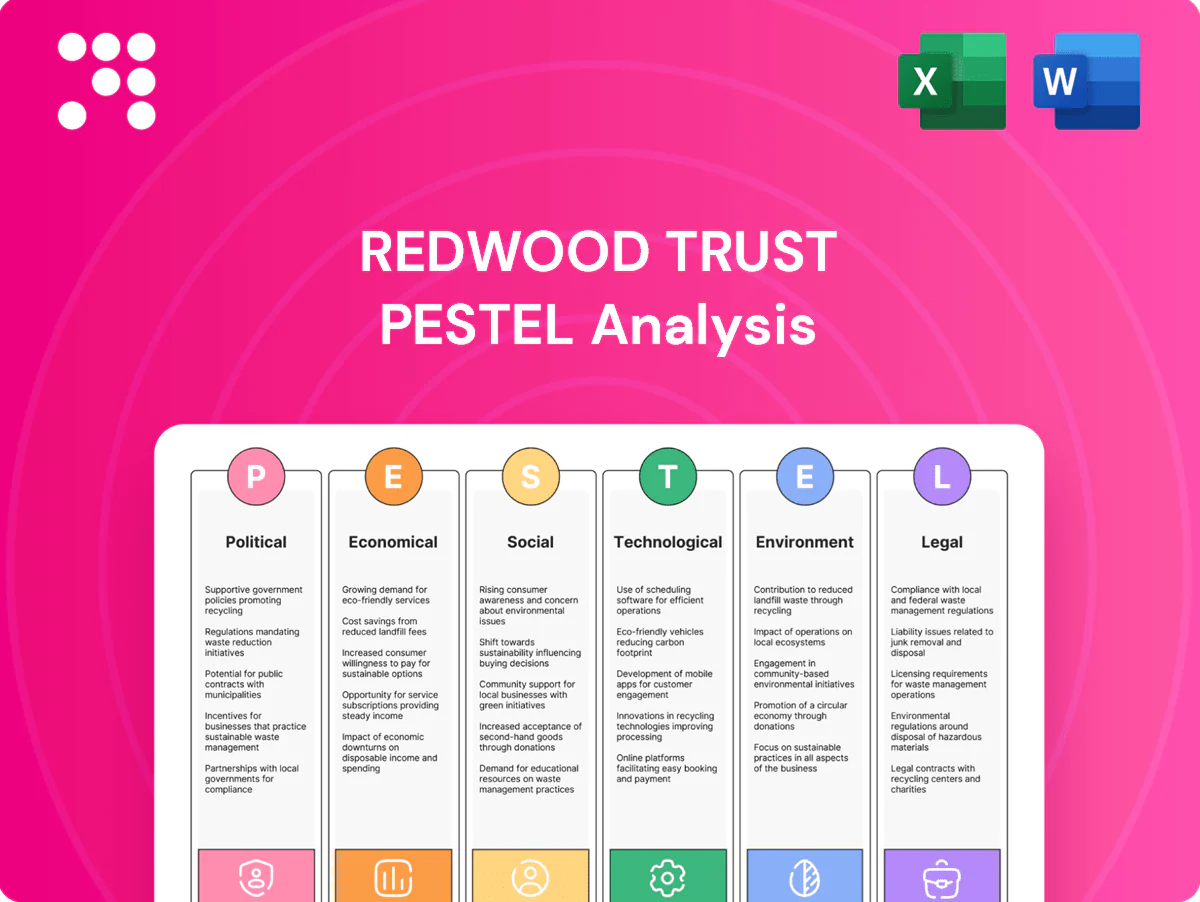

Redwood Trust PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our PESTLE Analysis tailored for Redwood Trust—three to five external forces distilled into actionable insights that reveal regulatory, economic, and technological risks and opportunities. Ideal for investors and strategists, this concise briefing points to where value and vulnerability lie. Purchase the full analysis to access the complete, editable report and make confident decisions today.

Political factors

Housing finance policy and GSE reform

Reform of Fannie Mae and Freddie Mac, in conservatorship since 2008, could reshape mortgage liquidity and pricing across a combined guarantee book of roughly $6.3 trillion, changing competitive dynamics for Redwood Trust. Expanded credit boxes or shifts in capital rules would alter loan eligibility and advance rates, impacting Redwood’s securitization economics and pipeline. Clear policy narrows execution risk and tightens securitization spreads; prolonged uncertainty widens spreads and raises funding costs.

Federal and state housing incentives

Federal and state housing incentives—including tax credits, down-payment assistance and nearly $46 billion in ARPA-era rental assistance—drive origination volumes and can accelerate prepayment speeds by stimulating purchases and refinances. Such incentives boost pipeline velocity for residential platforms but program sunset or expansion shifts credit mix and coupon stacks. Redwood must design products to capture policy tailwinds while avoiding concentration risk across supported geographies and cohorts.

Administrative priorities and regulatory appointments

Leadership at HUD, FHFA, CFPB and OCC sets supervisory tone for mortgage markets; 2024 US mortgage originations were roughly $1.0T, so stricter oversight can raise compliance costs and slow approvals while deregulatory stances may boost volumes. Post‑election shifts alter fair lending, appraisal and servicing rules; Redwood’s policy‑transition planning preserves execution certainty.

Local zoning and development politics

Zoning reforms that allow higher density (ADUs, duplexes) are widening supply and mortgage origination potential amid a US estimated housing shortfall of roughly 4 million units (Bipartisan Policy Center, 2023), while NIMBY-driven permit delays—often adding 6–12 months—constrain inventory and can pressure origination volume and credit performance.

- Density reforms boost supply and mortgage pool size

- NIMBY delays (6–12 months) raise refinance/repayment risk

- Regional policy divergence creates geographic concentration risk

- Redwood exposure mapping must track local policy cycles

Geopolitical and federal budget dynamics

Government shutdowns and processing slowdowns for FHA/VA (seen in past shutdowns and 2023 funding frictions) can delay data releases and closings, disrupting Redwood Trust origination pipelines. Geopolitical tensions have pushed risk premiums higher, with securitization spreads moving roughly 20–40 bps during recent shocks while the 10-year Treasury traded near 4.5% in 2024–mid‑2025. Fiscal policy shifts that reduce real disposable income compress housing demand; Redwood should keep liquidity buffers to manage funding volatility and wider spreads.

- Impact: delayed closings, origination drag

- Market: securitization spreads +20–40 bps; 10y ≈4.5%

- Demand: fiscal shifts lower disposable income → weaker housing demand

- Action: maintain liquidity buffers for funding volatility

GSE reform and oversight tighten mortgage liquidity; $6.3T guarantee book

Policy shifts on GSE reform ($6.3T guarantee book) and agency oversight drive mortgage liquidity and pricing; 2024 US originations ≈ $1.0T, so rule changes alter securitization economics. Housing shortfall ~4M units and zoning reforms affect origination volumes; geopolitical/fiscal shocks moved spreads +20–40bps with 10y ≈4.5%, raising funding risk.

| Factor | Metric | Impact | Action |

|---|---|---|---|

| GSE reform | $6.3T book | Liquidity/pricing | Model scenarios |

| Originations | $1.0T (2024) | Volume risk | Hedge spreads |

| Housing supply | −4M units | Credit mix | Geographic mapping |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely shape Redwood Trust’s mortgage investment business, using current market data and regulatory trends to identify risks and opportunities; designed for executives, consultants, and investors to support strategic planning, scenario analysis, and funding decisions.

A concise, visually segmented PESTLE summary of Redwood Trust that can be dropped into presentations, easily shared across teams, and annotated with local notes to streamline external risk discussions and strategic planning.

Economic factors

Interest rate cycles and mortgage rates

Federal funds at 5.25–5.50% and a 30-year mortgage averaging about 7.1% in mid-2025 have reduced affordability, lowering origination and refi incentives and slowing prepayment speeds. Rate moves shift product mix and reduce pull-through, while volatility has raised hedge costs and pipeline fallout risk. Redwood’s margin is highly sensitive to effective rate-risk and convexity management given these conditions.

Credit spreads and securitization market depth

RMBS/CMBS spread levels (senior CMBS ~120 bps, mezzanine tranches often 300–400 bps) directly determine Redwood Trust gain-on-sale and retained-tranche returns; spread widening in 2024–H1 2025 compressed issuance windows and knocked mark-to-market book values.

Housing supply, prices, and affordability

Tight inventory (roughly 2 months' supply in 2024) has propped national median prices near $390k while constraining purchase volumes; higher 30-year mortgage rates (~7% in 2024) and affordability shocks push borrower DTI toward the mid-30s, shifting FICO mix and raising early payment default risk. Wide regional price dispersion alters loss-severity assumptions, so Redwood’s underwriting and pricing must be calibrated to local supply-demand imbalances.

Employment and income trends

Job growth underpins loan performance and keeps delinquencies low in non-agency collateral; US unemployment 3.7% (June 2025) and average hourly earnings +4.1% YoY (May 2025) influence payment capacity and prepayment behavior. Sector-specific layoffs create localized stress pockets; Redwood’s credit models require real-time labor market signals at the MSA level.

- Job growth -> stronger performance

- Wages -> payment capacity/prepayments

- Layoffs -> micro stress pockets

- Need -> MSA-level real-time signals

Liquidity and funding conditions

Warehouse capacity, haircuts and repo terms drive carry and scalability for Redwood Trust; tighter funding increases cost of capital and compresses ROE on retained credit exposure, as noted in Redwood Trust’s 2024 filings. Counterparty diversification reduces rollover risk, while committed facilities and stress-tested liquidity planning support execution in down cycles.

- Warehouse capacity impacts leverage and spread capture

- Higher haircuts/repo costs lower carry and ROE

- Counterparty diversification mitigates rollover risk

- Committed facilities + stress tests bolster liquidity

GSE reform and oversight tighten mortgage liquidity; $6.3T guarantee book

Higher policy rates (Fed 5.25–5.50%) and 30-year mortgage ~7.1% (mid-2025) cut affordability, slowing originations and prepayments while raising hedge costs. RMBS/CMBS spreads (senior ~120 bps; mezz 300–400 bps) compress issuance and mark-to-market values. Tight inventory (~2 months, median price ~$390k in 2024) and unemployment 3.7% (June 2025) keep credit performance mixed across MSAs. Funding costs, haircuts and repo terms tighten ROE and scale.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| 30y mortgage | ~7.1% (mid-2025) |

| Unemployment | 3.7% (Jun 2025) |

| Median price | $390k (2024) |

| Senior CMBS spread | ~120 bps |

| Mezz spread | 300–400 bps |

What You See Is What You Get

Redwood Trust PESTLE Analysis

The Redwood Trust PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the same structured political, economic, social, technological, legal, and environmental insights as the final download with no placeholders or teasers. After checkout you’ll instantly get this finished file, ready for analysis and presentation.

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our PESTLE Analysis tailored for Redwood Trust—three to five external forces distilled into actionable insights that reveal regulatory, economic, and technological risks and opportunities. Ideal for investors and strategists, this concise briefing points to where value and vulnerability lie. Purchase the full analysis to access the complete, editable report and make confident decisions today.

Political factors

Housing finance policy and GSE reform

Reform of Fannie Mae and Freddie Mac, in conservatorship since 2008, could reshape mortgage liquidity and pricing across a combined guarantee book of roughly $6.3 trillion, changing competitive dynamics for Redwood Trust. Expanded credit boxes or shifts in capital rules would alter loan eligibility and advance rates, impacting Redwood’s securitization economics and pipeline. Clear policy narrows execution risk and tightens securitization spreads; prolonged uncertainty widens spreads and raises funding costs.

Federal and state housing incentives

Federal and state housing incentives—including tax credits, down-payment assistance and nearly $46 billion in ARPA-era rental assistance—drive origination volumes and can accelerate prepayment speeds by stimulating purchases and refinances. Such incentives boost pipeline velocity for residential platforms but program sunset or expansion shifts credit mix and coupon stacks. Redwood must design products to capture policy tailwinds while avoiding concentration risk across supported geographies and cohorts.

Administrative priorities and regulatory appointments

Leadership at HUD, FHFA, CFPB and OCC sets supervisory tone for mortgage markets; 2024 US mortgage originations were roughly $1.0T, so stricter oversight can raise compliance costs and slow approvals while deregulatory stances may boost volumes. Post‑election shifts alter fair lending, appraisal and servicing rules; Redwood’s policy‑transition planning preserves execution certainty.

Local zoning and development politics

Zoning reforms that allow higher density (ADUs, duplexes) are widening supply and mortgage origination potential amid a US estimated housing shortfall of roughly 4 million units (Bipartisan Policy Center, 2023), while NIMBY-driven permit delays—often adding 6–12 months—constrain inventory and can pressure origination volume and credit performance.

- Density reforms boost supply and mortgage pool size

- NIMBY delays (6–12 months) raise refinance/repayment risk

- Regional policy divergence creates geographic concentration risk

- Redwood exposure mapping must track local policy cycles

Geopolitical and federal budget dynamics

Government shutdowns and processing slowdowns for FHA/VA (seen in past shutdowns and 2023 funding frictions) can delay data releases and closings, disrupting Redwood Trust origination pipelines. Geopolitical tensions have pushed risk premiums higher, with securitization spreads moving roughly 20–40 bps during recent shocks while the 10-year Treasury traded near 4.5% in 2024–mid‑2025. Fiscal policy shifts that reduce real disposable income compress housing demand; Redwood should keep liquidity buffers to manage funding volatility and wider spreads.

- Impact: delayed closings, origination drag

- Market: securitization spreads +20–40 bps; 10y ≈4.5%

- Demand: fiscal shifts lower disposable income → weaker housing demand

- Action: maintain liquidity buffers for funding volatility

GSE reform and oversight tighten mortgage liquidity; $6.3T guarantee book

Policy shifts on GSE reform ($6.3T guarantee book) and agency oversight drive mortgage liquidity and pricing; 2024 US originations ≈ $1.0T, so rule changes alter securitization economics. Housing shortfall ~4M units and zoning reforms affect origination volumes; geopolitical/fiscal shocks moved spreads +20–40bps with 10y ≈4.5%, raising funding risk.

| Factor | Metric | Impact | Action |

|---|---|---|---|

| GSE reform | $6.3T book | Liquidity/pricing | Model scenarios |

| Originations | $1.0T (2024) | Volume risk | Hedge spreads |

| Housing supply | −4M units | Credit mix | Geographic mapping |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely shape Redwood Trust’s mortgage investment business, using current market data and regulatory trends to identify risks and opportunities; designed for executives, consultants, and investors to support strategic planning, scenario analysis, and funding decisions.

A concise, visually segmented PESTLE summary of Redwood Trust that can be dropped into presentations, easily shared across teams, and annotated with local notes to streamline external risk discussions and strategic planning.

Economic factors

Interest rate cycles and mortgage rates

Federal funds at 5.25–5.50% and a 30-year mortgage averaging about 7.1% in mid-2025 have reduced affordability, lowering origination and refi incentives and slowing prepayment speeds. Rate moves shift product mix and reduce pull-through, while volatility has raised hedge costs and pipeline fallout risk. Redwood’s margin is highly sensitive to effective rate-risk and convexity management given these conditions.

Credit spreads and securitization market depth

RMBS/CMBS spread levels (senior CMBS ~120 bps, mezzanine tranches often 300–400 bps) directly determine Redwood Trust gain-on-sale and retained-tranche returns; spread widening in 2024–H1 2025 compressed issuance windows and knocked mark-to-market book values.

Housing supply, prices, and affordability

Tight inventory (roughly 2 months' supply in 2024) has propped national median prices near $390k while constraining purchase volumes; higher 30-year mortgage rates (~7% in 2024) and affordability shocks push borrower DTI toward the mid-30s, shifting FICO mix and raising early payment default risk. Wide regional price dispersion alters loss-severity assumptions, so Redwood’s underwriting and pricing must be calibrated to local supply-demand imbalances.

Employment and income trends

Job growth underpins loan performance and keeps delinquencies low in non-agency collateral; US unemployment 3.7% (June 2025) and average hourly earnings +4.1% YoY (May 2025) influence payment capacity and prepayment behavior. Sector-specific layoffs create localized stress pockets; Redwood’s credit models require real-time labor market signals at the MSA level.

- Job growth -> stronger performance

- Wages -> payment capacity/prepayments

- Layoffs -> micro stress pockets

- Need -> MSA-level real-time signals

Liquidity and funding conditions

Warehouse capacity, haircuts and repo terms drive carry and scalability for Redwood Trust; tighter funding increases cost of capital and compresses ROE on retained credit exposure, as noted in Redwood Trust’s 2024 filings. Counterparty diversification reduces rollover risk, while committed facilities and stress-tested liquidity planning support execution in down cycles.

- Warehouse capacity impacts leverage and spread capture

- Higher haircuts/repo costs lower carry and ROE

- Counterparty diversification mitigates rollover risk

- Committed facilities + stress tests bolster liquidity

GSE reform and oversight tighten mortgage liquidity; $6.3T guarantee book

Higher policy rates (Fed 5.25–5.50%) and 30-year mortgage ~7.1% (mid-2025) cut affordability, slowing originations and prepayments while raising hedge costs. RMBS/CMBS spreads (senior ~120 bps; mezz 300–400 bps) compress issuance and mark-to-market values. Tight inventory (~2 months, median price ~$390k in 2024) and unemployment 3.7% (June 2025) keep credit performance mixed across MSAs. Funding costs, haircuts and repo terms tighten ROE and scale.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| 30y mortgage | ~7.1% (mid-2025) |

| Unemployment | 3.7% (Jun 2025) |

| Median price | $390k (2024) |

| Senior CMBS spread | ~120 bps |

| Mezz spread | 300–400 bps |

What You See Is What You Get

Redwood Trust PESTLE Analysis

The Redwood Trust PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the same structured political, economic, social, technological, legal, and environmental insights as the final download with no placeholders or teasers. After checkout you’ll instantly get this finished file, ready for analysis and presentation.

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our PESTLE Analysis tailored for Redwood Trust—three to five external forces distilled into actionable insights that reveal regulatory, economic, and technological risks and opportunities. Ideal for investors and strategists, this concise briefing points to where value and vulnerability lie. Purchase the full analysis to access the complete, editable report and make confident decisions today.

Political factors

Housing finance policy and GSE reform

Reform of Fannie Mae and Freddie Mac, in conservatorship since 2008, could reshape mortgage liquidity and pricing across a combined guarantee book of roughly $6.3 trillion, changing competitive dynamics for Redwood Trust. Expanded credit boxes or shifts in capital rules would alter loan eligibility and advance rates, impacting Redwood’s securitization economics and pipeline. Clear policy narrows execution risk and tightens securitization spreads; prolonged uncertainty widens spreads and raises funding costs.

Federal and state housing incentives

Federal and state housing incentives—including tax credits, down-payment assistance and nearly $46 billion in ARPA-era rental assistance—drive origination volumes and can accelerate prepayment speeds by stimulating purchases and refinances. Such incentives boost pipeline velocity for residential platforms but program sunset or expansion shifts credit mix and coupon stacks. Redwood must design products to capture policy tailwinds while avoiding concentration risk across supported geographies and cohorts.

Administrative priorities and regulatory appointments

Leadership at HUD, FHFA, CFPB and OCC sets supervisory tone for mortgage markets; 2024 US mortgage originations were roughly $1.0T, so stricter oversight can raise compliance costs and slow approvals while deregulatory stances may boost volumes. Post‑election shifts alter fair lending, appraisal and servicing rules; Redwood’s policy‑transition planning preserves execution certainty.

Local zoning and development politics

Zoning reforms that allow higher density (ADUs, duplexes) are widening supply and mortgage origination potential amid a US estimated housing shortfall of roughly 4 million units (Bipartisan Policy Center, 2023), while NIMBY-driven permit delays—often adding 6–12 months—constrain inventory and can pressure origination volume and credit performance.

- Density reforms boost supply and mortgage pool size

- NIMBY delays (6–12 months) raise refinance/repayment risk

- Regional policy divergence creates geographic concentration risk

- Redwood exposure mapping must track local policy cycles

Geopolitical and federal budget dynamics

Government shutdowns and processing slowdowns for FHA/VA (seen in past shutdowns and 2023 funding frictions) can delay data releases and closings, disrupting Redwood Trust origination pipelines. Geopolitical tensions have pushed risk premiums higher, with securitization spreads moving roughly 20–40 bps during recent shocks while the 10-year Treasury traded near 4.5% in 2024–mid‑2025. Fiscal policy shifts that reduce real disposable income compress housing demand; Redwood should keep liquidity buffers to manage funding volatility and wider spreads.

- Impact: delayed closings, origination drag

- Market: securitization spreads +20–40 bps; 10y ≈4.5%

- Demand: fiscal shifts lower disposable income → weaker housing demand

- Action: maintain liquidity buffers for funding volatility

GSE reform and oversight tighten mortgage liquidity; $6.3T guarantee book

Policy shifts on GSE reform ($6.3T guarantee book) and agency oversight drive mortgage liquidity and pricing; 2024 US originations ≈ $1.0T, so rule changes alter securitization economics. Housing shortfall ~4M units and zoning reforms affect origination volumes; geopolitical/fiscal shocks moved spreads +20–40bps with 10y ≈4.5%, raising funding risk.

| Factor | Metric | Impact | Action |

|---|---|---|---|

| GSE reform | $6.3T book | Liquidity/pricing | Model scenarios |

| Originations | $1.0T (2024) | Volume risk | Hedge spreads |

| Housing supply | −4M units | Credit mix | Geographic mapping |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely shape Redwood Trust’s mortgage investment business, using current market data and regulatory trends to identify risks and opportunities; designed for executives, consultants, and investors to support strategic planning, scenario analysis, and funding decisions.

A concise, visually segmented PESTLE summary of Redwood Trust that can be dropped into presentations, easily shared across teams, and annotated with local notes to streamline external risk discussions and strategic planning.

Economic factors

Interest rate cycles and mortgage rates

Federal funds at 5.25–5.50% and a 30-year mortgage averaging about 7.1% in mid-2025 have reduced affordability, lowering origination and refi incentives and slowing prepayment speeds. Rate moves shift product mix and reduce pull-through, while volatility has raised hedge costs and pipeline fallout risk. Redwood’s margin is highly sensitive to effective rate-risk and convexity management given these conditions.

Credit spreads and securitization market depth

RMBS/CMBS spread levels (senior CMBS ~120 bps, mezzanine tranches often 300–400 bps) directly determine Redwood Trust gain-on-sale and retained-tranche returns; spread widening in 2024–H1 2025 compressed issuance windows and knocked mark-to-market book values.

Housing supply, prices, and affordability

Tight inventory (roughly 2 months' supply in 2024) has propped national median prices near $390k while constraining purchase volumes; higher 30-year mortgage rates (~7% in 2024) and affordability shocks push borrower DTI toward the mid-30s, shifting FICO mix and raising early payment default risk. Wide regional price dispersion alters loss-severity assumptions, so Redwood’s underwriting and pricing must be calibrated to local supply-demand imbalances.

Employment and income trends

Job growth underpins loan performance and keeps delinquencies low in non-agency collateral; US unemployment 3.7% (June 2025) and average hourly earnings +4.1% YoY (May 2025) influence payment capacity and prepayment behavior. Sector-specific layoffs create localized stress pockets; Redwood’s credit models require real-time labor market signals at the MSA level.

- Job growth -> stronger performance

- Wages -> payment capacity/prepayments

- Layoffs -> micro stress pockets

- Need -> MSA-level real-time signals

Liquidity and funding conditions

Warehouse capacity, haircuts and repo terms drive carry and scalability for Redwood Trust; tighter funding increases cost of capital and compresses ROE on retained credit exposure, as noted in Redwood Trust’s 2024 filings. Counterparty diversification reduces rollover risk, while committed facilities and stress-tested liquidity planning support execution in down cycles.

- Warehouse capacity impacts leverage and spread capture

- Higher haircuts/repo costs lower carry and ROE

- Counterparty diversification mitigates rollover risk

- Committed facilities + stress tests bolster liquidity

GSE reform and oversight tighten mortgage liquidity; $6.3T guarantee book

Higher policy rates (Fed 5.25–5.50%) and 30-year mortgage ~7.1% (mid-2025) cut affordability, slowing originations and prepayments while raising hedge costs. RMBS/CMBS spreads (senior ~120 bps; mezz 300–400 bps) compress issuance and mark-to-market values. Tight inventory (~2 months, median price ~$390k in 2024) and unemployment 3.7% (June 2025) keep credit performance mixed across MSAs. Funding costs, haircuts and repo terms tighten ROE and scale.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| 30y mortgage | ~7.1% (mid-2025) |

| Unemployment | 3.7% (Jun 2025) |

| Median price | $390k (2024) |

| Senior CMBS spread | ~120 bps |

| Mezz spread | 300–400 bps |

What You See Is What You Get

Redwood Trust PESTLE Analysis

The Redwood Trust PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the same structured political, economic, social, technological, legal, and environmental insights as the final download with no placeholders or teasers. After checkout you’ll instantly get this finished file, ready for analysis and presentation.