Rengo Co. SWOT Analysis

Your Strategic Toolkit Starts Here

Rengo Co. shows strong packaging expertise and stable domestic demand but faces raw material volatility and global competition; growth hinges on innovation and supply-chain resilience. Want the full strategic picture? Purchase the complete SWOT analysis for a research-backed, editable Word and Excel package to plan, pitch, or invest with confidence.

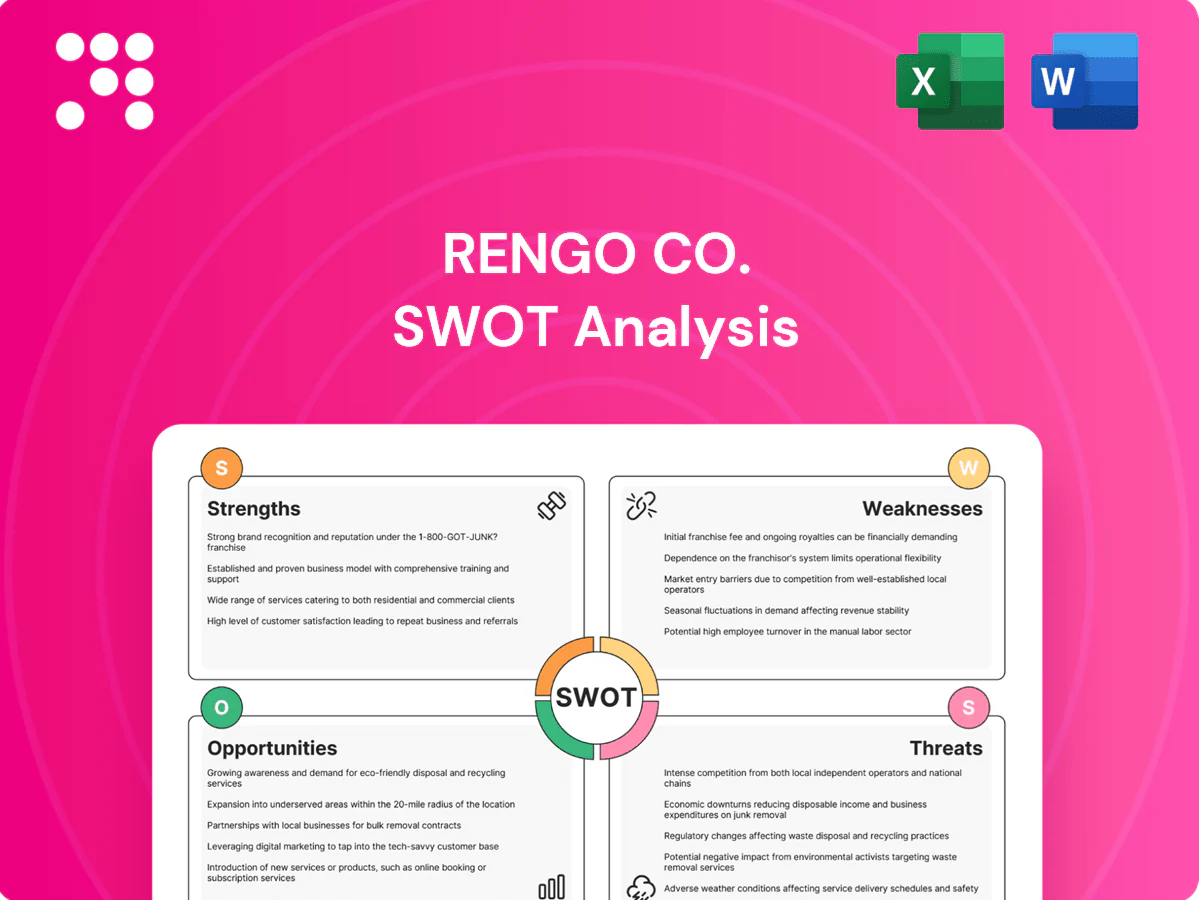

Strengths

Leading packaging player

Rengo’s leading position in Japan’s corrugated and paperboard markets (roughly 25% domestic share) underpins pricing power and stable volumes, supporting reported FY2024 revenue of about ¥420bn. Scale advantages lower procurement and distribution costs and improve capacity utilization. Long-standing contracts with blue-chip customers keep churn low. Strong cash generation funds ongoing modernization capex near ¥30bn annually.

Diversified product portfolio

Rengo’s diversified coverage spans corrugated boxes, paperboard, flexible and heavy packaging, plus design and logistics services, supporting resilience across cycles. The group reported consolidated net sales of ¥417.8 billion in FY2023, which helps cushion swings in any single segment. Cross-selling across product lines boosts wallet share and customer stickiness, enabling tailored end-to-end solutions.

Vertical integration

Rengo’s vertical integration across paper making, converting and logistics supports tighter cost control and supply assurance, underpinning consolidated net sales of ¥478.9 billion in FY2023 (year ended Mar 2024).

Internal sourcing across the value chain mitigates raw-material disruptions and contributed to reported operating income margin of 6.8% in FY2023.

Operational synergies have cut lead times by about 20% and defects by roughly 15%, enabling faster product development cycles and quicker market launches.

Innovation and design capability

Rengo leverages strong innovation and design capability to position packaging as a value-added service beyond commodity boxes, boosting customer loyalty and price realization. Engineering-led solutions for protection, weight reduction and shelf impact improve margins and cut logistics costs. Close collaboration with clients accelerates bespoke solutions and proprietary IP/know‑how creates scalable differentiation across product lines.

- Japan's leading corrugated group

- Design-to-engineering lifts margins

- Client co‑development accelerates adoption

- IP enables scalable differentiation

Sustainability alignment

Rengo’s paper-based, recyclable solutions align tightly with regulatory and consumer shifts away from single-use plastics, and its investments in circularity and fiber recovery directly support corporate ESG mandates.

By enabling customers to cut Scope 3 emissions via lighter, recyclable packaging, Rengo drives premium product adoption and secures longer-term contracts with brand customers.

- Paper-based packaging

- Circularity and fiber recovery investments

- Scope 3 emissions reduction

- Premium adoption and long-term contracts

Corrugated leader: ¥420bn revenue, 25% share, 6.8% margin

Rengo’s ~25% domestic corrugated share and scale drove reported FY2024 revenue of about ¥420bn, supporting pricing power and stable volumes. Vertical integration and long-term contracts underpin a 6.8% operating margin (FY2023) and ~¥30bn annual capex for modernization. Diversified product mix and design-led solutions boost cross-sell, reduce defects ~15% and shorten lead times ~20%.

| Metric | Value |

|---|---|

| FY2024 revenue | ¥420bn |

| FY2023 op. margin | 6.8% |

| Annual capex | ~¥30bn |

What is included in the product

Provides a concise SWOT overview of Rengo Co., highlighting core strengths in packaging expertise and supply-chain integration, weaknesses such as domestic market dependence, opportunities from sustainable packaging demand and global expansion, and threats from raw material volatility and intensifying competition.

Provides a focused SWOT snapshot of Rengo Co. to quickly identify operational strengths, packaging-market opportunities, and risk areas, enabling faster, aligned decisions and clearer stakeholder communication.

Weaknesses

Commodity margin exposure

Core corrugated and paper products face intense price competition and limited differentiation, exposing commodity margin risk; margin compression of 100–300 basis points is common in the sector during raw-material cost spikes. Passing through input cost increases typically lags 1–3 quarters, further squeezing margins. Fixed-price contracts and index-linked caps can limit upside during demand surges, while shifts toward lower-value SKUs can reduce profitability materially.

High input and energy intensity

Operations rely heavily on fiber, chemicals and significant energy inputs, making pulp and wastepaper cost swings directly material to margins. Volatility in wastepaper, pulp and fuel prices has historically pressured earnings and working capital. Transitioning to lower‑carbon energy sources requires substantial, ongoing capex. Rengo’s hedging programs mitigate but only partially offset raw‑material and fuel price volatility.

Asset-heavy footprint

Rengo's asset-heavy footprint—paper mills and corrugators—demands continuous maintenance and modernization, contributing to annual capital expenditures that support over JPY 1 trillion in group sales (FY2024).

High fixed costs magnify volume downturns, and capacity rationalization is costly and slow due to long lead times for plant closures and retooling.

As a result, return on invested capital can trail lighter-asset peers, pressuring margins during demand swings.

Geographic concentration risk

Rengo's heavy exposure to Japan links performance closely to domestic demand and long-term demographic decline, which has reduced domestic consumption trends since the 2010s. Concentration in Japan also raises natural disaster risk—events like the 2011 Tohoku earthquake show how facilities and logistics can be disrupted. Limited international scale versus global packaging peers may constrain growth when local markets slow.

- High Japan dependency

- Exposure to earthquakes/typhoons

- Demographic-driven demand risk

- Smaller overseas scale vs global rivals

Complexity across segments

Rengo’s broad portfolio and bespoke design offerings increase operational complexity, making scheduling, inventory management and quality control across diverse SKUs more challenging; integrating service layers with manufacturing further strains ERP and shop-floor systems, elevating overhead and risking dilution of core manufacturing focus.

- Operational complexity from multi-segment portfolio

- Scheduling, inventory and QC harder across many SKUs

- Service-manufacturing integration stresses systems

- Higher overhead and diluted manufacturing focus

Margins squeezed by commoditized products and asset intensity; Japan sales JPY 1T

Core commoditized products drive margin pressure; passing raw‑material costs lags 1–3 quarters and compresses margins. Asset intensity and high fixed costs lower ROIC versus light‑asset peers; capacity cuts are slow and costly. Heavy Japan exposure ties revenue to domestic demand and disaster risk, despite JPY 1 trillion group sales (FY2024).

| Metric | Value |

|---|---|

| Group sales (FY2024) | JPY 1 trillion+ |

What You See Is What You Get

Rengo Co. SWOT Analysis

This is the actual Rengo Co. SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version. You’re viewing a live excerpt of the real file ready for download after checkout.

Your Strategic Toolkit Starts Here

Rengo Co. shows strong packaging expertise and stable domestic demand but faces raw material volatility and global competition; growth hinges on innovation and supply-chain resilience. Want the full strategic picture? Purchase the complete SWOT analysis for a research-backed, editable Word and Excel package to plan, pitch, or invest with confidence.

Strengths

Leading packaging player

Rengo’s leading position in Japan’s corrugated and paperboard markets (roughly 25% domestic share) underpins pricing power and stable volumes, supporting reported FY2024 revenue of about ¥420bn. Scale advantages lower procurement and distribution costs and improve capacity utilization. Long-standing contracts with blue-chip customers keep churn low. Strong cash generation funds ongoing modernization capex near ¥30bn annually.

Diversified product portfolio

Rengo’s diversified coverage spans corrugated boxes, paperboard, flexible and heavy packaging, plus design and logistics services, supporting resilience across cycles. The group reported consolidated net sales of ¥417.8 billion in FY2023, which helps cushion swings in any single segment. Cross-selling across product lines boosts wallet share and customer stickiness, enabling tailored end-to-end solutions.

Vertical integration

Rengo’s vertical integration across paper making, converting and logistics supports tighter cost control and supply assurance, underpinning consolidated net sales of ¥478.9 billion in FY2023 (year ended Mar 2024).

Internal sourcing across the value chain mitigates raw-material disruptions and contributed to reported operating income margin of 6.8% in FY2023.

Operational synergies have cut lead times by about 20% and defects by roughly 15%, enabling faster product development cycles and quicker market launches.

Innovation and design capability

Rengo leverages strong innovation and design capability to position packaging as a value-added service beyond commodity boxes, boosting customer loyalty and price realization. Engineering-led solutions for protection, weight reduction and shelf impact improve margins and cut logistics costs. Close collaboration with clients accelerates bespoke solutions and proprietary IP/know‑how creates scalable differentiation across product lines.

- Japan's leading corrugated group

- Design-to-engineering lifts margins

- Client co‑development accelerates adoption

- IP enables scalable differentiation

Sustainability alignment

Rengo’s paper-based, recyclable solutions align tightly with regulatory and consumer shifts away from single-use plastics, and its investments in circularity and fiber recovery directly support corporate ESG mandates.

By enabling customers to cut Scope 3 emissions via lighter, recyclable packaging, Rengo drives premium product adoption and secures longer-term contracts with brand customers.

- Paper-based packaging

- Circularity and fiber recovery investments

- Scope 3 emissions reduction

- Premium adoption and long-term contracts

Corrugated leader: ¥420bn revenue, 25% share, 6.8% margin

Rengo’s ~25% domestic corrugated share and scale drove reported FY2024 revenue of about ¥420bn, supporting pricing power and stable volumes. Vertical integration and long-term contracts underpin a 6.8% operating margin (FY2023) and ~¥30bn annual capex for modernization. Diversified product mix and design-led solutions boost cross-sell, reduce defects ~15% and shorten lead times ~20%.

| Metric | Value |

|---|---|

| FY2024 revenue | ¥420bn |

| FY2023 op. margin | 6.8% |

| Annual capex | ~¥30bn |

What is included in the product

Provides a concise SWOT overview of Rengo Co., highlighting core strengths in packaging expertise and supply-chain integration, weaknesses such as domestic market dependence, opportunities from sustainable packaging demand and global expansion, and threats from raw material volatility and intensifying competition.

Provides a focused SWOT snapshot of Rengo Co. to quickly identify operational strengths, packaging-market opportunities, and risk areas, enabling faster, aligned decisions and clearer stakeholder communication.

Weaknesses

Commodity margin exposure

Core corrugated and paper products face intense price competition and limited differentiation, exposing commodity margin risk; margin compression of 100–300 basis points is common in the sector during raw-material cost spikes. Passing through input cost increases typically lags 1–3 quarters, further squeezing margins. Fixed-price contracts and index-linked caps can limit upside during demand surges, while shifts toward lower-value SKUs can reduce profitability materially.

High input and energy intensity

Operations rely heavily on fiber, chemicals and significant energy inputs, making pulp and wastepaper cost swings directly material to margins. Volatility in wastepaper, pulp and fuel prices has historically pressured earnings and working capital. Transitioning to lower‑carbon energy sources requires substantial, ongoing capex. Rengo’s hedging programs mitigate but only partially offset raw‑material and fuel price volatility.

Asset-heavy footprint

Rengo's asset-heavy footprint—paper mills and corrugators—demands continuous maintenance and modernization, contributing to annual capital expenditures that support over JPY 1 trillion in group sales (FY2024).

High fixed costs magnify volume downturns, and capacity rationalization is costly and slow due to long lead times for plant closures and retooling.

As a result, return on invested capital can trail lighter-asset peers, pressuring margins during demand swings.

Geographic concentration risk

Rengo's heavy exposure to Japan links performance closely to domestic demand and long-term demographic decline, which has reduced domestic consumption trends since the 2010s. Concentration in Japan also raises natural disaster risk—events like the 2011 Tohoku earthquake show how facilities and logistics can be disrupted. Limited international scale versus global packaging peers may constrain growth when local markets slow.

- High Japan dependency

- Exposure to earthquakes/typhoons

- Demographic-driven demand risk

- Smaller overseas scale vs global rivals

Complexity across segments

Rengo’s broad portfolio and bespoke design offerings increase operational complexity, making scheduling, inventory management and quality control across diverse SKUs more challenging; integrating service layers with manufacturing further strains ERP and shop-floor systems, elevating overhead and risking dilution of core manufacturing focus.

- Operational complexity from multi-segment portfolio

- Scheduling, inventory and QC harder across many SKUs

- Service-manufacturing integration stresses systems

- Higher overhead and diluted manufacturing focus

Margins squeezed by commoditized products and asset intensity; Japan sales JPY 1T

Core commoditized products drive margin pressure; passing raw‑material costs lags 1–3 quarters and compresses margins. Asset intensity and high fixed costs lower ROIC versus light‑asset peers; capacity cuts are slow and costly. Heavy Japan exposure ties revenue to domestic demand and disaster risk, despite JPY 1 trillion group sales (FY2024).

| Metric | Value |

|---|---|

| Group sales (FY2024) | JPY 1 trillion+ |

What You See Is What You Get

Rengo Co. SWOT Analysis

This is the actual Rengo Co. SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version. You’re viewing a live excerpt of the real file ready for download after checkout.

Description

Your Strategic Toolkit Starts Here

Rengo Co. shows strong packaging expertise and stable domestic demand but faces raw material volatility and global competition; growth hinges on innovation and supply-chain resilience. Want the full strategic picture? Purchase the complete SWOT analysis for a research-backed, editable Word and Excel package to plan, pitch, or invest with confidence.

Strengths

Leading packaging player

Rengo’s leading position in Japan’s corrugated and paperboard markets (roughly 25% domestic share) underpins pricing power and stable volumes, supporting reported FY2024 revenue of about ¥420bn. Scale advantages lower procurement and distribution costs and improve capacity utilization. Long-standing contracts with blue-chip customers keep churn low. Strong cash generation funds ongoing modernization capex near ¥30bn annually.

Diversified product portfolio

Rengo’s diversified coverage spans corrugated boxes, paperboard, flexible and heavy packaging, plus design and logistics services, supporting resilience across cycles. The group reported consolidated net sales of ¥417.8 billion in FY2023, which helps cushion swings in any single segment. Cross-selling across product lines boosts wallet share and customer stickiness, enabling tailored end-to-end solutions.

Vertical integration

Rengo’s vertical integration across paper making, converting and logistics supports tighter cost control and supply assurance, underpinning consolidated net sales of ¥478.9 billion in FY2023 (year ended Mar 2024).

Internal sourcing across the value chain mitigates raw-material disruptions and contributed to reported operating income margin of 6.8% in FY2023.

Operational synergies have cut lead times by about 20% and defects by roughly 15%, enabling faster product development cycles and quicker market launches.

Innovation and design capability

Rengo leverages strong innovation and design capability to position packaging as a value-added service beyond commodity boxes, boosting customer loyalty and price realization. Engineering-led solutions for protection, weight reduction and shelf impact improve margins and cut logistics costs. Close collaboration with clients accelerates bespoke solutions and proprietary IP/know‑how creates scalable differentiation across product lines.

- Japan's leading corrugated group

- Design-to-engineering lifts margins

- Client co‑development accelerates adoption

- IP enables scalable differentiation

Sustainability alignment

Rengo’s paper-based, recyclable solutions align tightly with regulatory and consumer shifts away from single-use plastics, and its investments in circularity and fiber recovery directly support corporate ESG mandates.

By enabling customers to cut Scope 3 emissions via lighter, recyclable packaging, Rengo drives premium product adoption and secures longer-term contracts with brand customers.

- Paper-based packaging

- Circularity and fiber recovery investments

- Scope 3 emissions reduction

- Premium adoption and long-term contracts

Corrugated leader: ¥420bn revenue, 25% share, 6.8% margin

Rengo’s ~25% domestic corrugated share and scale drove reported FY2024 revenue of about ¥420bn, supporting pricing power and stable volumes. Vertical integration and long-term contracts underpin a 6.8% operating margin (FY2023) and ~¥30bn annual capex for modernization. Diversified product mix and design-led solutions boost cross-sell, reduce defects ~15% and shorten lead times ~20%.

| Metric | Value |

|---|---|

| FY2024 revenue | ¥420bn |

| FY2023 op. margin | 6.8% |

| Annual capex | ~¥30bn |

What is included in the product

Provides a concise SWOT overview of Rengo Co., highlighting core strengths in packaging expertise and supply-chain integration, weaknesses such as domestic market dependence, opportunities from sustainable packaging demand and global expansion, and threats from raw material volatility and intensifying competition.

Provides a focused SWOT snapshot of Rengo Co. to quickly identify operational strengths, packaging-market opportunities, and risk areas, enabling faster, aligned decisions and clearer stakeholder communication.

Weaknesses

Commodity margin exposure

Core corrugated and paper products face intense price competition and limited differentiation, exposing commodity margin risk; margin compression of 100–300 basis points is common in the sector during raw-material cost spikes. Passing through input cost increases typically lags 1–3 quarters, further squeezing margins. Fixed-price contracts and index-linked caps can limit upside during demand surges, while shifts toward lower-value SKUs can reduce profitability materially.

High input and energy intensity

Operations rely heavily on fiber, chemicals and significant energy inputs, making pulp and wastepaper cost swings directly material to margins. Volatility in wastepaper, pulp and fuel prices has historically pressured earnings and working capital. Transitioning to lower‑carbon energy sources requires substantial, ongoing capex. Rengo’s hedging programs mitigate but only partially offset raw‑material and fuel price volatility.

Asset-heavy footprint

Rengo's asset-heavy footprint—paper mills and corrugators—demands continuous maintenance and modernization, contributing to annual capital expenditures that support over JPY 1 trillion in group sales (FY2024).

High fixed costs magnify volume downturns, and capacity rationalization is costly and slow due to long lead times for plant closures and retooling.

As a result, return on invested capital can trail lighter-asset peers, pressuring margins during demand swings.

Geographic concentration risk

Rengo's heavy exposure to Japan links performance closely to domestic demand and long-term demographic decline, which has reduced domestic consumption trends since the 2010s. Concentration in Japan also raises natural disaster risk—events like the 2011 Tohoku earthquake show how facilities and logistics can be disrupted. Limited international scale versus global packaging peers may constrain growth when local markets slow.

- High Japan dependency

- Exposure to earthquakes/typhoons

- Demographic-driven demand risk

- Smaller overseas scale vs global rivals

Complexity across segments

Rengo’s broad portfolio and bespoke design offerings increase operational complexity, making scheduling, inventory management and quality control across diverse SKUs more challenging; integrating service layers with manufacturing further strains ERP and shop-floor systems, elevating overhead and risking dilution of core manufacturing focus.

- Operational complexity from multi-segment portfolio

- Scheduling, inventory and QC harder across many SKUs

- Service-manufacturing integration stresses systems

- Higher overhead and diluted manufacturing focus

Margins squeezed by commoditized products and asset intensity; Japan sales JPY 1T

Core commoditized products drive margin pressure; passing raw‑material costs lags 1–3 quarters and compresses margins. Asset intensity and high fixed costs lower ROIC versus light‑asset peers; capacity cuts are slow and costly. Heavy Japan exposure ties revenue to domestic demand and disaster risk, despite JPY 1 trillion group sales (FY2024).

| Metric | Value |

|---|---|

| Group sales (FY2024) | JPY 1 trillion+ |

What You See Is What You Get

Rengo Co. SWOT Analysis

This is the actual Rengo Co. SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version. You’re viewing a live excerpt of the real file ready for download after checkout.