Rent-A-Center Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

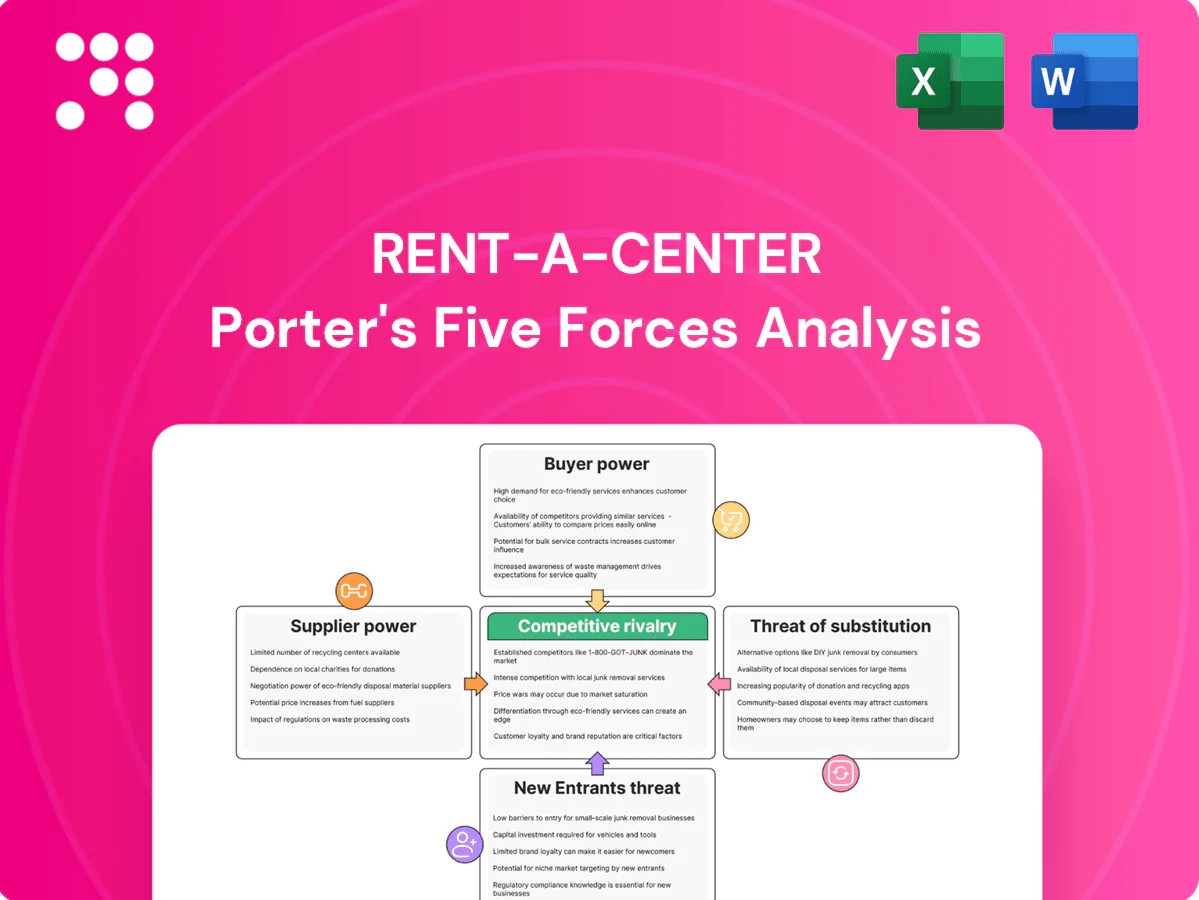

Rent-A-Center faces intense rivalry, shifting buyer preferences, and rising substitution risks from installment fintech and retailers—this snapshot highlights key pressures but only scratches the surface. The full Porter's Five Forces Analysis unpacks supplier leverage, entry barriers, and strategic responses with force-by-force ratings and visuals. Unlock the complete report to convert these insights into actionable strategy and investment decisions.

Suppliers Bargaining Power

Brand concentration in core categories

As of 2024 major appliances and electronics are concentrated in a few brands such as Samsung, LG and Whirlpool, giving them leverage over price, terms and model allocation. Popular SKUs are often steered to higher-margin channels, pressuring lease-to-own margins. Multiple comparable brands enable Rent-A-Center to diversify sourcing and negotiate. Private-label and refurbished inventory further temper supplier power.

Scale purchasing moderates pricing

Rent-A-Center’s national scale — roughly 2,300 stores and $1.6 billion revenue in 2024 — enables volume commitments, co-op marketing and centralized logistics that compress supplier margins and lower per-unit costs; consolidated procurement and standardized assortments strengthen negotiating leverage while smaller regional rivals typically face 5–15% higher supplier pricing, and suppliers prize RAC’s predictable offtake and repeat orders.

Low switching costs across vendors

Switching among furniture and mid-tier electronics suppliers is straightforward, reducing supplier bargaining power for Rent-A-Center; FY2023 revenue was $2.74 billion, underscoring scale to negotiate volume deals. Specification parity in mid-tier sofas, washers and TVs makes substitution easy without hurting customer acceptance. Exceptions persist for flagship devices with unique features. RAC can tier assortments to avoid single-vendor dependence.

Refurbished and secondary sourcing

RAC leverages refurbishing and off-price/discontinued sourcing to widen supply options, reducing dependence on OEMs and helping sustain margins; the global refurbished electronics market reached about $52.7 billion in 2024, supporting scale economics. Secondary channels also mitigate shortages during disruptions but require strict quality control and warranty management to preserve customer satisfaction and reduce returns.

- Supply diversification: refurb/off-price

- Margin resilience: lower COGS via secondary sourcing

- Disruption buffer: bridges OEM shortfalls

- Risk controls: quality checks, warranties

Logistics and availability volatility

Supplier power rises when freight costs spike or supply chains tighten, forcing Rent-A-Center to accept higher shipping premiums or extended terms during component shortages; lead-time variability can compel concessions to preserve in-stock rates. Diversified supplier bases and forward buys reduce exposure, while a regional DC network buffers local outages; RAC operates roughly 1,600 company-owned stores in North America (2024).

- Freight spikes increase supplier leverage

- Lead-time variability → weaker purchasing terms

- Forward buys and supplier diversification mitigate risk

- Regional DCs buffer local outages

Moderate supplier power: scale, centralized procurement and refurb sourcing limit supplier leverage

Supplier power is moderate: major appliance/electronics brands (Samsung, LG, Whirlpool) exert leverage on models and terms, but RAC’s scale (roughly 1,600–2,300 stores; revenue cited $1.6B–$2.74B in 2024) and centralized procurement compress supplier margins. Diversification via private-label, refurbished (global market $52.7B in 2024) and off-price sourcing limits dependence; freight spikes and lead-time volatility remain key risks.

| Metric | 2024 |

|---|---|

| Stores | 1,600–2,300 |

| Revenue | $1.6B–$2.74B |

| Refurb market | $52.7B |

| Supplier concentration | High for appliances/electronics |

| Procurement levers | Centralized buying, private-label, refurb |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for Rent-A-Center, uncovering competitive rivalry, buyer and supplier power, entry barriers, and substitute threats to assess pricing pressure and profitability; identifies disruptive forces and strategic levers to defend market share and inform investor or management decisions.

Clear, one-sheet Porter’s Five Forces for Rent-A-Center — instantly identify competitive pressure and relief points with a customizable spider chart and pressure sliders, ready to copy into decks or plug into broader dashboards with no macros.

Customers Bargaining Power

Price-sensitive, credit-constrained customers

Price-sensitive, credit-constrained customers prioritize low upfront costs and weekly affordability, making them highly sensitive to payment amounts and fees; in 2024 roughly 24% of U.S. adults were estimated as unbanked or underbanked, limiting traditional credit access and increasing scrutiny of total cost to own. Small price differences can shift store choice, so clear value communication is essential to limit churn.

Moderate switching costs

Customers can switch to competitors or BNPL options with relative ease before ownership is achieved; about 25% of US shoppers used BNPL in 2024, increasing alternatives to Rent-A-Center. Proximity, delivery speed and service quality add friction but are not insurmountable, while early-payoff discounts and return policies materially affect loyalty. Strong in-store relationships and service interactions reduce propensity to switch.

Transparency and online comparability

Online listings, reviews, and weekly-rate calculators make cross-provider comparison trivial, with surveys in 2024 showing roughly 79% of shoppers consult reviews before purchase. This transparency raises buyer leverage on promotions and contract terms. RAC’s omnichannel reach and instant decisioning help defend share by shortening conversion paths. Clear, prominent disclosures increase trust among skeptical renters and reduce churn.

Service and maintenance expectations

Customers depend heavily on delivery, setup, and servicing, so service quality is a key negotiation lever; as of 2024, rapid warranty handling and replacements are widely cited as decisive factors in rent-to-own choices.

- Service quality increases willingness to pay

- Weak service boosts cancellation/return threats

- Fast replacements reduce churn

- Warranty handling is a competitive differentiator

Default risk influences terms

Higher delinquency risk in Rent-A-Center’s customer base forces tighter approval criteria and pricing to protect unit economics; with U.S. unemployment near 4.0% (June 2024) and many customers below prime credit tiers, flex-pay features lower acquisition friction but raise collections exposure. Customers use hardship flexibility to renegotiate schedules, meaning policies must trade off lifetime revenue versus short-term recoveries. Data-driven underwriting and behavioral scoring let RCII tailor offers while preserving margins.

Price-sensitive renters, BNPL and reviews force low upfronts, flexible terms, and service focus

Price-sensitive, credit-constrained renters (≈24% unbanked/underbanked in 2024) push Rent-A-Center to prioritize low upfronts and clear total-costs. Easy switching and BNPL adoption (~25% of US shoppers in 2024) raise customer leverage, while review-driven transparency (≈79% consult reviews) amplifies pricing pressure. Service, delivery and flexible terms (with ~4.0% unemployment June 2024) are key retention levers.

| Metric | 2024 |

|---|---|

| Unbanked/Underbanked | 24% |

| BNPL users | 25% |

| Shoppers using reviews | 79% |

| Unemployment (Jun) | 4.0% |

Same Document Delivered

Rent-A-Center Porter's Five Forces Analysis

This preview shows the exact Rent‑A‑Center Porter’s Five Forces analysis you’ll receive—no placeholders or samples. It is the complete, professionally formatted document, ready for download and immediate use upon purchase. What you see here is precisely what will be delivered instantly after payment.

A Must-Have Tool for Decision-Makers

Rent-A-Center faces intense rivalry, shifting buyer preferences, and rising substitution risks from installment fintech and retailers—this snapshot highlights key pressures but only scratches the surface. The full Porter's Five Forces Analysis unpacks supplier leverage, entry barriers, and strategic responses with force-by-force ratings and visuals. Unlock the complete report to convert these insights into actionable strategy and investment decisions.

Suppliers Bargaining Power

Brand concentration in core categories

As of 2024 major appliances and electronics are concentrated in a few brands such as Samsung, LG and Whirlpool, giving them leverage over price, terms and model allocation. Popular SKUs are often steered to higher-margin channels, pressuring lease-to-own margins. Multiple comparable brands enable Rent-A-Center to diversify sourcing and negotiate. Private-label and refurbished inventory further temper supplier power.

Scale purchasing moderates pricing

Rent-A-Center’s national scale — roughly 2,300 stores and $1.6 billion revenue in 2024 — enables volume commitments, co-op marketing and centralized logistics that compress supplier margins and lower per-unit costs; consolidated procurement and standardized assortments strengthen negotiating leverage while smaller regional rivals typically face 5–15% higher supplier pricing, and suppliers prize RAC’s predictable offtake and repeat orders.

Low switching costs across vendors

Switching among furniture and mid-tier electronics suppliers is straightforward, reducing supplier bargaining power for Rent-A-Center; FY2023 revenue was $2.74 billion, underscoring scale to negotiate volume deals. Specification parity in mid-tier sofas, washers and TVs makes substitution easy without hurting customer acceptance. Exceptions persist for flagship devices with unique features. RAC can tier assortments to avoid single-vendor dependence.

Refurbished and secondary sourcing

RAC leverages refurbishing and off-price/discontinued sourcing to widen supply options, reducing dependence on OEMs and helping sustain margins; the global refurbished electronics market reached about $52.7 billion in 2024, supporting scale economics. Secondary channels also mitigate shortages during disruptions but require strict quality control and warranty management to preserve customer satisfaction and reduce returns.

- Supply diversification: refurb/off-price

- Margin resilience: lower COGS via secondary sourcing

- Disruption buffer: bridges OEM shortfalls

- Risk controls: quality checks, warranties

Logistics and availability volatility

Supplier power rises when freight costs spike or supply chains tighten, forcing Rent-A-Center to accept higher shipping premiums or extended terms during component shortages; lead-time variability can compel concessions to preserve in-stock rates. Diversified supplier bases and forward buys reduce exposure, while a regional DC network buffers local outages; RAC operates roughly 1,600 company-owned stores in North America (2024).

- Freight spikes increase supplier leverage

- Lead-time variability → weaker purchasing terms

- Forward buys and supplier diversification mitigate risk

- Regional DCs buffer local outages

Moderate supplier power: scale, centralized procurement and refurb sourcing limit supplier leverage

Supplier power is moderate: major appliance/electronics brands (Samsung, LG, Whirlpool) exert leverage on models and terms, but RAC’s scale (roughly 1,600–2,300 stores; revenue cited $1.6B–$2.74B in 2024) and centralized procurement compress supplier margins. Diversification via private-label, refurbished (global market $52.7B in 2024) and off-price sourcing limits dependence; freight spikes and lead-time volatility remain key risks.

| Metric | 2024 |

|---|---|

| Stores | 1,600–2,300 |

| Revenue | $1.6B–$2.74B |

| Refurb market | $52.7B |

| Supplier concentration | High for appliances/electronics |

| Procurement levers | Centralized buying, private-label, refurb |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for Rent-A-Center, uncovering competitive rivalry, buyer and supplier power, entry barriers, and substitute threats to assess pricing pressure and profitability; identifies disruptive forces and strategic levers to defend market share and inform investor or management decisions.

Clear, one-sheet Porter’s Five Forces for Rent-A-Center — instantly identify competitive pressure and relief points with a customizable spider chart and pressure sliders, ready to copy into decks or plug into broader dashboards with no macros.

Customers Bargaining Power

Price-sensitive, credit-constrained customers

Price-sensitive, credit-constrained customers prioritize low upfront costs and weekly affordability, making them highly sensitive to payment amounts and fees; in 2024 roughly 24% of U.S. adults were estimated as unbanked or underbanked, limiting traditional credit access and increasing scrutiny of total cost to own. Small price differences can shift store choice, so clear value communication is essential to limit churn.

Moderate switching costs

Customers can switch to competitors or BNPL options with relative ease before ownership is achieved; about 25% of US shoppers used BNPL in 2024, increasing alternatives to Rent-A-Center. Proximity, delivery speed and service quality add friction but are not insurmountable, while early-payoff discounts and return policies materially affect loyalty. Strong in-store relationships and service interactions reduce propensity to switch.

Transparency and online comparability

Online listings, reviews, and weekly-rate calculators make cross-provider comparison trivial, with surveys in 2024 showing roughly 79% of shoppers consult reviews before purchase. This transparency raises buyer leverage on promotions and contract terms. RAC’s omnichannel reach and instant decisioning help defend share by shortening conversion paths. Clear, prominent disclosures increase trust among skeptical renters and reduce churn.

Service and maintenance expectations

Customers depend heavily on delivery, setup, and servicing, so service quality is a key negotiation lever; as of 2024, rapid warranty handling and replacements are widely cited as decisive factors in rent-to-own choices.

- Service quality increases willingness to pay

- Weak service boosts cancellation/return threats

- Fast replacements reduce churn

- Warranty handling is a competitive differentiator

Default risk influences terms

Higher delinquency risk in Rent-A-Center’s customer base forces tighter approval criteria and pricing to protect unit economics; with U.S. unemployment near 4.0% (June 2024) and many customers below prime credit tiers, flex-pay features lower acquisition friction but raise collections exposure. Customers use hardship flexibility to renegotiate schedules, meaning policies must trade off lifetime revenue versus short-term recoveries. Data-driven underwriting and behavioral scoring let RCII tailor offers while preserving margins.

Price-sensitive renters, BNPL and reviews force low upfronts, flexible terms, and service focus

Price-sensitive, credit-constrained renters (≈24% unbanked/underbanked in 2024) push Rent-A-Center to prioritize low upfronts and clear total-costs. Easy switching and BNPL adoption (~25% of US shoppers in 2024) raise customer leverage, while review-driven transparency (≈79% consult reviews) amplifies pricing pressure. Service, delivery and flexible terms (with ~4.0% unemployment June 2024) are key retention levers.

| Metric | 2024 |

|---|---|

| Unbanked/Underbanked | 24% |

| BNPL users | 25% |

| Shoppers using reviews | 79% |

| Unemployment (Jun) | 4.0% |

Same Document Delivered

Rent-A-Center Porter's Five Forces Analysis

This preview shows the exact Rent‑A‑Center Porter’s Five Forces analysis you’ll receive—no placeholders or samples. It is the complete, professionally formatted document, ready for download and immediate use upon purchase. What you see here is precisely what will be delivered instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Rent-A-Center faces intense rivalry, shifting buyer preferences, and rising substitution risks from installment fintech and retailers—this snapshot highlights key pressures but only scratches the surface. The full Porter's Five Forces Analysis unpacks supplier leverage, entry barriers, and strategic responses with force-by-force ratings and visuals. Unlock the complete report to convert these insights into actionable strategy and investment decisions.

Suppliers Bargaining Power

Brand concentration in core categories

As of 2024 major appliances and electronics are concentrated in a few brands such as Samsung, LG and Whirlpool, giving them leverage over price, terms and model allocation. Popular SKUs are often steered to higher-margin channels, pressuring lease-to-own margins. Multiple comparable brands enable Rent-A-Center to diversify sourcing and negotiate. Private-label and refurbished inventory further temper supplier power.

Scale purchasing moderates pricing

Rent-A-Center’s national scale — roughly 2,300 stores and $1.6 billion revenue in 2024 — enables volume commitments, co-op marketing and centralized logistics that compress supplier margins and lower per-unit costs; consolidated procurement and standardized assortments strengthen negotiating leverage while smaller regional rivals typically face 5–15% higher supplier pricing, and suppliers prize RAC’s predictable offtake and repeat orders.

Low switching costs across vendors

Switching among furniture and mid-tier electronics suppliers is straightforward, reducing supplier bargaining power for Rent-A-Center; FY2023 revenue was $2.74 billion, underscoring scale to negotiate volume deals. Specification parity in mid-tier sofas, washers and TVs makes substitution easy without hurting customer acceptance. Exceptions persist for flagship devices with unique features. RAC can tier assortments to avoid single-vendor dependence.

Refurbished and secondary sourcing

RAC leverages refurbishing and off-price/discontinued sourcing to widen supply options, reducing dependence on OEMs and helping sustain margins; the global refurbished electronics market reached about $52.7 billion in 2024, supporting scale economics. Secondary channels also mitigate shortages during disruptions but require strict quality control and warranty management to preserve customer satisfaction and reduce returns.

- Supply diversification: refurb/off-price

- Margin resilience: lower COGS via secondary sourcing

- Disruption buffer: bridges OEM shortfalls

- Risk controls: quality checks, warranties

Logistics and availability volatility

Supplier power rises when freight costs spike or supply chains tighten, forcing Rent-A-Center to accept higher shipping premiums or extended terms during component shortages; lead-time variability can compel concessions to preserve in-stock rates. Diversified supplier bases and forward buys reduce exposure, while a regional DC network buffers local outages; RAC operates roughly 1,600 company-owned stores in North America (2024).

- Freight spikes increase supplier leverage

- Lead-time variability → weaker purchasing terms

- Forward buys and supplier diversification mitigate risk

- Regional DCs buffer local outages

Moderate supplier power: scale, centralized procurement and refurb sourcing limit supplier leverage

Supplier power is moderate: major appliance/electronics brands (Samsung, LG, Whirlpool) exert leverage on models and terms, but RAC’s scale (roughly 1,600–2,300 stores; revenue cited $1.6B–$2.74B in 2024) and centralized procurement compress supplier margins. Diversification via private-label, refurbished (global market $52.7B in 2024) and off-price sourcing limits dependence; freight spikes and lead-time volatility remain key risks.

| Metric | 2024 |

|---|---|

| Stores | 1,600–2,300 |

| Revenue | $1.6B–$2.74B |

| Refurb market | $52.7B |

| Supplier concentration | High for appliances/electronics |

| Procurement levers | Centralized buying, private-label, refurb |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for Rent-A-Center, uncovering competitive rivalry, buyer and supplier power, entry barriers, and substitute threats to assess pricing pressure and profitability; identifies disruptive forces and strategic levers to defend market share and inform investor or management decisions.

Clear, one-sheet Porter’s Five Forces for Rent-A-Center — instantly identify competitive pressure and relief points with a customizable spider chart and pressure sliders, ready to copy into decks or plug into broader dashboards with no macros.

Customers Bargaining Power

Price-sensitive, credit-constrained customers

Price-sensitive, credit-constrained customers prioritize low upfront costs and weekly affordability, making them highly sensitive to payment amounts and fees; in 2024 roughly 24% of U.S. adults were estimated as unbanked or underbanked, limiting traditional credit access and increasing scrutiny of total cost to own. Small price differences can shift store choice, so clear value communication is essential to limit churn.

Moderate switching costs

Customers can switch to competitors or BNPL options with relative ease before ownership is achieved; about 25% of US shoppers used BNPL in 2024, increasing alternatives to Rent-A-Center. Proximity, delivery speed and service quality add friction but are not insurmountable, while early-payoff discounts and return policies materially affect loyalty. Strong in-store relationships and service interactions reduce propensity to switch.

Transparency and online comparability

Online listings, reviews, and weekly-rate calculators make cross-provider comparison trivial, with surveys in 2024 showing roughly 79% of shoppers consult reviews before purchase. This transparency raises buyer leverage on promotions and contract terms. RAC’s omnichannel reach and instant decisioning help defend share by shortening conversion paths. Clear, prominent disclosures increase trust among skeptical renters and reduce churn.

Service and maintenance expectations

Customers depend heavily on delivery, setup, and servicing, so service quality is a key negotiation lever; as of 2024, rapid warranty handling and replacements are widely cited as decisive factors in rent-to-own choices.

- Service quality increases willingness to pay

- Weak service boosts cancellation/return threats

- Fast replacements reduce churn

- Warranty handling is a competitive differentiator

Default risk influences terms

Higher delinquency risk in Rent-A-Center’s customer base forces tighter approval criteria and pricing to protect unit economics; with U.S. unemployment near 4.0% (June 2024) and many customers below prime credit tiers, flex-pay features lower acquisition friction but raise collections exposure. Customers use hardship flexibility to renegotiate schedules, meaning policies must trade off lifetime revenue versus short-term recoveries. Data-driven underwriting and behavioral scoring let RCII tailor offers while preserving margins.

Price-sensitive renters, BNPL and reviews force low upfronts, flexible terms, and service focus

Price-sensitive, credit-constrained renters (≈24% unbanked/underbanked in 2024) push Rent-A-Center to prioritize low upfronts and clear total-costs. Easy switching and BNPL adoption (~25% of US shoppers in 2024) raise customer leverage, while review-driven transparency (≈79% consult reviews) amplifies pricing pressure. Service, delivery and flexible terms (with ~4.0% unemployment June 2024) are key retention levers.

| Metric | 2024 |

|---|---|

| Unbanked/Underbanked | 24% |

| BNPL users | 25% |

| Shoppers using reviews | 79% |

| Unemployment (Jun) | 4.0% |

Same Document Delivered

Rent-A-Center Porter's Five Forces Analysis

This preview shows the exact Rent‑A‑Center Porter’s Five Forces analysis you’ll receive—no placeholders or samples. It is the complete, professionally formatted document, ready for download and immediate use upon purchase. What you see here is precisely what will be delivered instantly after payment.