ResMed Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

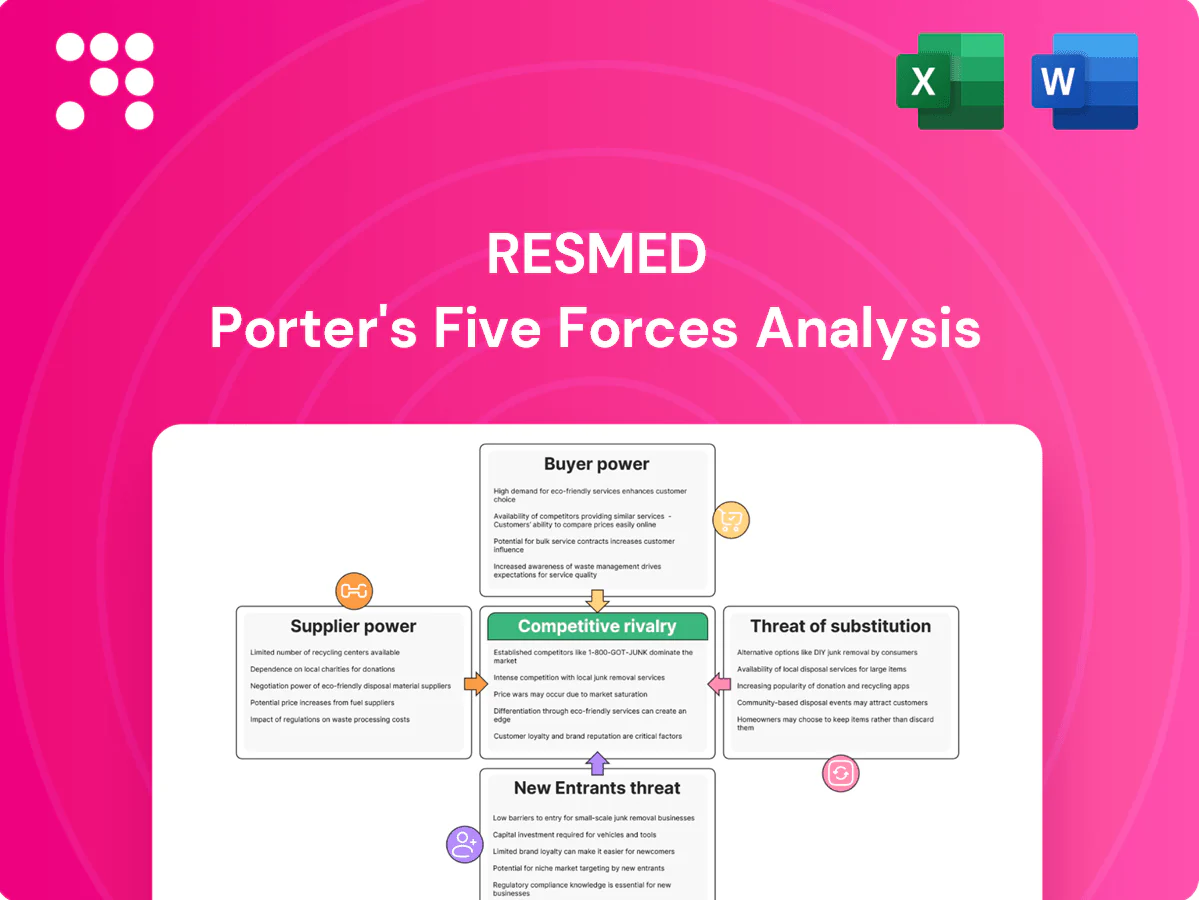

ResMed faces intense rivalry in sleep and respiratory care, moderate supplier power due to specialized components, rising buyer sophistication, and growing substitute threats from digital therapeutics and homecare innovations; regulatory barriers limit new entrants but reimbursement shifts add pressure. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy for ResMed.

Suppliers Bargaining Power

Specialized components concentration

ResMed depends on niche suppliers for blowers, sensors, semiconductors and medical‑grade polymers, concentrating bargaining power among few qualified vendors; this raises switching costs and extends lead times. Supply disruptions can constrain production runs and limit pricing flexibility. Dual‑sourcing and design‑for‑manufacture reduce exposure but do not eliminate supplier concentration risk.

Quality and regulatory requirements

ResMed relies on medical-grade QA and ISO 13485:2016 plus FDA 21 CFR Part 820 compliance, which narrows the supplier pool to those meeting device-quality systems and validated materials.

High compliance costs and limited FDA-compliant material sources increase supplier leverage, while mandatory audits and multi-stage validation cycles lengthen supplier changeovers.

Supplier failures can prompt device recalls and immediate regulatory scrutiny, exposing ResMed to corrective actions and market disruption.

Cloud and software dependencies

Cloud infrastructure and analytics partners create platform lock-in for ResMed, with AWS (≈33%), Azure (≈22%) and GCP (≈11%) dominating IaaS in 2024, raising supplier leverage. Uptime SLAs of 99.95–99.99%, data residency rules and cybersecurity needs heighten vendor importance and patient-data continuity risk. Switching providers is costly and operationally risky; negotiated volume discounts (often 5–15%) partially offset supplier power.

Contract manufacturing flexibility

Contract manufacturing adds surge capacity for ResMed but EMS/ODM partners can gain leverage during tight global supply; ResMed reported approximately US$4.7 billion revenue in fiscal 2024, underscoring heavy manufacturing scale reliance. Tooling, custom firmware, and partner know-how create supplier stickiness, while geographic diversification and long-term volume agreements reduce single-point exposure and price pressure.

- Supply leverage: EMS/ODM can tighten terms during shortages

- Stickiness: tooling + firmware embed partner dependence

- Mitigants: geographic diversification, volume visibility, long-term contracts

Input cost volatility

Input cost volatility: in 2024 resin, electronics and logistics remained cyclical with suppliers able to pass through price spikes during shortages; hedging and larger inventories have cushioned ResMed margins but increased working capital, and design substitutions trigger device revalidation that slows response times.

- Resins, electronics, logistics cyclical in 2024

- Suppliers can pass through costs during shortages

- Hedging/inventory protect margins but tie up working capital

- Design substitutions require revalidation, slowing response

Supplier concentration, cloud reliance and regulatory QA raise switching costs for CPAP makers

ResMed faces concentrated supplier power for blowers, sensors, semiconductors and medical polymers, raising switching costs and lead times; FY2024 revenue ≈ US$4.7B heightens scale dependence. Regulatory QA (ISO 13485, FDA) and cloud/IaaS reliance (AWS 33%, Azure 22%, GCP 11% in 2024) increase vendor leverage; mitigants include dual‑sourcing, long‑term contracts and geographic diversification.

| Metric | 2024 |

|---|---|

| Revenue | US$4.7B |

| AWS/Azure/GCP | 33%/22%/11% |

| Uptime SLA | 99.95–99.99% |

What is included in the product

Tailored Porter's Five Forces analysis for ResMed uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, plus disruptive trends in digital health and home sleep apnea therapy; strategic commentary and industry data highlight pricing pressure, margins, and barriers protecting incumbency for use in investor reports and strategy decks.

A concise ResMed Porter's Five Forces one-sheet highlighting supplier, buyer, substitute, entrant, and competitive rivalry pressures—easy to adjust for evolving healthcare regulations, device innovation, and reimbursement shifts to guide fast strategic decisions.

Customers Bargaining Power

Concentrated institutional buyers

Concentrated buyers—DMEs, hospital systems and sleep-lab networks—negotiate bulk contracts, with GPOs representing the majority of hospital procurement and driving discounts of roughly 5–20%. Large accounts extract rebates and tight service SLAs; ResMed reported FY2024 revenue of about $4.7 billion, so losing a few key contracts can cut double-digit regional share.

Payer and reimbursement influence

Payers shape ResMed demand through coverage rules and rental versus purchase policies, with Medicare CPAP adherence defined as ≥4 hours/night on ≥70% of nights during a consecutive 30‑day period within the first 90 days. Competitive bidding has compressed margins—CMS reported average bid price reductions up to ~40% in some rounds—so maintaining evidence-based outcomes is critical to preserve codes and pricing; tightened adherence rules lower device utilization.

Product differentiation and switching costs

ResMed's mask-fit ecosystems, connected compliance and clinician portals create strong stickiness, reinforced by over 7 million cloud-connected devices reported by 2024. Data continuity and patient familiarity materially reduce switching, as clinicians cite 1–2 hours average setup/training per patient. Standardized interfaces mean competitors can win share if price gaps exceed roughly 15%. Training and ongoing support remain key buyer considerations.

Physician prescribing power

Clinicians largely determine device choice through experience and outcomes, with strong KOL advocacy shown to lift adoption rates materially; recalls (eg, the 2021 Philips CPAP recall) caused >30% rapid shifts in prescription patterns in some centers. Education, telemonitoring and support programs have been associated with ~10–15% higher CPAP adherence, strengthening brand loyalty and countering pure price competition.

- Clinician-driven choice: primary demand driver

- KOL advocacy: increases adoption materially

- Recalls: can shift >30% prescriptions quickly

- Education/support: ~10–15% adherence lift

End-user sensitivity and outcomes

Patients prioritize comfort, noise and aesthetics, driving churn; CPAP adherence averages around 50%, while Medicare requires ≥4 hours/night on 70% of nights for coverage, heightening price sensitivity. Remote monitoring and coaching demonstrably lift adherence and enable value-based pricing; co-pays (Medicare Part B 20% coinsurance) increase price sensitivity. Consumer reviews and telehealth pathways heavily shape brand choice.

- tags: adherence ~50%

- tags: Medicare rule 70% ≥4 hrs

- tags: Medicare coinsurance 20%

- tags: remote monitoring → higher adherence

Concentrated buyers push 5–20% cuts; lost contracts threaten $4.7B revenue

Concentrated buyers (DMEs, GPOs, hospitals) extract 5–20% discounts; ResMed FY2024 revenue ≈ $4.7B so lost contracts can cut double-digit regional share. Payers (Medicare: ≥4 hrs/night on ≥70% nights; 20% coinsurance) and CMS bidding (up to ~40% price cuts) compress pricing. Product stickiness (7M+ cloud devices in 2024) and clinician/KOL influence raise switching costs; price gaps >15% invite churn.

| Metric | 2024 Value | Buyer Impact |

|---|---|---|

| Revenue | $4.7B | High contract risk |

| Connected devices | 7M+ | High retention |

| GPO discounts | 5–20% | Margin pressure |

| CMS bid cuts | Up to ~40% | Price compression |

What You See Is What You Get

ResMed Porter's Five Forces Analysis

This preview shows the exact ResMed Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is the full, professionally formatted analysis covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. Once you buy, you’ll get instant access to this identical, ready-to-use file.

A Must-Have Tool for Decision-Makers

ResMed faces intense rivalry in sleep and respiratory care, moderate supplier power due to specialized components, rising buyer sophistication, and growing substitute threats from digital therapeutics and homecare innovations; regulatory barriers limit new entrants but reimbursement shifts add pressure. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy for ResMed.

Suppliers Bargaining Power

Specialized components concentration

ResMed depends on niche suppliers for blowers, sensors, semiconductors and medical‑grade polymers, concentrating bargaining power among few qualified vendors; this raises switching costs and extends lead times. Supply disruptions can constrain production runs and limit pricing flexibility. Dual‑sourcing and design‑for‑manufacture reduce exposure but do not eliminate supplier concentration risk.

Quality and regulatory requirements

ResMed relies on medical-grade QA and ISO 13485:2016 plus FDA 21 CFR Part 820 compliance, which narrows the supplier pool to those meeting device-quality systems and validated materials.

High compliance costs and limited FDA-compliant material sources increase supplier leverage, while mandatory audits and multi-stage validation cycles lengthen supplier changeovers.

Supplier failures can prompt device recalls and immediate regulatory scrutiny, exposing ResMed to corrective actions and market disruption.

Cloud and software dependencies

Cloud infrastructure and analytics partners create platform lock-in for ResMed, with AWS (≈33%), Azure (≈22%) and GCP (≈11%) dominating IaaS in 2024, raising supplier leverage. Uptime SLAs of 99.95–99.99%, data residency rules and cybersecurity needs heighten vendor importance and patient-data continuity risk. Switching providers is costly and operationally risky; negotiated volume discounts (often 5–15%) partially offset supplier power.

Contract manufacturing flexibility

Contract manufacturing adds surge capacity for ResMed but EMS/ODM partners can gain leverage during tight global supply; ResMed reported approximately US$4.7 billion revenue in fiscal 2024, underscoring heavy manufacturing scale reliance. Tooling, custom firmware, and partner know-how create supplier stickiness, while geographic diversification and long-term volume agreements reduce single-point exposure and price pressure.

- Supply leverage: EMS/ODM can tighten terms during shortages

- Stickiness: tooling + firmware embed partner dependence

- Mitigants: geographic diversification, volume visibility, long-term contracts

Input cost volatility

Input cost volatility: in 2024 resin, electronics and logistics remained cyclical with suppliers able to pass through price spikes during shortages; hedging and larger inventories have cushioned ResMed margins but increased working capital, and design substitutions trigger device revalidation that slows response times.

- Resins, electronics, logistics cyclical in 2024

- Suppliers can pass through costs during shortages

- Hedging/inventory protect margins but tie up working capital

- Design substitutions require revalidation, slowing response

Supplier concentration, cloud reliance and regulatory QA raise switching costs for CPAP makers

ResMed faces concentrated supplier power for blowers, sensors, semiconductors and medical polymers, raising switching costs and lead times; FY2024 revenue ≈ US$4.7B heightens scale dependence. Regulatory QA (ISO 13485, FDA) and cloud/IaaS reliance (AWS 33%, Azure 22%, GCP 11% in 2024) increase vendor leverage; mitigants include dual‑sourcing, long‑term contracts and geographic diversification.

| Metric | 2024 |

|---|---|

| Revenue | US$4.7B |

| AWS/Azure/GCP | 33%/22%/11% |

| Uptime SLA | 99.95–99.99% |

What is included in the product

Tailored Porter's Five Forces analysis for ResMed uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, plus disruptive trends in digital health and home sleep apnea therapy; strategic commentary and industry data highlight pricing pressure, margins, and barriers protecting incumbency for use in investor reports and strategy decks.

A concise ResMed Porter's Five Forces one-sheet highlighting supplier, buyer, substitute, entrant, and competitive rivalry pressures—easy to adjust for evolving healthcare regulations, device innovation, and reimbursement shifts to guide fast strategic decisions.

Customers Bargaining Power

Concentrated institutional buyers

Concentrated buyers—DMEs, hospital systems and sleep-lab networks—negotiate bulk contracts, with GPOs representing the majority of hospital procurement and driving discounts of roughly 5–20%. Large accounts extract rebates and tight service SLAs; ResMed reported FY2024 revenue of about $4.7 billion, so losing a few key contracts can cut double-digit regional share.

Payer and reimbursement influence

Payers shape ResMed demand through coverage rules and rental versus purchase policies, with Medicare CPAP adherence defined as ≥4 hours/night on ≥70% of nights during a consecutive 30‑day period within the first 90 days. Competitive bidding has compressed margins—CMS reported average bid price reductions up to ~40% in some rounds—so maintaining evidence-based outcomes is critical to preserve codes and pricing; tightened adherence rules lower device utilization.

Product differentiation and switching costs

ResMed's mask-fit ecosystems, connected compliance and clinician portals create strong stickiness, reinforced by over 7 million cloud-connected devices reported by 2024. Data continuity and patient familiarity materially reduce switching, as clinicians cite 1–2 hours average setup/training per patient. Standardized interfaces mean competitors can win share if price gaps exceed roughly 15%. Training and ongoing support remain key buyer considerations.

Physician prescribing power

Clinicians largely determine device choice through experience and outcomes, with strong KOL advocacy shown to lift adoption rates materially; recalls (eg, the 2021 Philips CPAP recall) caused >30% rapid shifts in prescription patterns in some centers. Education, telemonitoring and support programs have been associated with ~10–15% higher CPAP adherence, strengthening brand loyalty and countering pure price competition.

- Clinician-driven choice: primary demand driver

- KOL advocacy: increases adoption materially

- Recalls: can shift >30% prescriptions quickly

- Education/support: ~10–15% adherence lift

End-user sensitivity and outcomes

Patients prioritize comfort, noise and aesthetics, driving churn; CPAP adherence averages around 50%, while Medicare requires ≥4 hours/night on 70% of nights for coverage, heightening price sensitivity. Remote monitoring and coaching demonstrably lift adherence and enable value-based pricing; co-pays (Medicare Part B 20% coinsurance) increase price sensitivity. Consumer reviews and telehealth pathways heavily shape brand choice.

- tags: adherence ~50%

- tags: Medicare rule 70% ≥4 hrs

- tags: Medicare coinsurance 20%

- tags: remote monitoring → higher adherence

Concentrated buyers push 5–20% cuts; lost contracts threaten $4.7B revenue

Concentrated buyers (DMEs, GPOs, hospitals) extract 5–20% discounts; ResMed FY2024 revenue ≈ $4.7B so lost contracts can cut double-digit regional share. Payers (Medicare: ≥4 hrs/night on ≥70% nights; 20% coinsurance) and CMS bidding (up to ~40% price cuts) compress pricing. Product stickiness (7M+ cloud devices in 2024) and clinician/KOL influence raise switching costs; price gaps >15% invite churn.

| Metric | 2024 Value | Buyer Impact |

|---|---|---|

| Revenue | $4.7B | High contract risk |

| Connected devices | 7M+ | High retention |

| GPO discounts | 5–20% | Margin pressure |

| CMS bid cuts | Up to ~40% | Price compression |

What You See Is What You Get

ResMed Porter's Five Forces Analysis

This preview shows the exact ResMed Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is the full, professionally formatted analysis covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. Once you buy, you’ll get instant access to this identical, ready-to-use file.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

ResMed faces intense rivalry in sleep and respiratory care, moderate supplier power due to specialized components, rising buyer sophistication, and growing substitute threats from digital therapeutics and homecare innovations; regulatory barriers limit new entrants but reimbursement shifts add pressure. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy for ResMed.

Suppliers Bargaining Power

Specialized components concentration

ResMed depends on niche suppliers for blowers, sensors, semiconductors and medical‑grade polymers, concentrating bargaining power among few qualified vendors; this raises switching costs and extends lead times. Supply disruptions can constrain production runs and limit pricing flexibility. Dual‑sourcing and design‑for‑manufacture reduce exposure but do not eliminate supplier concentration risk.

Quality and regulatory requirements

ResMed relies on medical-grade QA and ISO 13485:2016 plus FDA 21 CFR Part 820 compliance, which narrows the supplier pool to those meeting device-quality systems and validated materials.

High compliance costs and limited FDA-compliant material sources increase supplier leverage, while mandatory audits and multi-stage validation cycles lengthen supplier changeovers.

Supplier failures can prompt device recalls and immediate regulatory scrutiny, exposing ResMed to corrective actions and market disruption.

Cloud and software dependencies

Cloud infrastructure and analytics partners create platform lock-in for ResMed, with AWS (≈33%), Azure (≈22%) and GCP (≈11%) dominating IaaS in 2024, raising supplier leverage. Uptime SLAs of 99.95–99.99%, data residency rules and cybersecurity needs heighten vendor importance and patient-data continuity risk. Switching providers is costly and operationally risky; negotiated volume discounts (often 5–15%) partially offset supplier power.

Contract manufacturing flexibility

Contract manufacturing adds surge capacity for ResMed but EMS/ODM partners can gain leverage during tight global supply; ResMed reported approximately US$4.7 billion revenue in fiscal 2024, underscoring heavy manufacturing scale reliance. Tooling, custom firmware, and partner know-how create supplier stickiness, while geographic diversification and long-term volume agreements reduce single-point exposure and price pressure.

- Supply leverage: EMS/ODM can tighten terms during shortages

- Stickiness: tooling + firmware embed partner dependence

- Mitigants: geographic diversification, volume visibility, long-term contracts

Input cost volatility

Input cost volatility: in 2024 resin, electronics and logistics remained cyclical with suppliers able to pass through price spikes during shortages; hedging and larger inventories have cushioned ResMed margins but increased working capital, and design substitutions trigger device revalidation that slows response times.

- Resins, electronics, logistics cyclical in 2024

- Suppliers can pass through costs during shortages

- Hedging/inventory protect margins but tie up working capital

- Design substitutions require revalidation, slowing response

Supplier concentration, cloud reliance and regulatory QA raise switching costs for CPAP makers

ResMed faces concentrated supplier power for blowers, sensors, semiconductors and medical polymers, raising switching costs and lead times; FY2024 revenue ≈ US$4.7B heightens scale dependence. Regulatory QA (ISO 13485, FDA) and cloud/IaaS reliance (AWS 33%, Azure 22%, GCP 11% in 2024) increase vendor leverage; mitigants include dual‑sourcing, long‑term contracts and geographic diversification.

| Metric | 2024 |

|---|---|

| Revenue | US$4.7B |

| AWS/Azure/GCP | 33%/22%/11% |

| Uptime SLA | 99.95–99.99% |

What is included in the product

Tailored Porter's Five Forces analysis for ResMed uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, plus disruptive trends in digital health and home sleep apnea therapy; strategic commentary and industry data highlight pricing pressure, margins, and barriers protecting incumbency for use in investor reports and strategy decks.

A concise ResMed Porter's Five Forces one-sheet highlighting supplier, buyer, substitute, entrant, and competitive rivalry pressures—easy to adjust for evolving healthcare regulations, device innovation, and reimbursement shifts to guide fast strategic decisions.

Customers Bargaining Power

Concentrated institutional buyers

Concentrated buyers—DMEs, hospital systems and sleep-lab networks—negotiate bulk contracts, with GPOs representing the majority of hospital procurement and driving discounts of roughly 5–20%. Large accounts extract rebates and tight service SLAs; ResMed reported FY2024 revenue of about $4.7 billion, so losing a few key contracts can cut double-digit regional share.

Payer and reimbursement influence

Payers shape ResMed demand through coverage rules and rental versus purchase policies, with Medicare CPAP adherence defined as ≥4 hours/night on ≥70% of nights during a consecutive 30‑day period within the first 90 days. Competitive bidding has compressed margins—CMS reported average bid price reductions up to ~40% in some rounds—so maintaining evidence-based outcomes is critical to preserve codes and pricing; tightened adherence rules lower device utilization.

Product differentiation and switching costs

ResMed's mask-fit ecosystems, connected compliance and clinician portals create strong stickiness, reinforced by over 7 million cloud-connected devices reported by 2024. Data continuity and patient familiarity materially reduce switching, as clinicians cite 1–2 hours average setup/training per patient. Standardized interfaces mean competitors can win share if price gaps exceed roughly 15%. Training and ongoing support remain key buyer considerations.

Physician prescribing power

Clinicians largely determine device choice through experience and outcomes, with strong KOL advocacy shown to lift adoption rates materially; recalls (eg, the 2021 Philips CPAP recall) caused >30% rapid shifts in prescription patterns in some centers. Education, telemonitoring and support programs have been associated with ~10–15% higher CPAP adherence, strengthening brand loyalty and countering pure price competition.

- Clinician-driven choice: primary demand driver

- KOL advocacy: increases adoption materially

- Recalls: can shift >30% prescriptions quickly

- Education/support: ~10–15% adherence lift

End-user sensitivity and outcomes

Patients prioritize comfort, noise and aesthetics, driving churn; CPAP adherence averages around 50%, while Medicare requires ≥4 hours/night on 70% of nights for coverage, heightening price sensitivity. Remote monitoring and coaching demonstrably lift adherence and enable value-based pricing; co-pays (Medicare Part B 20% coinsurance) increase price sensitivity. Consumer reviews and telehealth pathways heavily shape brand choice.

- tags: adherence ~50%

- tags: Medicare rule 70% ≥4 hrs

- tags: Medicare coinsurance 20%

- tags: remote monitoring → higher adherence

Concentrated buyers push 5–20% cuts; lost contracts threaten $4.7B revenue

Concentrated buyers (DMEs, GPOs, hospitals) extract 5–20% discounts; ResMed FY2024 revenue ≈ $4.7B so lost contracts can cut double-digit regional share. Payers (Medicare: ≥4 hrs/night on ≥70% nights; 20% coinsurance) and CMS bidding (up to ~40% price cuts) compress pricing. Product stickiness (7M+ cloud devices in 2024) and clinician/KOL influence raise switching costs; price gaps >15% invite churn.

| Metric | 2024 Value | Buyer Impact |

|---|---|---|

| Revenue | $4.7B | High contract risk |

| Connected devices | 7M+ | High retention |

| GPO discounts | 5–20% | Margin pressure |

| CMS bid cuts | Up to ~40% | Price compression |

What You See Is What You Get

ResMed Porter's Five Forces Analysis

This preview shows the exact ResMed Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is the full, professionally formatted analysis covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. Once you buy, you’ll get instant access to this identical, ready-to-use file.