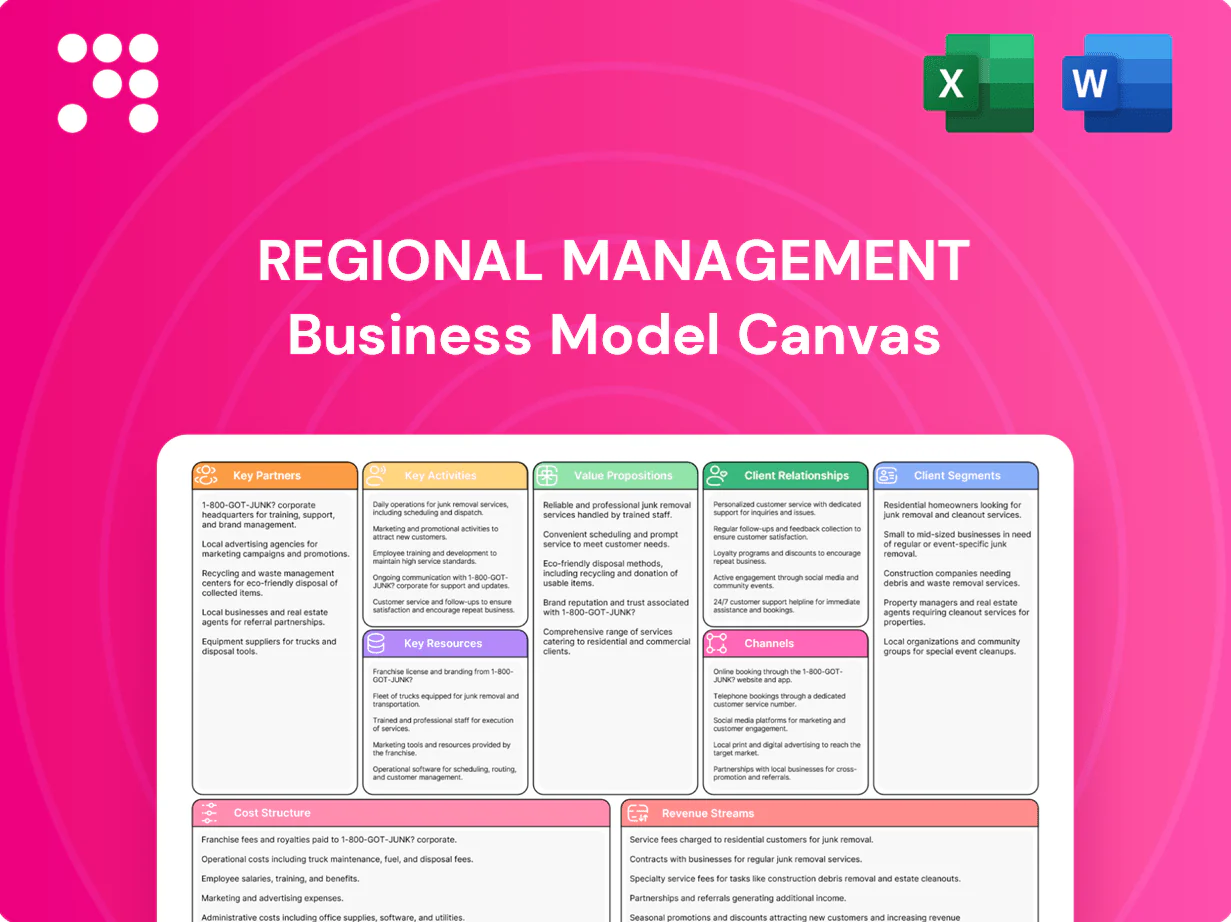

Regional Management Business Model Canvas

Unlock a strategic Business Model Canvas for regional lenders — actionable insights & toolkit

Unlock the full strategic blueprint behind Regional Management's business model. This in-depth Business Model Canvas reveals how the company drives value, captures market share, and stays ahead in a competitive landscape. Ideal for entrepreneurs, consultants, and investors seeking actionable insights—download the complete Word/Excel canvas to benchmark, plan, and present with confidence.

Partnerships

Banking and Capital Markets Lenders

Regional Management partners with banks, credit unions, and institutional lenders to fund loan originations and maintain liquidity, with banks providing roughly two-thirds of external financing to US small businesses in 2024. Warehouse lines and revolvers support seasonal demand and portfolio growth, often covering short-term funding gaps. These partners optimize cost of funds and diversify financing sources, and strong lender ties enable covenant flexibility during credit cycles.

Payment Processors and Fintech Vendors

Third-party processors enable ACH, card and digital-wallet payments, unlocking faster receipts and reducing settlement friction; integrated processors helped firms cut servicing costs by up to 30% in 2024 while the global digital-payments market topped $8 trillion. Fintech vendors add e-signature, ID verification and fraud tools that shorten verification times by as much as 70%. Together these integrations boost repayment success 5–12% and lift customer satisfaction/NPS by ~8 points.

Credit Bureaus and Data Providers

Partnerships with credit bureaus supply credit reports, trended data, and alternative data for underwriting, drawing on roughly 220 million credit-active US consumers (2024). Data providers enhance risk models for near-prime and non-prime cohorts, improving loan approval accuracy and loss forecasting. This richer data mix supports responsible portfolio expansion while managing delinquency and capital allocation.

Retail and Auto Merchants for Sales Financing

Merchants offer point-of-sale installment options financed by Regional Management, creating captive demand that lowers customer acquisition costs and boosts repeat business. Co-marketing at checkout increases conversion rates and average ticket size, while integrated decisioning delivers near-instant approvals and higher customer satisfaction. These merchant partnerships anchor distribution and scale receivables efficiently.

- Captive demand

- Lower acquisition costs

- Higher conversion & ticket size

- Instant approvals & satisfaction

Regulatory and Compliance Advisors

External legal counsel and compliance consultants navigate consumer finance rules across 50 states and DC, supporting policy updates, audits and licensing to keep branches and online channels compliant. Their work reduces regulatory risk and operational interruptions while ensuring disclosure accuracy and adherence to fair lending practices under federal and state regimes. This centralized expertise scales across the regional footprint.

- Coverage: 50 states + DC

- Services: policy updates, audits, licensing

- Outcomes: reduced regulatory risk, accurate disclosures, fair lending compliance

Regional finance: 66% bank funding; 220M consumer access

Regional Management relies on banks/credit unions for ~66% of external funding (2024), uses warehouse lines for seasonality, and leverages processors and fintechs that cut servicing costs up to 30% and supported a global $8T digital-payments market (2024). Credit bureau access across ~220M credit-active US consumers improves underwriting for near/non-prime segments. Legal/compliance coverage spans 50 states + DC, reducing regulatory risk.

| Partner | Role | 2024 metric |

|---|---|---|

| Banks/Lenders | Funding/liquidity | ~66% of SMB external finance |

| Processors/Fintech | Payments/ID/fraud | Servicing cost ↓ up to 30% |

| Credit Bureaus | Data for underwriting | ~220M credit-active consumers |

| Legal/Compliance | Regulatory coverage | 50 states + DC |

What is included in the product

A comprehensive Business Model Canvas tailored to Regional Management’s strategy, covering nine BMC blocks with detailed narratives on value propositions, customer segments, channels, revenue streams, key activities and resources. Includes SWOT-linked insights, competitive advantages and a polished design for presentations and funding discussions.

High-level view of the regional management business model with editable cells for local adaptation; quickly identify core components to streamline operations and align regional strategy. Great for comparing territories, sharing with teams, and saving hours on structuring tailored plans.

Activities

Risk-Based Underwriting and Pricing

The company assesses creditworthiness using bureau data, income verification, and alternative data increasingly adopted by lenders in 2024. Loans are priced by risk tiers, collateral and term, targeting portfolio yields of 8–12% with expected loss rates of 2–4%. Continuous model monitoring adapts to macro shifts (inflation, unemployment) and regulatory changes. This approach balances approval rates against yield and losses.

Loan Origination and Servicing

End-to-end loan origination covers application, verification, funding and payment management, with digital origination accounting for about 55% of new loans in 2024. Servicing handles collections, extensions and restructures, with restructuring rates near 2.8% in 2024. Omnichannel tools support in-branch and digital flows, and automation has cut servicing costs by up to 30%, improving CX and margin control.

Branch Network Operations

Branches execute local customer acquisition, underwriting, and relationship servicing while field teams drive community outreach and referral generation. Regional managers monitor compliance, credit performance, and operational KPIs across branches. Physical branch presence builds trust with underbanked populations; 1.4 billion adults remained unbanked per World Bank Global Findex 2021.

Collections and Loss Mitigation

Collections and loss mitigation rely on proactive reminders, tailored hardship plans and structured collections to reduce charge-offs; 2024 benchmarks show reminders cut early delinquencies ~12–20% and hardship plans lower charge-offs ~10–15%. Segmentation by risk and behavior lifts recovery rates ~8–12%, while digital self-cure tools increase cure rates ~20–30% and lower cost-to-collect ~25–35%. Continuous feedback loops refine underwriting and reduced default rates ~4–6%.

- Proactive reminders: delinquencies -12–20%

- Hardship plans: charge-offs -10–15%

- Segmentation: recovery +8–12%

- Digital self-cure: cure +20–30%, cost-to-collect -25–35%

- Feedback loops: default -4–6%

Regulatory Compliance and Reporting

Regional credit targets 8–12% yield, 2–4% loss, 55% digital

Regional management executes credit assessment, pricing and continuous model monitoring to target portfolio yields of 8–12% with expected losses of 2–4% (2024). End-to-end origination and servicing—55% digital in 2024—reduce costs and improve CX; restructures ~2.8%. Collections use reminders, hardship plans and segmentation to cut delinquencies and charge-offs.

| KPI | 2024 | Target |

|---|---|---|

| Digital origination | 55% | 60% |

| Portfolio yield | 8–12% | 9–11% |

| Expected loss | 2–4% | ≤3% |

| Restructure rate | 2.8% | ≤3% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Regional Management Business Model Canvas you will receive—no mockup or sample. Upon purchase you'll get this exact file, fully formatted and editable in Word and Excel. It’s ready for immediate use in planning, presenting, and implementation.

Unlock a strategic Business Model Canvas for regional lenders — actionable insights & toolkit

Unlock the full strategic blueprint behind Regional Management's business model. This in-depth Business Model Canvas reveals how the company drives value, captures market share, and stays ahead in a competitive landscape. Ideal for entrepreneurs, consultants, and investors seeking actionable insights—download the complete Word/Excel canvas to benchmark, plan, and present with confidence.

Partnerships

Banking and Capital Markets Lenders

Regional Management partners with banks, credit unions, and institutional lenders to fund loan originations and maintain liquidity, with banks providing roughly two-thirds of external financing to US small businesses in 2024. Warehouse lines and revolvers support seasonal demand and portfolio growth, often covering short-term funding gaps. These partners optimize cost of funds and diversify financing sources, and strong lender ties enable covenant flexibility during credit cycles.

Payment Processors and Fintech Vendors

Third-party processors enable ACH, card and digital-wallet payments, unlocking faster receipts and reducing settlement friction; integrated processors helped firms cut servicing costs by up to 30% in 2024 while the global digital-payments market topped $8 trillion. Fintech vendors add e-signature, ID verification and fraud tools that shorten verification times by as much as 70%. Together these integrations boost repayment success 5–12% and lift customer satisfaction/NPS by ~8 points.

Credit Bureaus and Data Providers

Partnerships with credit bureaus supply credit reports, trended data, and alternative data for underwriting, drawing on roughly 220 million credit-active US consumers (2024). Data providers enhance risk models for near-prime and non-prime cohorts, improving loan approval accuracy and loss forecasting. This richer data mix supports responsible portfolio expansion while managing delinquency and capital allocation.

Retail and Auto Merchants for Sales Financing

Merchants offer point-of-sale installment options financed by Regional Management, creating captive demand that lowers customer acquisition costs and boosts repeat business. Co-marketing at checkout increases conversion rates and average ticket size, while integrated decisioning delivers near-instant approvals and higher customer satisfaction. These merchant partnerships anchor distribution and scale receivables efficiently.

- Captive demand

- Lower acquisition costs

- Higher conversion & ticket size

- Instant approvals & satisfaction

Regulatory and Compliance Advisors

External legal counsel and compliance consultants navigate consumer finance rules across 50 states and DC, supporting policy updates, audits and licensing to keep branches and online channels compliant. Their work reduces regulatory risk and operational interruptions while ensuring disclosure accuracy and adherence to fair lending practices under federal and state regimes. This centralized expertise scales across the regional footprint.

- Coverage: 50 states + DC

- Services: policy updates, audits, licensing

- Outcomes: reduced regulatory risk, accurate disclosures, fair lending compliance

Regional finance: 66% bank funding; 220M consumer access

Regional Management relies on banks/credit unions for ~66% of external funding (2024), uses warehouse lines for seasonality, and leverages processors and fintechs that cut servicing costs up to 30% and supported a global $8T digital-payments market (2024). Credit bureau access across ~220M credit-active US consumers improves underwriting for near/non-prime segments. Legal/compliance coverage spans 50 states + DC, reducing regulatory risk.

| Partner | Role | 2024 metric |

|---|---|---|

| Banks/Lenders | Funding/liquidity | ~66% of SMB external finance |

| Processors/Fintech | Payments/ID/fraud | Servicing cost ↓ up to 30% |

| Credit Bureaus | Data for underwriting | ~220M credit-active consumers |

| Legal/Compliance | Regulatory coverage | 50 states + DC |

What is included in the product

A comprehensive Business Model Canvas tailored to Regional Management’s strategy, covering nine BMC blocks with detailed narratives on value propositions, customer segments, channels, revenue streams, key activities and resources. Includes SWOT-linked insights, competitive advantages and a polished design for presentations and funding discussions.

High-level view of the regional management business model with editable cells for local adaptation; quickly identify core components to streamline operations and align regional strategy. Great for comparing territories, sharing with teams, and saving hours on structuring tailored plans.

Activities

Risk-Based Underwriting and Pricing

The company assesses creditworthiness using bureau data, income verification, and alternative data increasingly adopted by lenders in 2024. Loans are priced by risk tiers, collateral and term, targeting portfolio yields of 8–12% with expected loss rates of 2–4%. Continuous model monitoring adapts to macro shifts (inflation, unemployment) and regulatory changes. This approach balances approval rates against yield and losses.

Loan Origination and Servicing

End-to-end loan origination covers application, verification, funding and payment management, with digital origination accounting for about 55% of new loans in 2024. Servicing handles collections, extensions and restructures, with restructuring rates near 2.8% in 2024. Omnichannel tools support in-branch and digital flows, and automation has cut servicing costs by up to 30%, improving CX and margin control.

Branch Network Operations

Branches execute local customer acquisition, underwriting, and relationship servicing while field teams drive community outreach and referral generation. Regional managers monitor compliance, credit performance, and operational KPIs across branches. Physical branch presence builds trust with underbanked populations; 1.4 billion adults remained unbanked per World Bank Global Findex 2021.

Collections and Loss Mitigation

Collections and loss mitigation rely on proactive reminders, tailored hardship plans and structured collections to reduce charge-offs; 2024 benchmarks show reminders cut early delinquencies ~12–20% and hardship plans lower charge-offs ~10–15%. Segmentation by risk and behavior lifts recovery rates ~8–12%, while digital self-cure tools increase cure rates ~20–30% and lower cost-to-collect ~25–35%. Continuous feedback loops refine underwriting and reduced default rates ~4–6%.

- Proactive reminders: delinquencies -12–20%

- Hardship plans: charge-offs -10–15%

- Segmentation: recovery +8–12%

- Digital self-cure: cure +20–30%, cost-to-collect -25–35%

- Feedback loops: default -4–6%

Regulatory Compliance and Reporting

Regional credit targets 8–12% yield, 2–4% loss, 55% digital

Regional management executes credit assessment, pricing and continuous model monitoring to target portfolio yields of 8–12% with expected losses of 2–4% (2024). End-to-end origination and servicing—55% digital in 2024—reduce costs and improve CX; restructures ~2.8%. Collections use reminders, hardship plans and segmentation to cut delinquencies and charge-offs.

| KPI | 2024 | Target |

|---|---|---|

| Digital origination | 55% | 60% |

| Portfolio yield | 8–12% | 9–11% |

| Expected loss | 2–4% | ≤3% |

| Restructure rate | 2.8% | ≤3% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Regional Management Business Model Canvas you will receive—no mockup or sample. Upon purchase you'll get this exact file, fully formatted and editable in Word and Excel. It’s ready for immediate use in planning, presenting, and implementation.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a strategic Business Model Canvas for regional lenders — actionable insights & toolkit

Unlock the full strategic blueprint behind Regional Management's business model. This in-depth Business Model Canvas reveals how the company drives value, captures market share, and stays ahead in a competitive landscape. Ideal for entrepreneurs, consultants, and investors seeking actionable insights—download the complete Word/Excel canvas to benchmark, plan, and present with confidence.

Partnerships

Banking and Capital Markets Lenders

Regional Management partners with banks, credit unions, and institutional lenders to fund loan originations and maintain liquidity, with banks providing roughly two-thirds of external financing to US small businesses in 2024. Warehouse lines and revolvers support seasonal demand and portfolio growth, often covering short-term funding gaps. These partners optimize cost of funds and diversify financing sources, and strong lender ties enable covenant flexibility during credit cycles.

Payment Processors and Fintech Vendors

Third-party processors enable ACH, card and digital-wallet payments, unlocking faster receipts and reducing settlement friction; integrated processors helped firms cut servicing costs by up to 30% in 2024 while the global digital-payments market topped $8 trillion. Fintech vendors add e-signature, ID verification and fraud tools that shorten verification times by as much as 70%. Together these integrations boost repayment success 5–12% and lift customer satisfaction/NPS by ~8 points.

Credit Bureaus and Data Providers

Partnerships with credit bureaus supply credit reports, trended data, and alternative data for underwriting, drawing on roughly 220 million credit-active US consumers (2024). Data providers enhance risk models for near-prime and non-prime cohorts, improving loan approval accuracy and loss forecasting. This richer data mix supports responsible portfolio expansion while managing delinquency and capital allocation.

Retail and Auto Merchants for Sales Financing

Merchants offer point-of-sale installment options financed by Regional Management, creating captive demand that lowers customer acquisition costs and boosts repeat business. Co-marketing at checkout increases conversion rates and average ticket size, while integrated decisioning delivers near-instant approvals and higher customer satisfaction. These merchant partnerships anchor distribution and scale receivables efficiently.

- Captive demand

- Lower acquisition costs

- Higher conversion & ticket size

- Instant approvals & satisfaction

Regulatory and Compliance Advisors

External legal counsel and compliance consultants navigate consumer finance rules across 50 states and DC, supporting policy updates, audits and licensing to keep branches and online channels compliant. Their work reduces regulatory risk and operational interruptions while ensuring disclosure accuracy and adherence to fair lending practices under federal and state regimes. This centralized expertise scales across the regional footprint.

- Coverage: 50 states + DC

- Services: policy updates, audits, licensing

- Outcomes: reduced regulatory risk, accurate disclosures, fair lending compliance

Regional finance: 66% bank funding; 220M consumer access

Regional Management relies on banks/credit unions for ~66% of external funding (2024), uses warehouse lines for seasonality, and leverages processors and fintechs that cut servicing costs up to 30% and supported a global $8T digital-payments market (2024). Credit bureau access across ~220M credit-active US consumers improves underwriting for near/non-prime segments. Legal/compliance coverage spans 50 states + DC, reducing regulatory risk.

| Partner | Role | 2024 metric |

|---|---|---|

| Banks/Lenders | Funding/liquidity | ~66% of SMB external finance |

| Processors/Fintech | Payments/ID/fraud | Servicing cost ↓ up to 30% |

| Credit Bureaus | Data for underwriting | ~220M credit-active consumers |

| Legal/Compliance | Regulatory coverage | 50 states + DC |

What is included in the product

A comprehensive Business Model Canvas tailored to Regional Management’s strategy, covering nine BMC blocks with detailed narratives on value propositions, customer segments, channels, revenue streams, key activities and resources. Includes SWOT-linked insights, competitive advantages and a polished design for presentations and funding discussions.

High-level view of the regional management business model with editable cells for local adaptation; quickly identify core components to streamline operations and align regional strategy. Great for comparing territories, sharing with teams, and saving hours on structuring tailored plans.

Activities

Risk-Based Underwriting and Pricing

The company assesses creditworthiness using bureau data, income verification, and alternative data increasingly adopted by lenders in 2024. Loans are priced by risk tiers, collateral and term, targeting portfolio yields of 8–12% with expected loss rates of 2–4%. Continuous model monitoring adapts to macro shifts (inflation, unemployment) and regulatory changes. This approach balances approval rates against yield and losses.

Loan Origination and Servicing

End-to-end loan origination covers application, verification, funding and payment management, with digital origination accounting for about 55% of new loans in 2024. Servicing handles collections, extensions and restructures, with restructuring rates near 2.8% in 2024. Omnichannel tools support in-branch and digital flows, and automation has cut servicing costs by up to 30%, improving CX and margin control.

Branch Network Operations

Branches execute local customer acquisition, underwriting, and relationship servicing while field teams drive community outreach and referral generation. Regional managers monitor compliance, credit performance, and operational KPIs across branches. Physical branch presence builds trust with underbanked populations; 1.4 billion adults remained unbanked per World Bank Global Findex 2021.

Collections and Loss Mitigation

Collections and loss mitigation rely on proactive reminders, tailored hardship plans and structured collections to reduce charge-offs; 2024 benchmarks show reminders cut early delinquencies ~12–20% and hardship plans lower charge-offs ~10–15%. Segmentation by risk and behavior lifts recovery rates ~8–12%, while digital self-cure tools increase cure rates ~20–30% and lower cost-to-collect ~25–35%. Continuous feedback loops refine underwriting and reduced default rates ~4–6%.

- Proactive reminders: delinquencies -12–20%

- Hardship plans: charge-offs -10–15%

- Segmentation: recovery +8–12%

- Digital self-cure: cure +20–30%, cost-to-collect -25–35%

- Feedback loops: default -4–6%

Regulatory Compliance and Reporting

Regional credit targets 8–12% yield, 2–4% loss, 55% digital

Regional management executes credit assessment, pricing and continuous model monitoring to target portfolio yields of 8–12% with expected losses of 2–4% (2024). End-to-end origination and servicing—55% digital in 2024—reduce costs and improve CX; restructures ~2.8%. Collections use reminders, hardship plans and segmentation to cut delinquencies and charge-offs.

| KPI | 2024 | Target |

|---|---|---|

| Digital origination | 55% | 60% |

| Portfolio yield | 8–12% | 9–11% |

| Expected loss | 2–4% | ≤3% |

| Restructure rate | 2.8% | ≤3% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Regional Management Business Model Canvas you will receive—no mockup or sample. Upon purchase you'll get this exact file, fully formatted and editable in Word and Excel. It’s ready for immediate use in planning, presenting, and implementation.