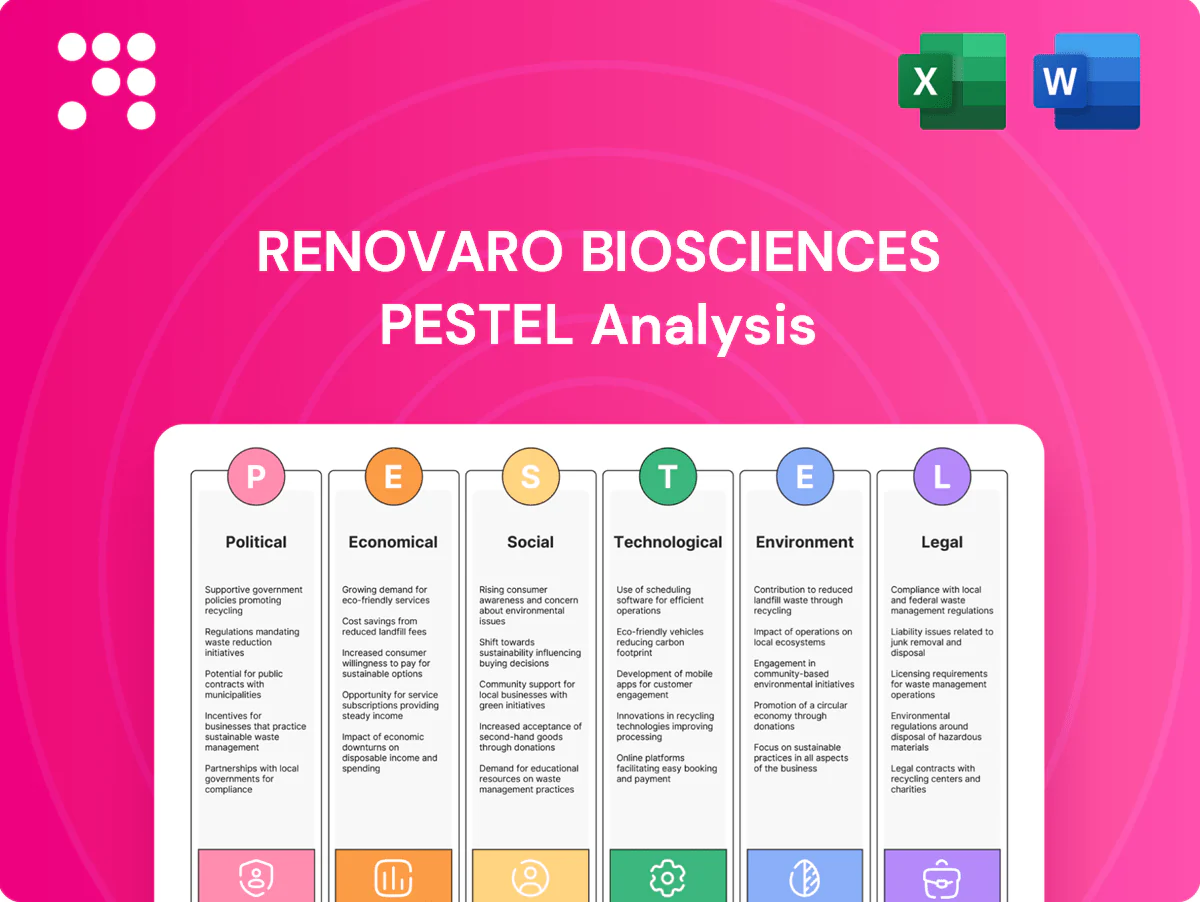

Renovaro Biosciences PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock how political shifts, market forces, and tech advances are shaping Renovaro Biosciences’ prospects with our concise PESTLE snapshot—then dive deeper with the full analysis to inform investments, strategy, and risk planning. Download the complete report now for actionable insights.

Political factors

Regulatory prioritization and agency stance

Shifts in FDA, EMA and global regulators’ priorities for cell, gene and immunotherapies can accelerate or delay Renovaro’s programs; FDA Priority Review shortens review to 6 months vs 10 months standard. RMAT (est 2017), Breakthrough, Fast Track and EMA PRIME (est 2016) materially affect timelines and capital needs. Alignment with oncology/HIV/infectious‑disease goals often unlocks expedited pathways.

Public health funding and grants

NIH funding (~$49B FY2024), BARDA appropriations (~$1.7B) and international agency budgets (WHO base ~ $1.5B 2024–25) materially drive non-dilutive grants for HIV and infectious disease platforms.

Election and budget cycles can rapidly expand or contract grant pools, so aligning programs to national priorities raises award and partnership odds.

Sustained cuts would force Renovaro toward greater equity raises or strategic licensing and consortium partnerships to fund development.

Drug pricing and reimbursement policy

Government scrutiny of advanced therapy pricing—highlighted by the US Inflation Reduction Act price negotiation beginning 2026—shapes Renovaro Biosciences market access and revenue. Reference pricing and HTA thresholds such as UK NICE’s £20,000–£30,000/QALY range can compress margins versus list prices for gene therapies like Zolgensma at $2.1m and Luxturna at $850k. Political pressure favors value-based contracts and outcomes-linked rebates, making early pharmacoeconomic evidence critical for policy acceptance.

Geopolitical supply chain stability

Export controls, sanctions and trade tensions have restricted access to vector components and specialized reagents, driving shipment delays of roughly 2–12 weeks and pushing inventory carrying costs up an estimated 15–30% for biotechs. Political instability in supplier regions increases lead-time variability and contingency spend; diversifying suppliers and sourcing geographies reduces disruption risk and single‑country concentration. Cross-border clinical trials frequently face visa backlogs, customs holds and data transfer constraints that can delay enrollment and add regulatory compliance costs.

- Export controls: restricted inputs, 2–12 week delays

- Inventory impact: +15–30% carrying costs

- Mitigation: supplier/geography diversification

- Trials: visa, customs, data transfer constraints

Pandemic preparedness and biodefense agendas

Governments prioritizing infectious-disease resilience has accelerated regulatory reviews and collaborations, as seen after Operation Warp Speed mobilized about 18 billion USD in 2020; WHO estimates a roughly 10.5 billion USD annual gap for global preparedness. Reduced policy focus would slow partnering momentum, while platform-agile policies favor modular immunotherapy and public-private consortia de-risk development.

- Policy push: accelerates reviews & partnerships

- Risk: funding shift = lower partnering momentum

- Tech fit: modular platforms favored

- De-risk: consortia reduce clinical & commercial risk

Expedited regs: FDA 6m; public funding $49B

Regulatory expedited pathways (RMAT/Breakthrough/Fast Track/EMA PRIME) materially shorten timelines and capital needs; FDA Priority Review cuts review to 6 months. Public funding shapes non-dilutive support: NIH ~$49B FY2024, BARDA ~$1.7B; policy shifts alter grant pools. Pricing/payer rules (US IRA negotiations 2026, NICE £20–30k/QALY) and export controls (2–12 week delays; +15–30% inventory) affect market access and costs.

| Metric | Value |

|---|---|

| NIH FY2024 | $49B |

| BARDA | $1.7B |

| Operation Warp Speed | $18B |

| WHO preparedness gap | $10.5B/yr |

| Export delays | 2–12 weeks |

| Inventory impact | +15–30% |

| Zolgensma list price | $2.1M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Renovaro Biosciences, with data-backed, region- and industry-specific insights to identify risks, opportunities and strategic responses; designed for executives, investors and planners and formatted for immediate use.

Renovaro Biosciences PESTLE provides a clean, visually segmented summary of external risks and market drivers for quick reference in meetings or presentations, easily shareable and drop‑in ready for slide decks; its clear language and editable notes make it a practical pain‑point reliever for aligning teams and supporting strategy discussions.

Economic factors

Capital market conditions and cost of capital

Biotech funding cycles and elevated interest rates (US fed funds roughly 5.25–5.50% in 2024–2025) raise Renovaro’s cost of capital, shortening runway and compressing valuations. Risk-on markets ease follow-on financings, while tightening liquidity forces strict pipeline prioritization and milestone-focused de‑risking. Milestone-driven catalysts are vital to access capital efficiently and strategic partnerships can offset dilution during risk-off periods.

Manufacturing scale-up and COGS

Advanced therapy GMP manufacturing is capital-intensive (clinical-to-commercial suites often cost $50–200m in 2024) and highly yield-sensitive. Vector, cell processing and QC can drive per-dose COGS from $20k to $200k, directly squeezing gross margins and pricing flexibility. Early process optimization commonly cuts per-dose costs 30–60% and lowers supply risk. Outsourcing reduces near-term capex but typically raises per-dose costs 20–40% versus in-house control.

Payer willingness-to-pay and HTA outcomes

Oncology and HIV programs are rewarded for meaningful survival or functional cure endpoints; HTAs enforce cost-effectiveness thresholds (NICE £20–30k/QALY; US commonly $100–150k/QALY). Payers have supported premium prices for strong real-world evidence (RWE) with observed uplifts of ~10–25%; weak comparative effectiveness often collapses reimbursement and adoption, as seen with slower uptake of therapies priced like CAR-Ts ($373–475k) or gene therapies ($2.1M).

M&A and partnership landscape

Large pharmas favor de‑risked cell, gene and immunotherapy assets, setting deal comps; 2024 recorded over 200 relevant licensing/M&A transactions globally, shaping valuation benchmarks. Option‑to‑buy and co‑development structures increasingly fund late‑stage trials with multi‑million upfronts and milestone pools, while rising competitive interest boosts bargaining power and tougher milestone terms; consolidation may amplify or ease pressure.

- Deal volume: >200 cell/gene/immuno deals (2024)

- Structures: option‑to‑buy & co‑dev fund late‑stage trials

- Terms: stronger partner bargaining, higher milestone demands

- Consolidation: can intensify or relieve competition

Labor and input inflation

Talent competition for GMP, computational biology and clinical ops is pushing compensation higher—biochemists/biophysicists median pay was about $102,690 in May 2023 (BLS)—while reagent and vector component inflation has increased trial costs and COGS; global biotech VC funding fell roughly 30% in 2023, tightening sponsor capital. Long-term vendor contracts can cap input price volatility, but economic downturns may lower labor cost pressure even as financing becomes constrained.

- Wage pressure: BLS median pay ~$102,690 (May 2023)

- Input inflation: higher reagent/vector costs raising COGS

- Mitigation: long-term vendor contracts stabilize pricing

- Macro: downturn eases wages but limits financing (VC down ~30% in 2023)

Expedited regs: FDA 6m; public funding $49B

Higher rates (Fed funds ~5.25–5.50% in 2024–25) raise Renovaro’s cost of capital, shortening runway and pressuring valuations. GMP buildouts ($50–200M) and per‑dose COGS ($20k–$200k) compress margins; outsourcing trades capex for 20–40% higher unit costs. VC funding down ~30% (2023) and >200 cell/gene deals (2024) shape partnering and milestone-driven financing.

| Metric | Value |

|---|---|

| Fed funds (2024–25) | 5.25–5.50% |

| GMP capex | $50–200M |

| Per‑dose COGS | $20k–$200k |

| VC funding change (2023) | −30% |

| Deals (2024) | >200 |

Preview the Actual Deliverable

Renovaro Biosciences PESTLE Analysis

The Renovaro Biosciences PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—this is the finished file you’ll download immediately after buying.

Skip the Research. Get the Strategy.

Unlock how political shifts, market forces, and tech advances are shaping Renovaro Biosciences’ prospects with our concise PESTLE snapshot—then dive deeper with the full analysis to inform investments, strategy, and risk planning. Download the complete report now for actionable insights.

Political factors

Regulatory prioritization and agency stance

Shifts in FDA, EMA and global regulators’ priorities for cell, gene and immunotherapies can accelerate or delay Renovaro’s programs; FDA Priority Review shortens review to 6 months vs 10 months standard. RMAT (est 2017), Breakthrough, Fast Track and EMA PRIME (est 2016) materially affect timelines and capital needs. Alignment with oncology/HIV/infectious‑disease goals often unlocks expedited pathways.

Public health funding and grants

NIH funding (~$49B FY2024), BARDA appropriations (~$1.7B) and international agency budgets (WHO base ~ $1.5B 2024–25) materially drive non-dilutive grants for HIV and infectious disease platforms.

Election and budget cycles can rapidly expand or contract grant pools, so aligning programs to national priorities raises award and partnership odds.

Sustained cuts would force Renovaro toward greater equity raises or strategic licensing and consortium partnerships to fund development.

Drug pricing and reimbursement policy

Government scrutiny of advanced therapy pricing—highlighted by the US Inflation Reduction Act price negotiation beginning 2026—shapes Renovaro Biosciences market access and revenue. Reference pricing and HTA thresholds such as UK NICE’s £20,000–£30,000/QALY range can compress margins versus list prices for gene therapies like Zolgensma at $2.1m and Luxturna at $850k. Political pressure favors value-based contracts and outcomes-linked rebates, making early pharmacoeconomic evidence critical for policy acceptance.

Geopolitical supply chain stability

Export controls, sanctions and trade tensions have restricted access to vector components and specialized reagents, driving shipment delays of roughly 2–12 weeks and pushing inventory carrying costs up an estimated 15–30% for biotechs. Political instability in supplier regions increases lead-time variability and contingency spend; diversifying suppliers and sourcing geographies reduces disruption risk and single‑country concentration. Cross-border clinical trials frequently face visa backlogs, customs holds and data transfer constraints that can delay enrollment and add regulatory compliance costs.

- Export controls: restricted inputs, 2–12 week delays

- Inventory impact: +15–30% carrying costs

- Mitigation: supplier/geography diversification

- Trials: visa, customs, data transfer constraints

Pandemic preparedness and biodefense agendas

Governments prioritizing infectious-disease resilience has accelerated regulatory reviews and collaborations, as seen after Operation Warp Speed mobilized about 18 billion USD in 2020; WHO estimates a roughly 10.5 billion USD annual gap for global preparedness. Reduced policy focus would slow partnering momentum, while platform-agile policies favor modular immunotherapy and public-private consortia de-risk development.

- Policy push: accelerates reviews & partnerships

- Risk: funding shift = lower partnering momentum

- Tech fit: modular platforms favored

- De-risk: consortia reduce clinical & commercial risk

Expedited regs: FDA 6m; public funding $49B

Regulatory expedited pathways (RMAT/Breakthrough/Fast Track/EMA PRIME) materially shorten timelines and capital needs; FDA Priority Review cuts review to 6 months. Public funding shapes non-dilutive support: NIH ~$49B FY2024, BARDA ~$1.7B; policy shifts alter grant pools. Pricing/payer rules (US IRA negotiations 2026, NICE £20–30k/QALY) and export controls (2–12 week delays; +15–30% inventory) affect market access and costs.

| Metric | Value |

|---|---|

| NIH FY2024 | $49B |

| BARDA | $1.7B |

| Operation Warp Speed | $18B |

| WHO preparedness gap | $10.5B/yr |

| Export delays | 2–12 weeks |

| Inventory impact | +15–30% |

| Zolgensma list price | $2.1M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Renovaro Biosciences, with data-backed, region- and industry-specific insights to identify risks, opportunities and strategic responses; designed for executives, investors and planners and formatted for immediate use.

Renovaro Biosciences PESTLE provides a clean, visually segmented summary of external risks and market drivers for quick reference in meetings or presentations, easily shareable and drop‑in ready for slide decks; its clear language and editable notes make it a practical pain‑point reliever for aligning teams and supporting strategy discussions.

Economic factors

Capital market conditions and cost of capital

Biotech funding cycles and elevated interest rates (US fed funds roughly 5.25–5.50% in 2024–2025) raise Renovaro’s cost of capital, shortening runway and compressing valuations. Risk-on markets ease follow-on financings, while tightening liquidity forces strict pipeline prioritization and milestone-focused de‑risking. Milestone-driven catalysts are vital to access capital efficiently and strategic partnerships can offset dilution during risk-off periods.

Manufacturing scale-up and COGS

Advanced therapy GMP manufacturing is capital-intensive (clinical-to-commercial suites often cost $50–200m in 2024) and highly yield-sensitive. Vector, cell processing and QC can drive per-dose COGS from $20k to $200k, directly squeezing gross margins and pricing flexibility. Early process optimization commonly cuts per-dose costs 30–60% and lowers supply risk. Outsourcing reduces near-term capex but typically raises per-dose costs 20–40% versus in-house control.

Payer willingness-to-pay and HTA outcomes

Oncology and HIV programs are rewarded for meaningful survival or functional cure endpoints; HTAs enforce cost-effectiveness thresholds (NICE £20–30k/QALY; US commonly $100–150k/QALY). Payers have supported premium prices for strong real-world evidence (RWE) with observed uplifts of ~10–25%; weak comparative effectiveness often collapses reimbursement and adoption, as seen with slower uptake of therapies priced like CAR-Ts ($373–475k) or gene therapies ($2.1M).

M&A and partnership landscape

Large pharmas favor de‑risked cell, gene and immunotherapy assets, setting deal comps; 2024 recorded over 200 relevant licensing/M&A transactions globally, shaping valuation benchmarks. Option‑to‑buy and co‑development structures increasingly fund late‑stage trials with multi‑million upfronts and milestone pools, while rising competitive interest boosts bargaining power and tougher milestone terms; consolidation may amplify or ease pressure.

- Deal volume: >200 cell/gene/immuno deals (2024)

- Structures: option‑to‑buy & co‑dev fund late‑stage trials

- Terms: stronger partner bargaining, higher milestone demands

- Consolidation: can intensify or relieve competition

Labor and input inflation

Talent competition for GMP, computational biology and clinical ops is pushing compensation higher—biochemists/biophysicists median pay was about $102,690 in May 2023 (BLS)—while reagent and vector component inflation has increased trial costs and COGS; global biotech VC funding fell roughly 30% in 2023, tightening sponsor capital. Long-term vendor contracts can cap input price volatility, but economic downturns may lower labor cost pressure even as financing becomes constrained.

- Wage pressure: BLS median pay ~$102,690 (May 2023)

- Input inflation: higher reagent/vector costs raising COGS

- Mitigation: long-term vendor contracts stabilize pricing

- Macro: downturn eases wages but limits financing (VC down ~30% in 2023)

Expedited regs: FDA 6m; public funding $49B

Higher rates (Fed funds ~5.25–5.50% in 2024–25) raise Renovaro’s cost of capital, shortening runway and pressuring valuations. GMP buildouts ($50–200M) and per‑dose COGS ($20k–$200k) compress margins; outsourcing trades capex for 20–40% higher unit costs. VC funding down ~30% (2023) and >200 cell/gene deals (2024) shape partnering and milestone-driven financing.

| Metric | Value |

|---|---|

| Fed funds (2024–25) | 5.25–5.50% |

| GMP capex | $50–200M |

| Per‑dose COGS | $20k–$200k |

| VC funding change (2023) | −30% |

| Deals (2024) | >200 |

Preview the Actual Deliverable

Renovaro Biosciences PESTLE Analysis

The Renovaro Biosciences PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—this is the finished file you’ll download immediately after buying.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock how political shifts, market forces, and tech advances are shaping Renovaro Biosciences’ prospects with our concise PESTLE snapshot—then dive deeper with the full analysis to inform investments, strategy, and risk planning. Download the complete report now for actionable insights.

Political factors

Regulatory prioritization and agency stance

Shifts in FDA, EMA and global regulators’ priorities for cell, gene and immunotherapies can accelerate or delay Renovaro’s programs; FDA Priority Review shortens review to 6 months vs 10 months standard. RMAT (est 2017), Breakthrough, Fast Track and EMA PRIME (est 2016) materially affect timelines and capital needs. Alignment with oncology/HIV/infectious‑disease goals often unlocks expedited pathways.

Public health funding and grants

NIH funding (~$49B FY2024), BARDA appropriations (~$1.7B) and international agency budgets (WHO base ~ $1.5B 2024–25) materially drive non-dilutive grants for HIV and infectious disease platforms.

Election and budget cycles can rapidly expand or contract grant pools, so aligning programs to national priorities raises award and partnership odds.

Sustained cuts would force Renovaro toward greater equity raises or strategic licensing and consortium partnerships to fund development.

Drug pricing and reimbursement policy

Government scrutiny of advanced therapy pricing—highlighted by the US Inflation Reduction Act price negotiation beginning 2026—shapes Renovaro Biosciences market access and revenue. Reference pricing and HTA thresholds such as UK NICE’s £20,000–£30,000/QALY range can compress margins versus list prices for gene therapies like Zolgensma at $2.1m and Luxturna at $850k. Political pressure favors value-based contracts and outcomes-linked rebates, making early pharmacoeconomic evidence critical for policy acceptance.

Geopolitical supply chain stability

Export controls, sanctions and trade tensions have restricted access to vector components and specialized reagents, driving shipment delays of roughly 2–12 weeks and pushing inventory carrying costs up an estimated 15–30% for biotechs. Political instability in supplier regions increases lead-time variability and contingency spend; diversifying suppliers and sourcing geographies reduces disruption risk and single‑country concentration. Cross-border clinical trials frequently face visa backlogs, customs holds and data transfer constraints that can delay enrollment and add regulatory compliance costs.

- Export controls: restricted inputs, 2–12 week delays

- Inventory impact: +15–30% carrying costs

- Mitigation: supplier/geography diversification

- Trials: visa, customs, data transfer constraints

Pandemic preparedness and biodefense agendas

Governments prioritizing infectious-disease resilience has accelerated regulatory reviews and collaborations, as seen after Operation Warp Speed mobilized about 18 billion USD in 2020; WHO estimates a roughly 10.5 billion USD annual gap for global preparedness. Reduced policy focus would slow partnering momentum, while platform-agile policies favor modular immunotherapy and public-private consortia de-risk development.

- Policy push: accelerates reviews & partnerships

- Risk: funding shift = lower partnering momentum

- Tech fit: modular platforms favored

- De-risk: consortia reduce clinical & commercial risk

Expedited regs: FDA 6m; public funding $49B

Regulatory expedited pathways (RMAT/Breakthrough/Fast Track/EMA PRIME) materially shorten timelines and capital needs; FDA Priority Review cuts review to 6 months. Public funding shapes non-dilutive support: NIH ~$49B FY2024, BARDA ~$1.7B; policy shifts alter grant pools. Pricing/payer rules (US IRA negotiations 2026, NICE £20–30k/QALY) and export controls (2–12 week delays; +15–30% inventory) affect market access and costs.

| Metric | Value |

|---|---|

| NIH FY2024 | $49B |

| BARDA | $1.7B |

| Operation Warp Speed | $18B |

| WHO preparedness gap | $10.5B/yr |

| Export delays | 2–12 weeks |

| Inventory impact | +15–30% |

| Zolgensma list price | $2.1M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Renovaro Biosciences, with data-backed, region- and industry-specific insights to identify risks, opportunities and strategic responses; designed for executives, investors and planners and formatted for immediate use.

Renovaro Biosciences PESTLE provides a clean, visually segmented summary of external risks and market drivers for quick reference in meetings or presentations, easily shareable and drop‑in ready for slide decks; its clear language and editable notes make it a practical pain‑point reliever for aligning teams and supporting strategy discussions.

Economic factors

Capital market conditions and cost of capital

Biotech funding cycles and elevated interest rates (US fed funds roughly 5.25–5.50% in 2024–2025) raise Renovaro’s cost of capital, shortening runway and compressing valuations. Risk-on markets ease follow-on financings, while tightening liquidity forces strict pipeline prioritization and milestone-focused de‑risking. Milestone-driven catalysts are vital to access capital efficiently and strategic partnerships can offset dilution during risk-off periods.

Manufacturing scale-up and COGS

Advanced therapy GMP manufacturing is capital-intensive (clinical-to-commercial suites often cost $50–200m in 2024) and highly yield-sensitive. Vector, cell processing and QC can drive per-dose COGS from $20k to $200k, directly squeezing gross margins and pricing flexibility. Early process optimization commonly cuts per-dose costs 30–60% and lowers supply risk. Outsourcing reduces near-term capex but typically raises per-dose costs 20–40% versus in-house control.

Payer willingness-to-pay and HTA outcomes

Oncology and HIV programs are rewarded for meaningful survival or functional cure endpoints; HTAs enforce cost-effectiveness thresholds (NICE £20–30k/QALY; US commonly $100–150k/QALY). Payers have supported premium prices for strong real-world evidence (RWE) with observed uplifts of ~10–25%; weak comparative effectiveness often collapses reimbursement and adoption, as seen with slower uptake of therapies priced like CAR-Ts ($373–475k) or gene therapies ($2.1M).

M&A and partnership landscape

Large pharmas favor de‑risked cell, gene and immunotherapy assets, setting deal comps; 2024 recorded over 200 relevant licensing/M&A transactions globally, shaping valuation benchmarks. Option‑to‑buy and co‑development structures increasingly fund late‑stage trials with multi‑million upfronts and milestone pools, while rising competitive interest boosts bargaining power and tougher milestone terms; consolidation may amplify or ease pressure.

- Deal volume: >200 cell/gene/immuno deals (2024)

- Structures: option‑to‑buy & co‑dev fund late‑stage trials

- Terms: stronger partner bargaining, higher milestone demands

- Consolidation: can intensify or relieve competition

Labor and input inflation

Talent competition for GMP, computational biology and clinical ops is pushing compensation higher—biochemists/biophysicists median pay was about $102,690 in May 2023 (BLS)—while reagent and vector component inflation has increased trial costs and COGS; global biotech VC funding fell roughly 30% in 2023, tightening sponsor capital. Long-term vendor contracts can cap input price volatility, but economic downturns may lower labor cost pressure even as financing becomes constrained.

- Wage pressure: BLS median pay ~$102,690 (May 2023)

- Input inflation: higher reagent/vector costs raising COGS

- Mitigation: long-term vendor contracts stabilize pricing

- Macro: downturn eases wages but limits financing (VC down ~30% in 2023)

Expedited regs: FDA 6m; public funding $49B

Higher rates (Fed funds ~5.25–5.50% in 2024–25) raise Renovaro’s cost of capital, shortening runway and pressuring valuations. GMP buildouts ($50–200M) and per‑dose COGS ($20k–$200k) compress margins; outsourcing trades capex for 20–40% higher unit costs. VC funding down ~30% (2023) and >200 cell/gene deals (2024) shape partnering and milestone-driven financing.

| Metric | Value |

|---|---|

| Fed funds (2024–25) | 5.25–5.50% |

| GMP capex | $50–200M |

| Per‑dose COGS | $20k–$200k |

| VC funding change (2023) | −30% |

| Deals (2024) | >200 |

Preview the Actual Deliverable

Renovaro Biosciences PESTLE Analysis

The Renovaro Biosciences PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—this is the finished file you’ll download immediately after buying.