Reka Industrial Porter's Five Forces Analysis

From Overview to Strategy Blueprint

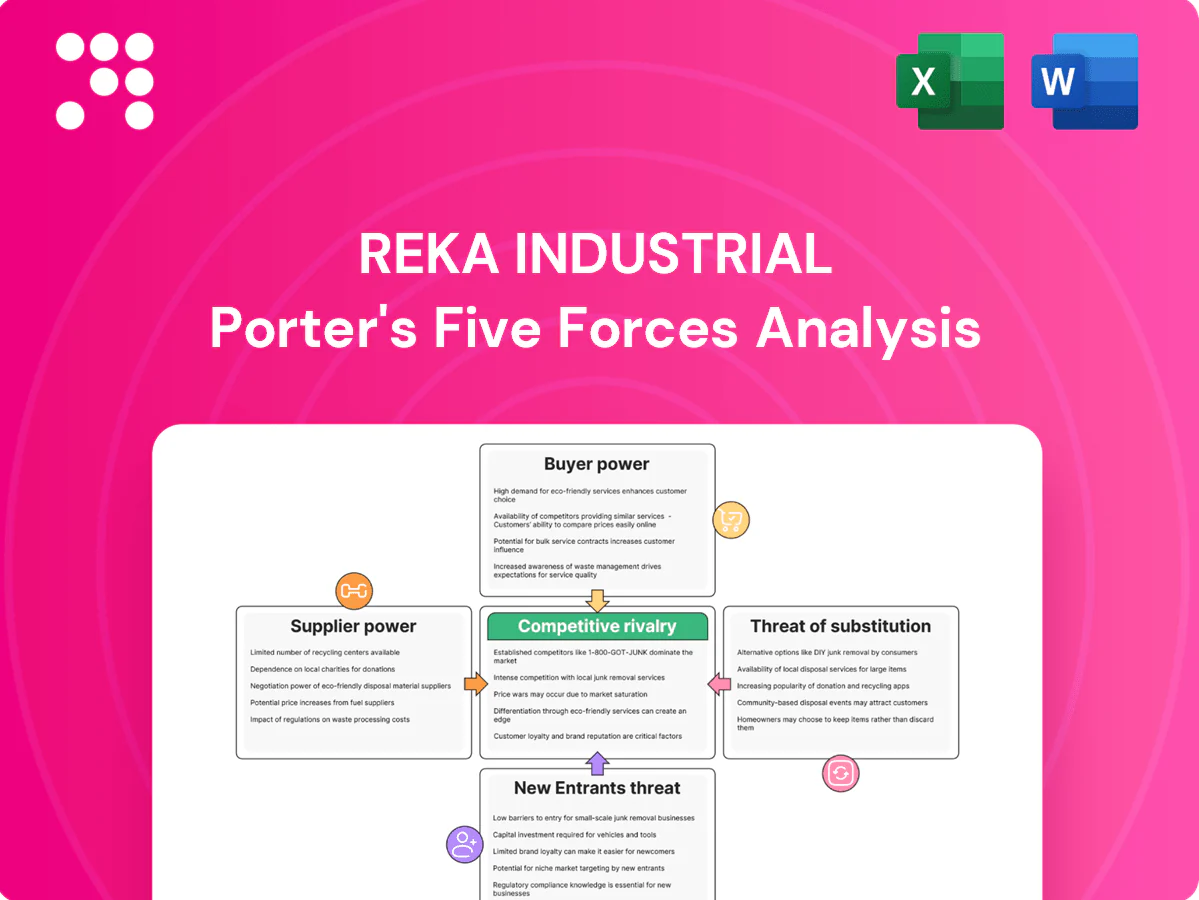

Reka Industrial faces moderate buyer power and capital-intensive barriers that limit new entrants, while supplier concentration and evolving substitutes shape margin pressure. Competitive rivalry is high in core segments, driven by scale and efficiency. This snapshot highlights key tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to explore Reka Industrial’s competitive dynamics and market pressures in detail.

Suppliers Bargaining Power

Concentrated raw materials

Core inputs like copper and aluminum come from concentrated suppliers—Chile produced about 28% of mined copper and China accounted for roughly 55% of primary aluminum output in 2024—while polymers, carbon black and specialty chemicals are dominated by a handful of global firms. Commodity price swings can compress margins quickly where pass-through clauses are weak. Reka’s long-term ownership enables hedging and multi-year supply contracts to mitigate volatility. Smelter outages or supply shocks nonetheless boost supplier leverage.

Specification-driven inputs

Cable and rubber compounds for Reka often require certified grades and customized formulations, typically tied to UL 1581 and IEC 60216 compliance. Qualification limits easy switching, increasing supplier power for niche additives and compounds. Dual-sourcing is feasible but time-consuming due to third-party testing, batch traceability and regulatory audits. Supplier compounding know-how can become a production bottleneck and strategic dependency.

Energy and logistics exposure

Production is energy intensive and Reka is sensitive to Nordic electricity and freight; Nord Pool day‑ahead averaged about 60 EUR/MWh in 2024, while spot freight volatility pushed short‑term shipping costs up ~15% year‑on‑year. Power providers and carriers can gain leverage during tight markets or fuel spikes, especially if grid constraints emerge. Long‑term PPAs and optimized freight contracts notably reduce supplier pressure and cash‑flow volatility.

Tooling and machinery dependencies

- Lead times: 9–18 months

- High switching costs: proprietary parts

- Service contracts: lock-in risk

- Mitigation: preventive CAPEX, spare inventories

ESG and compliance requirements

Traceability, REACH (EU chemical rules) and conflict-minerals laws (EU regulation effective 2021; Dodd-Frank Section 1502) have narrowed the qualified supplier pool, allowing compliant vendors to command premiums (industry surveys cite roughly 5–15%) and stricter contract terms; non-compliance raises remediation costs and increases supplier leverage. Reka can use active ownership to standardize ESG audits, broaden vetted vendors and reduce supplier bargaining power.

- Traceability: tighter scope limits suppliers

- Regulations: REACH updates + EU conflict-minerals enforcement

- Premiums: compliant suppliers capture ~5–15%

- Mitigation: standard ESG audits widen vendor base

Supply concentration and energy costs squeeze margins: Chile 28% Cu, China 55% Al

Concentrated metal suppliers and specialty-chemical vendors (Chile 28% copper, China 55% primary aluminum in 2024) and certified-compound providers raise supplier power; commodity swings and smelter outages tighten leverage. Energy and freight pressure (Nord Pool ~60 EUR/MWh 2024; freight +15% YoY) amplify risk despite Reka’s hedges and PPAs. Long OEM lead times (9–18 months) and compliance premiums (5–15%) sustain switching costs.

| Metric | 2024/value |

|---|---|

| Copper supply share (Chile) | 28% |

| Aluminum supply (China) | 55% |

| Nord Pool avg price | 60 EUR/MWh |

| Freight YoY | +15% |

| OEM lead times | 9–18 months |

| Compliance premium | 5–15% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Reka Industrial, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptive forces that influence pricing, margins and strategic positioning.

One-sheet Porter’s Five Forces for Reka Industrial—instantly visualize competitive pressure with an editable spider chart, customize inputs for changing market conditions, and drop the clean summary straight into pitch decks or reports.

Customers Bargaining Power

Large buyers with volume leverage

Utilities, EPCs, industrial OEMs and automotive customers buy at scale via framework tenders and volume commitments that commonly drive price concessions of roughly 5–15% in 2024; large buyers often secure regional leverage and can pit suppliers against each other across markets. Visible volumes let Reka trade margin for utilization, shifting output to protect cash flow when needed.

High qualification and approval cycles

Product approvals, type tests and certifications create significant switching costs—procurement cycles and re-tenders typically occur every 3–5 years—so once specified incumbents gain stickiness despite price pressure. Re-tenders reset pricing power periodically, giving buyers leverage at bid time. Strong QA and >95% on-time delivery rates preserve incumbency between tenders.

Price sensitivity in commoditized SKUs

Standard power cables and general rubber goods trade on tight cost-plus terms with customers demanding commodity indexation to benchmark metal and polymer prices (eg LME-based clauses) and transparent surcharges. Differentiation must therefore come from superior service, optimized logistics and proven reliability to capture share beyond spot price competition. Targeted value-added engineering programs can shift purchasing from price to total-cost-of-ownership.

Service, lead-time, and reliability demands

Buyers penalize delays due to project-critical timelines; 2024 OTIF benchmarks sit around 95%, and strong inventory programs plus technical support materially reduce customer bargaining power. Collaborative planning and VMI—often cutting inventory 20–30%—deepen lock-in and raise switching costs. Poor service rapidly shifts leverage back to buyers via churn and penalties.

- OTIF ≥95%

- VMI: −20–30% inventory

- Collaborative planning: +10–15% forecast accuracy

- Service failures → rapid churn

ESG and lifecycle requirements

- Demand: buyers require low-carbon/recyclable inputs

- Regulation: CSRD ~49,000 firms covered in 2024

- Advantage: EPDs/circularity enable premiums

- Risk: noncompliance → substitution and tougher terms

Buyers force 5-15% concessions; VMI, OTIF and EPDs reshape 2024 tenders

Customers exert moderate-strong power: framework tenders drive 5–15% price concessions in 2024, large buyers leverage regional scope and re-tenders every 3–5 years. High switching costs from approvals and >95% OTIF preserve incumbency, while VMI (-20–30% inventory) and low-carbon demands (CSRD ~49,000 firms in 2024) shift negotiation toward suppliers offering EPDs.

| Metric | 2024 Value | Impact |

|---|---|---|

| Price concessions | 5–15% | Margin pressure |

| Re-tender cycle | 3–5 yrs | Periodic leverage |

| OTIF | >=95% | Incumbency |

| VMI | -20–30% inventory | Lock-in |

| CSRD coverage | ~49,000 firms | Higher sustainability demands |

Preview Before You Purchase

Reka Industrial Porter's Five Forces Analysis

This preview shows the exact Reka Industrial Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders or samples. The document displayed is the professionally formatted, ready-to-use file included with your order. Once you buy, you’ll get instant access to this identical analysis.

From Overview to Strategy Blueprint

Reka Industrial faces moderate buyer power and capital-intensive barriers that limit new entrants, while supplier concentration and evolving substitutes shape margin pressure. Competitive rivalry is high in core segments, driven by scale and efficiency. This snapshot highlights key tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to explore Reka Industrial’s competitive dynamics and market pressures in detail.

Suppliers Bargaining Power

Concentrated raw materials

Core inputs like copper and aluminum come from concentrated suppliers—Chile produced about 28% of mined copper and China accounted for roughly 55% of primary aluminum output in 2024—while polymers, carbon black and specialty chemicals are dominated by a handful of global firms. Commodity price swings can compress margins quickly where pass-through clauses are weak. Reka’s long-term ownership enables hedging and multi-year supply contracts to mitigate volatility. Smelter outages or supply shocks nonetheless boost supplier leverage.

Specification-driven inputs

Cable and rubber compounds for Reka often require certified grades and customized formulations, typically tied to UL 1581 and IEC 60216 compliance. Qualification limits easy switching, increasing supplier power for niche additives and compounds. Dual-sourcing is feasible but time-consuming due to third-party testing, batch traceability and regulatory audits. Supplier compounding know-how can become a production bottleneck and strategic dependency.

Energy and logistics exposure

Production is energy intensive and Reka is sensitive to Nordic electricity and freight; Nord Pool day‑ahead averaged about 60 EUR/MWh in 2024, while spot freight volatility pushed short‑term shipping costs up ~15% year‑on‑year. Power providers and carriers can gain leverage during tight markets or fuel spikes, especially if grid constraints emerge. Long‑term PPAs and optimized freight contracts notably reduce supplier pressure and cash‑flow volatility.

Tooling and machinery dependencies

- Lead times: 9–18 months

- High switching costs: proprietary parts

- Service contracts: lock-in risk

- Mitigation: preventive CAPEX, spare inventories

ESG and compliance requirements

Traceability, REACH (EU chemical rules) and conflict-minerals laws (EU regulation effective 2021; Dodd-Frank Section 1502) have narrowed the qualified supplier pool, allowing compliant vendors to command premiums (industry surveys cite roughly 5–15%) and stricter contract terms; non-compliance raises remediation costs and increases supplier leverage. Reka can use active ownership to standardize ESG audits, broaden vetted vendors and reduce supplier bargaining power.

- Traceability: tighter scope limits suppliers

- Regulations: REACH updates + EU conflict-minerals enforcement

- Premiums: compliant suppliers capture ~5–15%

- Mitigation: standard ESG audits widen vendor base

Supply concentration and energy costs squeeze margins: Chile 28% Cu, China 55% Al

Concentrated metal suppliers and specialty-chemical vendors (Chile 28% copper, China 55% primary aluminum in 2024) and certified-compound providers raise supplier power; commodity swings and smelter outages tighten leverage. Energy and freight pressure (Nord Pool ~60 EUR/MWh 2024; freight +15% YoY) amplify risk despite Reka’s hedges and PPAs. Long OEM lead times (9–18 months) and compliance premiums (5–15%) sustain switching costs.

| Metric | 2024/value |

|---|---|

| Copper supply share (Chile) | 28% |

| Aluminum supply (China) | 55% |

| Nord Pool avg price | 60 EUR/MWh |

| Freight YoY | +15% |

| OEM lead times | 9–18 months |

| Compliance premium | 5–15% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Reka Industrial, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptive forces that influence pricing, margins and strategic positioning.

One-sheet Porter’s Five Forces for Reka Industrial—instantly visualize competitive pressure with an editable spider chart, customize inputs for changing market conditions, and drop the clean summary straight into pitch decks or reports.

Customers Bargaining Power

Large buyers with volume leverage

Utilities, EPCs, industrial OEMs and automotive customers buy at scale via framework tenders and volume commitments that commonly drive price concessions of roughly 5–15% in 2024; large buyers often secure regional leverage and can pit suppliers against each other across markets. Visible volumes let Reka trade margin for utilization, shifting output to protect cash flow when needed.

High qualification and approval cycles

Product approvals, type tests and certifications create significant switching costs—procurement cycles and re-tenders typically occur every 3–5 years—so once specified incumbents gain stickiness despite price pressure. Re-tenders reset pricing power periodically, giving buyers leverage at bid time. Strong QA and >95% on-time delivery rates preserve incumbency between tenders.

Price sensitivity in commoditized SKUs

Standard power cables and general rubber goods trade on tight cost-plus terms with customers demanding commodity indexation to benchmark metal and polymer prices (eg LME-based clauses) and transparent surcharges. Differentiation must therefore come from superior service, optimized logistics and proven reliability to capture share beyond spot price competition. Targeted value-added engineering programs can shift purchasing from price to total-cost-of-ownership.

Service, lead-time, and reliability demands

Buyers penalize delays due to project-critical timelines; 2024 OTIF benchmarks sit around 95%, and strong inventory programs plus technical support materially reduce customer bargaining power. Collaborative planning and VMI—often cutting inventory 20–30%—deepen lock-in and raise switching costs. Poor service rapidly shifts leverage back to buyers via churn and penalties.

- OTIF ≥95%

- VMI: −20–30% inventory

- Collaborative planning: +10–15% forecast accuracy

- Service failures → rapid churn

ESG and lifecycle requirements

- Demand: buyers require low-carbon/recyclable inputs

- Regulation: CSRD ~49,000 firms covered in 2024

- Advantage: EPDs/circularity enable premiums

- Risk: noncompliance → substitution and tougher terms

Buyers force 5-15% concessions; VMI, OTIF and EPDs reshape 2024 tenders

Customers exert moderate-strong power: framework tenders drive 5–15% price concessions in 2024, large buyers leverage regional scope and re-tenders every 3–5 years. High switching costs from approvals and >95% OTIF preserve incumbency, while VMI (-20–30% inventory) and low-carbon demands (CSRD ~49,000 firms in 2024) shift negotiation toward suppliers offering EPDs.

| Metric | 2024 Value | Impact |

|---|---|---|

| Price concessions | 5–15% | Margin pressure |

| Re-tender cycle | 3–5 yrs | Periodic leverage |

| OTIF | >=95% | Incumbency |

| VMI | -20–30% inventory | Lock-in |

| CSRD coverage | ~49,000 firms | Higher sustainability demands |

Preview Before You Purchase

Reka Industrial Porter's Five Forces Analysis

This preview shows the exact Reka Industrial Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders or samples. The document displayed is the professionally formatted, ready-to-use file included with your order. Once you buy, you’ll get instant access to this identical analysis.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Reka Industrial faces moderate buyer power and capital-intensive barriers that limit new entrants, while supplier concentration and evolving substitutes shape margin pressure. Competitive rivalry is high in core segments, driven by scale and efficiency. This snapshot highlights key tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to explore Reka Industrial’s competitive dynamics and market pressures in detail.

Suppliers Bargaining Power

Concentrated raw materials

Core inputs like copper and aluminum come from concentrated suppliers—Chile produced about 28% of mined copper and China accounted for roughly 55% of primary aluminum output in 2024—while polymers, carbon black and specialty chemicals are dominated by a handful of global firms. Commodity price swings can compress margins quickly where pass-through clauses are weak. Reka’s long-term ownership enables hedging and multi-year supply contracts to mitigate volatility. Smelter outages or supply shocks nonetheless boost supplier leverage.

Specification-driven inputs

Cable and rubber compounds for Reka often require certified grades and customized formulations, typically tied to UL 1581 and IEC 60216 compliance. Qualification limits easy switching, increasing supplier power for niche additives and compounds. Dual-sourcing is feasible but time-consuming due to third-party testing, batch traceability and regulatory audits. Supplier compounding know-how can become a production bottleneck and strategic dependency.

Energy and logistics exposure

Production is energy intensive and Reka is sensitive to Nordic electricity and freight; Nord Pool day‑ahead averaged about 60 EUR/MWh in 2024, while spot freight volatility pushed short‑term shipping costs up ~15% year‑on‑year. Power providers and carriers can gain leverage during tight markets or fuel spikes, especially if grid constraints emerge. Long‑term PPAs and optimized freight contracts notably reduce supplier pressure and cash‑flow volatility.

Tooling and machinery dependencies

- Lead times: 9–18 months

- High switching costs: proprietary parts

- Service contracts: lock-in risk

- Mitigation: preventive CAPEX, spare inventories

ESG and compliance requirements

Traceability, REACH (EU chemical rules) and conflict-minerals laws (EU regulation effective 2021; Dodd-Frank Section 1502) have narrowed the qualified supplier pool, allowing compliant vendors to command premiums (industry surveys cite roughly 5–15%) and stricter contract terms; non-compliance raises remediation costs and increases supplier leverage. Reka can use active ownership to standardize ESG audits, broaden vetted vendors and reduce supplier bargaining power.

- Traceability: tighter scope limits suppliers

- Regulations: REACH updates + EU conflict-minerals enforcement

- Premiums: compliant suppliers capture ~5–15%

- Mitigation: standard ESG audits widen vendor base

Supply concentration and energy costs squeeze margins: Chile 28% Cu, China 55% Al

Concentrated metal suppliers and specialty-chemical vendors (Chile 28% copper, China 55% primary aluminum in 2024) and certified-compound providers raise supplier power; commodity swings and smelter outages tighten leverage. Energy and freight pressure (Nord Pool ~60 EUR/MWh 2024; freight +15% YoY) amplify risk despite Reka’s hedges and PPAs. Long OEM lead times (9–18 months) and compliance premiums (5–15%) sustain switching costs.

| Metric | 2024/value |

|---|---|

| Copper supply share (Chile) | 28% |

| Aluminum supply (China) | 55% |

| Nord Pool avg price | 60 EUR/MWh |

| Freight YoY | +15% |

| OEM lead times | 9–18 months |

| Compliance premium | 5–15% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Reka Industrial, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptive forces that influence pricing, margins and strategic positioning.

One-sheet Porter’s Five Forces for Reka Industrial—instantly visualize competitive pressure with an editable spider chart, customize inputs for changing market conditions, and drop the clean summary straight into pitch decks or reports.

Customers Bargaining Power

Large buyers with volume leverage

Utilities, EPCs, industrial OEMs and automotive customers buy at scale via framework tenders and volume commitments that commonly drive price concessions of roughly 5–15% in 2024; large buyers often secure regional leverage and can pit suppliers against each other across markets. Visible volumes let Reka trade margin for utilization, shifting output to protect cash flow when needed.

High qualification and approval cycles

Product approvals, type tests and certifications create significant switching costs—procurement cycles and re-tenders typically occur every 3–5 years—so once specified incumbents gain stickiness despite price pressure. Re-tenders reset pricing power periodically, giving buyers leverage at bid time. Strong QA and >95% on-time delivery rates preserve incumbency between tenders.

Price sensitivity in commoditized SKUs

Standard power cables and general rubber goods trade on tight cost-plus terms with customers demanding commodity indexation to benchmark metal and polymer prices (eg LME-based clauses) and transparent surcharges. Differentiation must therefore come from superior service, optimized logistics and proven reliability to capture share beyond spot price competition. Targeted value-added engineering programs can shift purchasing from price to total-cost-of-ownership.

Service, lead-time, and reliability demands

Buyers penalize delays due to project-critical timelines; 2024 OTIF benchmarks sit around 95%, and strong inventory programs plus technical support materially reduce customer bargaining power. Collaborative planning and VMI—often cutting inventory 20–30%—deepen lock-in and raise switching costs. Poor service rapidly shifts leverage back to buyers via churn and penalties.

- OTIF ≥95%

- VMI: −20–30% inventory

- Collaborative planning: +10–15% forecast accuracy

- Service failures → rapid churn

ESG and lifecycle requirements

- Demand: buyers require low-carbon/recyclable inputs

- Regulation: CSRD ~49,000 firms covered in 2024

- Advantage: EPDs/circularity enable premiums

- Risk: noncompliance → substitution and tougher terms

Buyers force 5-15% concessions; VMI, OTIF and EPDs reshape 2024 tenders

Customers exert moderate-strong power: framework tenders drive 5–15% price concessions in 2024, large buyers leverage regional scope and re-tenders every 3–5 years. High switching costs from approvals and >95% OTIF preserve incumbency, while VMI (-20–30% inventory) and low-carbon demands (CSRD ~49,000 firms in 2024) shift negotiation toward suppliers offering EPDs.

| Metric | 2024 Value | Impact |

|---|---|---|

| Price concessions | 5–15% | Margin pressure |

| Re-tender cycle | 3–5 yrs | Periodic leverage |

| OTIF | >=95% | Incumbency |

| VMI | -20–30% inventory | Lock-in |

| CSRD coverage | ~49,000 firms | Higher sustainability demands |

Preview Before You Purchase

Reka Industrial Porter's Five Forces Analysis

This preview shows the exact Reka Industrial Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders or samples. The document displayed is the professionally formatted, ready-to-use file included with your order. Once you buy, you’ll get instant access to this identical analysis.