Repco Home Finance Business Model Canvas

Unlock the strategic playbook: 9-block Business Model Canvas for mortgage lenders

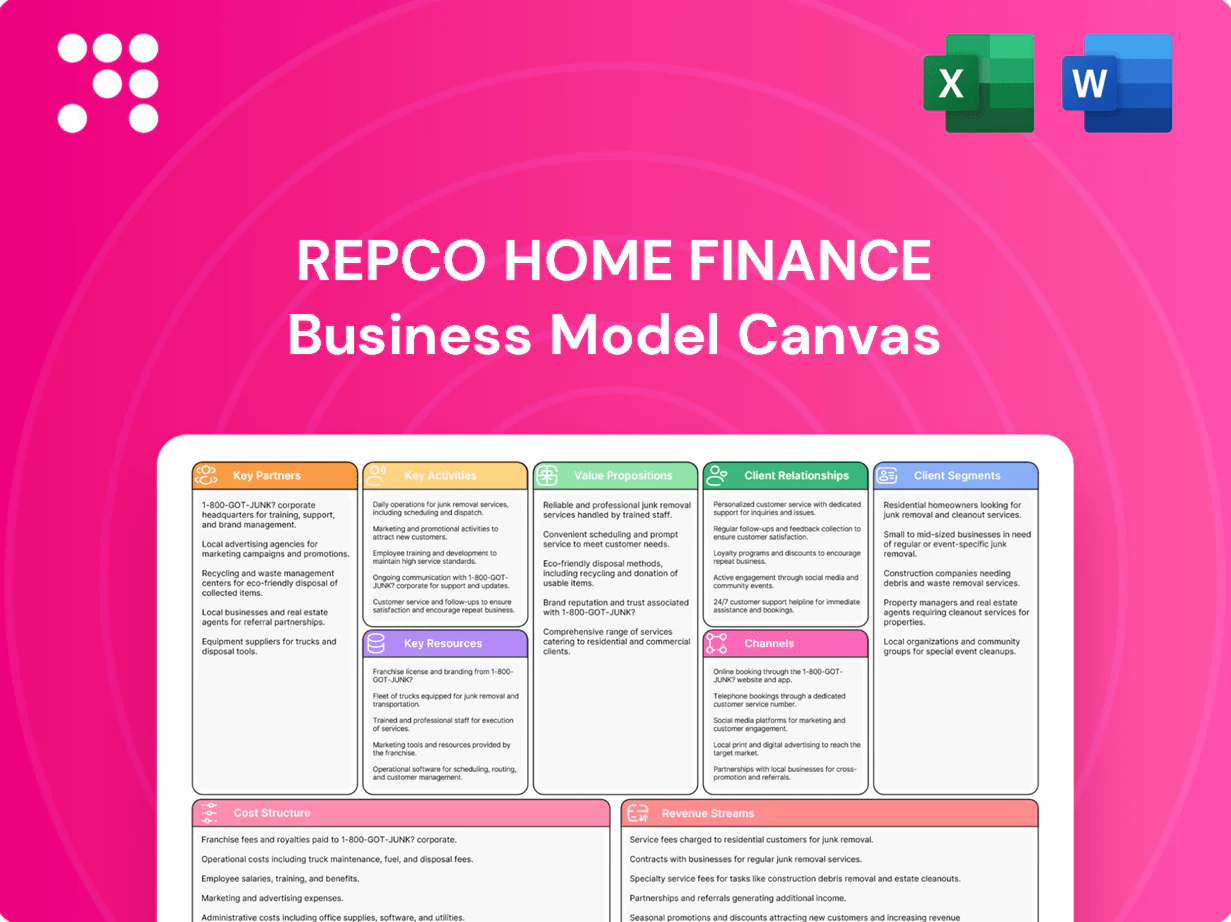

Unlock Repco Home Finance’s strategic playbook with our concise Business Model Canvas — a 9-block breakdown showing customer segments, value propositions, channels, and revenue levers. Ideal for investors, advisors, and founders seeking actionable insights. Download the full Word/Excel canvas to benchmark, adapt, and execute faster.

Partnerships

Repco Bank and other lenders

Repco Bank, as promoter, supplies core funding lines, brand credibility and governance oversight, backing Repco Home Finance’s balance sheet while enabling access to term loans and cash credit; Repco Home Finance reported AUM around ₹7,000 crore in 2024. Supplementary ties with public/private banks and NBFCs diversify liabilities and helped lower blended cost of funds by several hundred basis points versus standalone unsecured rates in 2024. Robust lender relationships also facilitate securitization conduits and stabilize liquidity across cycles, supporting funding continuity during stress periods.

NHB and regulatory bodies

Engagement with National Housing Bank, established in 1988, ensures access to refinance and alignment with statutory housing finance norms. Compliance partnerships with regulatory bodies secure priority sector classification and participation in affordable housing schemes. Regular supervision enforces prudent risk practices and enhances investor and customer confidence.

Builders, developers, and property brokers

Tie-ups with builders, developers and brokers supply high-quality sourced leads for purchase and construction loans, leveraging Repco Home Finance’s distribution to support its Rs 27,732 crore AUM as of March 31, 2024; preferred partner projects standardize property due diligence and documentation. Joint marketing expands reach in target micro-markets, shortening turnaround times and improving conversion rates materially (industry reports cite up to 30% faster disbursals for tied channels).

Fintechs and technology vendors

Fintechs and tech vendors supply LOS/LMS, e-KYC, credit analytics and payment rails, with API-driven integrations streamlining underwriting and collections to cut turnaround and operational overhead.

Digital partners enable Repco Home Finance to scale beyond core geographies while lowering cost per file and reducing fraud exposure through real-time scoring and automated verification.

- LOS/LMS: operational workflow automation

- e-KYC: faster ID verification, lower fraud

- Credit analytics: improved risk-based pricing

- Payments/APIs: efficient collections and scalability

Credit bureaus and verification agencies

Partnerships with credit bureaus enable more accurate credit scoring for informal-income customers by incorporating alternative data and bureau overlays; TransUnion CIBIL reported about 540 million credit-active consumers in 2024, expanding reference data for Repco’s underwriting. Field verification vendors provide income-surrogate checks and property valuations, strengthening portfolio quality, lowering NPAs, and enabling granular risk-based pricing.

- Enhanced scoring for informal incomes

- Field verification: income surrogates & property checks

- Improves portfolio quality, reduces NPAs

- Enables risk-based pricing

Bank-backed home loans: AUM ₹27,732 cr, ≈540M

Repco Bank provides core funding, governance and brand support, underpinning Repco Home Finance’s balance sheet and scale (AUM ₹27,732 crore as of Mar 31, 2024). Lender and NBFC tie-ups diversify liabilities and stabilize liquidity while lowering blended funding costs in 2024. Fintechs, field vendors and TransUnion CIBIL (≈540 million credit-active consumers in 2024) enhance underwriting, verification and risk pricing.

| Partner | Role | 2024 metric |

|---|---|---|

| Repco Bank | Promoter funding & governance | AUM ₹27,732 cr (Mar 31, 2024) |

| Lenders/NBFCs | Liability diversification, securitization | Lowered blended funding cost (2024) |

| TransUnion CIBIL | Credit data provider | ≈540M credit-active consumers (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Repco Home Finance outlining customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, with linked competitive advantages and SWOT insights; ideal for presentations, investor discussions and strategic decision-making.

High-level view of Repco Home Finance’s business model that quickly pinpoints lending, distribution and risk-management pain points; editable and shareable to save hours structuring strategic plans and align teams for faster decision-making.

Activities

Retail housing loan origination

Sourcing and assessing applications for purchase, construction, repair and improvement focuses on middle and lower-income segments with localized underwriting tailored to informal incomes; field visits and income surrogate assessments verify cash flows and collateral.

Underwriting and risk management

Credit appraisal blends bank statement analytics, project cash-flow assessments and field verification to underwrite informal-income and self-employed borrowers, improving affordability scoring and repayment prediction. Collateral valuation, title and legal checks and strict LTV discipline protect recovery value and legal enforceability. Continuous portfolio monitoring with vintage tracking and early-warning triggers enables timely remediation. Risk-based pricing and conservative provisioning sustain asset quality.

Collections and customer servicing

Timely EMI collections are executed via digital payment rails and field recovery teams, aligning with RBI/HFC regulatory framework as of 2024. Soft- and hard-bucket segmentation (eg 30/90/180-day buckets) is used to prioritize interventions and control delinquencies. Customer grievance redressal and service requests follow statutory timelines and restructuring support is provided where permissible under 2024 RBI norms.

Liability management and securitization

Repco manages cost of funds through bank lines, NHB refinance and market borrowings, using securitization/assignment to recycle capital and support lending growth; ALM tracks tenors to control interest‑rate and liquidity risk amid a 2024 repo backdrop of ~6.5% and tight spreads. Hedging is used selectively to stabilize net interest margins while prioritizing low‑cost, long‑tenor funding.

- Bank/NHB/market mix

- Securitization for capital recycling; ALM + selective hedging

Branch network expansion and marketing

Repco Home Finance is deepening its South India footprint while selectively entering new states, leveraging a branch network of about 135 locations in 2024 to improve retail sourcing and loan disbursals. Localized campaigns and community outreach drive trust and NPA-sensitive borrower screening, complemented by partnerships with developers and a 1,200-strong DSA network for pipeline growth. Digital marketing and CRM tools augment feet-on-street sourcing, raising lead conversion and reducing customer acquisition cost.

Field-verified low-income lending with strict LTVs; repo 6.5%

Sourcing/appraisal focused on middle‑low incomes with field verification, bank‑stmt analytics and strict LTVs to protect recoveries. Collections via digital rails and field teams; vintage monitoring and RBI‑aligned restructuring processes (2024 norms). Funding mix: bank/NHB/market + securitization; ALM/hedging manage rate risk (repo ~6.5%). Distribution: ~135 branches, ~1,200 DSAs driving sourcing.

| Metric | 2024 |

|---|---|

| Branches | ~135 |

| DSAs | ~1,200 |

| Repo rate | ~6.5% |

Delivered as Displayed

Business Model Canvas

The Repco Home Finance Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the same structure and content you’ll receive after purchase. When you complete your order, you’ll get this exact document ready to edit and present in the provided formats. No surprises—what you see is what you’ll download.

Unlock the strategic playbook: 9-block Business Model Canvas for mortgage lenders

Unlock Repco Home Finance’s strategic playbook with our concise Business Model Canvas — a 9-block breakdown showing customer segments, value propositions, channels, and revenue levers. Ideal for investors, advisors, and founders seeking actionable insights. Download the full Word/Excel canvas to benchmark, adapt, and execute faster.

Partnerships

Repco Bank and other lenders

Repco Bank, as promoter, supplies core funding lines, brand credibility and governance oversight, backing Repco Home Finance’s balance sheet while enabling access to term loans and cash credit; Repco Home Finance reported AUM around ₹7,000 crore in 2024. Supplementary ties with public/private banks and NBFCs diversify liabilities and helped lower blended cost of funds by several hundred basis points versus standalone unsecured rates in 2024. Robust lender relationships also facilitate securitization conduits and stabilize liquidity across cycles, supporting funding continuity during stress periods.

NHB and regulatory bodies

Engagement with National Housing Bank, established in 1988, ensures access to refinance and alignment with statutory housing finance norms. Compliance partnerships with regulatory bodies secure priority sector classification and participation in affordable housing schemes. Regular supervision enforces prudent risk practices and enhances investor and customer confidence.

Builders, developers, and property brokers

Tie-ups with builders, developers and brokers supply high-quality sourced leads for purchase and construction loans, leveraging Repco Home Finance’s distribution to support its Rs 27,732 crore AUM as of March 31, 2024; preferred partner projects standardize property due diligence and documentation. Joint marketing expands reach in target micro-markets, shortening turnaround times and improving conversion rates materially (industry reports cite up to 30% faster disbursals for tied channels).

Fintechs and technology vendors

Fintechs and tech vendors supply LOS/LMS, e-KYC, credit analytics and payment rails, with API-driven integrations streamlining underwriting and collections to cut turnaround and operational overhead.

Digital partners enable Repco Home Finance to scale beyond core geographies while lowering cost per file and reducing fraud exposure through real-time scoring and automated verification.

- LOS/LMS: operational workflow automation

- e-KYC: faster ID verification, lower fraud

- Credit analytics: improved risk-based pricing

- Payments/APIs: efficient collections and scalability

Credit bureaus and verification agencies

Partnerships with credit bureaus enable more accurate credit scoring for informal-income customers by incorporating alternative data and bureau overlays; TransUnion CIBIL reported about 540 million credit-active consumers in 2024, expanding reference data for Repco’s underwriting. Field verification vendors provide income-surrogate checks and property valuations, strengthening portfolio quality, lowering NPAs, and enabling granular risk-based pricing.

- Enhanced scoring for informal incomes

- Field verification: income surrogates & property checks

- Improves portfolio quality, reduces NPAs

- Enables risk-based pricing

Bank-backed home loans: AUM ₹27,732 cr, ≈540M

Repco Bank provides core funding, governance and brand support, underpinning Repco Home Finance’s balance sheet and scale (AUM ₹27,732 crore as of Mar 31, 2024). Lender and NBFC tie-ups diversify liabilities and stabilize liquidity while lowering blended funding costs in 2024. Fintechs, field vendors and TransUnion CIBIL (≈540 million credit-active consumers in 2024) enhance underwriting, verification and risk pricing.

| Partner | Role | 2024 metric |

|---|---|---|

| Repco Bank | Promoter funding & governance | AUM ₹27,732 cr (Mar 31, 2024) |

| Lenders/NBFCs | Liability diversification, securitization | Lowered blended funding cost (2024) |

| TransUnion CIBIL | Credit data provider | ≈540M credit-active consumers (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Repco Home Finance outlining customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, with linked competitive advantages and SWOT insights; ideal for presentations, investor discussions and strategic decision-making.

High-level view of Repco Home Finance’s business model that quickly pinpoints lending, distribution and risk-management pain points; editable and shareable to save hours structuring strategic plans and align teams for faster decision-making.

Activities

Retail housing loan origination

Sourcing and assessing applications for purchase, construction, repair and improvement focuses on middle and lower-income segments with localized underwriting tailored to informal incomes; field visits and income surrogate assessments verify cash flows and collateral.

Underwriting and risk management

Credit appraisal blends bank statement analytics, project cash-flow assessments and field verification to underwrite informal-income and self-employed borrowers, improving affordability scoring and repayment prediction. Collateral valuation, title and legal checks and strict LTV discipline protect recovery value and legal enforceability. Continuous portfolio monitoring with vintage tracking and early-warning triggers enables timely remediation. Risk-based pricing and conservative provisioning sustain asset quality.

Collections and customer servicing

Timely EMI collections are executed via digital payment rails and field recovery teams, aligning with RBI/HFC regulatory framework as of 2024. Soft- and hard-bucket segmentation (eg 30/90/180-day buckets) is used to prioritize interventions and control delinquencies. Customer grievance redressal and service requests follow statutory timelines and restructuring support is provided where permissible under 2024 RBI norms.

Liability management and securitization

Repco manages cost of funds through bank lines, NHB refinance and market borrowings, using securitization/assignment to recycle capital and support lending growth; ALM tracks tenors to control interest‑rate and liquidity risk amid a 2024 repo backdrop of ~6.5% and tight spreads. Hedging is used selectively to stabilize net interest margins while prioritizing low‑cost, long‑tenor funding.

- Bank/NHB/market mix

- Securitization for capital recycling; ALM + selective hedging

Branch network expansion and marketing

Repco Home Finance is deepening its South India footprint while selectively entering new states, leveraging a branch network of about 135 locations in 2024 to improve retail sourcing and loan disbursals. Localized campaigns and community outreach drive trust and NPA-sensitive borrower screening, complemented by partnerships with developers and a 1,200-strong DSA network for pipeline growth. Digital marketing and CRM tools augment feet-on-street sourcing, raising lead conversion and reducing customer acquisition cost.

Field-verified low-income lending with strict LTVs; repo 6.5%

Sourcing/appraisal focused on middle‑low incomes with field verification, bank‑stmt analytics and strict LTVs to protect recoveries. Collections via digital rails and field teams; vintage monitoring and RBI‑aligned restructuring processes (2024 norms). Funding mix: bank/NHB/market + securitization; ALM/hedging manage rate risk (repo ~6.5%). Distribution: ~135 branches, ~1,200 DSAs driving sourcing.

| Metric | 2024 |

|---|---|

| Branches | ~135 |

| DSAs | ~1,200 |

| Repo rate | ~6.5% |

Delivered as Displayed

Business Model Canvas

The Repco Home Finance Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the same structure and content you’ll receive after purchase. When you complete your order, you’ll get this exact document ready to edit and present in the provided formats. No surprises—what you see is what you’ll download.

Original: $10.00

-65%$10.00

$3.50Description

Unlock the strategic playbook: 9-block Business Model Canvas for mortgage lenders

Unlock Repco Home Finance’s strategic playbook with our concise Business Model Canvas — a 9-block breakdown showing customer segments, value propositions, channels, and revenue levers. Ideal for investors, advisors, and founders seeking actionable insights. Download the full Word/Excel canvas to benchmark, adapt, and execute faster.

Partnerships

Repco Bank and other lenders

Repco Bank, as promoter, supplies core funding lines, brand credibility and governance oversight, backing Repco Home Finance’s balance sheet while enabling access to term loans and cash credit; Repco Home Finance reported AUM around ₹7,000 crore in 2024. Supplementary ties with public/private banks and NBFCs diversify liabilities and helped lower blended cost of funds by several hundred basis points versus standalone unsecured rates in 2024. Robust lender relationships also facilitate securitization conduits and stabilize liquidity across cycles, supporting funding continuity during stress periods.

NHB and regulatory bodies

Engagement with National Housing Bank, established in 1988, ensures access to refinance and alignment with statutory housing finance norms. Compliance partnerships with regulatory bodies secure priority sector classification and participation in affordable housing schemes. Regular supervision enforces prudent risk practices and enhances investor and customer confidence.

Builders, developers, and property brokers

Tie-ups with builders, developers and brokers supply high-quality sourced leads for purchase and construction loans, leveraging Repco Home Finance’s distribution to support its Rs 27,732 crore AUM as of March 31, 2024; preferred partner projects standardize property due diligence and documentation. Joint marketing expands reach in target micro-markets, shortening turnaround times and improving conversion rates materially (industry reports cite up to 30% faster disbursals for tied channels).

Fintechs and technology vendors

Fintechs and tech vendors supply LOS/LMS, e-KYC, credit analytics and payment rails, with API-driven integrations streamlining underwriting and collections to cut turnaround and operational overhead.

Digital partners enable Repco Home Finance to scale beyond core geographies while lowering cost per file and reducing fraud exposure through real-time scoring and automated verification.

- LOS/LMS: operational workflow automation

- e-KYC: faster ID verification, lower fraud

- Credit analytics: improved risk-based pricing

- Payments/APIs: efficient collections and scalability

Credit bureaus and verification agencies

Partnerships with credit bureaus enable more accurate credit scoring for informal-income customers by incorporating alternative data and bureau overlays; TransUnion CIBIL reported about 540 million credit-active consumers in 2024, expanding reference data for Repco’s underwriting. Field verification vendors provide income-surrogate checks and property valuations, strengthening portfolio quality, lowering NPAs, and enabling granular risk-based pricing.

- Enhanced scoring for informal incomes

- Field verification: income surrogates & property checks

- Improves portfolio quality, reduces NPAs

- Enables risk-based pricing

Bank-backed home loans: AUM ₹27,732 cr, ≈540M

Repco Bank provides core funding, governance and brand support, underpinning Repco Home Finance’s balance sheet and scale (AUM ₹27,732 crore as of Mar 31, 2024). Lender and NBFC tie-ups diversify liabilities and stabilize liquidity while lowering blended funding costs in 2024. Fintechs, field vendors and TransUnion CIBIL (≈540 million credit-active consumers in 2024) enhance underwriting, verification and risk pricing.

| Partner | Role | 2024 metric |

|---|---|---|

| Repco Bank | Promoter funding & governance | AUM ₹27,732 cr (Mar 31, 2024) |

| Lenders/NBFCs | Liability diversification, securitization | Lowered blended funding cost (2024) |

| TransUnion CIBIL | Credit data provider | ≈540M credit-active consumers (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Repco Home Finance outlining customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, with linked competitive advantages and SWOT insights; ideal for presentations, investor discussions and strategic decision-making.

High-level view of Repco Home Finance’s business model that quickly pinpoints lending, distribution and risk-management pain points; editable and shareable to save hours structuring strategic plans and align teams for faster decision-making.

Activities

Retail housing loan origination

Sourcing and assessing applications for purchase, construction, repair and improvement focuses on middle and lower-income segments with localized underwriting tailored to informal incomes; field visits and income surrogate assessments verify cash flows and collateral.

Underwriting and risk management

Credit appraisal blends bank statement analytics, project cash-flow assessments and field verification to underwrite informal-income and self-employed borrowers, improving affordability scoring and repayment prediction. Collateral valuation, title and legal checks and strict LTV discipline protect recovery value and legal enforceability. Continuous portfolio monitoring with vintage tracking and early-warning triggers enables timely remediation. Risk-based pricing and conservative provisioning sustain asset quality.

Collections and customer servicing

Timely EMI collections are executed via digital payment rails and field recovery teams, aligning with RBI/HFC regulatory framework as of 2024. Soft- and hard-bucket segmentation (eg 30/90/180-day buckets) is used to prioritize interventions and control delinquencies. Customer grievance redressal and service requests follow statutory timelines and restructuring support is provided where permissible under 2024 RBI norms.

Liability management and securitization

Repco manages cost of funds through bank lines, NHB refinance and market borrowings, using securitization/assignment to recycle capital and support lending growth; ALM tracks tenors to control interest‑rate and liquidity risk amid a 2024 repo backdrop of ~6.5% and tight spreads. Hedging is used selectively to stabilize net interest margins while prioritizing low‑cost, long‑tenor funding.

- Bank/NHB/market mix

- Securitization for capital recycling; ALM + selective hedging

Branch network expansion and marketing

Repco Home Finance is deepening its South India footprint while selectively entering new states, leveraging a branch network of about 135 locations in 2024 to improve retail sourcing and loan disbursals. Localized campaigns and community outreach drive trust and NPA-sensitive borrower screening, complemented by partnerships with developers and a 1,200-strong DSA network for pipeline growth. Digital marketing and CRM tools augment feet-on-street sourcing, raising lead conversion and reducing customer acquisition cost.

Field-verified low-income lending with strict LTVs; repo 6.5%

Sourcing/appraisal focused on middle‑low incomes with field verification, bank‑stmt analytics and strict LTVs to protect recoveries. Collections via digital rails and field teams; vintage monitoring and RBI‑aligned restructuring processes (2024 norms). Funding mix: bank/NHB/market + securitization; ALM/hedging manage rate risk (repo ~6.5%). Distribution: ~135 branches, ~1,200 DSAs driving sourcing.

| Metric | 2024 |

|---|---|

| Branches | ~135 |

| DSAs | ~1,200 |

| Repo rate | ~6.5% |

Delivered as Displayed

Business Model Canvas

The Repco Home Finance Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the same structure and content you’ll receive after purchase. When you complete your order, you’ll get this exact document ready to edit and present in the provided formats. No surprises—what you see is what you’ll download.