Regional Management Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

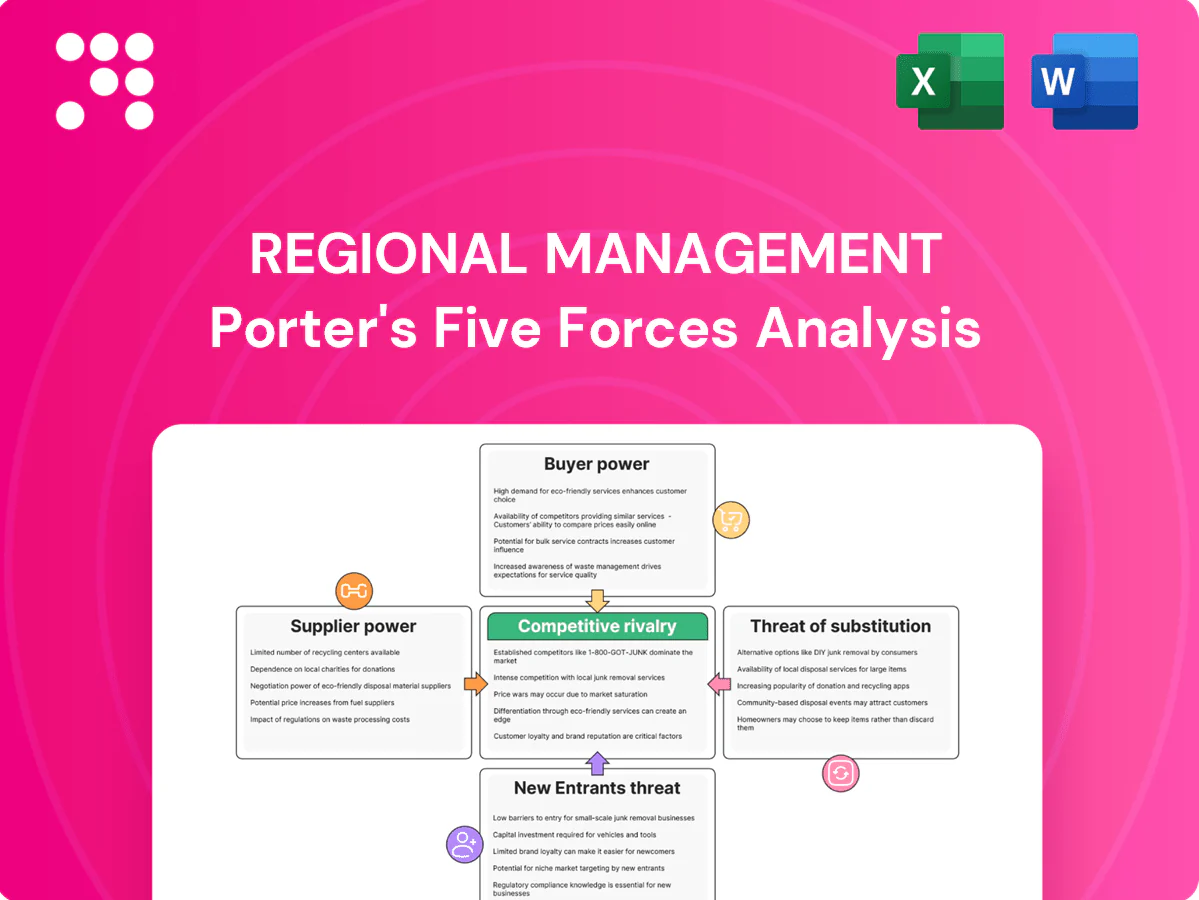

Regional Management faces moderate buyer power, localized supplier relationships, and steady barriers to entry that shape its competitive landscape; competitive rivalry is intensified by similar regional players. This snapshot highlights key pressure points and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategic decisions. Purchase the complete report to access consultant-grade insights tailored to Regional Management.

Suppliers Bargaining Power

Concentrated funding sources

Regional management relies mainly on bank facilities, securitizations and institutional lenders; 2024 saw a tighter CRE funding backdrop per the Federal Reserve. A concentrated creditor pool can dictate covenants, pricing and advance rates, increasing negotiation power. Tight credit cycles in 2023–24 pushed up cost of funds, so diversifying maturities and lender types reduces single-source risk.

Interest rate sensitivity

Rising benchmark rates — federal funds at 5.25–5.50% in 2024 — flow directly into warehouse line pricing and ABS coupons, raising funding costs for regional managers.

When risk appetite falls, suppliers can demand higher spreads and tighter structures, compressing net interest margins unless higher rates are passed to borrowers.

Hedging and locking in fixed-rate funding materially reduce this interest-rate exposure.

Data and credit bureau reliance

Three national credit bureaus and rising alternative data providers are core to underwriting, with the bureaus covering roughly 200 million credit-active US consumers as of 2024. Switching vendors is feasible but often requires months of integration and model recalibration, plus nontrivial IT spend. Vendors can raise access fees or restrict data, degrading score quality; multi-sourcing and proprietary scorecards materially reduce single-vendor dependence.

Technology and servicing vendors

Loan origination, servicing platforms, and payment processors are highly specialized, with payment fees typically 1–3% per transaction and platform SLAs commonly targeting 99.9% uptime, creating vendor leverage and outage risk via lock-in and high switching costs. Negotiating strict SLAs, dual-provider redundancy, and exit clauses reduces supplier operational leverage. Building in-house origination and servicing capabilities improves bargaining power over time.

- Specialization: high technical dependence

- Costs: payment fees ~1–3%

- Risk: vendor lock-in raises switching/outage exposure

- Mitigation: SLAs, redundancy, exit terms

- Strategy: phased in-house build strengthens position

Talent and branch real estate

Experienced credit, collections, and compliance staff remain inelastic in tight labor markets, with the US quits rate at 2.4% in 2024 increasing hiring pressure; landlords in prime locations retain pricing power, keeping core CBD rents elevated. Training pipelines and remote tools cut concentration risk, while performance-based retention reduced turnover costs in 2024 case studies.

- Inelastic talent: quits 2.4% (2024)

- Landlord pricing: prime rents elevated

- Mitigation: training + remote tools

- Retention: performance pay lowers turnover costs

Supplier squeeze 2024: higher funding costs, data lock-in, diversify, hedge, phase builds

Suppliers (banks, ABS investors, bureaus, platforms, talent, landlords) tightened terms in 2023–24 as Fed funds reached 5.25–5.50% in 2024, raising funding and servicing costs. Concentrated lenders and bureau lock‑in increase covenant, pricing and data risks. Mitigants: diversify lenders/vendors, dual providers, hedging and phased in‑house builds.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Banks/ABS | Fed funds 5.25–5.50% | ↑ funding cost |

| Credit bureaus | ~200M consumers | lock‑in/data risk |

| Payments | Fees 1–3% | operating drag |

What is included in the product

Concise Porter's Five Forces analysis for Regional Management that uncovers competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and identifies strategic vulnerabilities and protective dynamics shaping profitability.

A compact regional Porter's Five Forces summary that highlights local competitive pressures and relief strategies—ready to drop into decks, customize for new regulations or entrants, and quickly guide strategic decisions.

Customers Bargaining Power

Fragmented, price-sensitive borrowers

Customers are numerous but highly sensitive to APR, fees, and payment size; in 2024 roughly 70% of retail borrowers compare rates online, and a 0.5–1.0 percentage-point APR difference or a few dollars in monthly payment often shifts lender choice. They shop across online platforms and nearby branches, with approval likelihood as decisive as price. Transparent pricing and tailored terms (flexible payments, fee waivers) improve retention.

Low switching costs

Refinancing or taking a new loan elsewhere is easy with minimal prepayment penalties, and in 2024 about 63% of borrowers used online comparison tools before switching lenders. Digital competitors and aggregators accelerate comparisons and switching, shortening decision cycles. Loyalty is often transactional, driven by speed and approval odds rather than brand. High-touch relationship servicing and tailored cross-sell can raise perceived switching costs for select customer segments.

Limited prime credit access

Many Regional Management customers lack prime credit—FDIC reported 5.4% unbanked and 16.3% underbanked households (2022), which moderates bargaining power versus prime borrowers. Growth of subprime/near-prime alternative lenders expands options and price pressure. Promotional retail financing can temporarily undercut costs and boost conversion. Education and responsible lending improve trust and lower churn.

Regulatory and advocacy pressure

Service and speed expectations

Fast approvals and omnichannel convenience are baseline expectations in 2024, with industry benchmarks moving toward same-day approval and sub-24-hour onboarding; delays push customers to rivals rapidly, increasing churn risk. Streamlined onboarding and underwriting measurably boost perceived value, while integrated branch support plus digital tools can differentiate the customer experience.

- Same-day approvals; sub-24h onboarding

- Delays = rapid churn to competitors

- Streamlined underwriting increases value

- Branch + digital = differentiated experience

Borrowers compare rates: 70% online; 63% used tools

Customers are price- and approval-sensitive: in 2024 ~70% compare rates online and a 0.5–1.0pp APR gap often decides choice. Switching is easy: ~63% used online tools before switching lenders in 2024, shortening decision cycles. Regulatory pressure and complaints (+12% YoY) boost borrower leverage, while fast approvals and tailored terms raise retention.

| Metric | 2024 Value |

|---|---|

| Rate comparison online | 70% |

| Used tools before switching | 63% |

| Complaint growth YoY | +12% |

What You See Is What You Get

Regional Management Porter's Five Forces Analysis

This preview shows the exact Regional Management Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. It is the full, professionally formatted document, ready for download and use the moment you buy. You're viewing the final deliverable and will gain instant access to this same file upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Regional Management faces moderate buyer power, localized supplier relationships, and steady barriers to entry that shape its competitive landscape; competitive rivalry is intensified by similar regional players. This snapshot highlights key pressure points and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategic decisions. Purchase the complete report to access consultant-grade insights tailored to Regional Management.

Suppliers Bargaining Power

Concentrated funding sources

Regional management relies mainly on bank facilities, securitizations and institutional lenders; 2024 saw a tighter CRE funding backdrop per the Federal Reserve. A concentrated creditor pool can dictate covenants, pricing and advance rates, increasing negotiation power. Tight credit cycles in 2023–24 pushed up cost of funds, so diversifying maturities and lender types reduces single-source risk.

Interest rate sensitivity

Rising benchmark rates — federal funds at 5.25–5.50% in 2024 — flow directly into warehouse line pricing and ABS coupons, raising funding costs for regional managers.

When risk appetite falls, suppliers can demand higher spreads and tighter structures, compressing net interest margins unless higher rates are passed to borrowers.

Hedging and locking in fixed-rate funding materially reduce this interest-rate exposure.

Data and credit bureau reliance

Three national credit bureaus and rising alternative data providers are core to underwriting, with the bureaus covering roughly 200 million credit-active US consumers as of 2024. Switching vendors is feasible but often requires months of integration and model recalibration, plus nontrivial IT spend. Vendors can raise access fees or restrict data, degrading score quality; multi-sourcing and proprietary scorecards materially reduce single-vendor dependence.

Technology and servicing vendors

Loan origination, servicing platforms, and payment processors are highly specialized, with payment fees typically 1–3% per transaction and platform SLAs commonly targeting 99.9% uptime, creating vendor leverage and outage risk via lock-in and high switching costs. Negotiating strict SLAs, dual-provider redundancy, and exit clauses reduces supplier operational leverage. Building in-house origination and servicing capabilities improves bargaining power over time.

- Specialization: high technical dependence

- Costs: payment fees ~1–3%

- Risk: vendor lock-in raises switching/outage exposure

- Mitigation: SLAs, redundancy, exit terms

- Strategy: phased in-house build strengthens position

Talent and branch real estate

Experienced credit, collections, and compliance staff remain inelastic in tight labor markets, with the US quits rate at 2.4% in 2024 increasing hiring pressure; landlords in prime locations retain pricing power, keeping core CBD rents elevated. Training pipelines and remote tools cut concentration risk, while performance-based retention reduced turnover costs in 2024 case studies.

- Inelastic talent: quits 2.4% (2024)

- Landlord pricing: prime rents elevated

- Mitigation: training + remote tools

- Retention: performance pay lowers turnover costs

Supplier squeeze 2024: higher funding costs, data lock-in, diversify, hedge, phase builds

Suppliers (banks, ABS investors, bureaus, platforms, talent, landlords) tightened terms in 2023–24 as Fed funds reached 5.25–5.50% in 2024, raising funding and servicing costs. Concentrated lenders and bureau lock‑in increase covenant, pricing and data risks. Mitigants: diversify lenders/vendors, dual providers, hedging and phased in‑house builds.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Banks/ABS | Fed funds 5.25–5.50% | ↑ funding cost |

| Credit bureaus | ~200M consumers | lock‑in/data risk |

| Payments | Fees 1–3% | operating drag |

What is included in the product

Concise Porter's Five Forces analysis for Regional Management that uncovers competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and identifies strategic vulnerabilities and protective dynamics shaping profitability.

A compact regional Porter's Five Forces summary that highlights local competitive pressures and relief strategies—ready to drop into decks, customize for new regulations or entrants, and quickly guide strategic decisions.

Customers Bargaining Power

Fragmented, price-sensitive borrowers

Customers are numerous but highly sensitive to APR, fees, and payment size; in 2024 roughly 70% of retail borrowers compare rates online, and a 0.5–1.0 percentage-point APR difference or a few dollars in monthly payment often shifts lender choice. They shop across online platforms and nearby branches, with approval likelihood as decisive as price. Transparent pricing and tailored terms (flexible payments, fee waivers) improve retention.

Low switching costs

Refinancing or taking a new loan elsewhere is easy with minimal prepayment penalties, and in 2024 about 63% of borrowers used online comparison tools before switching lenders. Digital competitors and aggregators accelerate comparisons and switching, shortening decision cycles. Loyalty is often transactional, driven by speed and approval odds rather than brand. High-touch relationship servicing and tailored cross-sell can raise perceived switching costs for select customer segments.

Limited prime credit access

Many Regional Management customers lack prime credit—FDIC reported 5.4% unbanked and 16.3% underbanked households (2022), which moderates bargaining power versus prime borrowers. Growth of subprime/near-prime alternative lenders expands options and price pressure. Promotional retail financing can temporarily undercut costs and boost conversion. Education and responsible lending improve trust and lower churn.

Regulatory and advocacy pressure

Service and speed expectations

Fast approvals and omnichannel convenience are baseline expectations in 2024, with industry benchmarks moving toward same-day approval and sub-24-hour onboarding; delays push customers to rivals rapidly, increasing churn risk. Streamlined onboarding and underwriting measurably boost perceived value, while integrated branch support plus digital tools can differentiate the customer experience.

- Same-day approvals; sub-24h onboarding

- Delays = rapid churn to competitors

- Streamlined underwriting increases value

- Branch + digital = differentiated experience

Borrowers compare rates: 70% online; 63% used tools

Customers are price- and approval-sensitive: in 2024 ~70% compare rates online and a 0.5–1.0pp APR gap often decides choice. Switching is easy: ~63% used online tools before switching lenders in 2024, shortening decision cycles. Regulatory pressure and complaints (+12% YoY) boost borrower leverage, while fast approvals and tailored terms raise retention.

| Metric | 2024 Value |

|---|---|

| Rate comparison online | 70% |

| Used tools before switching | 63% |

| Complaint growth YoY | +12% |

What You See Is What You Get

Regional Management Porter's Five Forces Analysis

This preview shows the exact Regional Management Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. It is the full, professionally formatted document, ready for download and use the moment you buy. You're viewing the final deliverable and will gain instant access to this same file upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Regional Management faces moderate buyer power, localized supplier relationships, and steady barriers to entry that shape its competitive landscape; competitive rivalry is intensified by similar regional players. This snapshot highlights key pressure points and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategic decisions. Purchase the complete report to access consultant-grade insights tailored to Regional Management.

Suppliers Bargaining Power

Concentrated funding sources

Regional management relies mainly on bank facilities, securitizations and institutional lenders; 2024 saw a tighter CRE funding backdrop per the Federal Reserve. A concentrated creditor pool can dictate covenants, pricing and advance rates, increasing negotiation power. Tight credit cycles in 2023–24 pushed up cost of funds, so diversifying maturities and lender types reduces single-source risk.

Interest rate sensitivity

Rising benchmark rates — federal funds at 5.25–5.50% in 2024 — flow directly into warehouse line pricing and ABS coupons, raising funding costs for regional managers.

When risk appetite falls, suppliers can demand higher spreads and tighter structures, compressing net interest margins unless higher rates are passed to borrowers.

Hedging and locking in fixed-rate funding materially reduce this interest-rate exposure.

Data and credit bureau reliance

Three national credit bureaus and rising alternative data providers are core to underwriting, with the bureaus covering roughly 200 million credit-active US consumers as of 2024. Switching vendors is feasible but often requires months of integration and model recalibration, plus nontrivial IT spend. Vendors can raise access fees or restrict data, degrading score quality; multi-sourcing and proprietary scorecards materially reduce single-vendor dependence.

Technology and servicing vendors

Loan origination, servicing platforms, and payment processors are highly specialized, with payment fees typically 1–3% per transaction and platform SLAs commonly targeting 99.9% uptime, creating vendor leverage and outage risk via lock-in and high switching costs. Negotiating strict SLAs, dual-provider redundancy, and exit clauses reduces supplier operational leverage. Building in-house origination and servicing capabilities improves bargaining power over time.

- Specialization: high technical dependence

- Costs: payment fees ~1–3%

- Risk: vendor lock-in raises switching/outage exposure

- Mitigation: SLAs, redundancy, exit terms

- Strategy: phased in-house build strengthens position

Talent and branch real estate

Experienced credit, collections, and compliance staff remain inelastic in tight labor markets, with the US quits rate at 2.4% in 2024 increasing hiring pressure; landlords in prime locations retain pricing power, keeping core CBD rents elevated. Training pipelines and remote tools cut concentration risk, while performance-based retention reduced turnover costs in 2024 case studies.

- Inelastic talent: quits 2.4% (2024)

- Landlord pricing: prime rents elevated

- Mitigation: training + remote tools

- Retention: performance pay lowers turnover costs

Supplier squeeze 2024: higher funding costs, data lock-in, diversify, hedge, phase builds

Suppliers (banks, ABS investors, bureaus, platforms, talent, landlords) tightened terms in 2023–24 as Fed funds reached 5.25–5.50% in 2024, raising funding and servicing costs. Concentrated lenders and bureau lock‑in increase covenant, pricing and data risks. Mitigants: diversify lenders/vendors, dual providers, hedging and phased in‑house builds.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Banks/ABS | Fed funds 5.25–5.50% | ↑ funding cost |

| Credit bureaus | ~200M consumers | lock‑in/data risk |

| Payments | Fees 1–3% | operating drag |

What is included in the product

Concise Porter's Five Forces analysis for Regional Management that uncovers competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and identifies strategic vulnerabilities and protective dynamics shaping profitability.

A compact regional Porter's Five Forces summary that highlights local competitive pressures and relief strategies—ready to drop into decks, customize for new regulations or entrants, and quickly guide strategic decisions.

Customers Bargaining Power

Fragmented, price-sensitive borrowers

Customers are numerous but highly sensitive to APR, fees, and payment size; in 2024 roughly 70% of retail borrowers compare rates online, and a 0.5–1.0 percentage-point APR difference or a few dollars in monthly payment often shifts lender choice. They shop across online platforms and nearby branches, with approval likelihood as decisive as price. Transparent pricing and tailored terms (flexible payments, fee waivers) improve retention.

Low switching costs

Refinancing or taking a new loan elsewhere is easy with minimal prepayment penalties, and in 2024 about 63% of borrowers used online comparison tools before switching lenders. Digital competitors and aggregators accelerate comparisons and switching, shortening decision cycles. Loyalty is often transactional, driven by speed and approval odds rather than brand. High-touch relationship servicing and tailored cross-sell can raise perceived switching costs for select customer segments.

Limited prime credit access

Many Regional Management customers lack prime credit—FDIC reported 5.4% unbanked and 16.3% underbanked households (2022), which moderates bargaining power versus prime borrowers. Growth of subprime/near-prime alternative lenders expands options and price pressure. Promotional retail financing can temporarily undercut costs and boost conversion. Education and responsible lending improve trust and lower churn.

Regulatory and advocacy pressure

Service and speed expectations

Fast approvals and omnichannel convenience are baseline expectations in 2024, with industry benchmarks moving toward same-day approval and sub-24-hour onboarding; delays push customers to rivals rapidly, increasing churn risk. Streamlined onboarding and underwriting measurably boost perceived value, while integrated branch support plus digital tools can differentiate the customer experience.

- Same-day approvals; sub-24h onboarding

- Delays = rapid churn to competitors

- Streamlined underwriting increases value

- Branch + digital = differentiated experience

Borrowers compare rates: 70% online; 63% used tools

Customers are price- and approval-sensitive: in 2024 ~70% compare rates online and a 0.5–1.0pp APR gap often decides choice. Switching is easy: ~63% used online tools before switching lenders in 2024, shortening decision cycles. Regulatory pressure and complaints (+12% YoY) boost borrower leverage, while fast approvals and tailored terms raise retention.

| Metric | 2024 Value |

|---|---|

| Rate comparison online | 70% |

| Used tools before switching | 63% |

| Complaint growth YoY | +12% |

What You See Is What You Get

Regional Management Porter's Five Forces Analysis

This preview shows the exact Regional Management Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. It is the full, professionally formatted document, ready for download and use the moment you buy. You're viewing the final deliverable and will gain instant access to this same file upon payment.