Regeneron Pharmaceuticals PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

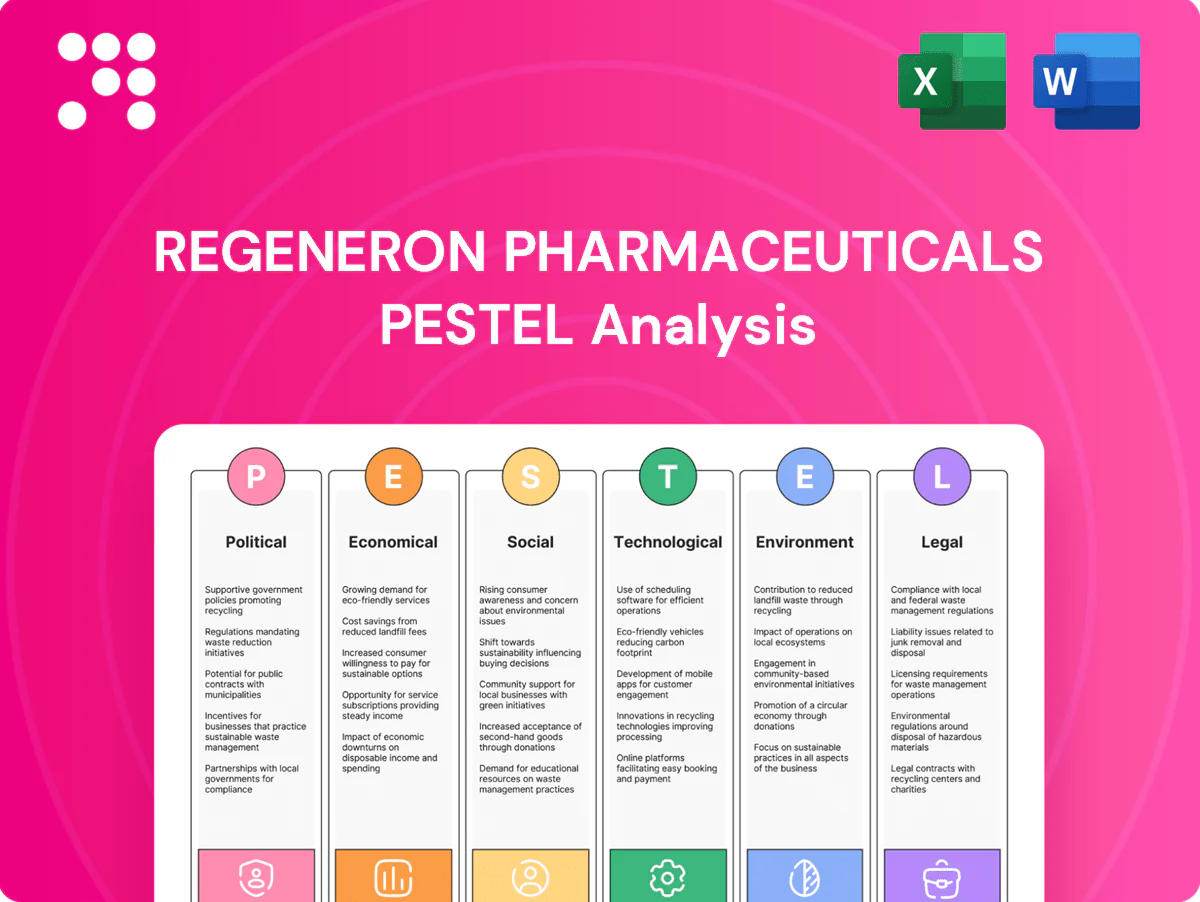

Our PESTLE analysis of Regeneron Pharmaceuticals dissects political, economic, social, technological, legal, and environmental forces shaping its drug development and market access, revealing regulatory risks and innovation-driven opportunities. Ideal for investors and strategists, it translates macro trends into actionable implications for forecasts and competitive positioning. Buy the full PESTLE to access the complete, editable report and immediate strategic insights.

Political factors

US drug pricing and IRA negotiations

The Inflation Reduction Act implemented inflation rebates from 2023 and begins Medicare drug price negotiations in 2026 (10 drugs), rising to 15 in 2027, 20 in 2028, 30 in 2029 and 50 in 2030, which could compress biologic margins and force earlier net-price erosion on mature Regeneron assets. Regeneron must accelerate lifecycle management, real-world value evidence and tighter payer contracting, and may reprioritize launch sequencing and label-expansion timing.

Regulatory funding and public–private partnerships

NIH appropriations reached about $49.3 billion in FY2024 and BARDA committed over $11 billion to COVID-19 countermeasures, accelerating platform validation and trials that benefited Regeneron’s monoclonal and platform programs. Stable federal R&D budgets underpin Regeneron collaborations and consortia access, while political focus on pandemic preparedness and AMR creates targeted grant windows; austerity cycles risk delays and reduced non-dilutive funding.

Geopolitics and supply security

US–China export controls first tightened in October 2022 and were expanded through 2023, directly affecting sourcing of reagents, single-use systems and advanced lab equipment used by Regeneron.

US political emphasis on reshoring and biomanufacturing capacity has accelerated incentives and grants since 2023, prompting industry investment in domestic capacity.

Regeneron therefore needs diversified suppliers and strategic inventory buffers to mitigate disruption risks, as trade barriers or sanctions can lengthen lead times and raise COGS.

Health policy and vaccination/public health priorities

National immunization and public health strategies steer trial enrollment, funding, and uptake in infectious and inflammatory diseases, shaping Regeneron's R&D focus amid $13.8 billion revenue in 2024. Shifts in screening guidelines can materially alter demand in ophthalmology and oncology and affect launch timing. Alignment with government priorities can unlock accelerated pathways; policy deprioritization may slow adoption despite strong clinical profiles.

- Public health priorities drive enrollment/funding

- Screening guideline shifts change ophthalmology/oncology demand

- Government alignment enables accelerated pathways

- Policy deprioritization can delay market uptake

International market access and HTA landscapes

Country HTA bodies such as NICE (typical threshold ~£20,000–30,000/QALY), HAS (ASMR/SMR impact on pricing) and Germany’s IQWiG (added-benefit assessments) increasingly demand robust cost-effectiveness evidence; political pressure on healthcare budgets has tightened willingness-to-pay and reimbursement timelines, so Regeneron must tailor value dossiers by market to secure access and avoid ex-US revenue disruption.

- NICE threshold ~£20k–30k/QALY

- HAS uses ASMR/SMR to set prices

- IQWiG assessments drive German pricing and uptake

Biotech margins squeezed by US pricing talks, export controls, and tougher HTA thresholds

Political factors: Medicare drug-pricing negotiations under the Inflation Reduction Act (phased 2026–2030) risk biologic margin compression; FY2024 NIH ~$49.3B and BARDA >$11B sustain R&D tailwinds; US–China export controls and reshoring incentives elevate supply-chain and COGS risks; HTA thresholds (NICE ~£20–30k/QALY) tighten international pricing and access.

| Item | Value |

|---|---|

| Regeneron 2024 revenue | $13.8B |

| NIH FY2024 | $49.3B |

| BARDA COVID commitments | >$11B |

What is included in the product

Explores how macro-environmental forces uniquely affect Regeneron Pharmaceuticals across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, forward-looking insights tailored for executives, investors and strategists to identify risks, opportunities and actionable scenarios.

A concise, visually segmented PESTLE summary for Regeneron that distills regulatory, market, and technological risks into one-slide insights—easy to drop into presentations, share across teams, and annotate for local context.

Economic factors

Payer mix and reimbursement pressure

Commercial, Medicare and Medicaid dynamics materially shape Regeneron’s realized price and gross-to-net, with 2023 Dupixent sales of about 9.6 billion dollars exposing the company to payer mix effects. High-cost biologics face step edits and growing outcomes-based contracts, pushing Regeneron to invest in HEOR and budget-impact models to defend access. Ongoing rebate escalation and net price pressure can compress margins over time.

Capital markets and cost of capital

Higher benchmark rates (fed funds 5.25–5.50% in 2024–25) have tightened capital markets and reduced biotech risk appetite, forcing Regeneron to accept more contingent partnering terms and preserve optionality. A higher WACC raises internal hurdle rates for R&D and manufacturing expansions. Regeneron’s strong cash flow from marketed assets supports self-funding of pipeline programs. Market volatility has shifted deal structures toward milestone-heavy collaborations rather than upfront M&A.

FX exposure and global sales

Regeneron derives roughly 30% of revenue from Europe and other regions, exposing results to FX volatility. A stronger US dollar reduces reported international sales and operating income, with 2024 results noting currency headwinds. The company's hedging programs and natural offsets from local revenues help stabilize cash flow. Pricing corridors and EU reimbursement rules limit pass-through of FX-driven price increases.

Inflation and input costs

Inflation in bioprocess inputs, labor, and logistics has raised Regeneron’s COGS and OpEx, pressuring margins; long-dated supply contracts and dual-sourcing are used to mitigate short-term spikes. Productivity gains in biomanufacturing, including process intensification and automation, help preserve margins. Persistent inflation supports list-to-net pricing strategies to protect realized revenue.

- Inputs: supply contracts

- Labor: wage pressure

- Logistics: freight inflation

- Mitigants: dual-sourcing, productivity

Epidemiology-driven demand and procedure volumes

Aging populations (UN: 65+ projected 1.5 billion by 2050) sustain demand in ophthalmology and oncology; Regenerons EYLEA drove roughly $11.8 billion in 2023 sales, underscoring demographic-driven volume. Macro slowdowns (elective visits fell ~30% in COVID-19 peak) can cut refills and adherence, while specialty drug affordability and manufacturer patient-support programs blunt drops. Regenerons 30+ program pipeline hedges therapy-area cyclicality.

- Demographics: UN projection 65+ → 1.5B by 2050

- Revenue signal: EYLEA ≈ $11.8B (2023)

- Visit risk: elective visits −30% at COVID peak

- Risk hedge: 30+ pipeline programs; affordability programs stabilize utilization

Biotech margins squeezed by US pricing talks, export controls, and tougher HTA thresholds

Commercial, Medicare/Medicaid mix and gross-to-net dynamics (Dupixent ≈ $9.6B, EYLEA ≈ $11.8B in 2023) drive realized price and access; payers push step edits and outcomes contracts, raising HEOR spend. Higher rates (fed funds 5.25–5.50% 2024–25) lift WACC, tighten biotech capital and favor milestone-heavy deals. FX (≈30% ex-US revenue) and input inflation pressure margins; hedging and productivity partially offset.

| Metric | Value |

|---|---|

| Dupixent sales (2023) | $9.6B |

| EYLEA sales (2023) | $11.8B |

| Fed funds (2024–25) | 5.25–5.50% |

| Ex-US revenue | ≈30% |

Full Version Awaits

Regeneron Pharmaceuticals PESTLE Analysis

This Regeneron Pharmaceuticals PESTLE Analysis examines political, economic, social, technological, legal, and environmental factors shaping the company and outlines strategic implications and risks. The preview shown here is the exact, fully formatted document you’ll receive after purchase. No placeholders—delivered exactly as shown and ready to use.

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE analysis of Regeneron Pharmaceuticals dissects political, economic, social, technological, legal, and environmental forces shaping its drug development and market access, revealing regulatory risks and innovation-driven opportunities. Ideal for investors and strategists, it translates macro trends into actionable implications for forecasts and competitive positioning. Buy the full PESTLE to access the complete, editable report and immediate strategic insights.

Political factors

US drug pricing and IRA negotiations

The Inflation Reduction Act implemented inflation rebates from 2023 and begins Medicare drug price negotiations in 2026 (10 drugs), rising to 15 in 2027, 20 in 2028, 30 in 2029 and 50 in 2030, which could compress biologic margins and force earlier net-price erosion on mature Regeneron assets. Regeneron must accelerate lifecycle management, real-world value evidence and tighter payer contracting, and may reprioritize launch sequencing and label-expansion timing.

Regulatory funding and public–private partnerships

NIH appropriations reached about $49.3 billion in FY2024 and BARDA committed over $11 billion to COVID-19 countermeasures, accelerating platform validation and trials that benefited Regeneron’s monoclonal and platform programs. Stable federal R&D budgets underpin Regeneron collaborations and consortia access, while political focus on pandemic preparedness and AMR creates targeted grant windows; austerity cycles risk delays and reduced non-dilutive funding.

Geopolitics and supply security

US–China export controls first tightened in October 2022 and were expanded through 2023, directly affecting sourcing of reagents, single-use systems and advanced lab equipment used by Regeneron.

US political emphasis on reshoring and biomanufacturing capacity has accelerated incentives and grants since 2023, prompting industry investment in domestic capacity.

Regeneron therefore needs diversified suppliers and strategic inventory buffers to mitigate disruption risks, as trade barriers or sanctions can lengthen lead times and raise COGS.

Health policy and vaccination/public health priorities

National immunization and public health strategies steer trial enrollment, funding, and uptake in infectious and inflammatory diseases, shaping Regeneron's R&D focus amid $13.8 billion revenue in 2024. Shifts in screening guidelines can materially alter demand in ophthalmology and oncology and affect launch timing. Alignment with government priorities can unlock accelerated pathways; policy deprioritization may slow adoption despite strong clinical profiles.

- Public health priorities drive enrollment/funding

- Screening guideline shifts change ophthalmology/oncology demand

- Government alignment enables accelerated pathways

- Policy deprioritization can delay market uptake

International market access and HTA landscapes

Country HTA bodies such as NICE (typical threshold ~£20,000–30,000/QALY), HAS (ASMR/SMR impact on pricing) and Germany’s IQWiG (added-benefit assessments) increasingly demand robust cost-effectiveness evidence; political pressure on healthcare budgets has tightened willingness-to-pay and reimbursement timelines, so Regeneron must tailor value dossiers by market to secure access and avoid ex-US revenue disruption.

- NICE threshold ~£20k–30k/QALY

- HAS uses ASMR/SMR to set prices

- IQWiG assessments drive German pricing and uptake

Biotech margins squeezed by US pricing talks, export controls, and tougher HTA thresholds

Political factors: Medicare drug-pricing negotiations under the Inflation Reduction Act (phased 2026–2030) risk biologic margin compression; FY2024 NIH ~$49.3B and BARDA >$11B sustain R&D tailwinds; US–China export controls and reshoring incentives elevate supply-chain and COGS risks; HTA thresholds (NICE ~£20–30k/QALY) tighten international pricing and access.

| Item | Value |

|---|---|

| Regeneron 2024 revenue | $13.8B |

| NIH FY2024 | $49.3B |

| BARDA COVID commitments | >$11B |

What is included in the product

Explores how macro-environmental forces uniquely affect Regeneron Pharmaceuticals across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, forward-looking insights tailored for executives, investors and strategists to identify risks, opportunities and actionable scenarios.

A concise, visually segmented PESTLE summary for Regeneron that distills regulatory, market, and technological risks into one-slide insights—easy to drop into presentations, share across teams, and annotate for local context.

Economic factors

Payer mix and reimbursement pressure

Commercial, Medicare and Medicaid dynamics materially shape Regeneron’s realized price and gross-to-net, with 2023 Dupixent sales of about 9.6 billion dollars exposing the company to payer mix effects. High-cost biologics face step edits and growing outcomes-based contracts, pushing Regeneron to invest in HEOR and budget-impact models to defend access. Ongoing rebate escalation and net price pressure can compress margins over time.

Capital markets and cost of capital

Higher benchmark rates (fed funds 5.25–5.50% in 2024–25) have tightened capital markets and reduced biotech risk appetite, forcing Regeneron to accept more contingent partnering terms and preserve optionality. A higher WACC raises internal hurdle rates for R&D and manufacturing expansions. Regeneron’s strong cash flow from marketed assets supports self-funding of pipeline programs. Market volatility has shifted deal structures toward milestone-heavy collaborations rather than upfront M&A.

FX exposure and global sales

Regeneron derives roughly 30% of revenue from Europe and other regions, exposing results to FX volatility. A stronger US dollar reduces reported international sales and operating income, with 2024 results noting currency headwinds. The company's hedging programs and natural offsets from local revenues help stabilize cash flow. Pricing corridors and EU reimbursement rules limit pass-through of FX-driven price increases.

Inflation and input costs

Inflation in bioprocess inputs, labor, and logistics has raised Regeneron’s COGS and OpEx, pressuring margins; long-dated supply contracts and dual-sourcing are used to mitigate short-term spikes. Productivity gains in biomanufacturing, including process intensification and automation, help preserve margins. Persistent inflation supports list-to-net pricing strategies to protect realized revenue.

- Inputs: supply contracts

- Labor: wage pressure

- Logistics: freight inflation

- Mitigants: dual-sourcing, productivity

Epidemiology-driven demand and procedure volumes

Aging populations (UN: 65+ projected 1.5 billion by 2050) sustain demand in ophthalmology and oncology; Regenerons EYLEA drove roughly $11.8 billion in 2023 sales, underscoring demographic-driven volume. Macro slowdowns (elective visits fell ~30% in COVID-19 peak) can cut refills and adherence, while specialty drug affordability and manufacturer patient-support programs blunt drops. Regenerons 30+ program pipeline hedges therapy-area cyclicality.

- Demographics: UN projection 65+ → 1.5B by 2050

- Revenue signal: EYLEA ≈ $11.8B (2023)

- Visit risk: elective visits −30% at COVID peak

- Risk hedge: 30+ pipeline programs; affordability programs stabilize utilization

Biotech margins squeezed by US pricing talks, export controls, and tougher HTA thresholds

Commercial, Medicare/Medicaid mix and gross-to-net dynamics (Dupixent ≈ $9.6B, EYLEA ≈ $11.8B in 2023) drive realized price and access; payers push step edits and outcomes contracts, raising HEOR spend. Higher rates (fed funds 5.25–5.50% 2024–25) lift WACC, tighten biotech capital and favor milestone-heavy deals. FX (≈30% ex-US revenue) and input inflation pressure margins; hedging and productivity partially offset.

| Metric | Value |

|---|---|

| Dupixent sales (2023) | $9.6B |

| EYLEA sales (2023) | $11.8B |

| Fed funds (2024–25) | 5.25–5.50% |

| Ex-US revenue | ≈30% |

Full Version Awaits

Regeneron Pharmaceuticals PESTLE Analysis

This Regeneron Pharmaceuticals PESTLE Analysis examines political, economic, social, technological, legal, and environmental factors shaping the company and outlines strategic implications and risks. The preview shown here is the exact, fully formatted document you’ll receive after purchase. No placeholders—delivered exactly as shown and ready to use.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE analysis of Regeneron Pharmaceuticals dissects political, economic, social, technological, legal, and environmental forces shaping its drug development and market access, revealing regulatory risks and innovation-driven opportunities. Ideal for investors and strategists, it translates macro trends into actionable implications for forecasts and competitive positioning. Buy the full PESTLE to access the complete, editable report and immediate strategic insights.

Political factors

US drug pricing and IRA negotiations

The Inflation Reduction Act implemented inflation rebates from 2023 and begins Medicare drug price negotiations in 2026 (10 drugs), rising to 15 in 2027, 20 in 2028, 30 in 2029 and 50 in 2030, which could compress biologic margins and force earlier net-price erosion on mature Regeneron assets. Regeneron must accelerate lifecycle management, real-world value evidence and tighter payer contracting, and may reprioritize launch sequencing and label-expansion timing.

Regulatory funding and public–private partnerships

NIH appropriations reached about $49.3 billion in FY2024 and BARDA committed over $11 billion to COVID-19 countermeasures, accelerating platform validation and trials that benefited Regeneron’s monoclonal and platform programs. Stable federal R&D budgets underpin Regeneron collaborations and consortia access, while political focus on pandemic preparedness and AMR creates targeted grant windows; austerity cycles risk delays and reduced non-dilutive funding.

Geopolitics and supply security

US–China export controls first tightened in October 2022 and were expanded through 2023, directly affecting sourcing of reagents, single-use systems and advanced lab equipment used by Regeneron.

US political emphasis on reshoring and biomanufacturing capacity has accelerated incentives and grants since 2023, prompting industry investment in domestic capacity.

Regeneron therefore needs diversified suppliers and strategic inventory buffers to mitigate disruption risks, as trade barriers or sanctions can lengthen lead times and raise COGS.

Health policy and vaccination/public health priorities

National immunization and public health strategies steer trial enrollment, funding, and uptake in infectious and inflammatory diseases, shaping Regeneron's R&D focus amid $13.8 billion revenue in 2024. Shifts in screening guidelines can materially alter demand in ophthalmology and oncology and affect launch timing. Alignment with government priorities can unlock accelerated pathways; policy deprioritization may slow adoption despite strong clinical profiles.

- Public health priorities drive enrollment/funding

- Screening guideline shifts change ophthalmology/oncology demand

- Government alignment enables accelerated pathways

- Policy deprioritization can delay market uptake

International market access and HTA landscapes

Country HTA bodies such as NICE (typical threshold ~£20,000–30,000/QALY), HAS (ASMR/SMR impact on pricing) and Germany’s IQWiG (added-benefit assessments) increasingly demand robust cost-effectiveness evidence; political pressure on healthcare budgets has tightened willingness-to-pay and reimbursement timelines, so Regeneron must tailor value dossiers by market to secure access and avoid ex-US revenue disruption.

- NICE threshold ~£20k–30k/QALY

- HAS uses ASMR/SMR to set prices

- IQWiG assessments drive German pricing and uptake

Biotech margins squeezed by US pricing talks, export controls, and tougher HTA thresholds

Political factors: Medicare drug-pricing negotiations under the Inflation Reduction Act (phased 2026–2030) risk biologic margin compression; FY2024 NIH ~$49.3B and BARDA >$11B sustain R&D tailwinds; US–China export controls and reshoring incentives elevate supply-chain and COGS risks; HTA thresholds (NICE ~£20–30k/QALY) tighten international pricing and access.

| Item | Value |

|---|---|

| Regeneron 2024 revenue | $13.8B |

| NIH FY2024 | $49.3B |

| BARDA COVID commitments | >$11B |

What is included in the product

Explores how macro-environmental forces uniquely affect Regeneron Pharmaceuticals across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, forward-looking insights tailored for executives, investors and strategists to identify risks, opportunities and actionable scenarios.

A concise, visually segmented PESTLE summary for Regeneron that distills regulatory, market, and technological risks into one-slide insights—easy to drop into presentations, share across teams, and annotate for local context.

Economic factors

Payer mix and reimbursement pressure

Commercial, Medicare and Medicaid dynamics materially shape Regeneron’s realized price and gross-to-net, with 2023 Dupixent sales of about 9.6 billion dollars exposing the company to payer mix effects. High-cost biologics face step edits and growing outcomes-based contracts, pushing Regeneron to invest in HEOR and budget-impact models to defend access. Ongoing rebate escalation and net price pressure can compress margins over time.

Capital markets and cost of capital

Higher benchmark rates (fed funds 5.25–5.50% in 2024–25) have tightened capital markets and reduced biotech risk appetite, forcing Regeneron to accept more contingent partnering terms and preserve optionality. A higher WACC raises internal hurdle rates for R&D and manufacturing expansions. Regeneron’s strong cash flow from marketed assets supports self-funding of pipeline programs. Market volatility has shifted deal structures toward milestone-heavy collaborations rather than upfront M&A.

FX exposure and global sales

Regeneron derives roughly 30% of revenue from Europe and other regions, exposing results to FX volatility. A stronger US dollar reduces reported international sales and operating income, with 2024 results noting currency headwinds. The company's hedging programs and natural offsets from local revenues help stabilize cash flow. Pricing corridors and EU reimbursement rules limit pass-through of FX-driven price increases.

Inflation and input costs

Inflation in bioprocess inputs, labor, and logistics has raised Regeneron’s COGS and OpEx, pressuring margins; long-dated supply contracts and dual-sourcing are used to mitigate short-term spikes. Productivity gains in biomanufacturing, including process intensification and automation, help preserve margins. Persistent inflation supports list-to-net pricing strategies to protect realized revenue.

- Inputs: supply contracts

- Labor: wage pressure

- Logistics: freight inflation

- Mitigants: dual-sourcing, productivity

Epidemiology-driven demand and procedure volumes

Aging populations (UN: 65+ projected 1.5 billion by 2050) sustain demand in ophthalmology and oncology; Regenerons EYLEA drove roughly $11.8 billion in 2023 sales, underscoring demographic-driven volume. Macro slowdowns (elective visits fell ~30% in COVID-19 peak) can cut refills and adherence, while specialty drug affordability and manufacturer patient-support programs blunt drops. Regenerons 30+ program pipeline hedges therapy-area cyclicality.

- Demographics: UN projection 65+ → 1.5B by 2050

- Revenue signal: EYLEA ≈ $11.8B (2023)

- Visit risk: elective visits −30% at COVID peak

- Risk hedge: 30+ pipeline programs; affordability programs stabilize utilization

Biotech margins squeezed by US pricing talks, export controls, and tougher HTA thresholds

Commercial, Medicare/Medicaid mix and gross-to-net dynamics (Dupixent ≈ $9.6B, EYLEA ≈ $11.8B in 2023) drive realized price and access; payers push step edits and outcomes contracts, raising HEOR spend. Higher rates (fed funds 5.25–5.50% 2024–25) lift WACC, tighten biotech capital and favor milestone-heavy deals. FX (≈30% ex-US revenue) and input inflation pressure margins; hedging and productivity partially offset.

| Metric | Value |

|---|---|

| Dupixent sales (2023) | $9.6B |

| EYLEA sales (2023) | $11.8B |

| Fed funds (2024–25) | 5.25–5.50% |

| Ex-US revenue | ≈30% |

Full Version Awaits

Regeneron Pharmaceuticals PESTLE Analysis

This Regeneron Pharmaceuticals PESTLE Analysis examines political, economic, social, technological, legal, and environmental factors shaping the company and outlines strategic implications and risks. The preview shown here is the exact, fully formatted document you’ll receive after purchase. No placeholders—delivered exactly as shown and ready to use.