining power. Switching distributors is feasible but disruptive due to logistics, specs and franchise alignment, and multi-year agreements limit short-term flexibility.

Supplier Power 3

Beverage agreements with dominant suppliers (Coca-Cola and PepsiCo account for roughly 70% of the US nonalcoholic beverage market in 2024) can be exclusive, limiting menu choice while delivering rebates and marketing funds. Exclusive fountain and equipment deals create moderate supplier power via lock-in, with contracts often tied to equipment, marketing support and fountain rights. Renegotiation cycles, commonly every 3–5 years, can materially reset economics.

Supplier Power 4

Spec-driven items like proprietary buns, sauces and seasonings lower supplier substitutability and raise switching costs; with four firms controlling about 85% of US beef processing (USDA 2023) ingredient concentration increases stock-out risk. Quality consistency is critical to Red Robin’s brand, strengthening select suppliers; dual-sourcing reduces risk but adds cost and operational complexity.

- Spec items → low substitutability

- 4 firms ≈85% beef capacity (USDA 2023)

- Dual-sourcing cuts risk, raises cost

Supplier Power 5

Supplier Power 5: Regional weather, disease and logistics shocks in 2023–24 tightened protein and produce availability, lifting input prices; trucking driver shortage (~80,000 short in 2024 per industry estimates) and processor labor gaps pushed costs higher. ESG and animal-welfare specs narrowed vetted vendors, modestly increasing supplier leverage, while franchised units’ mandatory approved-supplier policies limit local alternatives.

- Trucking shortage ~80,000 (2024)

- Franchise sourcing restricts local buying

- ESG/welfare standards shrink vendor pool

- Regional shocks raise commodity inflation

Foodservice margins squeezed by concentrated suppliers, volatile beef and driver shortfall

Red Robin is exposed to concentrated commodity inputs (beef, potatoes, wheat, dairy); U.S. beef futures swung ~15% in 2024, pressuring margins. Broadline distributors (Sysco + US Foods ≈50% share, 2024) and beverage duopolies (Coca‑Cola + PepsiCo ≈70%, 2024) raise supplier leverage; 4 firms control ≈85% of beef processing (USDA 2023). Trucking shortfall ~80,000 drivers (2024) and ESG specs further tighten vendor options.

| Metric | Value |

|---|---|

| Beef futures 2024 | ≈15% swing |

| Broadline distro share | Sysco+US Foods ≈50% (2024) |

| Beverage share | Coca‑Cola+Pepsi ≈70% (2024) |

| Beef processing | 4 firms ≈85% (USDA 2023) |

| Trucking shortage | ≈80,000 drivers (2024) |

What is included in the product

Tailored Porter's Five Forces for Red Robin Gourmet Burgers uncovering competitive drivers, buyer/supplier power, substitutes, entry barriers and emerging threats to market share.

A concise Porter's Five Forces snapshot for Red Robin that clarifies competitive pain points and mitigation levers—slide-ready, customizable, and easy to update with new market data.

Customers Bargaining Power

Buyer Power 1

Customers face abundant casual-dining and burger alternatives, making switching costs near zero and elevating buyer leverage in 2024. High price sensitivity in a value-seeking market means small check inflation quickly shifts traffic to QSR or at-home options. Promotions, bundles and limited-time offers strongly influence choice and can rapidly recapture share. Loyalty programs and discounting compress margins for Red Robin.

Buyer Power 2

Delivery marketplaces aggregate Red Robin options and surface price comparisons, amplifying buyer power as DoorDash held about 60% US market share in 2024. High average delivery fees near $4.95 and commissions of 20–30% shift perceived value unless offset by discounts. Ratings and reviews can swing demand quickly—each one-star change correlates with ~5–9% revenue impact. Platform algorithms can redirect visibility with minimal friction, changing order flow overnight.

Buyer Power 3

Red Robin Royalty modestly reduces churn and raises visit frequency, with personalization and tiered rewards muting price sensitivity among enrolled guests. Points liabilities and member discount expectations, however, create ongoing margin pressure on check averages. Despite loyalty stickiness, aggregated buyer bargaining power remains moderate due to abundant casual-dining alternatives and price-conscious segments.

Buyer Power 4

- High sensitivity to wait times — quick switching to competitors

- Value-driven families expect consistent Bottomless service

- Over 400 locations (2024) increase local competition exposure

Buyer Power 5

Buyer Power 5: Corporate catering and large-party orders for Red Robin are highly price- and reliability-sensitive; US catering market ~63 billion in 2023–24, and such accounts can represent roughly 5–10% of a unit’s weekly sales, giving buyers leverage to negotiate better pricing or shift to competitors with superior logistics.

Order aggregation concentrates spend, magnifying unit-level cost pressure; a single service failure can trigger outsized revenue swings and contract loss across multiple locations.

- Price sensitivity: high

- Market size: ~63B (2023–24)

- Unit revenue exposure: ~5–10%

- Risk: service failures cause outsized swings

Delivery reliance (~60% share), fees and 20-30% commissions hit margins

Customers face near-zero switching amid 400+ US Red Robin locations (2024), high price sensitivity, and strong delivery-platform influence (DoorDash ~60% 2024). Delivery fees ~$4.95 and 20–30% commissions compress perceived value; one-star review shifts revenue ~5–9%. Loyalty reduces churn but increases margin pressure via discounts and points.

| Metric | Value |

|---|---|

| Locations (2024) | 400+ |

| DoorDash share (2024) | ~60% |

| Delivery fee | ~$4.95 |

| Commissions | 20–30% |

| Review impact | 5–9% rev/★ |

| Catering market | $63B (2023–24) |

Same Document Delivered

Red Robin Gourmet Burgers Porter's Five Forces Analysis

This Porter's Five Forces analysis of Red Robin Gourmet Burgers evaluates competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes to inform strategy and valuation. The preview is the exact, fully formatted document you'll receive instantly after purchase—no placeholders or samples. Use it immediately for decision-making or presentation-ready reporting.

Don't Miss the Bigger Picture

Red Robin faces intense rivalry from casual dining peers, moderate supplier leverage, growing buyer price sensitivity, and mounting threat from fast-casual substitutes and delivery platforms. Labor costs and real estate shape barriers to entry. This snapshot highlights key pressures on margins and growth. Unlock the full Porter's Five Forces Analysis to explore Red Robin Gourmet Burgers’s competitive dynamics in detail.

Suppliers Bargaining Power

Supplier Power 1

Red Robin depends on large volumes of beef, potatoes, wheat, dairy and frying oil, leaving it exposed to commodity swings; U.S. beef futures moved roughly 15% in 2024, amplifying cost risk.

Commodity volatility can compress margins quickly if menu pricing lags—food & beverage costs historically drive ~30%+ of casual-dining costs and spikes hit margins fast.

Hedging and fixed-supply contracts mitigate but rarely eliminate exposure; heavy menu reliance on burgers and fries concentrates vulnerability to a few inputs.

Supplier Power 2

National distributors provide scale and coverage for Red Robin but wield negotiating leverage on pricing, slotting and fees. Sysco and US Foods together account for roughly 50% of US foodservice broadline distribution (2024), increasing supplier concentration and bargaining power. Switching distributors is feasible but disruptive due to logistics, specs and franchise alignment, and multi-year agreements limit short-term flexibility.

Supplier Power 3

Beverage agreements with dominant suppliers (Coca-Cola and PepsiCo account for roughly 70% of the US nonalcoholic beverage market in 2024) can be exclusive, limiting menu choice while delivering rebates and marketing funds. Exclusive fountain and equipment deals create moderate supplier power via lock-in, with contracts often tied to equipment, marketing support and fountain rights. Renegotiation cycles, commonly every 3–5 years, can materially reset economics.

Supplier Power 4

Spec-driven items like proprietary buns, sauces and seasonings lower supplier substitutability and raise switching costs; with four firms controlling about 85% of US beef processing (USDA 2023) ingredient concentration increases stock-out risk. Quality consistency is critical to Red Robin’s brand, strengthening select suppliers; dual-sourcing reduces risk but adds cost and operational complexity.

- Spec items → low substitutability

- 4 firms ≈85% beef capacity (USDA 2023)

- Dual-sourcing cuts risk, raises cost

Supplier Power 5

Supplier Power 5: Regional weather, disease and logistics shocks in 2023–24 tightened protein and produce availability, lifting input prices; trucking driver shortage (~80,000 short in 2024 per industry estimates) and processor labor gaps pushed costs higher. ESG and animal-welfare specs narrowed vetted vendors, modestly increasing supplier leverage, while franchised units’ mandatory approved-supplier policies limit local alternatives.

- Trucking shortage ~80,000 (2024)

- Franchise sourcing restricts local buying

- ESG/welfare standards shrink vendor pool

- Regional shocks raise commodity inflation

Foodservice margins squeezed by concentrated suppliers, volatile beef and driver shortfall

Red Robin is exposed to concentrated commodity inputs (beef, potatoes, wheat, dairy); U.S. beef futures swung ~15% in 2024, pressuring margins. Broadline distributors (Sysco + US Foods ≈50% share, 2024) and beverage duopolies (Coca‑Cola + PepsiCo ≈70%, 2024) raise supplier leverage; 4 firms control ≈85% of beef processing (USDA 2023). Trucking shortfall ~80,000 drivers (2024) and ESG specs further tighten vendor options.

| Metric | Value |

|---|---|

| Beef futures 2024 | ≈15% swing |

| Broadline distro share | Sysco+US Foods ≈50% (2024) |

| Beverage share | Coca‑Cola+Pepsi ≈70% (2024) |

| Beef processing | 4 firms ≈85% (USDA 2023) |

| Trucking shortage | ≈80,000 drivers (2024) |

What is included in the product

Tailored Porter's Five Forces for Red Robin Gourmet Burgers uncovering competitive drivers, buyer/supplier power, substitutes, entry barriers and emerging threats to market share.

A concise Porter's Five Forces snapshot for Red Robin that clarifies competitive pain points and mitigation levers—slide-ready, customizable, and easy to update with new market data.

Customers Bargaining Power

Buyer Power 1

Customers face abundant casual-dining and burger alternatives, making switching costs near zero and elevating buyer leverage in 2024. High price sensitivity in a value-seeking market means small check inflation quickly shifts traffic to QSR or at-home options. Promotions, bundles and limited-time offers strongly influence choice and can rapidly recapture share. Loyalty programs and discounting compress margins for Red Robin.

Buyer Power 2

Delivery marketplaces aggregate Red Robin options and surface price comparisons, amplifying buyer power as DoorDash held about 60% US market share in 2024. High average delivery fees near $4.95 and commissions of 20–30% shift perceived value unless offset by discounts. Ratings and reviews can swing demand quickly—each one-star change correlates with ~5–9% revenue impact. Platform algorithms can redirect visibility with minimal friction, changing order flow overnight.

Buyer Power 3

Red Robin Royalty modestly reduces churn and raises visit frequency, with personalization and tiered rewards muting price sensitivity among enrolled guests. Points liabilities and member discount expectations, however, create ongoing margin pressure on check averages. Despite loyalty stickiness, aggregated buyer bargaining power remains moderate due to abundant casual-dining alternatives and price-conscious segments.

Buyer Power 4

- High sensitivity to wait times — quick switching to competitors

- Value-driven families expect consistent Bottomless service

- Over 400 locations (2024) increase local competition exposure

Buyer Power 5

Buyer Power 5: Corporate catering and large-party orders for Red Robin are highly price- and reliability-sensitive; US catering market ~63 billion in 2023–24, and such accounts can represent roughly 5–10% of a unit’s weekly sales, giving buyers leverage to negotiate better pricing or shift to competitors with superior logistics.

Order aggregation concentrates spend, magnifying unit-level cost pressure; a single service failure can trigger outsized revenue swings and contract loss across multiple locations.

- Price sensitivity: high

- Market size: ~63B (2023–24)

- Unit revenue exposure: ~5–10%

- Risk: service failures cause outsized swings

Delivery reliance (~60% share), fees and 20-30% commissions hit margins

Customers face near-zero switching amid 400+ US Red Robin locations (2024), high price sensitivity, and strong delivery-platform influence (DoorDash ~60% 2024). Delivery fees ~$4.95 and 20–30% commissions compress perceived value; one-star review shifts revenue ~5–9%. Loyalty reduces churn but increases margin pressure via discounts and points.

| Metric | Value |

|---|---|

| Locations (2024) | 400+ |

| DoorDash share (2024) | ~60% |

| Delivery fee | ~$4.95 |

| Commissions | 20–30% |

| Review impact | 5–9% rev/★ |

| Catering market | $63B (2023–24) |

Same Document Delivered

Red Robin Gourmet Burgers Porter's Five Forces Analysis

This Porter's Five Forces analysis of Red Robin Gourmet Burgers evaluates competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes to inform strategy and valuation. The preview is the exact, fully formatted document you'll receive instantly after purchase—no placeholders or samples. Use it immediately for decision-making or presentation-ready reporting.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Red Robin faces intense rivalry from casual dining peers, moderate supplier leverage, growing buyer price sensitivity, and mounting threat from fast-casual substitutes and delivery platforms. Labor costs and real estate shape barriers to entry. This snapshot highlights key pressures on margins and growth. Unlock the full Porter's Five Forces Analysis to explore Red Robin Gourmet Burgers’s competitive dynamics in detail.

Suppliers Bargaining Power

Supplier Power 1

Red Robin depends on large volumes of beef, potatoes, wheat, dairy and frying oil, leaving it exposed to commodity swings; U.S. beef futures moved roughly 15% in 2024, amplifying cost risk.

Commodity volatility can compress margins quickly if menu pricing lags—food & beverage costs historically drive ~30%+ of casual-dining costs and spikes hit margins fast.

Hedging and fixed-supply contracts mitigate but rarely eliminate exposure; heavy menu reliance on burgers and fries concentrates vulnerability to a few inputs.

Supplier Power 2

National distributors provide scale and coverage for Red Robin but wield negotiating leverage on pricing, slotting and fees. Sysco and US Foods together account for roughly 50% of US foodservice broadline distribution (2024), increasing supplier concentration and bargaining power. Switching distributors is feasible but disruptive due to logistics, specs and franchise alignment, and multi-year agreements limit short-term flexibility.

Supplier Power 3

Beverage agreements with dominant suppliers (Coca-Cola and PepsiCo account for roughly 70% of the US nonalcoholic beverage market in 2024) can be exclusive, limiting menu choice while delivering rebates and marketing funds. Exclusive fountain and equipment deals create moderate supplier power via lock-in, with contracts often tied to equipment, marketing support and fountain rights. Renegotiation cycles, commonly every 3–5 years, can materially reset economics.

Supplier Power 4

Spec-driven items like proprietary buns, sauces and seasonings lower supplier substitutability and raise switching costs; with four firms controlling about 85% of US beef processing (USDA 2023) ingredient concentration increases stock-out risk. Quality consistency is critical to Red Robin’s brand, strengthening select suppliers; dual-sourcing reduces risk but adds cost and operational complexity.

- Spec items → low substitutability

- 4 firms ≈85% beef capacity (USDA 2023)

- Dual-sourcing cuts risk, raises cost

Supplier Power 5

Supplier Power 5: Regional weather, disease and logistics shocks in 2023–24 tightened protein and produce availability, lifting input prices; trucking driver shortage (~80,000 short in 2024 per industry estimates) and processor labor gaps pushed costs higher. ESG and animal-welfare specs narrowed vetted vendors, modestly increasing supplier leverage, while franchised units’ mandatory approved-supplier policies limit local alternatives.

- Trucking shortage ~80,000 (2024)

- Franchise sourcing restricts local buying

- ESG/welfare standards shrink vendor pool

- Regional shocks raise commodity inflation

Foodservice margins squeezed by concentrated suppliers, volatile beef and driver shortfall

Red Robin is exposed to concentrated commodity inputs (beef, potatoes, wheat, dairy); U.S. beef futures swung ~15% in 2024, pressuring margins. Broadline distributors (Sysco + US Foods ≈50% share, 2024) and beverage duopolies (Coca‑Cola + PepsiCo ≈70%, 2024) raise supplier leverage; 4 firms control ≈85% of beef processing (USDA 2023). Trucking shortfall ~80,000 drivers (2024) and ESG specs further tighten vendor options.

| Metric | Value |

|---|---|

| Beef futures 2024 | ≈15% swing |

| Broadline distro share | Sysco+US Foods ≈50% (2024) |

| Beverage share | Coca‑Cola+Pepsi ≈70% (2024) |

| Beef processing | 4 firms ≈85% (USDA 2023) |

| Trucking shortage | ≈80,000 drivers (2024) |

What is included in the product

Tailored Porter's Five Forces for Red Robin Gourmet Burgers uncovering competitive drivers, buyer/supplier power, substitutes, entry barriers and emerging threats to market share.

A concise Porter's Five Forces snapshot for Red Robin that clarifies competitive pain points and mitigation levers—slide-ready, customizable, and easy to update with new market data.

Customers Bargaining Power

Buyer Power 1

Customers face abundant casual-dining and burger alternatives, making switching costs near zero and elevating buyer leverage in 2024. High price sensitivity in a value-seeking market means small check inflation quickly shifts traffic to QSR or at-home options. Promotions, bundles and limited-time offers strongly influence choice and can rapidly recapture share. Loyalty programs and discounting compress margins for Red Robin.

Buyer Power 2

Delivery marketplaces aggregate Red Robin options and surface price comparisons, amplifying buyer power as DoorDash held about 60% US market share in 2024. High average delivery fees near $4.95 and commissions of 20–30% shift perceived value unless offset by discounts. Ratings and reviews can swing demand quickly—each one-star change correlates with ~5–9% revenue impact. Platform algorithms can redirect visibility with minimal friction, changing order flow overnight.

Buyer Power 3

Red Robin Royalty modestly reduces churn and raises visit frequency, with personalization and tiered rewards muting price sensitivity among enrolled guests. Points liabilities and member discount expectations, however, create ongoing margin pressure on check averages. Despite loyalty stickiness, aggregated buyer bargaining power remains moderate due to abundant casual-dining alternatives and price-conscious segments.

Buyer Power 4

- High sensitivity to wait times — quick switching to competitors

- Value-driven families expect consistent Bottomless service

- Over 400 locations (2024) increase local competition exposure

Buyer Power 5

Buyer Power 5: Corporate catering and large-party orders for Red Robin are highly price- and reliability-sensitive; US catering market ~63 billion in 2023–24, and such accounts can represent roughly 5–10% of a unit’s weekly sales, giving buyers leverage to negotiate better pricing or shift to competitors with superior logistics.

Order aggregation concentrates spend, magnifying unit-level cost pressure; a single service failure can trigger outsized revenue swings and contract loss across multiple locations.

- Price sensitivity: high

- Market size: ~63B (2023–24)

- Unit revenue exposure: ~5–10%

- Risk: service failures cause outsized swings

Delivery reliance (~60% share), fees and 20-30% commissions hit margins

Customers face near-zero switching amid 400+ US Red Robin locations (2024), high price sensitivity, and strong delivery-platform influence (DoorDash ~60% 2024). Delivery fees ~$4.95 and 20–30% commissions compress perceived value; one-star review shifts revenue ~5–9%. Loyalty reduces churn but increases margin pressure via discounts and points.

| Metric | Value |

|---|---|

| Locations (2024) | 400+ |

| DoorDash share (2024) | ~60% |

| Delivery fee | ~$4.95 |

| Commissions | 20–30% |

| Review impact | 5–9% rev/★ |

| Catering market | $63B (2023–24) |

Same Document Delivered

Red Robin Gourmet Burgers Porter's Five Forces Analysis

This Porter's Five Forces analysis of Red Robin Gourmet Burgers evaluates competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes to inform strategy and valuation. The preview is the exact, fully formatted document you'll receive instantly after purchase—no placeholders or samples. Use it immediately for decision-making or presentation-ready reporting.