Repsol Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

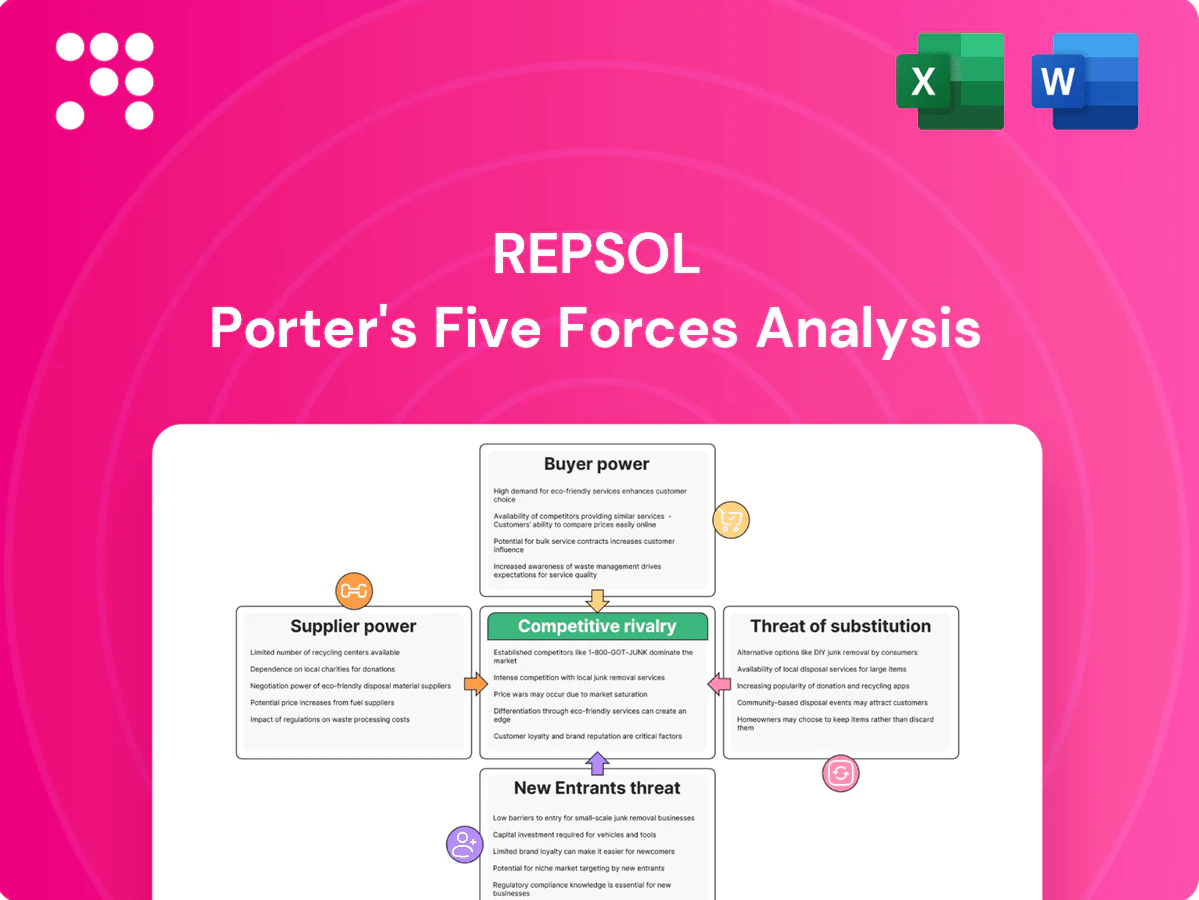

Repsol faces intense industry rivalry, significant regulatory and commodity-price pressures, moderate supplier bargaining power and growing threats from low‑carbon substitutes, while barriers to entry remain mixed. This snapshot highlights strategic pressure points that affect margins and growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations tailored to Repsol.

Suppliers Bargaining Power

Resource owners & NOCs

Access to upstream blocks is largely controlled by governments and NOCs, which in 2024 held over 80% of global oil and gas reserves, allowing them to set terms, local content rules and fiscal take that elevate supplier leverage.

License renewal risk and geopolitical exposure further strengthen NOC bargaining power, while long-cycle upstream investments (typically 5–15 years) limit Repsol’s negotiation flexibility.

Repsol’s diversified portfolio moderates concentration risk, though competitive bid rounds with multiple IOCs can still compress terms and royalties.

Oilfield services & equipment

Service majors and specialized OEMs (drilling, subsea, compressors) can lift pricing power in tight 2024 capacity cycles, with supplier bottlenecks contributing to higher unit costs; industry reports flagged double-digit input inflation in 2024 for key subsea components. Repsol counters via frame agreements, dual-sourcing and equipment standardization, preserving procurement flexibility against tech lock-in on critical kit such as advanced catalysts.

Renewables OEMs & EPCs

Turbine, inverter and tracker OEMs exert pricing power when order books are full, with typical turbine lead times reported at 12–24 months and inverter lead times often 6–12 months, while grid equipment and EPC capacity constraints can push COD delays of 6–18 months and compress returns. Repsol mitigates exposure via pipeline phasing, financial hedges and strategic supplier partnerships; localization rules in markets such as the US (IRA) and India further limit vendor choice.

Feedstocks for biofuels/SAF

Feedstocks for biofuels/SAF such as used cooking oil, tallow and advanced lipids remained scarce and price-volatile in 2024, increasing supplier bargaining power; sustainability certification requirements further narrow available pools and raise transaction costs. Repsol’s mitigation via vertical integration and long-term offtakes secures volumes but often at firm pricing, while growing SAF mandates intensify competition for limited feedstock supply.

- Scarcity 2024: tight UCO/tallow supplies

- Certification: reduces eligible suppliers

- Mitigation: vertical integration + long-term offtakes

- Market pressure: SAF mandates raise demand

Labor & technology providers

- Skilled labor: concentrated, ~25,000 employees (2023–24)

- Tech: proprietary subsurface/digital platforms → switching costs

- Regulation: unions and safety regimes impact schedules/costs

- Mitigation: partnerships + in‑house capability development

NOCs >80% reserves; bottlenecks fuel double-digit input inflation

Supplier power is high: NOCs/Governments control >80% reserves (2024), setting fiscal and local-content terms that limit Repsol’s upstream leverage. Service/OEM bottlenecks raised input inflation double-digits in 2024; turbines lead 12–24m, inverters 6–12m. Biofeedstocks (UCO/tallow) were tight in 2024, boosting prices; Repsol leans on vertical integration and long-term offtakes.

| Metric | 2024 |

|---|---|

| NOC reserve share | >80% |

| Repsol staff | ~25,000 |

| Turbine lead time | 12–24m |

| Input inflation (subsea) | Double-digit |

What is included in the product

Tailored for Repsol, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier power, entry barriers and substitute threats shaping its profitability; it highlights disruptive forces and strategic levers Repsol can use to defend market share and pricing.

A concise, one-sheet Porter's Five Forces for Repsol that clarifies competitive pressures for rapid decision-making. Editable pressure levels and an instant spider chart make scenario testing and slide-ready exports effortless.

Customers Bargaining Power

Retail fuel consumers

Retail fuel consumers exert significant bargaining power: gasoline/diesel buyers are highly price sensitive with low switching costs between stations, and Repsol’s network scale (roughly 4,700 service stations in 2024) and loyalty programs partially reduce churn but cannot fully offset near-real-time price transparency. Regulation on margins and competition law caps pricing flexibility, while rising EV market share — approaching low-double digits of new car sales in Europe by 2024 — gradually erodes fuel demand and long-term retail leverage.

Commercial & industrial fuels

Logistics fleets, construction and marine buyers push hard on volumes and discounts, with large tenders often driving price cuts of low- to mid-single digits; contract tendering increased supplier price pressure in 2024 as buyers consolidated suppliers. Repsol offsets this with bundled services, guaranteed delivery performance and emissions solutions, leveraging HVO and LNG differentiation—HVO pricing in 2024 remained roughly 20–30% above fossil diesel, requiring near price parity to scale uptake, while EU carbon was around €90/t in mid-2024.

Airlines for jet/SAF

Airlines wield outsized bargaining power through consortiums and long-term offtake contracts, leveraging IATA's 10% SAF-by-2030 ambition to demand cost pass-throughs and co-investment in supply projects. Price-indexing clauses and sustainability certification (e.g., ISCC, RSB) are central to negotiations. With global SAF supply still below 1% of jet fuel in 2024, scarcity can temporarily reduce buyer leverage.

Petrochemicals & refining offtakers

Commodity polymers and intermediates are priced off global benchmarks tied to ethylene and Brent, with Brent averaging about 86 USD/bbl in 2024, giving buyers strong leverage. Standardized specs make switching suppliers easy, pressuring margins. Repsol’s long-term customer ties and logistics proximity help defend volumes, but cyclical downturns compress spreads and amplify buyer bargaining.

- Benchmark linkage: Brent ~86 USD/bbl (2024)

- Standard specs = low switching costs

- Customer relationships/logistics = defensive

- Downcycles = tighter spreads

Power purchasers & PPAs

Corporate and utility offtakers use advanced analytics to push PPA tenor, price and shape; tenors commonly extend 10–15 years and markets show margin compression as pipeline and auction volumes rise. Repsol’s 2024 renewables push (targeting ~20 GW by 2030) can leverage hybridization and storage to capture higher value. Buyer credit quality materially alters financing costs and covenant terms.

- PPA tenor: 10–15 years

- Repsol target: ~20 GW by 2030

- Storage/hybrid: value uplift

- Buyer credit: impacts financing

2024: Buyers squeeze margins — retail ≈4,700 sts, Brent ≈86 USD/bbl

Customers exert strong price pressure across segments in 2024: retail price sensitivity (≈4,700 stations), fleets demand volume discounts, airlines push SAF cost-sharing, polymers follow Brent-linked benchmarks (Brent ≈86 USD/bbl), and PPAs show 10–15y tenors compressing margins.

| Segment | 2024 metric | Buyer power |

|---|---|---|

| Retail | ≈4,700 sts | High |

| Fleets | HVO +20–30% vs diesel | High |

| Airlines | SAF <1% supply | High |

| Polymers | Brent ≈86 USD/bbl | High |

| PPAs | 10–15y tenor | Medium–High |

Preview the Actual Deliverable

Repsol Porter's Five Forces Analysis

This preview shows the exact Repsol Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted, ready for download and use the moment you buy. You’re viewing the final deliverable, identical to the file provided after payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Repsol faces intense industry rivalry, significant regulatory and commodity-price pressures, moderate supplier bargaining power and growing threats from low‑carbon substitutes, while barriers to entry remain mixed. This snapshot highlights strategic pressure points that affect margins and growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations tailored to Repsol.

Suppliers Bargaining Power

Resource owners & NOCs

Access to upstream blocks is largely controlled by governments and NOCs, which in 2024 held over 80% of global oil and gas reserves, allowing them to set terms, local content rules and fiscal take that elevate supplier leverage.

License renewal risk and geopolitical exposure further strengthen NOC bargaining power, while long-cycle upstream investments (typically 5–15 years) limit Repsol’s negotiation flexibility.

Repsol’s diversified portfolio moderates concentration risk, though competitive bid rounds with multiple IOCs can still compress terms and royalties.

Oilfield services & equipment

Service majors and specialized OEMs (drilling, subsea, compressors) can lift pricing power in tight 2024 capacity cycles, with supplier bottlenecks contributing to higher unit costs; industry reports flagged double-digit input inflation in 2024 for key subsea components. Repsol counters via frame agreements, dual-sourcing and equipment standardization, preserving procurement flexibility against tech lock-in on critical kit such as advanced catalysts.

Renewables OEMs & EPCs

Turbine, inverter and tracker OEMs exert pricing power when order books are full, with typical turbine lead times reported at 12–24 months and inverter lead times often 6–12 months, while grid equipment and EPC capacity constraints can push COD delays of 6–18 months and compress returns. Repsol mitigates exposure via pipeline phasing, financial hedges and strategic supplier partnerships; localization rules in markets such as the US (IRA) and India further limit vendor choice.

Feedstocks for biofuels/SAF

Feedstocks for biofuels/SAF such as used cooking oil, tallow and advanced lipids remained scarce and price-volatile in 2024, increasing supplier bargaining power; sustainability certification requirements further narrow available pools and raise transaction costs. Repsol’s mitigation via vertical integration and long-term offtakes secures volumes but often at firm pricing, while growing SAF mandates intensify competition for limited feedstock supply.

- Scarcity 2024: tight UCO/tallow supplies

- Certification: reduces eligible suppliers

- Mitigation: vertical integration + long-term offtakes

- Market pressure: SAF mandates raise demand

Labor & technology providers

- Skilled labor: concentrated, ~25,000 employees (2023–24)

- Tech: proprietary subsurface/digital platforms → switching costs

- Regulation: unions and safety regimes impact schedules/costs

- Mitigation: partnerships + in‑house capability development

NOCs >80% reserves; bottlenecks fuel double-digit input inflation

Supplier power is high: NOCs/Governments control >80% reserves (2024), setting fiscal and local-content terms that limit Repsol’s upstream leverage. Service/OEM bottlenecks raised input inflation double-digits in 2024; turbines lead 12–24m, inverters 6–12m. Biofeedstocks (UCO/tallow) were tight in 2024, boosting prices; Repsol leans on vertical integration and long-term offtakes.

| Metric | 2024 |

|---|---|

| NOC reserve share | >80% |

| Repsol staff | ~25,000 |

| Turbine lead time | 12–24m |

| Input inflation (subsea) | Double-digit |

What is included in the product

Tailored for Repsol, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier power, entry barriers and substitute threats shaping its profitability; it highlights disruptive forces and strategic levers Repsol can use to defend market share and pricing.

A concise, one-sheet Porter's Five Forces for Repsol that clarifies competitive pressures for rapid decision-making. Editable pressure levels and an instant spider chart make scenario testing and slide-ready exports effortless.

Customers Bargaining Power

Retail fuel consumers

Retail fuel consumers exert significant bargaining power: gasoline/diesel buyers are highly price sensitive with low switching costs between stations, and Repsol’s network scale (roughly 4,700 service stations in 2024) and loyalty programs partially reduce churn but cannot fully offset near-real-time price transparency. Regulation on margins and competition law caps pricing flexibility, while rising EV market share — approaching low-double digits of new car sales in Europe by 2024 — gradually erodes fuel demand and long-term retail leverage.

Commercial & industrial fuels

Logistics fleets, construction and marine buyers push hard on volumes and discounts, with large tenders often driving price cuts of low- to mid-single digits; contract tendering increased supplier price pressure in 2024 as buyers consolidated suppliers. Repsol offsets this with bundled services, guaranteed delivery performance and emissions solutions, leveraging HVO and LNG differentiation—HVO pricing in 2024 remained roughly 20–30% above fossil diesel, requiring near price parity to scale uptake, while EU carbon was around €90/t in mid-2024.

Airlines for jet/SAF

Airlines wield outsized bargaining power through consortiums and long-term offtake contracts, leveraging IATA's 10% SAF-by-2030 ambition to demand cost pass-throughs and co-investment in supply projects. Price-indexing clauses and sustainability certification (e.g., ISCC, RSB) are central to negotiations. With global SAF supply still below 1% of jet fuel in 2024, scarcity can temporarily reduce buyer leverage.

Petrochemicals & refining offtakers

Commodity polymers and intermediates are priced off global benchmarks tied to ethylene and Brent, with Brent averaging about 86 USD/bbl in 2024, giving buyers strong leverage. Standardized specs make switching suppliers easy, pressuring margins. Repsol’s long-term customer ties and logistics proximity help defend volumes, but cyclical downturns compress spreads and amplify buyer bargaining.

- Benchmark linkage: Brent ~86 USD/bbl (2024)

- Standard specs = low switching costs

- Customer relationships/logistics = defensive

- Downcycles = tighter spreads

Power purchasers & PPAs

Corporate and utility offtakers use advanced analytics to push PPA tenor, price and shape; tenors commonly extend 10–15 years and markets show margin compression as pipeline and auction volumes rise. Repsol’s 2024 renewables push (targeting ~20 GW by 2030) can leverage hybridization and storage to capture higher value. Buyer credit quality materially alters financing costs and covenant terms.

- PPA tenor: 10–15 years

- Repsol target: ~20 GW by 2030

- Storage/hybrid: value uplift

- Buyer credit: impacts financing

2024: Buyers squeeze margins — retail ≈4,700 sts, Brent ≈86 USD/bbl

Customers exert strong price pressure across segments in 2024: retail price sensitivity (≈4,700 stations), fleets demand volume discounts, airlines push SAF cost-sharing, polymers follow Brent-linked benchmarks (Brent ≈86 USD/bbl), and PPAs show 10–15y tenors compressing margins.

| Segment | 2024 metric | Buyer power |

|---|---|---|

| Retail | ≈4,700 sts | High |

| Fleets | HVO +20–30% vs diesel | High |

| Airlines | SAF <1% supply | High |

| Polymers | Brent ≈86 USD/bbl | High |

| PPAs | 10–15y tenor | Medium–High |

Preview the Actual Deliverable

Repsol Porter's Five Forces Analysis

This preview shows the exact Repsol Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted, ready for download and use the moment you buy. You’re viewing the final deliverable, identical to the file provided after payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Repsol faces intense industry rivalry, significant regulatory and commodity-price pressures, moderate supplier bargaining power and growing threats from low‑carbon substitutes, while barriers to entry remain mixed. This snapshot highlights strategic pressure points that affect margins and growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations tailored to Repsol.

Suppliers Bargaining Power

Resource owners & NOCs

Access to upstream blocks is largely controlled by governments and NOCs, which in 2024 held over 80% of global oil and gas reserves, allowing them to set terms, local content rules and fiscal take that elevate supplier leverage.

License renewal risk and geopolitical exposure further strengthen NOC bargaining power, while long-cycle upstream investments (typically 5–15 years) limit Repsol’s negotiation flexibility.

Repsol’s diversified portfolio moderates concentration risk, though competitive bid rounds with multiple IOCs can still compress terms and royalties.

Oilfield services & equipment

Service majors and specialized OEMs (drilling, subsea, compressors) can lift pricing power in tight 2024 capacity cycles, with supplier bottlenecks contributing to higher unit costs; industry reports flagged double-digit input inflation in 2024 for key subsea components. Repsol counters via frame agreements, dual-sourcing and equipment standardization, preserving procurement flexibility against tech lock-in on critical kit such as advanced catalysts.

Renewables OEMs & EPCs

Turbine, inverter and tracker OEMs exert pricing power when order books are full, with typical turbine lead times reported at 12–24 months and inverter lead times often 6–12 months, while grid equipment and EPC capacity constraints can push COD delays of 6–18 months and compress returns. Repsol mitigates exposure via pipeline phasing, financial hedges and strategic supplier partnerships; localization rules in markets such as the US (IRA) and India further limit vendor choice.

Feedstocks for biofuels/SAF

Feedstocks for biofuels/SAF such as used cooking oil, tallow and advanced lipids remained scarce and price-volatile in 2024, increasing supplier bargaining power; sustainability certification requirements further narrow available pools and raise transaction costs. Repsol’s mitigation via vertical integration and long-term offtakes secures volumes but often at firm pricing, while growing SAF mandates intensify competition for limited feedstock supply.

- Scarcity 2024: tight UCO/tallow supplies

- Certification: reduces eligible suppliers

- Mitigation: vertical integration + long-term offtakes

- Market pressure: SAF mandates raise demand

Labor & technology providers

- Skilled labor: concentrated, ~25,000 employees (2023–24)

- Tech: proprietary subsurface/digital platforms → switching costs

- Regulation: unions and safety regimes impact schedules/costs

- Mitigation: partnerships + in‑house capability development

NOCs >80% reserves; bottlenecks fuel double-digit input inflation

Supplier power is high: NOCs/Governments control >80% reserves (2024), setting fiscal and local-content terms that limit Repsol’s upstream leverage. Service/OEM bottlenecks raised input inflation double-digits in 2024; turbines lead 12–24m, inverters 6–12m. Biofeedstocks (UCO/tallow) were tight in 2024, boosting prices; Repsol leans on vertical integration and long-term offtakes.

| Metric | 2024 |

|---|---|

| NOC reserve share | >80% |

| Repsol staff | ~25,000 |

| Turbine lead time | 12–24m |

| Input inflation (subsea) | Double-digit |

What is included in the product

Tailored for Repsol, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier power, entry barriers and substitute threats shaping its profitability; it highlights disruptive forces and strategic levers Repsol can use to defend market share and pricing.

A concise, one-sheet Porter's Five Forces for Repsol that clarifies competitive pressures for rapid decision-making. Editable pressure levels and an instant spider chart make scenario testing and slide-ready exports effortless.

Customers Bargaining Power

Retail fuel consumers

Retail fuel consumers exert significant bargaining power: gasoline/diesel buyers are highly price sensitive with low switching costs between stations, and Repsol’s network scale (roughly 4,700 service stations in 2024) and loyalty programs partially reduce churn but cannot fully offset near-real-time price transparency. Regulation on margins and competition law caps pricing flexibility, while rising EV market share — approaching low-double digits of new car sales in Europe by 2024 — gradually erodes fuel demand and long-term retail leverage.

Commercial & industrial fuels

Logistics fleets, construction and marine buyers push hard on volumes and discounts, with large tenders often driving price cuts of low- to mid-single digits; contract tendering increased supplier price pressure in 2024 as buyers consolidated suppliers. Repsol offsets this with bundled services, guaranteed delivery performance and emissions solutions, leveraging HVO and LNG differentiation—HVO pricing in 2024 remained roughly 20–30% above fossil diesel, requiring near price parity to scale uptake, while EU carbon was around €90/t in mid-2024.

Airlines for jet/SAF

Airlines wield outsized bargaining power through consortiums and long-term offtake contracts, leveraging IATA's 10% SAF-by-2030 ambition to demand cost pass-throughs and co-investment in supply projects. Price-indexing clauses and sustainability certification (e.g., ISCC, RSB) are central to negotiations. With global SAF supply still below 1% of jet fuel in 2024, scarcity can temporarily reduce buyer leverage.

Petrochemicals & refining offtakers

Commodity polymers and intermediates are priced off global benchmarks tied to ethylene and Brent, with Brent averaging about 86 USD/bbl in 2024, giving buyers strong leverage. Standardized specs make switching suppliers easy, pressuring margins. Repsol’s long-term customer ties and logistics proximity help defend volumes, but cyclical downturns compress spreads and amplify buyer bargaining.

- Benchmark linkage: Brent ~86 USD/bbl (2024)

- Standard specs = low switching costs

- Customer relationships/logistics = defensive

- Downcycles = tighter spreads

Power purchasers & PPAs

Corporate and utility offtakers use advanced analytics to push PPA tenor, price and shape; tenors commonly extend 10–15 years and markets show margin compression as pipeline and auction volumes rise. Repsol’s 2024 renewables push (targeting ~20 GW by 2030) can leverage hybridization and storage to capture higher value. Buyer credit quality materially alters financing costs and covenant terms.

- PPA tenor: 10–15 years

- Repsol target: ~20 GW by 2030

- Storage/hybrid: value uplift

- Buyer credit: impacts financing

2024: Buyers squeeze margins — retail ≈4,700 sts, Brent ≈86 USD/bbl

Customers exert strong price pressure across segments in 2024: retail price sensitivity (≈4,700 stations), fleets demand volume discounts, airlines push SAF cost-sharing, polymers follow Brent-linked benchmarks (Brent ≈86 USD/bbl), and PPAs show 10–15y tenors compressing margins.

| Segment | 2024 metric | Buyer power |

|---|---|---|

| Retail | ≈4,700 sts | High |

| Fleets | HVO +20–30% vs diesel | High |

| Airlines | SAF <1% supply | High |

| Polymers | Brent ≈86 USD/bbl | High |

| PPAs | 10–15y tenor | Medium–High |

Preview the Actual Deliverable

Repsol Porter's Five Forces Analysis

This preview shows the exact Repsol Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted, ready for download and use the moment you buy. You’re viewing the final deliverable, identical to the file provided after payment.