Repco Home Finance Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Repco Home Finance faces moderate buyer power, rising competitive intensity from banks and NBFCs, and regulatory pressures shaping margins. Our snapshot highlights key supplier and substitute threats but skips granular force ratings and scenarios. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed, actionable insights and visuals to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated funding sources

Repco Home Finance depends on bank lines, NHB refinance and market borrowings for liquidity; a concentrated pool of large lenders increases their ability to tighten pricing and impose stricter covenants. Market tightening in 2024, with the RBI policy repo at 6.50%, pushed wholesale funding costs higher, pressuring RHFLs funding margin. Supplier concentration therefore elevates negotiation power over RHFL, risking higher cost of funds and reduced flexibility.

NHB and regulatory dependence

NHB refinance and regulatory norms materially shape tenor, pricing and compliance costs for Repco Home Finance; NHB refinance outstanding to HFCs was about Rs 1.8 lakh crore in FY2023-24, underscoring dependence on its windows. Access is cyclical and conditional on portfolio quality and credit metrics, with tighter eligibility raising funding costs. Policy shifts—rate or tenor changes—directly compress spread sustainability, amplifying supplier leverage via this regulatory channel.

Promoter bank linkage

Repco Bank affiliation strengthens Repco Home Finance’s funding access and market credibility through promoter support, improving wholesale funding lines and depositor confidence. Dependence on the promoter for credit lines concentrates supplier power and can constrain pricing flexibility for the lender. Any repricing or allocation shifts by the promoter translate quickly into margin pressure and funding cost volatility. The relationship thus both stabilizes funding and concentrates supplier influence.

Capital market investors

Capital market investors buying NCDs and securitisations press RHFL for higher risk premiums tied to asset quality and liquidity; spread widening in credit cycles (repo 6.5% as of June 2024) raises RHFL’s funding costs and narrows margins. Rating downgrades or weaker disclosures quickly shift bargaining power to investors, who price in volatility and liquidity risk. Market investors therefore exert price-sensitive supplier power, forcing RHFL to manage credit metrics and transparency to retain access.

- Risk premiums: priced to asset quality/liquidity

- Funding impact: spreads rise in credit stress

- Disclosure/ratings: shift investor leverage

- Outcome: investors hold price-sensitive power

Technology and data vendors

Core lending systems, credit bureaus, and fintech partners are specialized suppliers for Repco Home Finance; switching these platforms is costly and often takes 6–18 months at scale, creating friction and operational risk. Vendor pricing and API/integration terms can lift unit costs by roughly 5–50 basis points on loan yield, giving suppliers moderate non-financial bargaining power.

- Specialized suppliers: core systems, bureaus, fintechs

- Switching time: 6–18 months

- Impact on unit economics: ~5–50 bps

- Result: moderate supplier power

Concentrated NHB/bank funding and 6.50% repo amplify cost-of-funds and repricing risk

Supplier power over Repco Home Finance is elevated: concentrated bank/NHB funding (NHB refinance ~Rs 1.8 lakh crore in FY2023-24) and repo at 6.50% (Jun 2024) raise cost-of-funds risk. Promoter lines and capital markets (NCDs/securitisations) amplify repricing pressure; vendors (core systems, bureaus) add 5–50 bps and take 6–18 months to replace.

| Supplier | Key metric (2024) |

|---|---|

| NHB/banks | Rs 1.8L Cr; repo 6.50% |

| Vendors | 5–50 bps; 6–18 months |

What is included in the product

Tailored Porter's Five Forces analysis for Repco Home Finance that uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, barriers deterring new entrants, and substitutes or disruptive threats to market share.

A clear one-sheet Porter's Five Forces summary for Repco Home Finance—perfect for quick boardroom decisions and investor briefs; customize pressure levels and swap in your own data to reflect changing RBI rules, new entrants, or mortgage-rate shifts without complex tools.

Customers Bargaining Power

Price-sensitive target segment

Middle and lower-income customers of Repco Home Finance are highly rate and EMI sensitive; CRISIL estimated affordable housing comprised about 65% of housing finance demand in 2024, concentrating pricing pressure. Even a 25–50 basis-point shift versus the RBI repo rate of 6.5% (June 2024) can change borrower EMI affordability, prompting switching or renegotiation. Subsidy schemes like PMAY further sharpen price focus, raising customer bargaining power on interest and fees.

Multiple lender options

Regional NBFC-HFCs, banks and 11 small finance banks compete for the same borrower cohorts; Repco Home Finance had an AUM of about ₹13,000 crore as of Mar 2024, illustrating crowded supply. Easy online comparison and doorstep sourcing raise switchability; prepayments and balance transfers spike when rates drop, and the presence of 40+ HFCs plus banks expands choice breadth, increasing customer bargaining power.

Service and turnaround time

Fast approvals and flexible underwriting drive selection in informal-income segments, where customers prioritize speed and ease of documentation. Delays of even a few days trigger churn to more agile rivals and DSAs, shifting bargaining power toward providers promising quicker turnaround. Operational speed thus becomes a key negotiation lever as many customers weigh convenience over brand.

Cross-sell and relationship depth

Repco Home Finance's limited cross-sell and shallow relationship depth reduce customer lock-in, enabling borrowers to switch lenders when better terms appear.

Limited ancillary benefits and minimal bundled services weaken switching costs, so customers face little friction to refinance.

As credit profiles improve, buyers can refinance with larger banks, increasing customer bargaining power and pressuring margins.

- Shallow cross-sell

- Weak ancillary benefits

- Refinance risk

- Higher bargaining power

Information parity via DSAs

Intermediaries such as DSAs present 3–4 competing offers transparently to Repco Home Finance borrowers, compressing spreads and standardizing pricing and documentation across lenders in 2024.

This information parity gives customers negotiating insight and faster comparison without heavy effort; DSAs therefore act as force multipliers that indirectly amplify buyer power by increasing quote transparency and conversion pressure on margins.

- DSA visibility: multiple lender offers

- Effect: narrower spreads, standardized terms

- Buyer benefit: easier negotiation, quicker decisions

- Net impact: increased bargaining power

65% affordable buyers shift with 6.5% repo moves

Customers (65% affordable housing demand in 2024 per CRISIL) are highly rate/EMI sensitive; RBI repo 6.5% (Jun 2024) shifts of 25–50bp prompt switching. Repco AUM ~₹13,000 crore (Mar 2024) faces crowded supply and easy quote comparison via DSAs, raising bargaining power and refinance risk.

| Metric | Value |

|---|---|

| Affordable share | 65% |

| RBI repo Jun 24 | 6.5% |

| Repco AUM Mar 24 | ₹13,000 cr |

Preview the Actual Deliverable

Repco Home Finance Porter's Five Forces Analysis

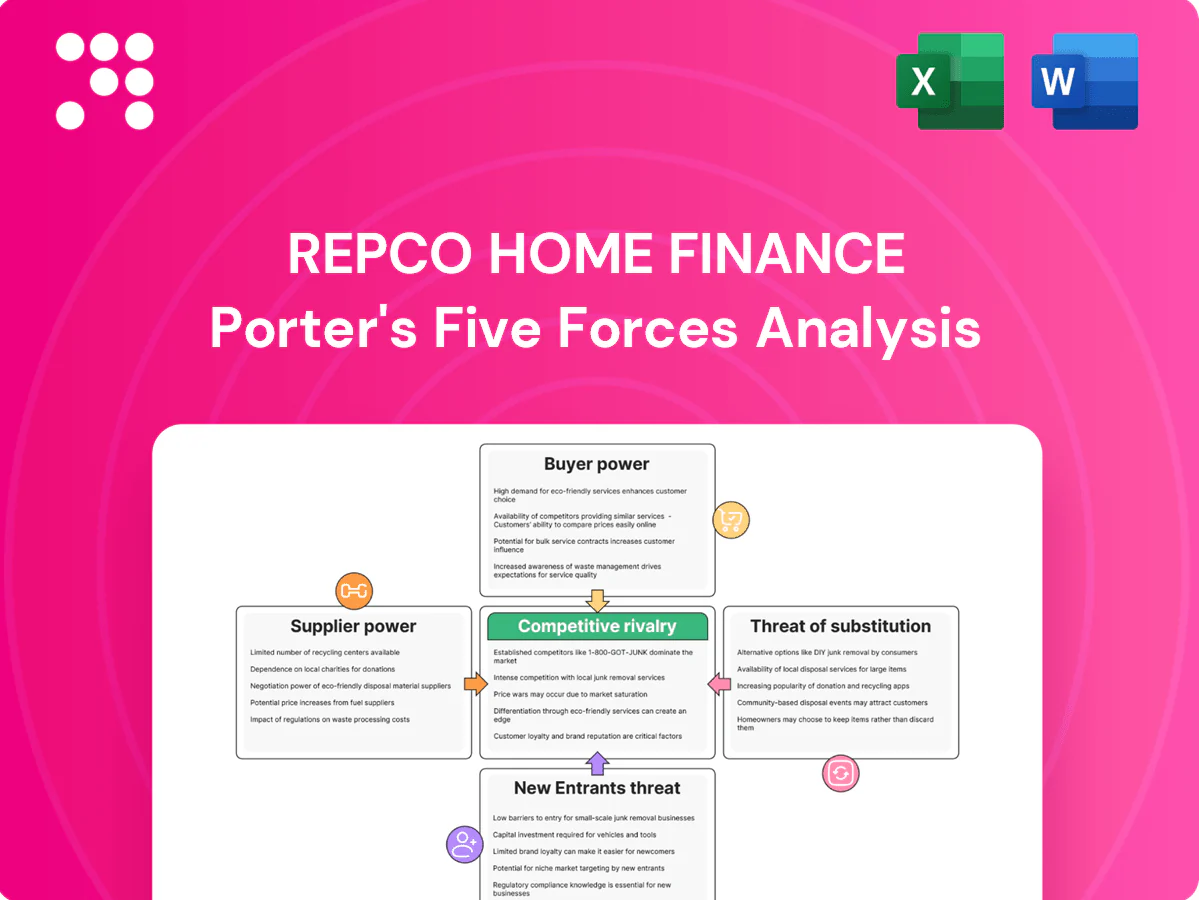

This preview shows the exact Repco Home Finance Porter's Five Forces analysis you'll receive—no placeholders or excerpts. Upon purchase you get instant access to this fully formatted, final document ready for download and use. It covers competitive rivalry, supplier and buyer power, threats of substitution and entry with actionable insights.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Repco Home Finance faces moderate buyer power, rising competitive intensity from banks and NBFCs, and regulatory pressures shaping margins. Our snapshot highlights key supplier and substitute threats but skips granular force ratings and scenarios. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed, actionable insights and visuals to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated funding sources

Repco Home Finance depends on bank lines, NHB refinance and market borrowings for liquidity; a concentrated pool of large lenders increases their ability to tighten pricing and impose stricter covenants. Market tightening in 2024, with the RBI policy repo at 6.50%, pushed wholesale funding costs higher, pressuring RHFLs funding margin. Supplier concentration therefore elevates negotiation power over RHFL, risking higher cost of funds and reduced flexibility.

NHB and regulatory dependence

NHB refinance and regulatory norms materially shape tenor, pricing and compliance costs for Repco Home Finance; NHB refinance outstanding to HFCs was about Rs 1.8 lakh crore in FY2023-24, underscoring dependence on its windows. Access is cyclical and conditional on portfolio quality and credit metrics, with tighter eligibility raising funding costs. Policy shifts—rate or tenor changes—directly compress spread sustainability, amplifying supplier leverage via this regulatory channel.

Promoter bank linkage

Repco Bank affiliation strengthens Repco Home Finance’s funding access and market credibility through promoter support, improving wholesale funding lines and depositor confidence. Dependence on the promoter for credit lines concentrates supplier power and can constrain pricing flexibility for the lender. Any repricing or allocation shifts by the promoter translate quickly into margin pressure and funding cost volatility. The relationship thus both stabilizes funding and concentrates supplier influence.

Capital market investors

Capital market investors buying NCDs and securitisations press RHFL for higher risk premiums tied to asset quality and liquidity; spread widening in credit cycles (repo 6.5% as of June 2024) raises RHFL’s funding costs and narrows margins. Rating downgrades or weaker disclosures quickly shift bargaining power to investors, who price in volatility and liquidity risk. Market investors therefore exert price-sensitive supplier power, forcing RHFL to manage credit metrics and transparency to retain access.

- Risk premiums: priced to asset quality/liquidity

- Funding impact: spreads rise in credit stress

- Disclosure/ratings: shift investor leverage

- Outcome: investors hold price-sensitive power

Technology and data vendors

Core lending systems, credit bureaus, and fintech partners are specialized suppliers for Repco Home Finance; switching these platforms is costly and often takes 6–18 months at scale, creating friction and operational risk. Vendor pricing and API/integration terms can lift unit costs by roughly 5–50 basis points on loan yield, giving suppliers moderate non-financial bargaining power.

- Specialized suppliers: core systems, bureaus, fintechs

- Switching time: 6–18 months

- Impact on unit economics: ~5–50 bps

- Result: moderate supplier power

Concentrated NHB/bank funding and 6.50% repo amplify cost-of-funds and repricing risk

Supplier power over Repco Home Finance is elevated: concentrated bank/NHB funding (NHB refinance ~Rs 1.8 lakh crore in FY2023-24) and repo at 6.50% (Jun 2024) raise cost-of-funds risk. Promoter lines and capital markets (NCDs/securitisations) amplify repricing pressure; vendors (core systems, bureaus) add 5–50 bps and take 6–18 months to replace.

| Supplier | Key metric (2024) |

|---|---|

| NHB/banks | Rs 1.8L Cr; repo 6.50% |

| Vendors | 5–50 bps; 6–18 months |

What is included in the product

Tailored Porter's Five Forces analysis for Repco Home Finance that uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, barriers deterring new entrants, and substitutes or disruptive threats to market share.

A clear one-sheet Porter's Five Forces summary for Repco Home Finance—perfect for quick boardroom decisions and investor briefs; customize pressure levels and swap in your own data to reflect changing RBI rules, new entrants, or mortgage-rate shifts without complex tools.

Customers Bargaining Power

Price-sensitive target segment

Middle and lower-income customers of Repco Home Finance are highly rate and EMI sensitive; CRISIL estimated affordable housing comprised about 65% of housing finance demand in 2024, concentrating pricing pressure. Even a 25–50 basis-point shift versus the RBI repo rate of 6.5% (June 2024) can change borrower EMI affordability, prompting switching or renegotiation. Subsidy schemes like PMAY further sharpen price focus, raising customer bargaining power on interest and fees.

Multiple lender options

Regional NBFC-HFCs, banks and 11 small finance banks compete for the same borrower cohorts; Repco Home Finance had an AUM of about ₹13,000 crore as of Mar 2024, illustrating crowded supply. Easy online comparison and doorstep sourcing raise switchability; prepayments and balance transfers spike when rates drop, and the presence of 40+ HFCs plus banks expands choice breadth, increasing customer bargaining power.

Service and turnaround time

Fast approvals and flexible underwriting drive selection in informal-income segments, where customers prioritize speed and ease of documentation. Delays of even a few days trigger churn to more agile rivals and DSAs, shifting bargaining power toward providers promising quicker turnaround. Operational speed thus becomes a key negotiation lever as many customers weigh convenience over brand.

Cross-sell and relationship depth

Repco Home Finance's limited cross-sell and shallow relationship depth reduce customer lock-in, enabling borrowers to switch lenders when better terms appear.

Limited ancillary benefits and minimal bundled services weaken switching costs, so customers face little friction to refinance.

As credit profiles improve, buyers can refinance with larger banks, increasing customer bargaining power and pressuring margins.

- Shallow cross-sell

- Weak ancillary benefits

- Refinance risk

- Higher bargaining power

Information parity via DSAs

Intermediaries such as DSAs present 3–4 competing offers transparently to Repco Home Finance borrowers, compressing spreads and standardizing pricing and documentation across lenders in 2024.

This information parity gives customers negotiating insight and faster comparison without heavy effort; DSAs therefore act as force multipliers that indirectly amplify buyer power by increasing quote transparency and conversion pressure on margins.

- DSA visibility: multiple lender offers

- Effect: narrower spreads, standardized terms

- Buyer benefit: easier negotiation, quicker decisions

- Net impact: increased bargaining power

65% affordable buyers shift with 6.5% repo moves

Customers (65% affordable housing demand in 2024 per CRISIL) are highly rate/EMI sensitive; RBI repo 6.5% (Jun 2024) shifts of 25–50bp prompt switching. Repco AUM ~₹13,000 crore (Mar 2024) faces crowded supply and easy quote comparison via DSAs, raising bargaining power and refinance risk.

| Metric | Value |

|---|---|

| Affordable share | 65% |

| RBI repo Jun 24 | 6.5% |

| Repco AUM Mar 24 | ₹13,000 cr |

Preview the Actual Deliverable

Repco Home Finance Porter's Five Forces Analysis

This preview shows the exact Repco Home Finance Porter's Five Forces analysis you'll receive—no placeholders or excerpts. Upon purchase you get instant access to this fully formatted, final document ready for download and use. It covers competitive rivalry, supplier and buyer power, threats of substitution and entry with actionable insights.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Repco Home Finance faces moderate buyer power, rising competitive intensity from banks and NBFCs, and regulatory pressures shaping margins. Our snapshot highlights key supplier and substitute threats but skips granular force ratings and scenarios. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed, actionable insights and visuals to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated funding sources

Repco Home Finance depends on bank lines, NHB refinance and market borrowings for liquidity; a concentrated pool of large lenders increases their ability to tighten pricing and impose stricter covenants. Market tightening in 2024, with the RBI policy repo at 6.50%, pushed wholesale funding costs higher, pressuring RHFLs funding margin. Supplier concentration therefore elevates negotiation power over RHFL, risking higher cost of funds and reduced flexibility.

NHB and regulatory dependence

NHB refinance and regulatory norms materially shape tenor, pricing and compliance costs for Repco Home Finance; NHB refinance outstanding to HFCs was about Rs 1.8 lakh crore in FY2023-24, underscoring dependence on its windows. Access is cyclical and conditional on portfolio quality and credit metrics, with tighter eligibility raising funding costs. Policy shifts—rate or tenor changes—directly compress spread sustainability, amplifying supplier leverage via this regulatory channel.

Promoter bank linkage

Repco Bank affiliation strengthens Repco Home Finance’s funding access and market credibility through promoter support, improving wholesale funding lines and depositor confidence. Dependence on the promoter for credit lines concentrates supplier power and can constrain pricing flexibility for the lender. Any repricing or allocation shifts by the promoter translate quickly into margin pressure and funding cost volatility. The relationship thus both stabilizes funding and concentrates supplier influence.

Capital market investors

Capital market investors buying NCDs and securitisations press RHFL for higher risk premiums tied to asset quality and liquidity; spread widening in credit cycles (repo 6.5% as of June 2024) raises RHFL’s funding costs and narrows margins. Rating downgrades or weaker disclosures quickly shift bargaining power to investors, who price in volatility and liquidity risk. Market investors therefore exert price-sensitive supplier power, forcing RHFL to manage credit metrics and transparency to retain access.

- Risk premiums: priced to asset quality/liquidity

- Funding impact: spreads rise in credit stress

- Disclosure/ratings: shift investor leverage

- Outcome: investors hold price-sensitive power

Technology and data vendors

Core lending systems, credit bureaus, and fintech partners are specialized suppliers for Repco Home Finance; switching these platforms is costly and often takes 6–18 months at scale, creating friction and operational risk. Vendor pricing and API/integration terms can lift unit costs by roughly 5–50 basis points on loan yield, giving suppliers moderate non-financial bargaining power.

- Specialized suppliers: core systems, bureaus, fintechs

- Switching time: 6–18 months

- Impact on unit economics: ~5–50 bps

- Result: moderate supplier power

Concentrated NHB/bank funding and 6.50% repo amplify cost-of-funds and repricing risk

Supplier power over Repco Home Finance is elevated: concentrated bank/NHB funding (NHB refinance ~Rs 1.8 lakh crore in FY2023-24) and repo at 6.50% (Jun 2024) raise cost-of-funds risk. Promoter lines and capital markets (NCDs/securitisations) amplify repricing pressure; vendors (core systems, bureaus) add 5–50 bps and take 6–18 months to replace.

| Supplier | Key metric (2024) |

|---|---|

| NHB/banks | Rs 1.8L Cr; repo 6.50% |

| Vendors | 5–50 bps; 6–18 months |

What is included in the product

Tailored Porter's Five Forces analysis for Repco Home Finance that uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, barriers deterring new entrants, and substitutes or disruptive threats to market share.

A clear one-sheet Porter's Five Forces summary for Repco Home Finance—perfect for quick boardroom decisions and investor briefs; customize pressure levels and swap in your own data to reflect changing RBI rules, new entrants, or mortgage-rate shifts without complex tools.

Customers Bargaining Power

Price-sensitive target segment

Middle and lower-income customers of Repco Home Finance are highly rate and EMI sensitive; CRISIL estimated affordable housing comprised about 65% of housing finance demand in 2024, concentrating pricing pressure. Even a 25–50 basis-point shift versus the RBI repo rate of 6.5% (June 2024) can change borrower EMI affordability, prompting switching or renegotiation. Subsidy schemes like PMAY further sharpen price focus, raising customer bargaining power on interest and fees.

Multiple lender options

Regional NBFC-HFCs, banks and 11 small finance banks compete for the same borrower cohorts; Repco Home Finance had an AUM of about ₹13,000 crore as of Mar 2024, illustrating crowded supply. Easy online comparison and doorstep sourcing raise switchability; prepayments and balance transfers spike when rates drop, and the presence of 40+ HFCs plus banks expands choice breadth, increasing customer bargaining power.

Service and turnaround time

Fast approvals and flexible underwriting drive selection in informal-income segments, where customers prioritize speed and ease of documentation. Delays of even a few days trigger churn to more agile rivals and DSAs, shifting bargaining power toward providers promising quicker turnaround. Operational speed thus becomes a key negotiation lever as many customers weigh convenience over brand.

Cross-sell and relationship depth

Repco Home Finance's limited cross-sell and shallow relationship depth reduce customer lock-in, enabling borrowers to switch lenders when better terms appear.

Limited ancillary benefits and minimal bundled services weaken switching costs, so customers face little friction to refinance.

As credit profiles improve, buyers can refinance with larger banks, increasing customer bargaining power and pressuring margins.

- Shallow cross-sell

- Weak ancillary benefits

- Refinance risk

- Higher bargaining power

Information parity via DSAs

Intermediaries such as DSAs present 3–4 competing offers transparently to Repco Home Finance borrowers, compressing spreads and standardizing pricing and documentation across lenders in 2024.

This information parity gives customers negotiating insight and faster comparison without heavy effort; DSAs therefore act as force multipliers that indirectly amplify buyer power by increasing quote transparency and conversion pressure on margins.

- DSA visibility: multiple lender offers

- Effect: narrower spreads, standardized terms

- Buyer benefit: easier negotiation, quicker decisions

- Net impact: increased bargaining power

65% affordable buyers shift with 6.5% repo moves

Customers (65% affordable housing demand in 2024 per CRISIL) are highly rate/EMI sensitive; RBI repo 6.5% (Jun 2024) shifts of 25–50bp prompt switching. Repco AUM ~₹13,000 crore (Mar 2024) faces crowded supply and easy quote comparison via DSAs, raising bargaining power and refinance risk.

| Metric | Value |

|---|---|

| Affordable share | 65% |

| RBI repo Jun 24 | 6.5% |

| Repco AUM Mar 24 | ₹13,000 cr |

Preview the Actual Deliverable

Repco Home Finance Porter's Five Forces Analysis

This preview shows the exact Repco Home Finance Porter's Five Forces analysis you'll receive—no placeholders or excerpts. Upon purchase you get instant access to this fully formatted, final document ready for download and use. It covers competitive rivalry, supplier and buyer power, threats of substitution and entry with actionable insights.