Renault Porter's Five Forces Analysis

From Overview to Strategy Blueprint

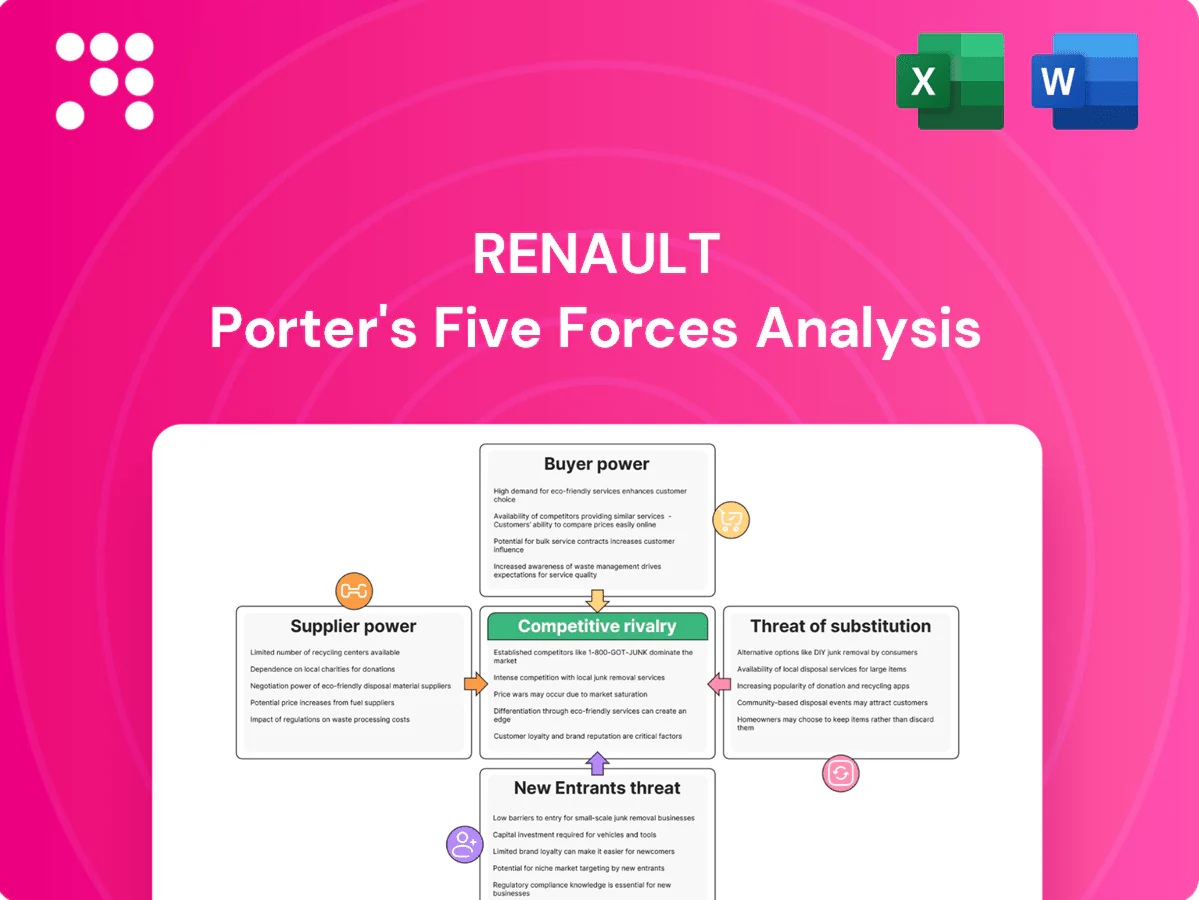

Renault faces shifting competitive dynamics—moderate supplier power, strong buyer expectations, intensifying rivalry, evolving substitute threats, and regulatory pressures shaping margins and strategy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Renault’s competitive intensity and strategic opportunities in depth.

Suppliers Bargaining Power

Critical components concentration

Semiconductors, batteries and advanced electronics are concentrated among a few Tier‑1 suppliers—the top three automotive semiconductor vendors held about 60% of the market in 2024 and the top five cell makers controlled roughly 80% of EV cell capacity—raising supplier leverage on price and delivery. Shortages or geopolitical constraints can quickly disrupt Renault’s cadence. Long‑term contracts and dual‑sourcing mitigate risk, but switching costs and qualification times stay high. Alliance scale and supplier development partially offset this power.

Battery and raw materials volatility

Batteries and raw-material swings—lithium, nickel, cobalt plus steel/aluminium—directly squeeze Renault margins; upstream processing is highly concentrated, with China accounting for over 70% of cathode and precursor capacity. Renault’s push for localized battery ecosystems and recycling partnerships in 2023–24 aims to dampen volatility and feed supply resilience. Index-based contracts and hedges limit exposure but cannot fully remove price or geopolitical risk.

Software and ADAS dependence

Reliance on specialized software, ASICs and sensor vendors creates technical lock-in for Renault, amplified by integration and certification costs that raise switching barriers and bring suppliers leverage; the automotive semiconductor market reached about $63.5 billion in 2024. Over-the-air architectures can diversify partners over time. Renault’s ramp-up of in-house software teams and strategic alliances aims to rebalance supplier bargaining power.

Logistics and just-in-time sensitivity

Global logistics constraints have kept freight costs elevated—around 20% above pre‑pandemic levels in 2024—raising delivery risk for Renault; JIT models turn supplier delays into plant stoppages, with some OEMs reporting weeks of lost production in 2021–24. Nearshoring and inventory buffers improve resilience but increase working capital needs, while multi‑modal routes and digital visibility cut disruption lead times.

- Freight +20% vs 2019

- JIT → plant stoppage risk

- Nearshoring ups working capital

- Multi‑modal + digital = lower lead‑time shocks

Alliance scale and localization

Renault’s Alliance purchasing leverage secures better terms with Tier-1s and supports localized sourcing in Europe, Morocco and Turkey to cut currency and tariff exposure; top battery-cell makers remain concentrated, with the top 10 suppliers accounting for about 85% of global capacity in 2024, limiting vendor competition for specialized EV components.

- Alliance scale: stronger Tier-1 terms

- Localization: reduced tariff/currency risk

- Supplier dev: quality and cost-downs

- EV parts: limited vendor competition (~top10 = 85% capacity 2024)

Supplier power: top-3 semis ≈60%, top-5 cells ≈80%

Supplier power is high for Renault: top-three semiconductors ≈60% (2024) and top-five EV cell makers ≈80% of capacity, creating price and delivery leverage. Upstream raw materials and China’s >70% cathode/precursor capacity amplify margin risk. Freight +20% vs 2019 and $63.5B automotive semiconductor market (2024) raise switching costs despite Alliance buying power.

| Metric | 2024 Value |

|---|---|

| Top-3 semiconductors | ~60% |

| Top-5 EV cell capacity | ~80% |

| Top-10 cell makers | ~85% |

| China cathode capacity | >70% |

| Freight vs 2019 | +20% |

| Auto sem market | $63.5B |

What is included in the product

Tailored Porter’s Five Forces assessment for Renault that uncovers competitive intensity, supplier and buyer bargaining power, threats from new entrants and substitutes, and regulatory/technological disruptors—paired with industry context and strategic implications.

A compact Renault Porter's Five Forces snapshot that highlights supplier, buyer, rivalry, entrant, and substitute pressures—ideal for quick strategy calls, customizable to reflect EV shifts and regulatory changes.

Customers Bargaining Power

Price-sensitive mass market

Renault and Dacia target price-sensitive, value-conscious buyers with elastic demand, Dacia entry-level models starting around €6,990 in 2024. Buyers compare aggressively across brands and trims online, using configurators and marketplaces that amplify switching. Discounts, financing and total cost of ownership considerations dominate purchase choices and increase buyer leverage. Cost leadership and crystal-clear value propositions are therefore essential.

Fleet and LCV procurement

Corporate, rental and public fleets negotiate steep volume-based pricing and bundled service packages, using standardized specs to heighten comparability and bargaining power. Total lifecycle cost and uptime (fleets target 3–5 year replacement cycles and >95% availability) drive procurement decisions. Renault’s 2024 refreshed LCV lineup, scale and dense service network help offset buyer leverage.

EV incentives and charging concerns

Consumer willingness to pay for Renault EVs hinges on subsidies, energy prices and charging access, with EU public chargers surpassing roughly 500,000 units by end-2024, shifting negotiation leverage to buyers. Rapid policy changes in 2024 altered demand and dealer bargaining power. Transparent TCO calculators and bundled home/public charging cut purchase hesitation, while Renaults 8-year/160,000km battery warranty plus OTA software updates raise perceived value.

Low switching costs and transparency

Digital platforms in 2024 enable instant cross-shopping on price and features, lowering bargaining power as consumers compare models and trims in real time; switching between mainstream brands remains relatively easy given similar feature sets and dealer networks. Certified used programs like Renault Selection compete directly with new sales, while loyalty programs and connected services aim to raise customer stickiness.

- Cross-shopping via digital platforms (2024)

- Low switching costs among mainstream brands

- Certified used programs compete with new sales

- Loyalty & connected services increase retention

Brand and design expectations

Styling, infotainment and safety tech are central to customer bargaining power as buyers increasingly choose vehicles on perceived design and connected features; Renault rolled out the Renault 5 prototype in 2024 to signal design-led EV intent.

Poor reviews or recalls can quickly depress demand and force incentives; Alpine’s performance halo (A110 limited series) supports Renault’s brand equity at the margin.

Continuous refresh cycles are required to retain pricing power amid fast tech turnover.

- 2024 model refreshes: Renault 5 prototype launched

- Alpine: limited-series halo effect

- Design, infotainment, safety = purchase drivers

- Recalls/reviews can rapidly shift demand

High buyer leverage: price-driven retail, fleet pressure; EVs hinge on subsidies, chargers

Renault/Dacia face high buyer leverage: price-sensitive retail buyers cross-shop (Dacia entry from €6,990) and digital platforms lower switching costs. Fleets exert strong volume bargaining, driven by >95% uptime targets and 3–5yr replacement cycles. EV demand/pricing tied to subsidies, charging access (~500,000+ EU public chargers end‑2024) and Renault’s 8y/160,000km battery warranty.

| Metric | 2024 |

|---|---|

| Entry price (Dacia) | €6,990 |

| EU public chargers | ~500,000+ |

| Battery warranty | 8y /160,000km |

| Fleet uptime target | >95% |

Same Document Delivered

Renault Porter's Five Forces Analysis

This preview shows the exact Renault Porter’s Five Forces analysis you'll receive after purchase—no placeholders. It covers competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. The file is fully formatted and ready for immediate download and use.

From Overview to Strategy Blueprint

Renault faces shifting competitive dynamics—moderate supplier power, strong buyer expectations, intensifying rivalry, evolving substitute threats, and regulatory pressures shaping margins and strategy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Renault’s competitive intensity and strategic opportunities in depth.

Suppliers Bargaining Power

Critical components concentration

Semiconductors, batteries and advanced electronics are concentrated among a few Tier‑1 suppliers—the top three automotive semiconductor vendors held about 60% of the market in 2024 and the top five cell makers controlled roughly 80% of EV cell capacity—raising supplier leverage on price and delivery. Shortages or geopolitical constraints can quickly disrupt Renault’s cadence. Long‑term contracts and dual‑sourcing mitigate risk, but switching costs and qualification times stay high. Alliance scale and supplier development partially offset this power.

Battery and raw materials volatility

Batteries and raw-material swings—lithium, nickel, cobalt plus steel/aluminium—directly squeeze Renault margins; upstream processing is highly concentrated, with China accounting for over 70% of cathode and precursor capacity. Renault’s push for localized battery ecosystems and recycling partnerships in 2023–24 aims to dampen volatility and feed supply resilience. Index-based contracts and hedges limit exposure but cannot fully remove price or geopolitical risk.

Software and ADAS dependence

Reliance on specialized software, ASICs and sensor vendors creates technical lock-in for Renault, amplified by integration and certification costs that raise switching barriers and bring suppliers leverage; the automotive semiconductor market reached about $63.5 billion in 2024. Over-the-air architectures can diversify partners over time. Renault’s ramp-up of in-house software teams and strategic alliances aims to rebalance supplier bargaining power.

Logistics and just-in-time sensitivity

Global logistics constraints have kept freight costs elevated—around 20% above pre‑pandemic levels in 2024—raising delivery risk for Renault; JIT models turn supplier delays into plant stoppages, with some OEMs reporting weeks of lost production in 2021–24. Nearshoring and inventory buffers improve resilience but increase working capital needs, while multi‑modal routes and digital visibility cut disruption lead times.

- Freight +20% vs 2019

- JIT → plant stoppage risk

- Nearshoring ups working capital

- Multi‑modal + digital = lower lead‑time shocks

Alliance scale and localization

Renault’s Alliance purchasing leverage secures better terms with Tier-1s and supports localized sourcing in Europe, Morocco and Turkey to cut currency and tariff exposure; top battery-cell makers remain concentrated, with the top 10 suppliers accounting for about 85% of global capacity in 2024, limiting vendor competition for specialized EV components.

- Alliance scale: stronger Tier-1 terms

- Localization: reduced tariff/currency risk

- Supplier dev: quality and cost-downs

- EV parts: limited vendor competition (~top10 = 85% capacity 2024)

Supplier power: top-3 semis ≈60%, top-5 cells ≈80%

Supplier power is high for Renault: top-three semiconductors ≈60% (2024) and top-five EV cell makers ≈80% of capacity, creating price and delivery leverage. Upstream raw materials and China’s >70% cathode/precursor capacity amplify margin risk. Freight +20% vs 2019 and $63.5B automotive semiconductor market (2024) raise switching costs despite Alliance buying power.

| Metric | 2024 Value |

|---|---|

| Top-3 semiconductors | ~60% |

| Top-5 EV cell capacity | ~80% |

| Top-10 cell makers | ~85% |

| China cathode capacity | >70% |

| Freight vs 2019 | +20% |

| Auto sem market | $63.5B |

What is included in the product

Tailored Porter’s Five Forces assessment for Renault that uncovers competitive intensity, supplier and buyer bargaining power, threats from new entrants and substitutes, and regulatory/technological disruptors—paired with industry context and strategic implications.

A compact Renault Porter's Five Forces snapshot that highlights supplier, buyer, rivalry, entrant, and substitute pressures—ideal for quick strategy calls, customizable to reflect EV shifts and regulatory changes.

Customers Bargaining Power

Price-sensitive mass market

Renault and Dacia target price-sensitive, value-conscious buyers with elastic demand, Dacia entry-level models starting around €6,990 in 2024. Buyers compare aggressively across brands and trims online, using configurators and marketplaces that amplify switching. Discounts, financing and total cost of ownership considerations dominate purchase choices and increase buyer leverage. Cost leadership and crystal-clear value propositions are therefore essential.

Fleet and LCV procurement

Corporate, rental and public fleets negotiate steep volume-based pricing and bundled service packages, using standardized specs to heighten comparability and bargaining power. Total lifecycle cost and uptime (fleets target 3–5 year replacement cycles and >95% availability) drive procurement decisions. Renault’s 2024 refreshed LCV lineup, scale and dense service network help offset buyer leverage.

EV incentives and charging concerns

Consumer willingness to pay for Renault EVs hinges on subsidies, energy prices and charging access, with EU public chargers surpassing roughly 500,000 units by end-2024, shifting negotiation leverage to buyers. Rapid policy changes in 2024 altered demand and dealer bargaining power. Transparent TCO calculators and bundled home/public charging cut purchase hesitation, while Renaults 8-year/160,000km battery warranty plus OTA software updates raise perceived value.

Low switching costs and transparency

Digital platforms in 2024 enable instant cross-shopping on price and features, lowering bargaining power as consumers compare models and trims in real time; switching between mainstream brands remains relatively easy given similar feature sets and dealer networks. Certified used programs like Renault Selection compete directly with new sales, while loyalty programs and connected services aim to raise customer stickiness.

- Cross-shopping via digital platforms (2024)

- Low switching costs among mainstream brands

- Certified used programs compete with new sales

- Loyalty & connected services increase retention

Brand and design expectations

Styling, infotainment and safety tech are central to customer bargaining power as buyers increasingly choose vehicles on perceived design and connected features; Renault rolled out the Renault 5 prototype in 2024 to signal design-led EV intent.

Poor reviews or recalls can quickly depress demand and force incentives; Alpine’s performance halo (A110 limited series) supports Renault’s brand equity at the margin.

Continuous refresh cycles are required to retain pricing power amid fast tech turnover.

- 2024 model refreshes: Renault 5 prototype launched

- Alpine: limited-series halo effect

- Design, infotainment, safety = purchase drivers

- Recalls/reviews can rapidly shift demand

High buyer leverage: price-driven retail, fleet pressure; EVs hinge on subsidies, chargers

Renault/Dacia face high buyer leverage: price-sensitive retail buyers cross-shop (Dacia entry from €6,990) and digital platforms lower switching costs. Fleets exert strong volume bargaining, driven by >95% uptime targets and 3–5yr replacement cycles. EV demand/pricing tied to subsidies, charging access (~500,000+ EU public chargers end‑2024) and Renault’s 8y/160,000km battery warranty.

| Metric | 2024 |

|---|---|

| Entry price (Dacia) | €6,990 |

| EU public chargers | ~500,000+ |

| Battery warranty | 8y /160,000km |

| Fleet uptime target | >95% |

Same Document Delivered

Renault Porter's Five Forces Analysis

This preview shows the exact Renault Porter’s Five Forces analysis you'll receive after purchase—no placeholders. It covers competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. The file is fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Renault faces shifting competitive dynamics—moderate supplier power, strong buyer expectations, intensifying rivalry, evolving substitute threats, and regulatory pressures shaping margins and strategy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Renault’s competitive intensity and strategic opportunities in depth.

Suppliers Bargaining Power

Critical components concentration

Semiconductors, batteries and advanced electronics are concentrated among a few Tier‑1 suppliers—the top three automotive semiconductor vendors held about 60% of the market in 2024 and the top five cell makers controlled roughly 80% of EV cell capacity—raising supplier leverage on price and delivery. Shortages or geopolitical constraints can quickly disrupt Renault’s cadence. Long‑term contracts and dual‑sourcing mitigate risk, but switching costs and qualification times stay high. Alliance scale and supplier development partially offset this power.

Battery and raw materials volatility

Batteries and raw-material swings—lithium, nickel, cobalt plus steel/aluminium—directly squeeze Renault margins; upstream processing is highly concentrated, with China accounting for over 70% of cathode and precursor capacity. Renault’s push for localized battery ecosystems and recycling partnerships in 2023–24 aims to dampen volatility and feed supply resilience. Index-based contracts and hedges limit exposure but cannot fully remove price or geopolitical risk.

Software and ADAS dependence

Reliance on specialized software, ASICs and sensor vendors creates technical lock-in for Renault, amplified by integration and certification costs that raise switching barriers and bring suppliers leverage; the automotive semiconductor market reached about $63.5 billion in 2024. Over-the-air architectures can diversify partners over time. Renault’s ramp-up of in-house software teams and strategic alliances aims to rebalance supplier bargaining power.

Logistics and just-in-time sensitivity

Global logistics constraints have kept freight costs elevated—around 20% above pre‑pandemic levels in 2024—raising delivery risk for Renault; JIT models turn supplier delays into plant stoppages, with some OEMs reporting weeks of lost production in 2021–24. Nearshoring and inventory buffers improve resilience but increase working capital needs, while multi‑modal routes and digital visibility cut disruption lead times.

- Freight +20% vs 2019

- JIT → plant stoppage risk

- Nearshoring ups working capital

- Multi‑modal + digital = lower lead‑time shocks

Alliance scale and localization

Renault’s Alliance purchasing leverage secures better terms with Tier-1s and supports localized sourcing in Europe, Morocco and Turkey to cut currency and tariff exposure; top battery-cell makers remain concentrated, with the top 10 suppliers accounting for about 85% of global capacity in 2024, limiting vendor competition for specialized EV components.

- Alliance scale: stronger Tier-1 terms

- Localization: reduced tariff/currency risk

- Supplier dev: quality and cost-downs

- EV parts: limited vendor competition (~top10 = 85% capacity 2024)

Supplier power: top-3 semis ≈60%, top-5 cells ≈80%

Supplier power is high for Renault: top-three semiconductors ≈60% (2024) and top-five EV cell makers ≈80% of capacity, creating price and delivery leverage. Upstream raw materials and China’s >70% cathode/precursor capacity amplify margin risk. Freight +20% vs 2019 and $63.5B automotive semiconductor market (2024) raise switching costs despite Alliance buying power.

| Metric | 2024 Value |

|---|---|

| Top-3 semiconductors | ~60% |

| Top-5 EV cell capacity | ~80% |

| Top-10 cell makers | ~85% |

| China cathode capacity | >70% |

| Freight vs 2019 | +20% |

| Auto sem market | $63.5B |

What is included in the product

Tailored Porter’s Five Forces assessment for Renault that uncovers competitive intensity, supplier and buyer bargaining power, threats from new entrants and substitutes, and regulatory/technological disruptors—paired with industry context and strategic implications.

A compact Renault Porter's Five Forces snapshot that highlights supplier, buyer, rivalry, entrant, and substitute pressures—ideal for quick strategy calls, customizable to reflect EV shifts and regulatory changes.

Customers Bargaining Power

Price-sensitive mass market

Renault and Dacia target price-sensitive, value-conscious buyers with elastic demand, Dacia entry-level models starting around €6,990 in 2024. Buyers compare aggressively across brands and trims online, using configurators and marketplaces that amplify switching. Discounts, financing and total cost of ownership considerations dominate purchase choices and increase buyer leverage. Cost leadership and crystal-clear value propositions are therefore essential.

Fleet and LCV procurement

Corporate, rental and public fleets negotiate steep volume-based pricing and bundled service packages, using standardized specs to heighten comparability and bargaining power. Total lifecycle cost and uptime (fleets target 3–5 year replacement cycles and >95% availability) drive procurement decisions. Renault’s 2024 refreshed LCV lineup, scale and dense service network help offset buyer leverage.

EV incentives and charging concerns

Consumer willingness to pay for Renault EVs hinges on subsidies, energy prices and charging access, with EU public chargers surpassing roughly 500,000 units by end-2024, shifting negotiation leverage to buyers. Rapid policy changes in 2024 altered demand and dealer bargaining power. Transparent TCO calculators and bundled home/public charging cut purchase hesitation, while Renaults 8-year/160,000km battery warranty plus OTA software updates raise perceived value.

Low switching costs and transparency

Digital platforms in 2024 enable instant cross-shopping on price and features, lowering bargaining power as consumers compare models and trims in real time; switching between mainstream brands remains relatively easy given similar feature sets and dealer networks. Certified used programs like Renault Selection compete directly with new sales, while loyalty programs and connected services aim to raise customer stickiness.

- Cross-shopping via digital platforms (2024)

- Low switching costs among mainstream brands

- Certified used programs compete with new sales

- Loyalty & connected services increase retention

Brand and design expectations

Styling, infotainment and safety tech are central to customer bargaining power as buyers increasingly choose vehicles on perceived design and connected features; Renault rolled out the Renault 5 prototype in 2024 to signal design-led EV intent.

Poor reviews or recalls can quickly depress demand and force incentives; Alpine’s performance halo (A110 limited series) supports Renault’s brand equity at the margin.

Continuous refresh cycles are required to retain pricing power amid fast tech turnover.

- 2024 model refreshes: Renault 5 prototype launched

- Alpine: limited-series halo effect

- Design, infotainment, safety = purchase drivers

- Recalls/reviews can rapidly shift demand

High buyer leverage: price-driven retail, fleet pressure; EVs hinge on subsidies, chargers

Renault/Dacia face high buyer leverage: price-sensitive retail buyers cross-shop (Dacia entry from €6,990) and digital platforms lower switching costs. Fleets exert strong volume bargaining, driven by >95% uptime targets and 3–5yr replacement cycles. EV demand/pricing tied to subsidies, charging access (~500,000+ EU public chargers end‑2024) and Renault’s 8y/160,000km battery warranty.

| Metric | 2024 |

|---|---|

| Entry price (Dacia) | €6,990 |

| EU public chargers | ~500,000+ |

| Battery warranty | 8y /160,000km |

| Fleet uptime target | >95% |

Same Document Delivered

Renault Porter's Five Forces Analysis

This preview shows the exact Renault Porter’s Five Forces analysis you'll receive after purchase—no placeholders. It covers competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. The file is fully formatted and ready for immediate download and use.