Regal Rexnord PESTLE Analysis

Your Competitive Advantage Starts with This Report

Explore how political, economic, social, technological, legal and environmental forces are shaping Regal Rexnord’s strategic outlook in our concise PESTLE snapshot; ideal for investors and strategists seeking quick clarity. Purchase the full PESTLE to access detailed risks, opportunities, and actionable recommendations.

Political factors

Trade policy and tariffs

Shifts in U.S.–China/EU trade policy, including U.S. Section 232 steel tariffs of 25% and Section 301 measures of 7.5–25% on many Chinese goods, directly affect Regal Rexnord component sourcing costs and pricing power. Tariffs on steel, copper and electronic subassemblies can compress margins or necessitate repricing. Proactive supply diversification and tariff engineering mitigate volatility, while policy stability steers capital planning for global plants.

Infrastructure and industrial policy

Government-backed programs such as the 2021 Infrastructure Investment and Jobs Act ($1.2 trillion) and semiconductor incentives (CHIPS Act ~ $52 billion) are expanding demand for motors, drives and power-transmission equipment, boosting public-project orders for Regal Rexnord. Funding cycles from federal/state appropriations affect order visibility and backlog quality, creating lumpiness in bookings. Strengthened Buy-American rules are reshaping tender eligibility and domestic-content strategies for bids. Active engagement in public projects can reduce cyclical exposure by stabilizing revenue streams.

Geopolitical risk and supply routes

Conflicts and sanctions disrupt Regal Rexnord’s logistics and extend lead times, constraining access to affected markets. Rerouting via alternative ports or nearshoring increases freight, inventory and coordination costs and adds operational complexity. Expanded sanction screening and export-control compliance raise administrative overhead and can delay shipments. Robust scenario planning is needed to protect continuity for critical end-markets.

Energy and industrial decarbonization policy

Energy-efficiency and electrification incentives, amplified by US IRA tax credits and EU grant programs, are lifting premium motor and drive adoption and can shorten heavy-industry retrofit paybacks to roughly 2–4 years. Carbon pricing—EU ETS ~€90–100/tCO2 in 2024—shifts customer decisions toward high-efficiency retrofits. Regional policy variation mandates tailored products and local certifications.

- Incentives boost premium motor uptake

- Carbon price accelerates retrofit timing

- Policy clarity shortens payback (2–4 yrs)

- Regional gaps require tailored offerings

Public procurement and standards alignment

Defense, healthcare and utilities demand strict sourcing and security criteria that affect Regal Rexnord access to contracts; the US defense budget was about 858 billion USD in FY2024, underscoring high-value opportunities tied to compliance. Political shifts and protectionist procurement policies can rapidly change standards and supplier preferences, while meeting local certification and localization targets opens government pipelines; OECD estimates public procurement at roughly 12% of GDP. Noncompliance risks exclusion from strategic projects and multi-year programs.

- Tag: defense — US FY2024 budget ~858B USD

- Tag: procurement — OECD: ~12% of GDP in public procurement

- Tag: localization — local certification often required for government tenders

- Tag: risk — noncompliance excludes suppliers from strategic projects

Tariffs, export controls and IIJA/CHIPS spur motor demand; nearshoring raises costs

Trade tariffs (US Section 232/301) and shifting US–China/EU policy raise input costs and force supply diversification; IIJA $1.2T and CHIPS ~$52B boost motor/drive demand. Sanctions, nearshoring and export controls increase lead times and compliance spend; EU ETS ~€90–100/tCO2 in 2024 accelerates efficiency adoption. US defense budget ~858B FY2024 and OECD ~12% GDP in public procurement favor localized, compliant suppliers.

| Policy | 2024/2025 Metric |

|---|---|

| IIJA | $1.2T |

| CHIPS | ~$52B |

| EU ETS | €90–100/tCO2 |

| US Defense | $858B FY2024 |

| Public Procure | ~12% GDP (OECD) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Regal Rexnord, with data-driven trends and sector-specific examples to surface risks and opportunities. Designed for executives and advisors to inform strategy, scenario planning and investor communications.

Condensed PESTLE summary of Regal Rexnord that relieves briefing pain points by highlighting key political, economic, social, technological, legal and environmental factors at a glance. Easily dropped into presentations or shared across teams to speed alignment and risk discussions during strategic planning.

Economic factors

Industrial cycle sensitivity

Orders at Regal Rexnord closely track capex cycles in manufacturing, energy and aerospace, with new-equipment spends rising in expansion phases while slowdowns typically defer purchases and boost MRO and retrofit demand. Backlog levels and book-to-bill ratios act as leading indicators of inflection points for the business. Diversified end-markets—HVAC, industrial, and power—help cushion sector-specific downturns.

Commodity and input cost volatility

Steel HRC swings (roughly $700/tonne in 2024) and copper (~$9,000/tonne LME 2024) plus rare-earths (neodymium ~ $60/kg 2024) and electronics component price volatility materially lift COGS for Regal Rexnord. Index-linked pricing and hedging mitigate margin pressure but lag effects persist across quarters. Supplier consolidation and dual-sourcing lower shock risk. Design-to-cost and value engineering sustain competitiveness.

Currency fluctuations

Regal Rexnord faces FX translation and transaction risk from global revenues and costs, with the US Dollar index near 105 in mid-2024 amplifying pressure on overseas margins and export competitiveness. Local production and sourcing provide natural hedges that stabilize results by matching costs and revenues by currency. Formal hedging programs smooth earnings volatility but add treasury complexity and potential hedge ineffectiveness risk.

Interest rates and credit conditions

Higher policy rates (Fed funds ~5.25–5.50% in mid‑2025) raise customer hurdle rates and slow capex approvals, while elevated borrowing spreads (investment‑grade yields ~4.5–6% in 2025) increase financing costs for M&A, inventory carry and working capital. Service and retrofit offerings can gain share as customers defer full replacements, and flexible payment terms plus ROI calculators materially improve deal conversion.

- Higher rates: Fed 5.25–5.50% (mid‑2025)

- Cost impacts: higher yields squeeze M&A and WC

- Opportunity: service/retrofit demand up

- Mitigant: flexible terms and ROI tools

M&A integration and synergies

Scale and portfolio breadth at Regal Rexnord enable cross-selling and cost synergies, while integration execution determines margin expansion and cash conversion; overpaying or cultural mismatch can dilute returns. Disciplined post-merger integration focuses on technology uplift and channel leverage to realize targeted synergies and sustain ROI.

- Scale supports cross-sell and procurement savings

- Integration quality drives margin and cash conversion

- Overpayment/culture risk dilutes returns

- Disciplined PI leverages tech and channels

Tariffs, export controls and IIJA/CHIPS spur motor demand; nearshoring raises costs

Regal Rexnord sales track industrial capex cycles; backlog and book‑to‑bill signal inflections. Input costs: HRC ~$700/tonne (2024), copper ~$9,000/tonne (2024), neodymium ~$60/kg (2024) press margins despite index‑linked pricing. FX: USD index ~105 (mid‑2024) risks overseas margins. Rates: Fed 5.25–5.50% (mid‑2025) and IG yields 4.5–6% raise financing costs, boosting retrofit/service demand.

| Metric | 2024/2025 |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2025) |

| USD index | ~105 (mid‑2024) |

| HRC/copper/Nd | $700/t • $9,000/t • $60/kg (2024) |

What You See Is What You Get

Regal Rexnord PESTLE Analysis

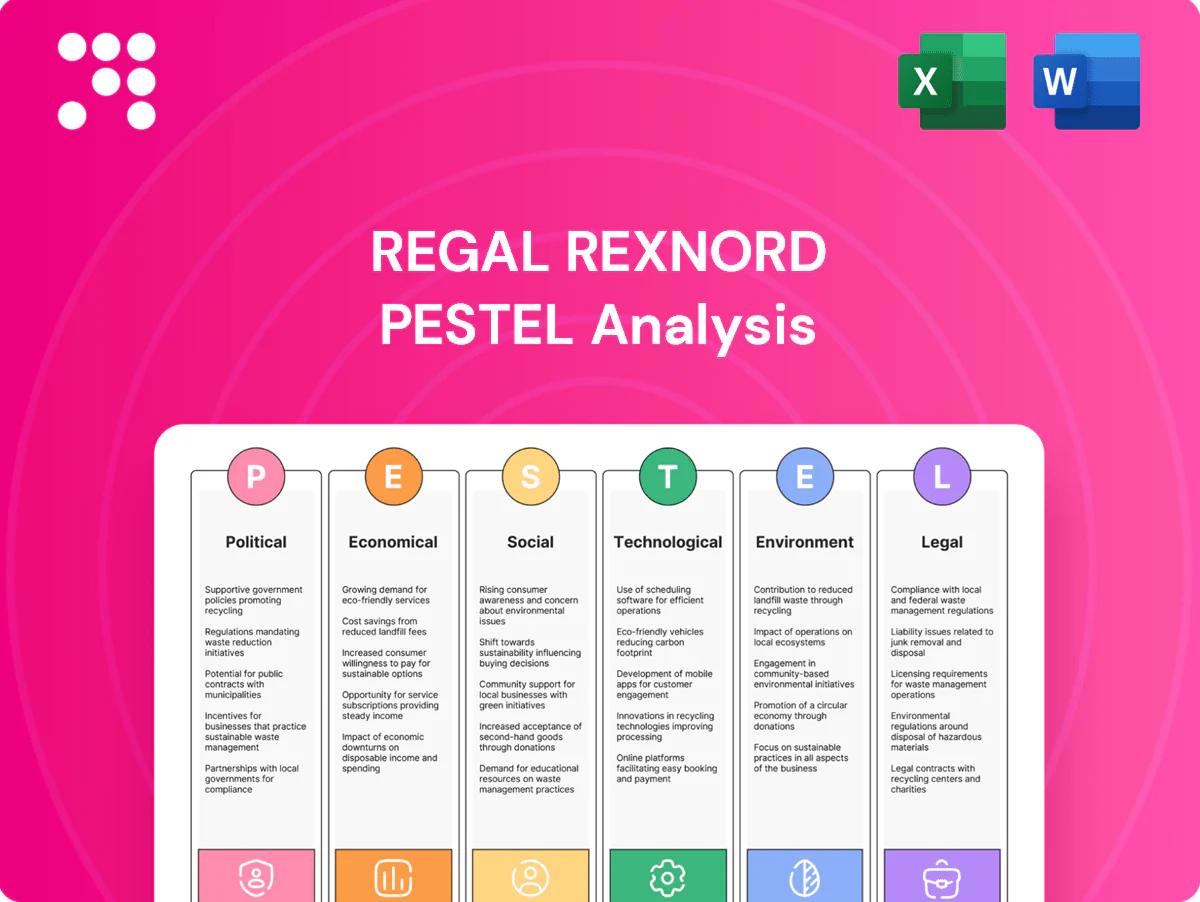

The Regal Rexnord PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—this is the final file you’ll download immediately after payment.

Your Competitive Advantage Starts with This Report

Explore how political, economic, social, technological, legal and environmental forces are shaping Regal Rexnord’s strategic outlook in our concise PESTLE snapshot; ideal for investors and strategists seeking quick clarity. Purchase the full PESTLE to access detailed risks, opportunities, and actionable recommendations.

Political factors

Trade policy and tariffs

Shifts in U.S.–China/EU trade policy, including U.S. Section 232 steel tariffs of 25% and Section 301 measures of 7.5–25% on many Chinese goods, directly affect Regal Rexnord component sourcing costs and pricing power. Tariffs on steel, copper and electronic subassemblies can compress margins or necessitate repricing. Proactive supply diversification and tariff engineering mitigate volatility, while policy stability steers capital planning for global plants.

Infrastructure and industrial policy

Government-backed programs such as the 2021 Infrastructure Investment and Jobs Act ($1.2 trillion) and semiconductor incentives (CHIPS Act ~ $52 billion) are expanding demand for motors, drives and power-transmission equipment, boosting public-project orders for Regal Rexnord. Funding cycles from federal/state appropriations affect order visibility and backlog quality, creating lumpiness in bookings. Strengthened Buy-American rules are reshaping tender eligibility and domestic-content strategies for bids. Active engagement in public projects can reduce cyclical exposure by stabilizing revenue streams.

Geopolitical risk and supply routes

Conflicts and sanctions disrupt Regal Rexnord’s logistics and extend lead times, constraining access to affected markets. Rerouting via alternative ports or nearshoring increases freight, inventory and coordination costs and adds operational complexity. Expanded sanction screening and export-control compliance raise administrative overhead and can delay shipments. Robust scenario planning is needed to protect continuity for critical end-markets.

Energy and industrial decarbonization policy

Energy-efficiency and electrification incentives, amplified by US IRA tax credits and EU grant programs, are lifting premium motor and drive adoption and can shorten heavy-industry retrofit paybacks to roughly 2–4 years. Carbon pricing—EU ETS ~€90–100/tCO2 in 2024—shifts customer decisions toward high-efficiency retrofits. Regional policy variation mandates tailored products and local certifications.

- Incentives boost premium motor uptake

- Carbon price accelerates retrofit timing

- Policy clarity shortens payback (2–4 yrs)

- Regional gaps require tailored offerings

Public procurement and standards alignment

Defense, healthcare and utilities demand strict sourcing and security criteria that affect Regal Rexnord access to contracts; the US defense budget was about 858 billion USD in FY2024, underscoring high-value opportunities tied to compliance. Political shifts and protectionist procurement policies can rapidly change standards and supplier preferences, while meeting local certification and localization targets opens government pipelines; OECD estimates public procurement at roughly 12% of GDP. Noncompliance risks exclusion from strategic projects and multi-year programs.

- Tag: defense — US FY2024 budget ~858B USD

- Tag: procurement — OECD: ~12% of GDP in public procurement

- Tag: localization — local certification often required for government tenders

- Tag: risk — noncompliance excludes suppliers from strategic projects

Tariffs, export controls and IIJA/CHIPS spur motor demand; nearshoring raises costs

Trade tariffs (US Section 232/301) and shifting US–China/EU policy raise input costs and force supply diversification; IIJA $1.2T and CHIPS ~$52B boost motor/drive demand. Sanctions, nearshoring and export controls increase lead times and compliance spend; EU ETS ~€90–100/tCO2 in 2024 accelerates efficiency adoption. US defense budget ~858B FY2024 and OECD ~12% GDP in public procurement favor localized, compliant suppliers.

| Policy | 2024/2025 Metric |

|---|---|

| IIJA | $1.2T |

| CHIPS | ~$52B |

| EU ETS | €90–100/tCO2 |

| US Defense | $858B FY2024 |

| Public Procure | ~12% GDP (OECD) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Regal Rexnord, with data-driven trends and sector-specific examples to surface risks and opportunities. Designed for executives and advisors to inform strategy, scenario planning and investor communications.

Condensed PESTLE summary of Regal Rexnord that relieves briefing pain points by highlighting key political, economic, social, technological, legal and environmental factors at a glance. Easily dropped into presentations or shared across teams to speed alignment and risk discussions during strategic planning.

Economic factors

Industrial cycle sensitivity

Orders at Regal Rexnord closely track capex cycles in manufacturing, energy and aerospace, with new-equipment spends rising in expansion phases while slowdowns typically defer purchases and boost MRO and retrofit demand. Backlog levels and book-to-bill ratios act as leading indicators of inflection points for the business. Diversified end-markets—HVAC, industrial, and power—help cushion sector-specific downturns.

Commodity and input cost volatility

Steel HRC swings (roughly $700/tonne in 2024) and copper (~$9,000/tonne LME 2024) plus rare-earths (neodymium ~ $60/kg 2024) and electronics component price volatility materially lift COGS for Regal Rexnord. Index-linked pricing and hedging mitigate margin pressure but lag effects persist across quarters. Supplier consolidation and dual-sourcing lower shock risk. Design-to-cost and value engineering sustain competitiveness.

Currency fluctuations

Regal Rexnord faces FX translation and transaction risk from global revenues and costs, with the US Dollar index near 105 in mid-2024 amplifying pressure on overseas margins and export competitiveness. Local production and sourcing provide natural hedges that stabilize results by matching costs and revenues by currency. Formal hedging programs smooth earnings volatility but add treasury complexity and potential hedge ineffectiveness risk.

Interest rates and credit conditions

Higher policy rates (Fed funds ~5.25–5.50% in mid‑2025) raise customer hurdle rates and slow capex approvals, while elevated borrowing spreads (investment‑grade yields ~4.5–6% in 2025) increase financing costs for M&A, inventory carry and working capital. Service and retrofit offerings can gain share as customers defer full replacements, and flexible payment terms plus ROI calculators materially improve deal conversion.

- Higher rates: Fed 5.25–5.50% (mid‑2025)

- Cost impacts: higher yields squeeze M&A and WC

- Opportunity: service/retrofit demand up

- Mitigant: flexible terms and ROI tools

M&A integration and synergies

Scale and portfolio breadth at Regal Rexnord enable cross-selling and cost synergies, while integration execution determines margin expansion and cash conversion; overpaying or cultural mismatch can dilute returns. Disciplined post-merger integration focuses on technology uplift and channel leverage to realize targeted synergies and sustain ROI.

- Scale supports cross-sell and procurement savings

- Integration quality drives margin and cash conversion

- Overpayment/culture risk dilutes returns

- Disciplined PI leverages tech and channels

Tariffs, export controls and IIJA/CHIPS spur motor demand; nearshoring raises costs

Regal Rexnord sales track industrial capex cycles; backlog and book‑to‑bill signal inflections. Input costs: HRC ~$700/tonne (2024), copper ~$9,000/tonne (2024), neodymium ~$60/kg (2024) press margins despite index‑linked pricing. FX: USD index ~105 (mid‑2024) risks overseas margins. Rates: Fed 5.25–5.50% (mid‑2025) and IG yields 4.5–6% raise financing costs, boosting retrofit/service demand.

| Metric | 2024/2025 |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2025) |

| USD index | ~105 (mid‑2024) |

| HRC/copper/Nd | $700/t • $9,000/t • $60/kg (2024) |

What You See Is What You Get

Regal Rexnord PESTLE Analysis

The Regal Rexnord PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—this is the final file you’ll download immediately after payment.

Description

Your Competitive Advantage Starts with This Report

Explore how political, economic, social, technological, legal and environmental forces are shaping Regal Rexnord’s strategic outlook in our concise PESTLE snapshot; ideal for investors and strategists seeking quick clarity. Purchase the full PESTLE to access detailed risks, opportunities, and actionable recommendations.

Political factors

Trade policy and tariffs

Shifts in U.S.–China/EU trade policy, including U.S. Section 232 steel tariffs of 25% and Section 301 measures of 7.5–25% on many Chinese goods, directly affect Regal Rexnord component sourcing costs and pricing power. Tariffs on steel, copper and electronic subassemblies can compress margins or necessitate repricing. Proactive supply diversification and tariff engineering mitigate volatility, while policy stability steers capital planning for global plants.

Infrastructure and industrial policy

Government-backed programs such as the 2021 Infrastructure Investment and Jobs Act ($1.2 trillion) and semiconductor incentives (CHIPS Act ~ $52 billion) are expanding demand for motors, drives and power-transmission equipment, boosting public-project orders for Regal Rexnord. Funding cycles from federal/state appropriations affect order visibility and backlog quality, creating lumpiness in bookings. Strengthened Buy-American rules are reshaping tender eligibility and domestic-content strategies for bids. Active engagement in public projects can reduce cyclical exposure by stabilizing revenue streams.

Geopolitical risk and supply routes

Conflicts and sanctions disrupt Regal Rexnord’s logistics and extend lead times, constraining access to affected markets. Rerouting via alternative ports or nearshoring increases freight, inventory and coordination costs and adds operational complexity. Expanded sanction screening and export-control compliance raise administrative overhead and can delay shipments. Robust scenario planning is needed to protect continuity for critical end-markets.

Energy and industrial decarbonization policy

Energy-efficiency and electrification incentives, amplified by US IRA tax credits and EU grant programs, are lifting premium motor and drive adoption and can shorten heavy-industry retrofit paybacks to roughly 2–4 years. Carbon pricing—EU ETS ~€90–100/tCO2 in 2024—shifts customer decisions toward high-efficiency retrofits. Regional policy variation mandates tailored products and local certifications.

- Incentives boost premium motor uptake

- Carbon price accelerates retrofit timing

- Policy clarity shortens payback (2–4 yrs)

- Regional gaps require tailored offerings

Public procurement and standards alignment

Defense, healthcare and utilities demand strict sourcing and security criteria that affect Regal Rexnord access to contracts; the US defense budget was about 858 billion USD in FY2024, underscoring high-value opportunities tied to compliance. Political shifts and protectionist procurement policies can rapidly change standards and supplier preferences, while meeting local certification and localization targets opens government pipelines; OECD estimates public procurement at roughly 12% of GDP. Noncompliance risks exclusion from strategic projects and multi-year programs.

- Tag: defense — US FY2024 budget ~858B USD

- Tag: procurement — OECD: ~12% of GDP in public procurement

- Tag: localization — local certification often required for government tenders

- Tag: risk — noncompliance excludes suppliers from strategic projects

Tariffs, export controls and IIJA/CHIPS spur motor demand; nearshoring raises costs

Trade tariffs (US Section 232/301) and shifting US–China/EU policy raise input costs and force supply diversification; IIJA $1.2T and CHIPS ~$52B boost motor/drive demand. Sanctions, nearshoring and export controls increase lead times and compliance spend; EU ETS ~€90–100/tCO2 in 2024 accelerates efficiency adoption. US defense budget ~858B FY2024 and OECD ~12% GDP in public procurement favor localized, compliant suppliers.

| Policy | 2024/2025 Metric |

|---|---|

| IIJA | $1.2T |

| CHIPS | ~$52B |

| EU ETS | €90–100/tCO2 |

| US Defense | $858B FY2024 |

| Public Procure | ~12% GDP (OECD) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Regal Rexnord, with data-driven trends and sector-specific examples to surface risks and opportunities. Designed for executives and advisors to inform strategy, scenario planning and investor communications.

Condensed PESTLE summary of Regal Rexnord that relieves briefing pain points by highlighting key political, economic, social, technological, legal and environmental factors at a glance. Easily dropped into presentations or shared across teams to speed alignment and risk discussions during strategic planning.

Economic factors

Industrial cycle sensitivity

Orders at Regal Rexnord closely track capex cycles in manufacturing, energy and aerospace, with new-equipment spends rising in expansion phases while slowdowns typically defer purchases and boost MRO and retrofit demand. Backlog levels and book-to-bill ratios act as leading indicators of inflection points for the business. Diversified end-markets—HVAC, industrial, and power—help cushion sector-specific downturns.

Commodity and input cost volatility

Steel HRC swings (roughly $700/tonne in 2024) and copper (~$9,000/tonne LME 2024) plus rare-earths (neodymium ~ $60/kg 2024) and electronics component price volatility materially lift COGS for Regal Rexnord. Index-linked pricing and hedging mitigate margin pressure but lag effects persist across quarters. Supplier consolidation and dual-sourcing lower shock risk. Design-to-cost and value engineering sustain competitiveness.

Currency fluctuations

Regal Rexnord faces FX translation and transaction risk from global revenues and costs, with the US Dollar index near 105 in mid-2024 amplifying pressure on overseas margins and export competitiveness. Local production and sourcing provide natural hedges that stabilize results by matching costs and revenues by currency. Formal hedging programs smooth earnings volatility but add treasury complexity and potential hedge ineffectiveness risk.

Interest rates and credit conditions

Higher policy rates (Fed funds ~5.25–5.50% in mid‑2025) raise customer hurdle rates and slow capex approvals, while elevated borrowing spreads (investment‑grade yields ~4.5–6% in 2025) increase financing costs for M&A, inventory carry and working capital. Service and retrofit offerings can gain share as customers defer full replacements, and flexible payment terms plus ROI calculators materially improve deal conversion.

- Higher rates: Fed 5.25–5.50% (mid‑2025)

- Cost impacts: higher yields squeeze M&A and WC

- Opportunity: service/retrofit demand up

- Mitigant: flexible terms and ROI tools

M&A integration and synergies

Scale and portfolio breadth at Regal Rexnord enable cross-selling and cost synergies, while integration execution determines margin expansion and cash conversion; overpaying or cultural mismatch can dilute returns. Disciplined post-merger integration focuses on technology uplift and channel leverage to realize targeted synergies and sustain ROI.

- Scale supports cross-sell and procurement savings

- Integration quality drives margin and cash conversion

- Overpayment/culture risk dilutes returns

- Disciplined PI leverages tech and channels

Tariffs, export controls and IIJA/CHIPS spur motor demand; nearshoring raises costs

Regal Rexnord sales track industrial capex cycles; backlog and book‑to‑bill signal inflections. Input costs: HRC ~$700/tonne (2024), copper ~$9,000/tonne (2024), neodymium ~$60/kg (2024) press margins despite index‑linked pricing. FX: USD index ~105 (mid‑2024) risks overseas margins. Rates: Fed 5.25–5.50% (mid‑2025) and IG yields 4.5–6% raise financing costs, boosting retrofit/service demand.

| Metric | 2024/2025 |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2025) |

| USD index | ~105 (mid‑2024) |

| HRC/copper/Nd | $700/t • $9,000/t • $60/kg (2024) |

What You See Is What You Get

Regal Rexnord PESTLE Analysis

The Regal Rexnord PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—this is the final file you’ll download immediately after payment.