Resideo Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Resideo faces moderate supplier power, shifting buyer expectations, and rising substitute threats as smart‑home competition intensifies. This snapshot highlights key pressures and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force‑by‑force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Dependence on specialized components

Resideo depends on semiconductors, sensors, radios and ASICs from a narrow vendor set, raising switching costs and lead-time risk; supply shocks or capacity constraints can compress margins and delay delivery. Global semiconductor sales were $583B in 2023 and projected near $600B in 2024, underscoring tight markets. Long-term contracts and dual-sourcing reduce but do not remove concentration; strategic inventory and interchangeable designs help rebalance supplier power.

Contract manufacturing leverage

EMS partners control throughput, yields and hardware line costs, with EMS industry utilization around 88% in H1 2024, giving manufacturers pricing and allocation leverage in tight markets. Volume commitments and utilization allow EMS to extract premiums and priority capacity, pressuring OEM margins. Resideo can rebid programs, multi-source or regionalize supply to reduce exposure while prioritizing quality, IP protection and contractual flexibility.

Software and cloud dependencies

Software and cloud dependencies create vendor lock-in across cloud hosting, mobile OS (Android ~70% global share, iOS ~27%) and core stacks, with hyperscalers (AWS, Azure, GCP) controlling >60% of IaaS market, concentrating risk. API changes or pricing shifts from these platforms can materially raise operating costs. Negotiated enterprise agreements and architecture portability temper that exposure, and building proprietary middleware increases resilience over time.

Branded supplier pull at ADI

ADI distributes leading security, fire and low-voltage brands that installers demand, and tier-one suppliers can still command shelf space, rebates and MDF terms. Resideo reported roughly $5.8 billion in net sales in FY2024, underscoring ADI’s scale which, together with breadth and sell-through data, provides countervailing leverage. Exclusive lines and private-label products further rebalance supplier power.

- Tier-one brand leverage: strong

- Resideo FY2024 net sales: 5.8 billion

- ADI scale & data: offset supplier demands

- Exclusive/private label: reduces supplier power

Standards and certification gatekeepers

Standards bodies (UL, NFPA, FCC) and cybersecurity rules plus protocol consortia strongly steer Resideo component choices; certification often adds 3–12 months and testing fees from roughly $5,000 to >$100,000, raising supplier leverage. Early supplier engagement and use of pre-certified modules can cut approvals to weeks, and active participation in standards groups lets suppliers influence spec direction.

- Certification time: 3–12 months

- Testing fees: ~$5k–$100k+

- Pre-certified modules: approvals in weeks

- Standards participation shapes requirements

Company has concentrated semiconductor, sensor & EMS suppliers; FY24 sales $5.8B

Resideo faces concentrated suppliers for semiconductors, sensors and EMS, elevating switching costs and margin risk. Global semiconductor sales were $583B in 2023 and near $600B in 2024; EMS utilization ~88% in H1 2024. Cloud IaaS >60% market share concentrates platform risk; Resideo FY2024 sales $5.8B help counterbalance supplier leverage.

| Metric | Value |

|---|---|

| Semiconductor sales 2023 | $583B |

| Projection 2024 | ~$600B |

| EMS utilization H1 2024 | ~88% |

| Resideo FY2024 sales | $5.8B |

| IaaS market share | >60% |

What is included in the product

Tailored exclusively for Resideo, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threats from substitutes and new entrants, and identifies disruptive forces and market dynamics shaping pricing, profitability, and barriers protecting incumbents.

A concise Resideo Porter's Five Forces one-sheet that clarifies competitive pressures, lets you customize force levels with current data, and exports cleanly into pitch decks for fast strategic decisions.

Customers Bargaining Power

Professional installers and dealers

Professional installers drive product selection for Resideo; in 2024 Resideo reported $4.07 billion in net sales, with ADI distribution contributing about $2.5 billion, reinforcing installer loyalty. Installers can switch brands if economics or reliability falter, and their sensitivity to failure rates is amplified by truck-roll costs and technical preferences. Training, loyalty programs and Resideo’s integrated ecosystem raise switching costs. ADI’s availability and credit terms further retain dealers.

Large national integrators and builders

Large national integrators and production builders push hard on price and service, often securing multi-year deals that compress margins while stabilizing volume; Resideo reported roughly $4.1B in net sales in FY2024, underscoring how critical scale is to absorb lower ASPs. Value-add services and differentiated features help defend ASPs, while integration support and strict SLAs are frequently decisive in contract awards.

Retail and DIY consumers

Retail and DIY consumers compare smart home devices primarily on price, ease of setup, and app experience, driving high cross-shopping in a global smart home market that surpassed $90 billion in 2024; marketplace transparency increases price sensitivity and churn. Bundles, subscriptions, and proven interoperability materially reduce switching by embedding services. Strong reviews and brand trust in safety categories temper pure price pressure and support premium positioning for players like Resideo (FY2024 revenue ~ $3.2B).

Product availability and lead-time expectations

Customers increasingly demand rapid fulfillment—commonly 24–48 hour delivery for replacements and code-driven installs—making lead times a key driver of bargaining power; stockouts immediately shift projects to competitors with compatible SKUs. ADI’s broad distribution and advanced demand planning materially reduce defections, while accurate ETAs and proposed substitutes protect long-term installer relationships.

- 24–48h fulfillment expectations

- Stockouts => instant defections to compatible SKUs

- ADI network + demand planning mitigate churn

- Accurate ETA & substitutes preserve customer ties

Data and integration demands

Customers demand open APIs, Matter/Zigbee/Z-Wave compatibility and cloud reliability, pressuring Resideo to shift roadmaps and absorb support costs; Matter had over 700 certified devices by mid-2024 and Resideo reported FY2023 revenue of about $4.1 billion, amplifying stakes for interoperability. Clear SDKs, certifications and partner ecosystems increase stickiness, while data portability and privacy assurances build customer trust.

- Open APIs

- Matter/Zigbee/Z-Wave

- Cloud reliability

- SDKs & certifications

- Data portability & privacy

Distributor power, 24–48h fulfillment and >$90B market boost switching risk

Installers and ADI dominance give customers strong leverage—Resideo reported $4.07B net sales in 2024 with ADI ~ $2.5B, making reliability, fill rates and credit terms decisive. Large integrators and builders compress ASPs via multi-year deals; smart-home market >$90B in 2024 raises cross-shopping. Interoperability (700+ Matter devices mid-2024) and 24–48h fulfillment further amplify switching risk.

| Metric | 2024 |

|---|---|

| Resideo net sales | $4.07B |

| ADI contribution | ~$2.5B |

| Smart-home market | >$90B |

| Matter devices | 700+ |

What You See Is What You Get

Resideo Porter's Five Forces Analysis

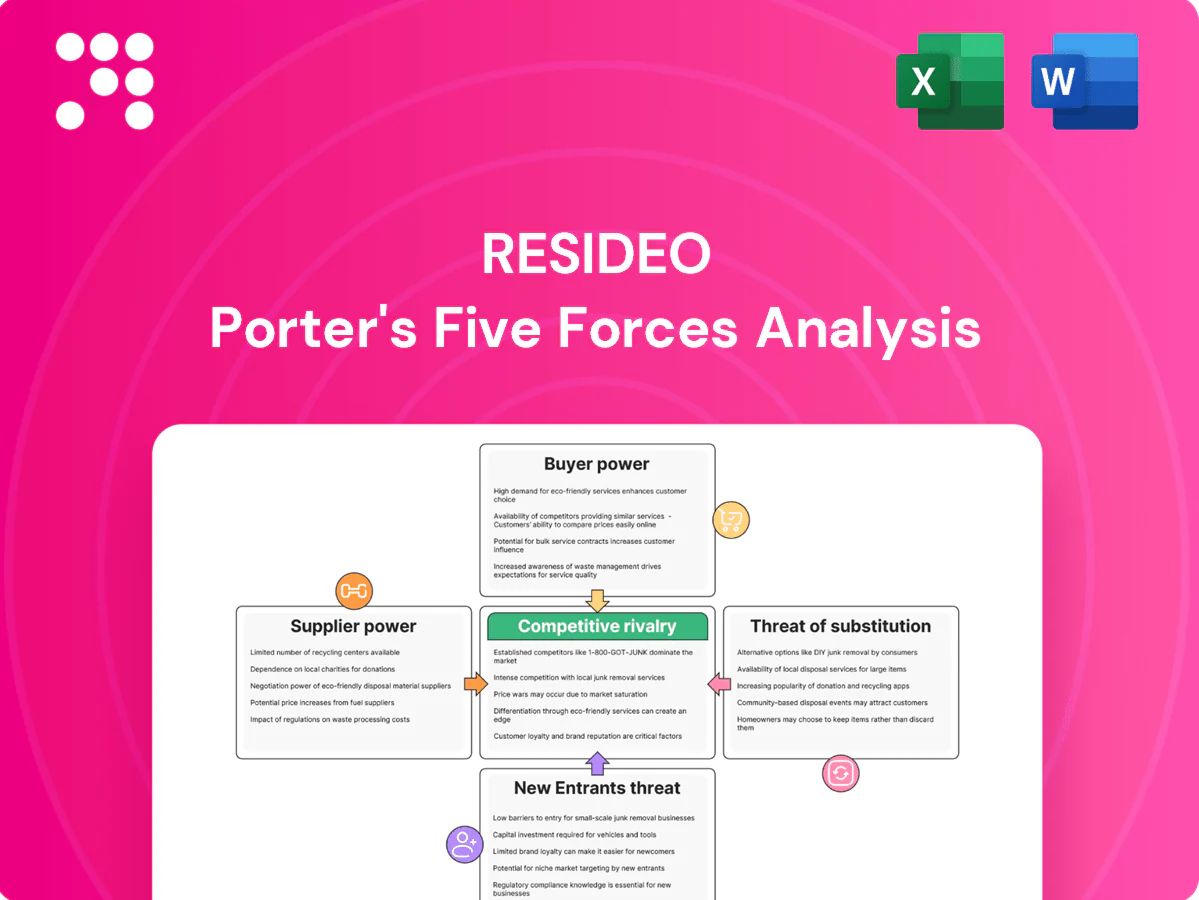

This preview shows the exact Resideo Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups. It covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with actionable insight. The document is fully formatted and ready for download and use the moment you buy.

A Must-Have Tool for Decision-Makers

Resideo faces moderate supplier power, shifting buyer expectations, and rising substitute threats as smart‑home competition intensifies. This snapshot highlights key pressures and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force‑by‑force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Dependence on specialized components

Resideo depends on semiconductors, sensors, radios and ASICs from a narrow vendor set, raising switching costs and lead-time risk; supply shocks or capacity constraints can compress margins and delay delivery. Global semiconductor sales were $583B in 2023 and projected near $600B in 2024, underscoring tight markets. Long-term contracts and dual-sourcing reduce but do not remove concentration; strategic inventory and interchangeable designs help rebalance supplier power.

Contract manufacturing leverage

EMS partners control throughput, yields and hardware line costs, with EMS industry utilization around 88% in H1 2024, giving manufacturers pricing and allocation leverage in tight markets. Volume commitments and utilization allow EMS to extract premiums and priority capacity, pressuring OEM margins. Resideo can rebid programs, multi-source or regionalize supply to reduce exposure while prioritizing quality, IP protection and contractual flexibility.

Software and cloud dependencies

Software and cloud dependencies create vendor lock-in across cloud hosting, mobile OS (Android ~70% global share, iOS ~27%) and core stacks, with hyperscalers (AWS, Azure, GCP) controlling >60% of IaaS market, concentrating risk. API changes or pricing shifts from these platforms can materially raise operating costs. Negotiated enterprise agreements and architecture portability temper that exposure, and building proprietary middleware increases resilience over time.

Branded supplier pull at ADI

ADI distributes leading security, fire and low-voltage brands that installers demand, and tier-one suppliers can still command shelf space, rebates and MDF terms. Resideo reported roughly $5.8 billion in net sales in FY2024, underscoring ADI’s scale which, together with breadth and sell-through data, provides countervailing leverage. Exclusive lines and private-label products further rebalance supplier power.

- Tier-one brand leverage: strong

- Resideo FY2024 net sales: 5.8 billion

- ADI scale & data: offset supplier demands

- Exclusive/private label: reduces supplier power

Standards and certification gatekeepers

Standards bodies (UL, NFPA, FCC) and cybersecurity rules plus protocol consortia strongly steer Resideo component choices; certification often adds 3–12 months and testing fees from roughly $5,000 to >$100,000, raising supplier leverage. Early supplier engagement and use of pre-certified modules can cut approvals to weeks, and active participation in standards groups lets suppliers influence spec direction.

- Certification time: 3–12 months

- Testing fees: ~$5k–$100k+

- Pre-certified modules: approvals in weeks

- Standards participation shapes requirements

Company has concentrated semiconductor, sensor & EMS suppliers; FY24 sales $5.8B

Resideo faces concentrated suppliers for semiconductors, sensors and EMS, elevating switching costs and margin risk. Global semiconductor sales were $583B in 2023 and near $600B in 2024; EMS utilization ~88% in H1 2024. Cloud IaaS >60% market share concentrates platform risk; Resideo FY2024 sales $5.8B help counterbalance supplier leverage.

| Metric | Value |

|---|---|

| Semiconductor sales 2023 | $583B |

| Projection 2024 | ~$600B |

| EMS utilization H1 2024 | ~88% |

| Resideo FY2024 sales | $5.8B |

| IaaS market share | >60% |

What is included in the product

Tailored exclusively for Resideo, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threats from substitutes and new entrants, and identifies disruptive forces and market dynamics shaping pricing, profitability, and barriers protecting incumbents.

A concise Resideo Porter's Five Forces one-sheet that clarifies competitive pressures, lets you customize force levels with current data, and exports cleanly into pitch decks for fast strategic decisions.

Customers Bargaining Power

Professional installers and dealers

Professional installers drive product selection for Resideo; in 2024 Resideo reported $4.07 billion in net sales, with ADI distribution contributing about $2.5 billion, reinforcing installer loyalty. Installers can switch brands if economics or reliability falter, and their sensitivity to failure rates is amplified by truck-roll costs and technical preferences. Training, loyalty programs and Resideo’s integrated ecosystem raise switching costs. ADI’s availability and credit terms further retain dealers.

Large national integrators and builders

Large national integrators and production builders push hard on price and service, often securing multi-year deals that compress margins while stabilizing volume; Resideo reported roughly $4.1B in net sales in FY2024, underscoring how critical scale is to absorb lower ASPs. Value-add services and differentiated features help defend ASPs, while integration support and strict SLAs are frequently decisive in contract awards.

Retail and DIY consumers

Retail and DIY consumers compare smart home devices primarily on price, ease of setup, and app experience, driving high cross-shopping in a global smart home market that surpassed $90 billion in 2024; marketplace transparency increases price sensitivity and churn. Bundles, subscriptions, and proven interoperability materially reduce switching by embedding services. Strong reviews and brand trust in safety categories temper pure price pressure and support premium positioning for players like Resideo (FY2024 revenue ~ $3.2B).

Product availability and lead-time expectations

Customers increasingly demand rapid fulfillment—commonly 24–48 hour delivery for replacements and code-driven installs—making lead times a key driver of bargaining power; stockouts immediately shift projects to competitors with compatible SKUs. ADI’s broad distribution and advanced demand planning materially reduce defections, while accurate ETAs and proposed substitutes protect long-term installer relationships.

- 24–48h fulfillment expectations

- Stockouts => instant defections to compatible SKUs

- ADI network + demand planning mitigate churn

- Accurate ETA & substitutes preserve customer ties

Data and integration demands

Customers demand open APIs, Matter/Zigbee/Z-Wave compatibility and cloud reliability, pressuring Resideo to shift roadmaps and absorb support costs; Matter had over 700 certified devices by mid-2024 and Resideo reported FY2023 revenue of about $4.1 billion, amplifying stakes for interoperability. Clear SDKs, certifications and partner ecosystems increase stickiness, while data portability and privacy assurances build customer trust.

- Open APIs

- Matter/Zigbee/Z-Wave

- Cloud reliability

- SDKs & certifications

- Data portability & privacy

Distributor power, 24–48h fulfillment and >$90B market boost switching risk

Installers and ADI dominance give customers strong leverage—Resideo reported $4.07B net sales in 2024 with ADI ~ $2.5B, making reliability, fill rates and credit terms decisive. Large integrators and builders compress ASPs via multi-year deals; smart-home market >$90B in 2024 raises cross-shopping. Interoperability (700+ Matter devices mid-2024) and 24–48h fulfillment further amplify switching risk.

| Metric | 2024 |

|---|---|

| Resideo net sales | $4.07B |

| ADI contribution | ~$2.5B |

| Smart-home market | >$90B |

| Matter devices | 700+ |

What You See Is What You Get

Resideo Porter's Five Forces Analysis

This preview shows the exact Resideo Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups. It covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with actionable insight. The document is fully formatted and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Resideo faces moderate supplier power, shifting buyer expectations, and rising substitute threats as smart‑home competition intensifies. This snapshot highlights key pressures and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force‑by‑force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Dependence on specialized components

Resideo depends on semiconductors, sensors, radios and ASICs from a narrow vendor set, raising switching costs and lead-time risk; supply shocks or capacity constraints can compress margins and delay delivery. Global semiconductor sales were $583B in 2023 and projected near $600B in 2024, underscoring tight markets. Long-term contracts and dual-sourcing reduce but do not remove concentration; strategic inventory and interchangeable designs help rebalance supplier power.

Contract manufacturing leverage

EMS partners control throughput, yields and hardware line costs, with EMS industry utilization around 88% in H1 2024, giving manufacturers pricing and allocation leverage in tight markets. Volume commitments and utilization allow EMS to extract premiums and priority capacity, pressuring OEM margins. Resideo can rebid programs, multi-source or regionalize supply to reduce exposure while prioritizing quality, IP protection and contractual flexibility.

Software and cloud dependencies

Software and cloud dependencies create vendor lock-in across cloud hosting, mobile OS (Android ~70% global share, iOS ~27%) and core stacks, with hyperscalers (AWS, Azure, GCP) controlling >60% of IaaS market, concentrating risk. API changes or pricing shifts from these platforms can materially raise operating costs. Negotiated enterprise agreements and architecture portability temper that exposure, and building proprietary middleware increases resilience over time.

Branded supplier pull at ADI

ADI distributes leading security, fire and low-voltage brands that installers demand, and tier-one suppliers can still command shelf space, rebates and MDF terms. Resideo reported roughly $5.8 billion in net sales in FY2024, underscoring ADI’s scale which, together with breadth and sell-through data, provides countervailing leverage. Exclusive lines and private-label products further rebalance supplier power.

- Tier-one brand leverage: strong

- Resideo FY2024 net sales: 5.8 billion

- ADI scale & data: offset supplier demands

- Exclusive/private label: reduces supplier power

Standards and certification gatekeepers

Standards bodies (UL, NFPA, FCC) and cybersecurity rules plus protocol consortia strongly steer Resideo component choices; certification often adds 3–12 months and testing fees from roughly $5,000 to >$100,000, raising supplier leverage. Early supplier engagement and use of pre-certified modules can cut approvals to weeks, and active participation in standards groups lets suppliers influence spec direction.

- Certification time: 3–12 months

- Testing fees: ~$5k–$100k+

- Pre-certified modules: approvals in weeks

- Standards participation shapes requirements

Company has concentrated semiconductor, sensor & EMS suppliers; FY24 sales $5.8B

Resideo faces concentrated suppliers for semiconductors, sensors and EMS, elevating switching costs and margin risk. Global semiconductor sales were $583B in 2023 and near $600B in 2024; EMS utilization ~88% in H1 2024. Cloud IaaS >60% market share concentrates platform risk; Resideo FY2024 sales $5.8B help counterbalance supplier leverage.

| Metric | Value |

|---|---|

| Semiconductor sales 2023 | $583B |

| Projection 2024 | ~$600B |

| EMS utilization H1 2024 | ~88% |

| Resideo FY2024 sales | $5.8B |

| IaaS market share | >60% |

What is included in the product

Tailored exclusively for Resideo, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threats from substitutes and new entrants, and identifies disruptive forces and market dynamics shaping pricing, profitability, and barriers protecting incumbents.

A concise Resideo Porter's Five Forces one-sheet that clarifies competitive pressures, lets you customize force levels with current data, and exports cleanly into pitch decks for fast strategic decisions.

Customers Bargaining Power

Professional installers and dealers

Professional installers drive product selection for Resideo; in 2024 Resideo reported $4.07 billion in net sales, with ADI distribution contributing about $2.5 billion, reinforcing installer loyalty. Installers can switch brands if economics or reliability falter, and their sensitivity to failure rates is amplified by truck-roll costs and technical preferences. Training, loyalty programs and Resideo’s integrated ecosystem raise switching costs. ADI’s availability and credit terms further retain dealers.

Large national integrators and builders

Large national integrators and production builders push hard on price and service, often securing multi-year deals that compress margins while stabilizing volume; Resideo reported roughly $4.1B in net sales in FY2024, underscoring how critical scale is to absorb lower ASPs. Value-add services and differentiated features help defend ASPs, while integration support and strict SLAs are frequently decisive in contract awards.

Retail and DIY consumers

Retail and DIY consumers compare smart home devices primarily on price, ease of setup, and app experience, driving high cross-shopping in a global smart home market that surpassed $90 billion in 2024; marketplace transparency increases price sensitivity and churn. Bundles, subscriptions, and proven interoperability materially reduce switching by embedding services. Strong reviews and brand trust in safety categories temper pure price pressure and support premium positioning for players like Resideo (FY2024 revenue ~ $3.2B).

Product availability and lead-time expectations

Customers increasingly demand rapid fulfillment—commonly 24–48 hour delivery for replacements and code-driven installs—making lead times a key driver of bargaining power; stockouts immediately shift projects to competitors with compatible SKUs. ADI’s broad distribution and advanced demand planning materially reduce defections, while accurate ETAs and proposed substitutes protect long-term installer relationships.

- 24–48h fulfillment expectations

- Stockouts => instant defections to compatible SKUs

- ADI network + demand planning mitigate churn

- Accurate ETA & substitutes preserve customer ties

Data and integration demands

Customers demand open APIs, Matter/Zigbee/Z-Wave compatibility and cloud reliability, pressuring Resideo to shift roadmaps and absorb support costs; Matter had over 700 certified devices by mid-2024 and Resideo reported FY2023 revenue of about $4.1 billion, amplifying stakes for interoperability. Clear SDKs, certifications and partner ecosystems increase stickiness, while data portability and privacy assurances build customer trust.

- Open APIs

- Matter/Zigbee/Z-Wave

- Cloud reliability

- SDKs & certifications

- Data portability & privacy

Distributor power, 24–48h fulfillment and >$90B market boost switching risk

Installers and ADI dominance give customers strong leverage—Resideo reported $4.07B net sales in 2024 with ADI ~ $2.5B, making reliability, fill rates and credit terms decisive. Large integrators and builders compress ASPs via multi-year deals; smart-home market >$90B in 2024 raises cross-shopping. Interoperability (700+ Matter devices mid-2024) and 24–48h fulfillment further amplify switching risk.

| Metric | 2024 |

|---|---|

| Resideo net sales | $4.07B |

| ADI contribution | ~$2.5B |

| Smart-home market | >$90B |

| Matter devices | 700+ |

What You See Is What You Get

Resideo Porter's Five Forces Analysis

This preview shows the exact Resideo Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups. It covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with actionable insight. The document is fully formatted and ready for download and use the moment you buy.