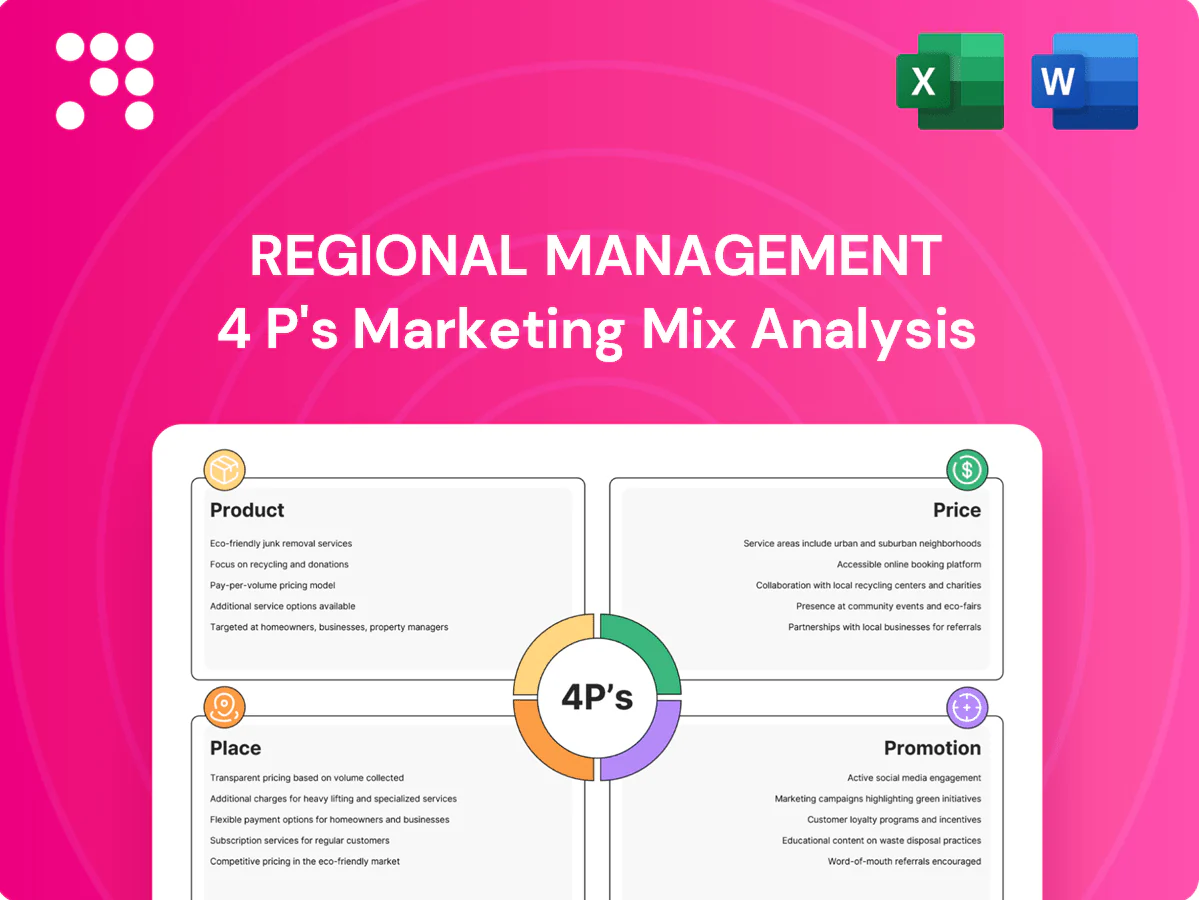

Regional Management Marketing Mix

Built for Strategy. Ready in Minutes.

Discover how Regional Management's Product, Price, Place and Promotion choices create competitive advantage; this concise 4P's analysis reveals market positioning, pricing architecture, channel strategy and promotional mix. The full, editable report delivers data-driven insights, examples and ready-to-use slides to save hours of research. Buy the complete Marketing Mix to apply these strategic learnings directly to your planning.

Product

Installment and secured personal loans

Offer small to mid-sized fixed-payment installment loans and secured personal loans backed by collateral, typically $1,000–25,000 with 12–60 month amortization and funding in 24–72 hours. Emphasize predictable terms, clear amortization schedules and industry median APRs for near-prime borrowers around 18–28% (2024). Tailor amounts and durations to measured income stability and repayment capacity. Include hardship options such as deferment or modified plans to maintain continuity of payment.

Retail sales financing solutions

Retail sales financing solutions provide point-of-sale financing via partner merchants for big-ticket purchases, driving average order value uplifts around 30% and conversion increases commonly reported between 20–40%.

They enable near-instant credit decisions (typically under 60 seconds) and seamless checkout integration for both in-store terminals and online carts, supporting mobile and omnichannel flows.

Flexible structures like deferred interest, 0% promotional periods, and installment plans broaden affordability and reduce cart abandonment.

Co-branded financing offers deepen merchant relationships and can improve repeat-purchase rates and loyalty metrics through shared marketing and data integration.

Underwriting with alternative data

Blend traditional credit files with alternative data—income stability, payment history, utility records—to extend reach to financially underserved populations (World Bank: ~1.4 billion adults lacked full financial access in 2021). Use scorecards calibrated to subprime and near-prime segments and automate approvals for the majority of clear cases while preserving manual review for edge cases. Continuously retrain models with quarterly portfolio performance feedback to reduce losses and improve hit rates.

Ancillary services and protection

Bundle credit insurance, collateral protection, and payment protection where permitted; offer optional add-ons with transparent terms and clear opt-in; provide budgeting tools and payment reminders to reduce delinquency; align services to boost borrower resilience and lifetime value.

- Bundle products: credit insurance + collateral + payment protection

- Transparent opt-in terms to increase uptake and compliance

- Budgeting tools & reminders to cut missed payments

Customer experience and servicing

Deliver omnichannel account management with branch, phone, and digital self-service—supported by e-signature, rapid ID verification and same-day credit decisions where feasible; 2024 usage: about 74% of customers used mobile banking monthly. Provide bilingual support and disclosures tailored to financial literacy, and maintain proactive servicing (early outreach reduces default rates by up to 30% in pilot programs).

- Omnichannel: branch, phone, digital

- Fast onboarding: e-sign, rapid verification, same-day decisions

- Bilingual + literacy‑level disclosures

- Proactive servicing to reduce defaults

Near-prime installment loans $1k-25k, 12-60 mo, 24-72h funding, 18-28% APR, 60s decisions

Product set targets small–mid installment and secured loans ($1k–25k, 12–60 months) with 24–72h funding, predictable amortization and 2024 near‑prime APRs ~18–28%. POS and co‑branded financing lift AOV ~30% and conversion 20–40%, offering 60s instant decisions and omnichannel checkout. Include hardship options, optional protection bundles, and digital tools to cut delinquencies and boost LTV.

| Metric | Value |

|---|---|

| Loan size | $1k–25k |

| Term | 12–60 mo |

| Funding | 24–72 hrs |

| Near‑prime APR (2024) | 18–28% |

| Mobile use (2024) | 74% |

What is included in the product

Delivers a concise, company-specific deep dive into Regional Management’s Product, Price, Place, and Promotion strategies, using real brand practices and competitive context to inform actionable recommendations for managers, consultants, and marketers.

Summarizes regional 4Ps into a concise, structured view that relieves analysis bottlenecks and speeds decision-making for cross-market teams; ideal for leadership briefings, workshops, or rapid comparisons across territories.

Place

Branch-centric distribution

Leverage a dense branch network in core regional markets for face-to-face origination and servicing, prioritizing physical outreach for credit-constrained segments. Position branches within a 10-minute walk of retail hubs and transit nodes to maximize footfall. Staff branches with local hires to build trust and extend hours around peak pay cycles (1–3 and 15–17 of each month).

Online and mobile platforms

Provide end-to-end digital application, e-sign, and funding with integrated document upload, income verification, and instant status updates. Offer mobile wallet payment options and autopay setup, supporting 2.5 billion mobile wallet users worldwide in 2024. Ensure ADA-compliant, responsive design for ease of access and regulatory alignment.

Merchant and dealer partnerships

Embedding point-of-need financing with partner retailers captured rapid growth as global BNPL GMV reached about $166 billion in 2023, and branded offers can increase AOV by up to 30% at checkout.

Supply instant credit decisions via APIs or tablets—many providers deliver approvals in under 2 seconds—enabling on-the-spot conversions and reducing drop-off.

Train merchant staff on offer positioning and compliance to lower disputes and improve uptake, and use co-op marketing (digital+in-store) to drive store traffic, often lifting approvals and visits by double-digit percentages.

Targeted geographic expansion

- Target: favorable regs + underserved credit

- Data: FDIC 2021 unbanked 5.4%, BLS 2023 unemployment 3.7%

- Method: ZIP-level analytics, pilot kiosks

- Ops: align servicing capacity with growth

Omnichannel fulfillment and payments

Omnichannel fulfillment and payments let customers start an application in one channel and finish in another with no friction, leveraging in-branch cash, ACH, debit and card acceptance and digital channels; FedNow (launched July 2023) and Same-Day ACH (available since 2016) enable same-day disbursements via ACH push or debit rails and centralized loan-product inventory with localized offer tiers.

Hyperlocal branches, sub-2s instant API credit and FedNow same-day payouts for underserved consumers

Place blends dense branch presence in core micro-markets with omnichannel digital fulfillment to reach credit-constrained segments; branches sited within 10-minute walk of transit/retail and staffed locally for peak pay cycles. Embed point-of-need BNPL and instant API credit (sub-2s) while leveraging FedNow/Same-Day ACH for same-day disbursements.

| Metric | Value |

|---|---|

| BNPL GMV 2023 | $166B |

| Mobile wallet users 2024 | 2.5B |

| Unbanked (FDIC 2021) | 5.4% |

| U.S. unemployment (BLS 2023) | 3.7% |

What You Preview Is What You Download

Regional Management 4P's Marketing Mix Analysis

This Regional Management 4P's Marketing Mix Analysis delivers a concise, actionable review of Product, Price, Place and Promotion tailored to regional dynamics. The preview you see is the exact document you’ll receive after purchase—no samples or mockups. It’s fully complete, editable and ready for immediate use.

Built for Strategy. Ready in Minutes.

Discover how Regional Management's Product, Price, Place and Promotion choices create competitive advantage; this concise 4P's analysis reveals market positioning, pricing architecture, channel strategy and promotional mix. The full, editable report delivers data-driven insights, examples and ready-to-use slides to save hours of research. Buy the complete Marketing Mix to apply these strategic learnings directly to your planning.

Product

Installment and secured personal loans

Offer small to mid-sized fixed-payment installment loans and secured personal loans backed by collateral, typically $1,000–25,000 with 12–60 month amortization and funding in 24–72 hours. Emphasize predictable terms, clear amortization schedules and industry median APRs for near-prime borrowers around 18–28% (2024). Tailor amounts and durations to measured income stability and repayment capacity. Include hardship options such as deferment or modified plans to maintain continuity of payment.

Retail sales financing solutions

Retail sales financing solutions provide point-of-sale financing via partner merchants for big-ticket purchases, driving average order value uplifts around 30% and conversion increases commonly reported between 20–40%.

They enable near-instant credit decisions (typically under 60 seconds) and seamless checkout integration for both in-store terminals and online carts, supporting mobile and omnichannel flows.

Flexible structures like deferred interest, 0% promotional periods, and installment plans broaden affordability and reduce cart abandonment.

Co-branded financing offers deepen merchant relationships and can improve repeat-purchase rates and loyalty metrics through shared marketing and data integration.

Underwriting with alternative data

Blend traditional credit files with alternative data—income stability, payment history, utility records—to extend reach to financially underserved populations (World Bank: ~1.4 billion adults lacked full financial access in 2021). Use scorecards calibrated to subprime and near-prime segments and automate approvals for the majority of clear cases while preserving manual review for edge cases. Continuously retrain models with quarterly portfolio performance feedback to reduce losses and improve hit rates.

Ancillary services and protection

Bundle credit insurance, collateral protection, and payment protection where permitted; offer optional add-ons with transparent terms and clear opt-in; provide budgeting tools and payment reminders to reduce delinquency; align services to boost borrower resilience and lifetime value.

- Bundle products: credit insurance + collateral + payment protection

- Transparent opt-in terms to increase uptake and compliance

- Budgeting tools & reminders to cut missed payments

Customer experience and servicing

Deliver omnichannel account management with branch, phone, and digital self-service—supported by e-signature, rapid ID verification and same-day credit decisions where feasible; 2024 usage: about 74% of customers used mobile banking monthly. Provide bilingual support and disclosures tailored to financial literacy, and maintain proactive servicing (early outreach reduces default rates by up to 30% in pilot programs).

- Omnichannel: branch, phone, digital

- Fast onboarding: e-sign, rapid verification, same-day decisions

- Bilingual + literacy‑level disclosures

- Proactive servicing to reduce defaults

Near-prime installment loans $1k-25k, 12-60 mo, 24-72h funding, 18-28% APR, 60s decisions

Product set targets small–mid installment and secured loans ($1k–25k, 12–60 months) with 24–72h funding, predictable amortization and 2024 near‑prime APRs ~18–28%. POS and co‑branded financing lift AOV ~30% and conversion 20–40%, offering 60s instant decisions and omnichannel checkout. Include hardship options, optional protection bundles, and digital tools to cut delinquencies and boost LTV.

| Metric | Value |

|---|---|

| Loan size | $1k–25k |

| Term | 12–60 mo |

| Funding | 24–72 hrs |

| Near‑prime APR (2024) | 18–28% |

| Mobile use (2024) | 74% |

What is included in the product

Delivers a concise, company-specific deep dive into Regional Management’s Product, Price, Place, and Promotion strategies, using real brand practices and competitive context to inform actionable recommendations for managers, consultants, and marketers.

Summarizes regional 4Ps into a concise, structured view that relieves analysis bottlenecks and speeds decision-making for cross-market teams; ideal for leadership briefings, workshops, or rapid comparisons across territories.

Place

Branch-centric distribution

Leverage a dense branch network in core regional markets for face-to-face origination and servicing, prioritizing physical outreach for credit-constrained segments. Position branches within a 10-minute walk of retail hubs and transit nodes to maximize footfall. Staff branches with local hires to build trust and extend hours around peak pay cycles (1–3 and 15–17 of each month).

Online and mobile platforms

Provide end-to-end digital application, e-sign, and funding with integrated document upload, income verification, and instant status updates. Offer mobile wallet payment options and autopay setup, supporting 2.5 billion mobile wallet users worldwide in 2024. Ensure ADA-compliant, responsive design for ease of access and regulatory alignment.

Merchant and dealer partnerships

Embedding point-of-need financing with partner retailers captured rapid growth as global BNPL GMV reached about $166 billion in 2023, and branded offers can increase AOV by up to 30% at checkout.

Supply instant credit decisions via APIs or tablets—many providers deliver approvals in under 2 seconds—enabling on-the-spot conversions and reducing drop-off.

Train merchant staff on offer positioning and compliance to lower disputes and improve uptake, and use co-op marketing (digital+in-store) to drive store traffic, often lifting approvals and visits by double-digit percentages.

Targeted geographic expansion

- Target: favorable regs + underserved credit

- Data: FDIC 2021 unbanked 5.4%, BLS 2023 unemployment 3.7%

- Method: ZIP-level analytics, pilot kiosks

- Ops: align servicing capacity with growth

Omnichannel fulfillment and payments

Omnichannel fulfillment and payments let customers start an application in one channel and finish in another with no friction, leveraging in-branch cash, ACH, debit and card acceptance and digital channels; FedNow (launched July 2023) and Same-Day ACH (available since 2016) enable same-day disbursements via ACH push or debit rails and centralized loan-product inventory with localized offer tiers.

Hyperlocal branches, sub-2s instant API credit and FedNow same-day payouts for underserved consumers

Place blends dense branch presence in core micro-markets with omnichannel digital fulfillment to reach credit-constrained segments; branches sited within 10-minute walk of transit/retail and staffed locally for peak pay cycles. Embed point-of-need BNPL and instant API credit (sub-2s) while leveraging FedNow/Same-Day ACH for same-day disbursements.

| Metric | Value |

|---|---|

| BNPL GMV 2023 | $166B |

| Mobile wallet users 2024 | 2.5B |

| Unbanked (FDIC 2021) | 5.4% |

| U.S. unemployment (BLS 2023) | 3.7% |

What You Preview Is What You Download

Regional Management 4P's Marketing Mix Analysis

This Regional Management 4P's Marketing Mix Analysis delivers a concise, actionable review of Product, Price, Place and Promotion tailored to regional dynamics. The preview you see is the exact document you’ll receive after purchase—no samples or mockups. It’s fully complete, editable and ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Built for Strategy. Ready in Minutes.

Discover how Regional Management's Product, Price, Place and Promotion choices create competitive advantage; this concise 4P's analysis reveals market positioning, pricing architecture, channel strategy and promotional mix. The full, editable report delivers data-driven insights, examples and ready-to-use slides to save hours of research. Buy the complete Marketing Mix to apply these strategic learnings directly to your planning.

Product

Installment and secured personal loans

Offer small to mid-sized fixed-payment installment loans and secured personal loans backed by collateral, typically $1,000–25,000 with 12–60 month amortization and funding in 24–72 hours. Emphasize predictable terms, clear amortization schedules and industry median APRs for near-prime borrowers around 18–28% (2024). Tailor amounts and durations to measured income stability and repayment capacity. Include hardship options such as deferment or modified plans to maintain continuity of payment.

Retail sales financing solutions

Retail sales financing solutions provide point-of-sale financing via partner merchants for big-ticket purchases, driving average order value uplifts around 30% and conversion increases commonly reported between 20–40%.

They enable near-instant credit decisions (typically under 60 seconds) and seamless checkout integration for both in-store terminals and online carts, supporting mobile and omnichannel flows.

Flexible structures like deferred interest, 0% promotional periods, and installment plans broaden affordability and reduce cart abandonment.

Co-branded financing offers deepen merchant relationships and can improve repeat-purchase rates and loyalty metrics through shared marketing and data integration.

Underwriting with alternative data

Blend traditional credit files with alternative data—income stability, payment history, utility records—to extend reach to financially underserved populations (World Bank: ~1.4 billion adults lacked full financial access in 2021). Use scorecards calibrated to subprime and near-prime segments and automate approvals for the majority of clear cases while preserving manual review for edge cases. Continuously retrain models with quarterly portfolio performance feedback to reduce losses and improve hit rates.

Ancillary services and protection

Bundle credit insurance, collateral protection, and payment protection where permitted; offer optional add-ons with transparent terms and clear opt-in; provide budgeting tools and payment reminders to reduce delinquency; align services to boost borrower resilience and lifetime value.

- Bundle products: credit insurance + collateral + payment protection

- Transparent opt-in terms to increase uptake and compliance

- Budgeting tools & reminders to cut missed payments

Customer experience and servicing

Deliver omnichannel account management with branch, phone, and digital self-service—supported by e-signature, rapid ID verification and same-day credit decisions where feasible; 2024 usage: about 74% of customers used mobile banking monthly. Provide bilingual support and disclosures tailored to financial literacy, and maintain proactive servicing (early outreach reduces default rates by up to 30% in pilot programs).

- Omnichannel: branch, phone, digital

- Fast onboarding: e-sign, rapid verification, same-day decisions

- Bilingual + literacy‑level disclosures

- Proactive servicing to reduce defaults

Near-prime installment loans $1k-25k, 12-60 mo, 24-72h funding, 18-28% APR, 60s decisions

Product set targets small–mid installment and secured loans ($1k–25k, 12–60 months) with 24–72h funding, predictable amortization and 2024 near‑prime APRs ~18–28%. POS and co‑branded financing lift AOV ~30% and conversion 20–40%, offering 60s instant decisions and omnichannel checkout. Include hardship options, optional protection bundles, and digital tools to cut delinquencies and boost LTV.

| Metric | Value |

|---|---|

| Loan size | $1k–25k |

| Term | 12–60 mo |

| Funding | 24–72 hrs |

| Near‑prime APR (2024) | 18–28% |

| Mobile use (2024) | 74% |

What is included in the product

Delivers a concise, company-specific deep dive into Regional Management’s Product, Price, Place, and Promotion strategies, using real brand practices and competitive context to inform actionable recommendations for managers, consultants, and marketers.

Summarizes regional 4Ps into a concise, structured view that relieves analysis bottlenecks and speeds decision-making for cross-market teams; ideal for leadership briefings, workshops, or rapid comparisons across territories.

Place

Branch-centric distribution

Leverage a dense branch network in core regional markets for face-to-face origination and servicing, prioritizing physical outreach for credit-constrained segments. Position branches within a 10-minute walk of retail hubs and transit nodes to maximize footfall. Staff branches with local hires to build trust and extend hours around peak pay cycles (1–3 and 15–17 of each month).

Online and mobile platforms

Provide end-to-end digital application, e-sign, and funding with integrated document upload, income verification, and instant status updates. Offer mobile wallet payment options and autopay setup, supporting 2.5 billion mobile wallet users worldwide in 2024. Ensure ADA-compliant, responsive design for ease of access and regulatory alignment.

Merchant and dealer partnerships

Embedding point-of-need financing with partner retailers captured rapid growth as global BNPL GMV reached about $166 billion in 2023, and branded offers can increase AOV by up to 30% at checkout.

Supply instant credit decisions via APIs or tablets—many providers deliver approvals in under 2 seconds—enabling on-the-spot conversions and reducing drop-off.

Train merchant staff on offer positioning and compliance to lower disputes and improve uptake, and use co-op marketing (digital+in-store) to drive store traffic, often lifting approvals and visits by double-digit percentages.

Targeted geographic expansion

- Target: favorable regs + underserved credit

- Data: FDIC 2021 unbanked 5.4%, BLS 2023 unemployment 3.7%

- Method: ZIP-level analytics, pilot kiosks

- Ops: align servicing capacity with growth

Omnichannel fulfillment and payments

Omnichannel fulfillment and payments let customers start an application in one channel and finish in another with no friction, leveraging in-branch cash, ACH, debit and card acceptance and digital channels; FedNow (launched July 2023) and Same-Day ACH (available since 2016) enable same-day disbursements via ACH push or debit rails and centralized loan-product inventory with localized offer tiers.

Hyperlocal branches, sub-2s instant API credit and FedNow same-day payouts for underserved consumers

Place blends dense branch presence in core micro-markets with omnichannel digital fulfillment to reach credit-constrained segments; branches sited within 10-minute walk of transit/retail and staffed locally for peak pay cycles. Embed point-of-need BNPL and instant API credit (sub-2s) while leveraging FedNow/Same-Day ACH for same-day disbursements.

| Metric | Value |

|---|---|

| BNPL GMV 2023 | $166B |

| Mobile wallet users 2024 | 2.5B |

| Unbanked (FDIC 2021) | 5.4% |

| U.S. unemployment (BLS 2023) | 3.7% |

What You Preview Is What You Download

Regional Management 4P's Marketing Mix Analysis

This Regional Management 4P's Marketing Mix Analysis delivers a concise, actionable review of Product, Price, Place and Promotion tailored to regional dynamics. The preview you see is the exact document you’ll receive after purchase—no samples or mockups. It’s fully complete, editable and ready for immediate use.