Resona Holdings Boston Consulting Group Matrix

See the Bigger Picture

Curious where Resona Holdings' businesses sit—Stars, Cash Cows, Dogs or Question Marks? This quick peek hints at risk and opportunity, but the full BCG Matrix gives quadrant-by-quadrant clarity, data-backed moves, and ready-to-use Word and Excel files you can act on fast. Buy the complete report to stop guessing and start reallocating capital with confidence.

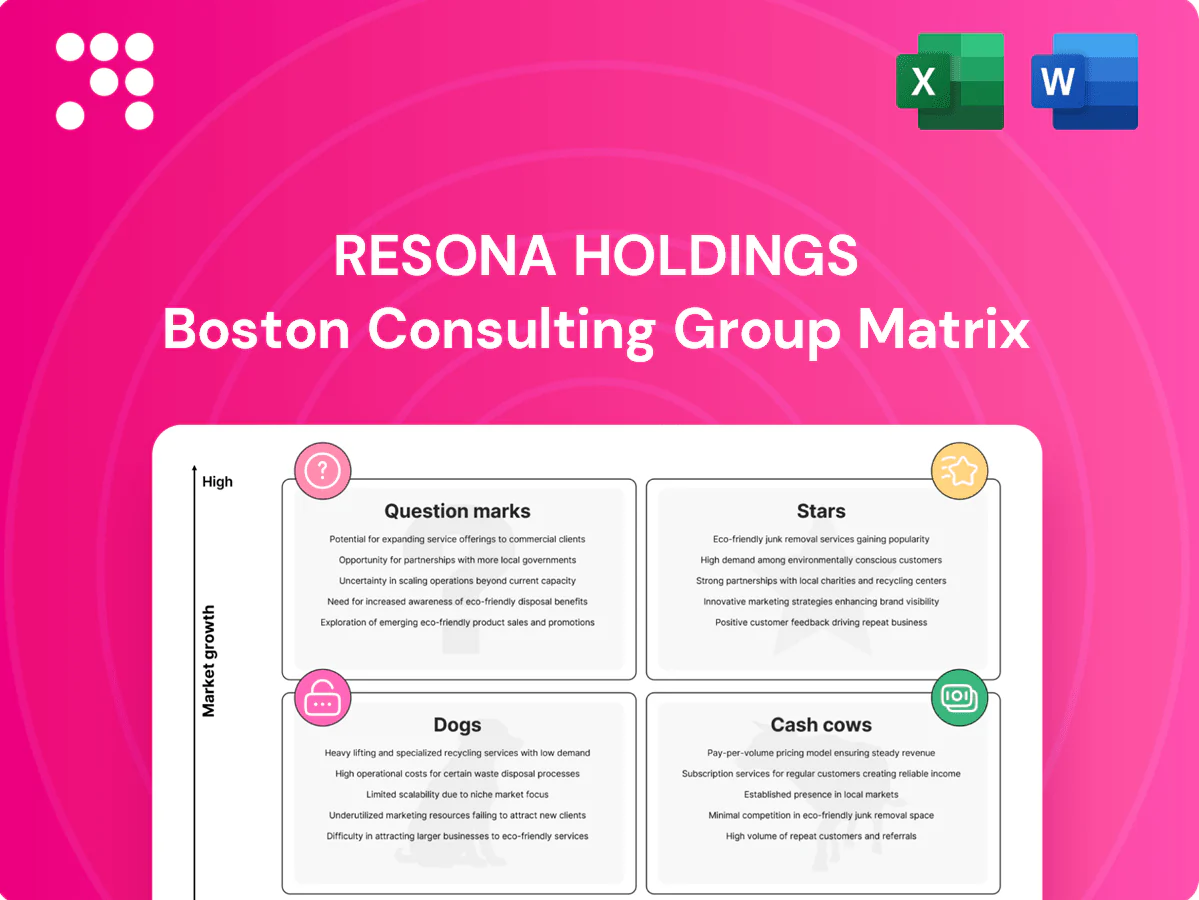

Stars

SME digital lending

Resona’s strong SME footprint (group assets ~¥29 trillion as of FY2024) drives share in SME digital lending, and digitized underwriting—cutting credit decision times to hours—is where growth is emerging. Faster automated approvals win mandates in Saitama and Kansai, translating into rising loan volumes and cross-sell opportunities. Keep investing in the data stack and partner rails to sustain the lead while market demand expands. Done right, the star can evolve into a hybrid fee-and-interest engine.

Green & transition finance

Decarbonization lending is ramping across Japan as the country pursues net-zero by 2050, and early movers are winning marquee transition deals. Resona’s regional corporate base increasingly demands sustainability-linked loans and advisory to meet regulatory and investor pressures. The growing pipeline boosts revenue but soaks up origination talent and risk capacity. Invest now to lock in mandates before pricing normalizes.

Wealth transfer trust solutions

Japan faces an accelerating inheritance wave—about ¥1,000 trillion expected to transfer over the coming decades (2024 estimates) while 65+ now ≈29% of the population—making trust banking a sweet spot. Resona can bundle wills, custody and estate settlement leveraging high share in its Kansai/core territories and rising demand. It needs concentrated marketing and certified planner coverage to scale. Strategy: hold share as the demographic tailwind runs, then harvest.

Embedded SME cash management

Embedded SME cash management—AP/AR, payroll, collections tied into ERP and marketplaces—is accelerating in 2024 as cashless and platform-native flows expand; Resona’s bank rails and local SME relationships create durable stickiness and volume, enabling land-and-expand wins versus national players; keep building integrations as the SME-facing TAM broadens.

- AP/AR integration

- Payroll & collections

- Resona rails = stickiness

- Regional land-and-expand

- TAM expanding in 2024

Retail mobile payments ecosystem

QR and account-to-account payments continue gaining acceptance among merchants and consumers, positioning Resona’s retail mobile payments ecosystem as a Star in the BCG matrix. Resona’s app combined with partner wallets boosts deposit velocity and fee income, but rapid user acquisition requires heavy marketing and incentive spending. Growth remains high; maintain aggressive investment until user density enables unit-economics improvement.

- Market position: Star

- Drivers: app + partner wallets

- P&L drag: marketing & incentives

- Playbook: stay aggressive until scale

SME lending, decarb finance & trusts backed by ¥29T

Resona’s SME digital lending, decarbonization finance, trust services and embedded cash management are Stars driven by group assets ~¥29 trillion (FY2024), rising SME loan volumes and Japan’s ¥1,000 trillion inheritance transfer; demographic 65+ ≈29% (2024) supports trust growth. Maintain heavy investment in data, partnerships and marketing until unit economics improve.

| Metric | 2024 |

|---|---|

| Group assets | ¥29 trillion |

| Inheritance transfer | ¥1,000 trillion |

| Population 65+ | ≈29% |

What is included in the product

Comprehensive BCG Matrix for Resona Holdings: maps Stars, Cash Cows, Question Marks, Dogs with invest/hold/divest guidance and risk notes.

One-page Resona BCG Matrix placing each unit in a quadrant to pinpoint cash cows and pain points fast.

Cash Cows

Core retail deposits

Core retail deposits provide Resona Holdings with stable, low-cost funding—exceeding ¥20 trillion as of FY2024—backed by deep regional loyalty and high market share in Kansai and Kanto. The segment sits in a mature market with predictable flows and minimal promotional spend required to maintain balances. These deposits act as cash cows, reliably supporting NIM and funding selective growth bets.

Residential mortgages

Resona’s residential mortgage cash cow features a large book—about ¥15 trillion retail mortgage balance in 2024—with seasoned underwriting and a steady prepayment rate near 3% annually, supporting predictable cash flows.

Transaction banking for SMEs

Transaction banking for SMEs—accounts, transfers, payroll, collections—captures everyday cash flows and yields high-retention, recurring fees supporting stable non-interest income. SMEs constitute 99.7% of Japanese firms and employ roughly 70% of the workforce, underpinning steady demand despite modest market growth. Resona’s regional footprint anchors share in this low-growth segment, while streamlined operations and automation offer clear levers to lift margins further.

Custody & basic trust services

Custody and basic trust services—pensions, safekeeping, and vanilla trustee mandates—exhibit high client stickiness with low churn, delivering predictable fee income despite limited organic growth.

Scale advantages and low onboarding sales intensity support solid profitability, enabling Resona to recycle steady cash flows to fund higher-growth trust innovations and digital custody pilots.

- sticky mandates

- low single-digit growth

- high margin via scale

- reinvest proceeds into innovation

ATM and branch cash services

ATM and branch cash services remain Resona’s cash cows: usage is drifting down as customers migrate to digital, but the network continues to generate steady fee income and float from deposits in core-city hubs with high market share, requiring low incremental investment and limited capex to sustain.

- High urban share

- Declining transactions

- Low incremental investment

- Optimize footprint, dont expand

- Milk while digital migration continues

Core deposits > ¥20T, mortgages ~¥15T underpin stable NII

Core deposits (>¥20T FY2024) and retail mortgages (~¥15T, 3% prepay) deliver stable NII; SME transaction banking (SMEs 99.7% of firms, ~70% workforce) and custody/trust fees provide recurring non‑interest income. ATM/branch float remains low‑capex cash cow while digital migration lowers volumes but not profitability; scale funds innovation.

| Metric | FY2024 |

|---|---|

| Core deposits | ¥20T+ |

| Retail mortgages | ¥15T |

| Mortgage prepay | ~3% p.a. |

Delivered as Shown

Resona Holdings BCG Matrix

The file you're previewing is the exact BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, analysis-ready report designed for strategic clarity. After purchase you get the same file immediately, ready to edit, print, or present to stakeholders. It's the real deal, crafted by strategy pros.

See the Bigger Picture

Curious where Resona Holdings' businesses sit—Stars, Cash Cows, Dogs or Question Marks? This quick peek hints at risk and opportunity, but the full BCG Matrix gives quadrant-by-quadrant clarity, data-backed moves, and ready-to-use Word and Excel files you can act on fast. Buy the complete report to stop guessing and start reallocating capital with confidence.

Stars

SME digital lending

Resona’s strong SME footprint (group assets ~¥29 trillion as of FY2024) drives share in SME digital lending, and digitized underwriting—cutting credit decision times to hours—is where growth is emerging. Faster automated approvals win mandates in Saitama and Kansai, translating into rising loan volumes and cross-sell opportunities. Keep investing in the data stack and partner rails to sustain the lead while market demand expands. Done right, the star can evolve into a hybrid fee-and-interest engine.

Green & transition finance

Decarbonization lending is ramping across Japan as the country pursues net-zero by 2050, and early movers are winning marquee transition deals. Resona’s regional corporate base increasingly demands sustainability-linked loans and advisory to meet regulatory and investor pressures. The growing pipeline boosts revenue but soaks up origination talent and risk capacity. Invest now to lock in mandates before pricing normalizes.

Wealth transfer trust solutions

Japan faces an accelerating inheritance wave—about ¥1,000 trillion expected to transfer over the coming decades (2024 estimates) while 65+ now ≈29% of the population—making trust banking a sweet spot. Resona can bundle wills, custody and estate settlement leveraging high share in its Kansai/core territories and rising demand. It needs concentrated marketing and certified planner coverage to scale. Strategy: hold share as the demographic tailwind runs, then harvest.

Embedded SME cash management

Embedded SME cash management—AP/AR, payroll, collections tied into ERP and marketplaces—is accelerating in 2024 as cashless and platform-native flows expand; Resona’s bank rails and local SME relationships create durable stickiness and volume, enabling land-and-expand wins versus national players; keep building integrations as the SME-facing TAM broadens.

- AP/AR integration

- Payroll & collections

- Resona rails = stickiness

- Regional land-and-expand

- TAM expanding in 2024

Retail mobile payments ecosystem

QR and account-to-account payments continue gaining acceptance among merchants and consumers, positioning Resona’s retail mobile payments ecosystem as a Star in the BCG matrix. Resona’s app combined with partner wallets boosts deposit velocity and fee income, but rapid user acquisition requires heavy marketing and incentive spending. Growth remains high; maintain aggressive investment until user density enables unit-economics improvement.

- Market position: Star

- Drivers: app + partner wallets

- P&L drag: marketing & incentives

- Playbook: stay aggressive until scale

SME lending, decarb finance & trusts backed by ¥29T

Resona’s SME digital lending, decarbonization finance, trust services and embedded cash management are Stars driven by group assets ~¥29 trillion (FY2024), rising SME loan volumes and Japan’s ¥1,000 trillion inheritance transfer; demographic 65+ ≈29% (2024) supports trust growth. Maintain heavy investment in data, partnerships and marketing until unit economics improve.

| Metric | 2024 |

|---|---|

| Group assets | ¥29 trillion |

| Inheritance transfer | ¥1,000 trillion |

| Population 65+ | ≈29% |

What is included in the product

Comprehensive BCG Matrix for Resona Holdings: maps Stars, Cash Cows, Question Marks, Dogs with invest/hold/divest guidance and risk notes.

One-page Resona BCG Matrix placing each unit in a quadrant to pinpoint cash cows and pain points fast.

Cash Cows

Core retail deposits

Core retail deposits provide Resona Holdings with stable, low-cost funding—exceeding ¥20 trillion as of FY2024—backed by deep regional loyalty and high market share in Kansai and Kanto. The segment sits in a mature market with predictable flows and minimal promotional spend required to maintain balances. These deposits act as cash cows, reliably supporting NIM and funding selective growth bets.

Residential mortgages

Resona’s residential mortgage cash cow features a large book—about ¥15 trillion retail mortgage balance in 2024—with seasoned underwriting and a steady prepayment rate near 3% annually, supporting predictable cash flows.

Transaction banking for SMEs

Transaction banking for SMEs—accounts, transfers, payroll, collections—captures everyday cash flows and yields high-retention, recurring fees supporting stable non-interest income. SMEs constitute 99.7% of Japanese firms and employ roughly 70% of the workforce, underpinning steady demand despite modest market growth. Resona’s regional footprint anchors share in this low-growth segment, while streamlined operations and automation offer clear levers to lift margins further.

Custody & basic trust services

Custody and basic trust services—pensions, safekeeping, and vanilla trustee mandates—exhibit high client stickiness with low churn, delivering predictable fee income despite limited organic growth.

Scale advantages and low onboarding sales intensity support solid profitability, enabling Resona to recycle steady cash flows to fund higher-growth trust innovations and digital custody pilots.

- sticky mandates

- low single-digit growth

- high margin via scale

- reinvest proceeds into innovation

ATM and branch cash services

ATM and branch cash services remain Resona’s cash cows: usage is drifting down as customers migrate to digital, but the network continues to generate steady fee income and float from deposits in core-city hubs with high market share, requiring low incremental investment and limited capex to sustain.

- High urban share

- Declining transactions

- Low incremental investment

- Optimize footprint, dont expand

- Milk while digital migration continues

Core deposits > ¥20T, mortgages ~¥15T underpin stable NII

Core deposits (>¥20T FY2024) and retail mortgages (~¥15T, 3% prepay) deliver stable NII; SME transaction banking (SMEs 99.7% of firms, ~70% workforce) and custody/trust fees provide recurring non‑interest income. ATM/branch float remains low‑capex cash cow while digital migration lowers volumes but not profitability; scale funds innovation.

| Metric | FY2024 |

|---|---|

| Core deposits | ¥20T+ |

| Retail mortgages | ¥15T |

| Mortgage prepay | ~3% p.a. |

Delivered as Shown

Resona Holdings BCG Matrix

The file you're previewing is the exact BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, analysis-ready report designed for strategic clarity. After purchase you get the same file immediately, ready to edit, print, or present to stakeholders. It's the real deal, crafted by strategy pros.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

Curious where Resona Holdings' businesses sit—Stars, Cash Cows, Dogs or Question Marks? This quick peek hints at risk and opportunity, but the full BCG Matrix gives quadrant-by-quadrant clarity, data-backed moves, and ready-to-use Word and Excel files you can act on fast. Buy the complete report to stop guessing and start reallocating capital with confidence.

Stars

SME digital lending

Resona’s strong SME footprint (group assets ~¥29 trillion as of FY2024) drives share in SME digital lending, and digitized underwriting—cutting credit decision times to hours—is where growth is emerging. Faster automated approvals win mandates in Saitama and Kansai, translating into rising loan volumes and cross-sell opportunities. Keep investing in the data stack and partner rails to sustain the lead while market demand expands. Done right, the star can evolve into a hybrid fee-and-interest engine.

Green & transition finance

Decarbonization lending is ramping across Japan as the country pursues net-zero by 2050, and early movers are winning marquee transition deals. Resona’s regional corporate base increasingly demands sustainability-linked loans and advisory to meet regulatory and investor pressures. The growing pipeline boosts revenue but soaks up origination talent and risk capacity. Invest now to lock in mandates before pricing normalizes.

Wealth transfer trust solutions

Japan faces an accelerating inheritance wave—about ¥1,000 trillion expected to transfer over the coming decades (2024 estimates) while 65+ now ≈29% of the population—making trust banking a sweet spot. Resona can bundle wills, custody and estate settlement leveraging high share in its Kansai/core territories and rising demand. It needs concentrated marketing and certified planner coverage to scale. Strategy: hold share as the demographic tailwind runs, then harvest.

Embedded SME cash management

Embedded SME cash management—AP/AR, payroll, collections tied into ERP and marketplaces—is accelerating in 2024 as cashless and platform-native flows expand; Resona’s bank rails and local SME relationships create durable stickiness and volume, enabling land-and-expand wins versus national players; keep building integrations as the SME-facing TAM broadens.

- AP/AR integration

- Payroll & collections

- Resona rails = stickiness

- Regional land-and-expand

- TAM expanding in 2024

Retail mobile payments ecosystem

QR and account-to-account payments continue gaining acceptance among merchants and consumers, positioning Resona’s retail mobile payments ecosystem as a Star in the BCG matrix. Resona’s app combined with partner wallets boosts deposit velocity and fee income, but rapid user acquisition requires heavy marketing and incentive spending. Growth remains high; maintain aggressive investment until user density enables unit-economics improvement.

- Market position: Star

- Drivers: app + partner wallets

- P&L drag: marketing & incentives

- Playbook: stay aggressive until scale

SME lending, decarb finance & trusts backed by ¥29T

Resona’s SME digital lending, decarbonization finance, trust services and embedded cash management are Stars driven by group assets ~¥29 trillion (FY2024), rising SME loan volumes and Japan’s ¥1,000 trillion inheritance transfer; demographic 65+ ≈29% (2024) supports trust growth. Maintain heavy investment in data, partnerships and marketing until unit economics improve.

| Metric | 2024 |

|---|---|

| Group assets | ¥29 trillion |

| Inheritance transfer | ¥1,000 trillion |

| Population 65+ | ≈29% |

What is included in the product

Comprehensive BCG Matrix for Resona Holdings: maps Stars, Cash Cows, Question Marks, Dogs with invest/hold/divest guidance and risk notes.

One-page Resona BCG Matrix placing each unit in a quadrant to pinpoint cash cows and pain points fast.

Cash Cows

Core retail deposits

Core retail deposits provide Resona Holdings with stable, low-cost funding—exceeding ¥20 trillion as of FY2024—backed by deep regional loyalty and high market share in Kansai and Kanto. The segment sits in a mature market with predictable flows and minimal promotional spend required to maintain balances. These deposits act as cash cows, reliably supporting NIM and funding selective growth bets.

Residential mortgages

Resona’s residential mortgage cash cow features a large book—about ¥15 trillion retail mortgage balance in 2024—with seasoned underwriting and a steady prepayment rate near 3% annually, supporting predictable cash flows.

Transaction banking for SMEs

Transaction banking for SMEs—accounts, transfers, payroll, collections—captures everyday cash flows and yields high-retention, recurring fees supporting stable non-interest income. SMEs constitute 99.7% of Japanese firms and employ roughly 70% of the workforce, underpinning steady demand despite modest market growth. Resona’s regional footprint anchors share in this low-growth segment, while streamlined operations and automation offer clear levers to lift margins further.

Custody & basic trust services

Custody and basic trust services—pensions, safekeeping, and vanilla trustee mandates—exhibit high client stickiness with low churn, delivering predictable fee income despite limited organic growth.

Scale advantages and low onboarding sales intensity support solid profitability, enabling Resona to recycle steady cash flows to fund higher-growth trust innovations and digital custody pilots.

- sticky mandates

- low single-digit growth

- high margin via scale

- reinvest proceeds into innovation

ATM and branch cash services

ATM and branch cash services remain Resona’s cash cows: usage is drifting down as customers migrate to digital, but the network continues to generate steady fee income and float from deposits in core-city hubs with high market share, requiring low incremental investment and limited capex to sustain.

- High urban share

- Declining transactions

- Low incremental investment

- Optimize footprint, dont expand

- Milk while digital migration continues

Core deposits > ¥20T, mortgages ~¥15T underpin stable NII

Core deposits (>¥20T FY2024) and retail mortgages (~¥15T, 3% prepay) deliver stable NII; SME transaction banking (SMEs 99.7% of firms, ~70% workforce) and custody/trust fees provide recurring non‑interest income. ATM/branch float remains low‑capex cash cow while digital migration lowers volumes but not profitability; scale funds innovation.

| Metric | FY2024 |

|---|---|

| Core deposits | ¥20T+ |

| Retail mortgages | ¥15T |

| Mortgage prepay | ~3% p.a. |

Delivered as Shown

Resona Holdings BCG Matrix

The file you're previewing is the exact BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, analysis-ready report designed for strategic clarity. After purchase you get the same file immediately, ready to edit, print, or present to stakeholders. It's the real deal, crafted by strategy pros.