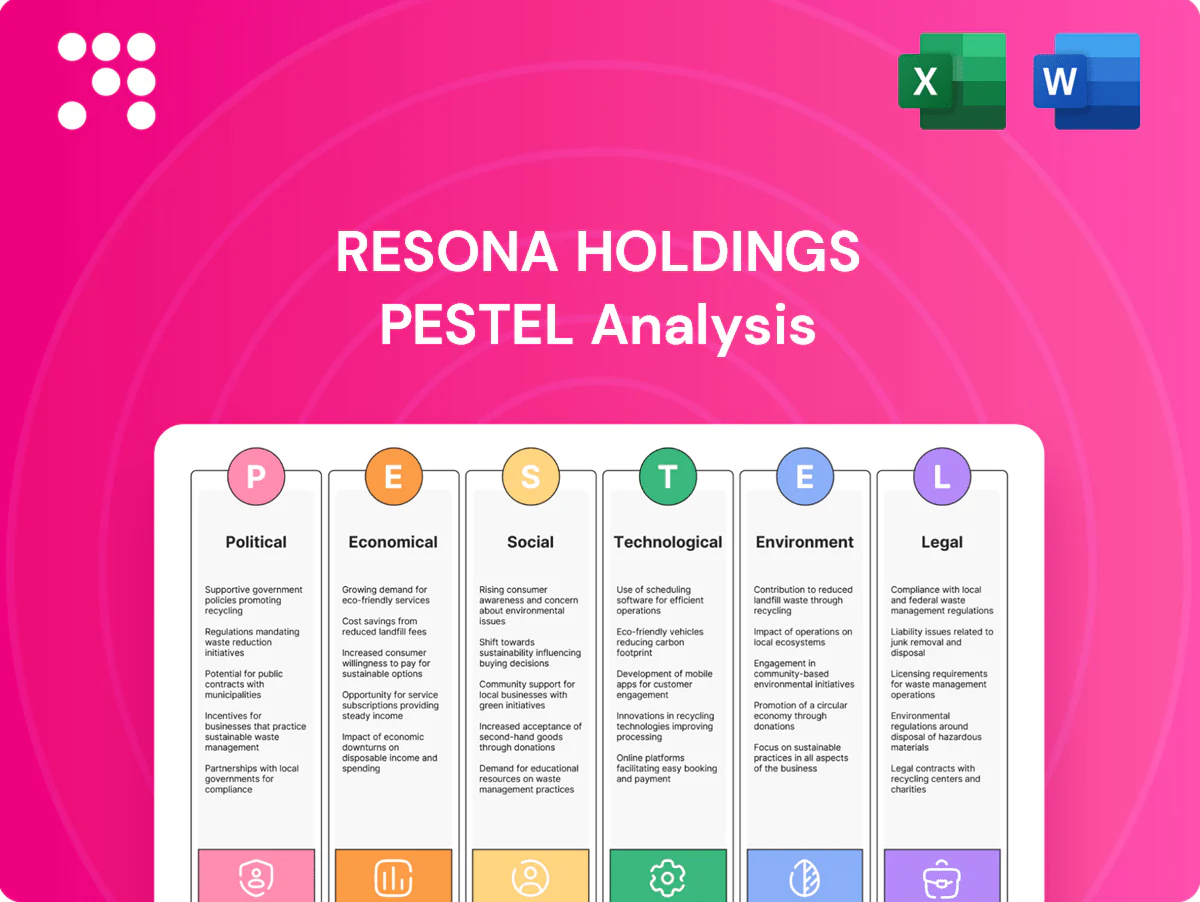

Resona Holdings PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, economic trends, and technological change are reshaping Resona Holdings with our concise PESTLE analysis—designed to inform investment and strategic decisions. This expert-ready brief highlights key risks and opportunities; buy the full PESTLE for a detailed, actionable breakdown you can use in minutes. Download now to turn external insights into competitive advantage.

Political factors

Policy continuity and fiscal stance

Japan’s relatively stable policymaking and pro-growth fiscal measures, including a ¥26.7 trillion supplementary package in 2023–24, support credit conditions, public investment and consumer confidence. A supportive stance can boost loan demand among SMEs and households, while fiscal consolidation risks dampening spending and raising credit risk. Resona must align portfolio and lending strategy with evolving budget priorities and subsidy shifts amid Japan’s ~260% general government debt/GDP backdrop.

Local government ties and regional policy

Resona Holdings (ticker 8308) and its core banks Resona Bank and Saitama Resona Bank interface closely with prefectural and municipal programs. Regional revitalization, tourism promotion and SME subsidy schemes feed loan pipelines and fee income and support deposits and project finance. Strong public-sector relationships bolster trust business, while policy shifts or leadership turnover can quickly change funding flows and collaboration.

Geopolitics and market stability

Global tensions drive yen volatility and dent equity risk appetite, pressuring SME credit via trade frictions and supply‑chain shifts; flight‑to‑safety has shifted deposits into low‑risk assets and JGBs (10y ~0.6% in 2024). Resona must maintain hedges and conservative liquidity buffers, including regulatory LCR above 100%, to withstand geopolitical shocks.

Corporate governance reforms

Japan’s Stewardship Code (revised 2020) and Corporate Governance Code (updated 2021) push banks toward higher capital efficiency and transparency, prompting Resona to prioritize ROE and streamline cross-shareholdings as investor scrutiny intensified in 2024.

- capital efficiency: ROE focus

- cross-shareholdings: optimization pressure

- board/disclosure: increased independence and reporting

- benefit: attract investors, potentially lower funding costs

Digital yen and public-sector digitization

Government-led digital transformation and the Bank of Japan CBDC experiments, initiated in 2021, could materially reshape payments and settlement rails, reducing reliance on cash and accelerating real-time settlement for Resona. Public infrastructure upgrades will lower cash-handling costs and shorten settlement cycles, while policy timelines will dictate Resona’s IT investment and interoperability roadmaps. Early adaptation can lock in transaction flows and ecosystem partnerships.

- Digital Agency est. 2021; BoJ CBDC work began 2021

- Policy drives IT spend timing and interoperability mandates

- Early movers capture payment volumes and partnerships

Fiscal stimulus ¥26.7tn boosts lending; public debt ~260% raises sovereign risk

Stable pro-growth fiscal moves (¥26.7tn sup. 2023–24) support loan demand but fiscal consolidation risk exists. High public debt (~260% of GDP) raises long-term sovereign risk. Geopolitical-driven yen/JGB moves (10y ~0.6% in 2024) pressure liquidity and credit. Governance rules push ROE/capital efficiency and faster digital/IT rollout.

| Metric | Value |

|---|---|

| Supplementary budget | ¥26.7tn (2023–24) |

| Debt/GDP | ~260% |

| JGB 10y | ~0.6% (2024) |

| LCR | >100% regulatory |

What is included in the product

Explores how external macro-environmental factors uniquely affect Resona Holdings across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, consultants and investors, the analysis offers detailed sub-points, forward-looking scenario insights and ready-to-insert formatting to identify risks, opportunities and strategic responses.

A concise, visually segmented PESTLE summary for Resona Holdings that relieves briefing pain points by enabling quick interpretation, easy edits for local context, and drop‑in use for presentations or team alignment.

Economic factors

BoJ policy normalization and rates

BoJ policy normalization from -0.1% toward positive territory and a rise in 10‑yr JGB yields (around 0.9% in 2024) has widened bank NIMs but marked down bond portfolios, raising unrealized losses for regional banks. Gradual rate hikes can boost Resona’s loan margins as loan repricing accelerates, yet funding costs and deposit betas will pressure short‑term gains. Resona must tighten ALM and expand hedging to balance rate risk and protect earnings.

Inflation and wage dynamics

Sustained wage gains—scheduled cash earnings rose about 3.6% in 2024—support household consumption and SME revenues, underpinning credit demand for Resona. Core CPI ran near 3.0% y/y in 2024, lifting nominal activity but tightening real affordability for some segments. Credit underwriting must track real income and price pass-through trends; pricing discipline and fee diversification help offset margin volatility.

SME health and credit demand

Resona’s SME-heavy loan book is vulnerable to input-cost swings and export cycles in a market where SMEs comprise 99.7% of Japanese firms and employ roughly 70% of workers (METI). Government credit guarantees and refinancing facilities (expanded since 2020) materially affect risk-adjusted returns. Tight labour markets with unemployment around 2.5% (2024) and rising capex plans lift working-capital drawdowns. Proactive advisory and covenant monitoring have helped keep bank NPLs low.

Housing and real estate cycle

Competition and consolidation

Competition and consolidation: three megabanks (MUFG, SMBC, Mizuho) and ongoing regional bank mergers intensify pressure on Resona, while fintechs compress pricing and fee income through digital channels.

Scale advantages in tech and compliance among larger players widen cost gaps and raise barriers to profitability for midsized banks; consolidation is reshaping local market shares and collaboration opportunities.

Resona must sharpen segment focus and accelerate cross-sell to protect margins and customer share.

- Megabanks: MUFG, SMBC, Mizuho

- Trend: regional bank consolidation ongoing

- Threat: fintechs press pricing and fees

- Response: sharpen segmentation; boost cross-sell

Fiscal stimulus ¥26.7tn boosts lending; public debt ~260% raises sovereign risk

BoJ normalization and 10‑yr JGB ~0.9% (2024) widened NIMs but raised unrealized losses; gradual hikes aid loan repricing while lifting funding costs. Scheduled cash earnings +3.6% (2024) and core CPI ~3.0% (2024) support demand but squeeze real affordability. SME exposure (99.7% of firms) and unemployment ~2.5% (2024) shape credit risk and working‑capex flows. Tight ALM, hedging, fee diversification and strict LTVs required.

| Metric | Value |

|---|---|

| 10‑yr JGB (2024) | ~0.9% |

| Core CPI (2024) | ~3.0% y/y |

| Scheduled cash earnings (2024) | +3.6% |

| Unemployment (2024) | ~2.5% |

| Population (2023) | ~124.6M |

Full Version Awaits

Resona Holdings PESTLE Analysis

The Resona Holdings PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content and structure visible in this preview are identical to the final file you’ll download immediately after payment. No placeholders or teasers—this is the real, professionally structured analysis you’ll own upon checkout.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, economic trends, and technological change are reshaping Resona Holdings with our concise PESTLE analysis—designed to inform investment and strategic decisions. This expert-ready brief highlights key risks and opportunities; buy the full PESTLE for a detailed, actionable breakdown you can use in minutes. Download now to turn external insights into competitive advantage.

Political factors

Policy continuity and fiscal stance

Japan’s relatively stable policymaking and pro-growth fiscal measures, including a ¥26.7 trillion supplementary package in 2023–24, support credit conditions, public investment and consumer confidence. A supportive stance can boost loan demand among SMEs and households, while fiscal consolidation risks dampening spending and raising credit risk. Resona must align portfolio and lending strategy with evolving budget priorities and subsidy shifts amid Japan’s ~260% general government debt/GDP backdrop.

Local government ties and regional policy

Resona Holdings (ticker 8308) and its core banks Resona Bank and Saitama Resona Bank interface closely with prefectural and municipal programs. Regional revitalization, tourism promotion and SME subsidy schemes feed loan pipelines and fee income and support deposits and project finance. Strong public-sector relationships bolster trust business, while policy shifts or leadership turnover can quickly change funding flows and collaboration.

Geopolitics and market stability

Global tensions drive yen volatility and dent equity risk appetite, pressuring SME credit via trade frictions and supply‑chain shifts; flight‑to‑safety has shifted deposits into low‑risk assets and JGBs (10y ~0.6% in 2024). Resona must maintain hedges and conservative liquidity buffers, including regulatory LCR above 100%, to withstand geopolitical shocks.

Corporate governance reforms

Japan’s Stewardship Code (revised 2020) and Corporate Governance Code (updated 2021) push banks toward higher capital efficiency and transparency, prompting Resona to prioritize ROE and streamline cross-shareholdings as investor scrutiny intensified in 2024.

- capital efficiency: ROE focus

- cross-shareholdings: optimization pressure

- board/disclosure: increased independence and reporting

- benefit: attract investors, potentially lower funding costs

Digital yen and public-sector digitization

Government-led digital transformation and the Bank of Japan CBDC experiments, initiated in 2021, could materially reshape payments and settlement rails, reducing reliance on cash and accelerating real-time settlement for Resona. Public infrastructure upgrades will lower cash-handling costs and shorten settlement cycles, while policy timelines will dictate Resona’s IT investment and interoperability roadmaps. Early adaptation can lock in transaction flows and ecosystem partnerships.

- Digital Agency est. 2021; BoJ CBDC work began 2021

- Policy drives IT spend timing and interoperability mandates

- Early movers capture payment volumes and partnerships

Fiscal stimulus ¥26.7tn boosts lending; public debt ~260% raises sovereign risk

Stable pro-growth fiscal moves (¥26.7tn sup. 2023–24) support loan demand but fiscal consolidation risk exists. High public debt (~260% of GDP) raises long-term sovereign risk. Geopolitical-driven yen/JGB moves (10y ~0.6% in 2024) pressure liquidity and credit. Governance rules push ROE/capital efficiency and faster digital/IT rollout.

| Metric | Value |

|---|---|

| Supplementary budget | ¥26.7tn (2023–24) |

| Debt/GDP | ~260% |

| JGB 10y | ~0.6% (2024) |

| LCR | >100% regulatory |

What is included in the product

Explores how external macro-environmental factors uniquely affect Resona Holdings across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, consultants and investors, the analysis offers detailed sub-points, forward-looking scenario insights and ready-to-insert formatting to identify risks, opportunities and strategic responses.

A concise, visually segmented PESTLE summary for Resona Holdings that relieves briefing pain points by enabling quick interpretation, easy edits for local context, and drop‑in use for presentations or team alignment.

Economic factors

BoJ policy normalization and rates

BoJ policy normalization from -0.1% toward positive territory and a rise in 10‑yr JGB yields (around 0.9% in 2024) has widened bank NIMs but marked down bond portfolios, raising unrealized losses for regional banks. Gradual rate hikes can boost Resona’s loan margins as loan repricing accelerates, yet funding costs and deposit betas will pressure short‑term gains. Resona must tighten ALM and expand hedging to balance rate risk and protect earnings.

Inflation and wage dynamics

Sustained wage gains—scheduled cash earnings rose about 3.6% in 2024—support household consumption and SME revenues, underpinning credit demand for Resona. Core CPI ran near 3.0% y/y in 2024, lifting nominal activity but tightening real affordability for some segments. Credit underwriting must track real income and price pass-through trends; pricing discipline and fee diversification help offset margin volatility.

SME health and credit demand

Resona’s SME-heavy loan book is vulnerable to input-cost swings and export cycles in a market where SMEs comprise 99.7% of Japanese firms and employ roughly 70% of workers (METI). Government credit guarantees and refinancing facilities (expanded since 2020) materially affect risk-adjusted returns. Tight labour markets with unemployment around 2.5% (2024) and rising capex plans lift working-capital drawdowns. Proactive advisory and covenant monitoring have helped keep bank NPLs low.

Housing and real estate cycle

Competition and consolidation

Competition and consolidation: three megabanks (MUFG, SMBC, Mizuho) and ongoing regional bank mergers intensify pressure on Resona, while fintechs compress pricing and fee income through digital channels.

Scale advantages in tech and compliance among larger players widen cost gaps and raise barriers to profitability for midsized banks; consolidation is reshaping local market shares and collaboration opportunities.

Resona must sharpen segment focus and accelerate cross-sell to protect margins and customer share.

- Megabanks: MUFG, SMBC, Mizuho

- Trend: regional bank consolidation ongoing

- Threat: fintechs press pricing and fees

- Response: sharpen segmentation; boost cross-sell

Fiscal stimulus ¥26.7tn boosts lending; public debt ~260% raises sovereign risk

BoJ normalization and 10‑yr JGB ~0.9% (2024) widened NIMs but raised unrealized losses; gradual hikes aid loan repricing while lifting funding costs. Scheduled cash earnings +3.6% (2024) and core CPI ~3.0% (2024) support demand but squeeze real affordability. SME exposure (99.7% of firms) and unemployment ~2.5% (2024) shape credit risk and working‑capex flows. Tight ALM, hedging, fee diversification and strict LTVs required.

| Metric | Value |

|---|---|

| 10‑yr JGB (2024) | ~0.9% |

| Core CPI (2024) | ~3.0% y/y |

| Scheduled cash earnings (2024) | +3.6% |

| Unemployment (2024) | ~2.5% |

| Population (2023) | ~124.6M |

Full Version Awaits

Resona Holdings PESTLE Analysis

The Resona Holdings PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content and structure visible in this preview are identical to the final file you’ll download immediately after payment. No placeholders or teasers—this is the real, professionally structured analysis you’ll own upon checkout.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, economic trends, and technological change are reshaping Resona Holdings with our concise PESTLE analysis—designed to inform investment and strategic decisions. This expert-ready brief highlights key risks and opportunities; buy the full PESTLE for a detailed, actionable breakdown you can use in minutes. Download now to turn external insights into competitive advantage.

Political factors

Policy continuity and fiscal stance

Japan’s relatively stable policymaking and pro-growth fiscal measures, including a ¥26.7 trillion supplementary package in 2023–24, support credit conditions, public investment and consumer confidence. A supportive stance can boost loan demand among SMEs and households, while fiscal consolidation risks dampening spending and raising credit risk. Resona must align portfolio and lending strategy with evolving budget priorities and subsidy shifts amid Japan’s ~260% general government debt/GDP backdrop.

Local government ties and regional policy

Resona Holdings (ticker 8308) and its core banks Resona Bank and Saitama Resona Bank interface closely with prefectural and municipal programs. Regional revitalization, tourism promotion and SME subsidy schemes feed loan pipelines and fee income and support deposits and project finance. Strong public-sector relationships bolster trust business, while policy shifts or leadership turnover can quickly change funding flows and collaboration.

Geopolitics and market stability

Global tensions drive yen volatility and dent equity risk appetite, pressuring SME credit via trade frictions and supply‑chain shifts; flight‑to‑safety has shifted deposits into low‑risk assets and JGBs (10y ~0.6% in 2024). Resona must maintain hedges and conservative liquidity buffers, including regulatory LCR above 100%, to withstand geopolitical shocks.

Corporate governance reforms

Japan’s Stewardship Code (revised 2020) and Corporate Governance Code (updated 2021) push banks toward higher capital efficiency and transparency, prompting Resona to prioritize ROE and streamline cross-shareholdings as investor scrutiny intensified in 2024.

- capital efficiency: ROE focus

- cross-shareholdings: optimization pressure

- board/disclosure: increased independence and reporting

- benefit: attract investors, potentially lower funding costs

Digital yen and public-sector digitization

Government-led digital transformation and the Bank of Japan CBDC experiments, initiated in 2021, could materially reshape payments and settlement rails, reducing reliance on cash and accelerating real-time settlement for Resona. Public infrastructure upgrades will lower cash-handling costs and shorten settlement cycles, while policy timelines will dictate Resona’s IT investment and interoperability roadmaps. Early adaptation can lock in transaction flows and ecosystem partnerships.

- Digital Agency est. 2021; BoJ CBDC work began 2021

- Policy drives IT spend timing and interoperability mandates

- Early movers capture payment volumes and partnerships

Fiscal stimulus ¥26.7tn boosts lending; public debt ~260% raises sovereign risk

Stable pro-growth fiscal moves (¥26.7tn sup. 2023–24) support loan demand but fiscal consolidation risk exists. High public debt (~260% of GDP) raises long-term sovereign risk. Geopolitical-driven yen/JGB moves (10y ~0.6% in 2024) pressure liquidity and credit. Governance rules push ROE/capital efficiency and faster digital/IT rollout.

| Metric | Value |

|---|---|

| Supplementary budget | ¥26.7tn (2023–24) |

| Debt/GDP | ~260% |

| JGB 10y | ~0.6% (2024) |

| LCR | >100% regulatory |

What is included in the product

Explores how external macro-environmental factors uniquely affect Resona Holdings across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, consultants and investors, the analysis offers detailed sub-points, forward-looking scenario insights and ready-to-insert formatting to identify risks, opportunities and strategic responses.

A concise, visually segmented PESTLE summary for Resona Holdings that relieves briefing pain points by enabling quick interpretation, easy edits for local context, and drop‑in use for presentations or team alignment.

Economic factors

BoJ policy normalization and rates

BoJ policy normalization from -0.1% toward positive territory and a rise in 10‑yr JGB yields (around 0.9% in 2024) has widened bank NIMs but marked down bond portfolios, raising unrealized losses for regional banks. Gradual rate hikes can boost Resona’s loan margins as loan repricing accelerates, yet funding costs and deposit betas will pressure short‑term gains. Resona must tighten ALM and expand hedging to balance rate risk and protect earnings.

Inflation and wage dynamics

Sustained wage gains—scheduled cash earnings rose about 3.6% in 2024—support household consumption and SME revenues, underpinning credit demand for Resona. Core CPI ran near 3.0% y/y in 2024, lifting nominal activity but tightening real affordability for some segments. Credit underwriting must track real income and price pass-through trends; pricing discipline and fee diversification help offset margin volatility.

SME health and credit demand

Resona’s SME-heavy loan book is vulnerable to input-cost swings and export cycles in a market where SMEs comprise 99.7% of Japanese firms and employ roughly 70% of workers (METI). Government credit guarantees and refinancing facilities (expanded since 2020) materially affect risk-adjusted returns. Tight labour markets with unemployment around 2.5% (2024) and rising capex plans lift working-capital drawdowns. Proactive advisory and covenant monitoring have helped keep bank NPLs low.

Housing and real estate cycle

Competition and consolidation

Competition and consolidation: three megabanks (MUFG, SMBC, Mizuho) and ongoing regional bank mergers intensify pressure on Resona, while fintechs compress pricing and fee income through digital channels.

Scale advantages in tech and compliance among larger players widen cost gaps and raise barriers to profitability for midsized banks; consolidation is reshaping local market shares and collaboration opportunities.

Resona must sharpen segment focus and accelerate cross-sell to protect margins and customer share.

- Megabanks: MUFG, SMBC, Mizuho

- Trend: regional bank consolidation ongoing

- Threat: fintechs press pricing and fees

- Response: sharpen segmentation; boost cross-sell

Fiscal stimulus ¥26.7tn boosts lending; public debt ~260% raises sovereign risk

BoJ normalization and 10‑yr JGB ~0.9% (2024) widened NIMs but raised unrealized losses; gradual hikes aid loan repricing while lifting funding costs. Scheduled cash earnings +3.6% (2024) and core CPI ~3.0% (2024) support demand but squeeze real affordability. SME exposure (99.7% of firms) and unemployment ~2.5% (2024) shape credit risk and working‑capex flows. Tight ALM, hedging, fee diversification and strict LTVs required.

| Metric | Value |

|---|---|

| 10‑yr JGB (2024) | ~0.9% |

| Core CPI (2024) | ~3.0% y/y |

| Scheduled cash earnings (2024) | +3.6% |

| Unemployment (2024) | ~2.5% |

| Population (2023) | ~124.6M |

Full Version Awaits

Resona Holdings PESTLE Analysis

The Resona Holdings PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content and structure visible in this preview are identical to the final file you’ll download immediately after payment. No placeholders or teasers—this is the real, professionally structured analysis you’ll own upon checkout.