Retif Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Retif Group faces moderate buyer power, concentrated suppliers for specialty products, and persistent rivalry from regional retailers, while substitutes and regulatory shifts subtly reshape margins. This snapshot highlights key pressures but leaves out force-by-force metrics and strategic options. Unlock the full Porter’s Five Forces Analysis to see ratings, visuals, and tailored recommendations for Retif Group.

Suppliers Bargaining Power

Diverse supplier base

Retif sources from a diversified base—over 200 manufacturers across fixtures, packaging, displays and POS hardware—diluting single-vendor leverage and enabling competitive bidding and dual-sourcing for most categories. Niche custom fabricators and branded POS vendors still command localized pricing power in specialized segments. Active vendor management and expanding private-label ranges (roughly 20% of merchandising SKUs) mitigate concentrated nodes.

Specialized components

Specialized components for custom shopfittings, digital signage and POS peripherals raise switching costs and lead times, with the digital signage market ~22 billion USD in 2024 highlighting scale and supplier leverage. Certification, compatibility and integration requirements reinforce certain suppliers’ influence, especially for proprietary POS systems. Framework agreements and industry standardization can reduce dependency, while modular designs further mitigate supplier lock-in.

Input price volatility

Input-price volatility remains high in 2024 as steel, aluminum, plastics, paper and electronics continue to track commodity and chip cycles, allowing suppliers to pass through costs and squeeze margins. Suppliers increasingly shifted price risk to buyers in 2024, pressuring gross margins for distributors like Retif. Hedging, should-cost models and multi-year contracts implemented in 2024 stabilize pricing and supply. Value engineering preserves price points while maintaining function and protects unit economics.

Logistics and lead-time risk

Global supply chains expose Retif to volatile freight rates, port congestion and geopolitical shocks; 2024 saw freight rates normalize versus 2021 peaks but congestion and red‑sea risks still cause episodic spikes that give logistics providers leverage in tight markets.

- Suppliers control logistics windows → higher bargaining power

- Nearshoring/regional warehousing → lowers lead‑time risk

- Vendor‑managed inventory → smooths supply variability

- Safety stocks → buffer against shipment disruption

ESG and compliance

ESG certifications such as FSC for paper and EU rules like REACH, WEEE and RoHS narrow qualified supplier pools, increasing supplier bargaining power as compliant vendors can command price premiums. Retif’s scale and internal compliance programs expand its qualified supplier pipeline over time, while strategic sustainability partnerships help secure longer-term, favorable terms and mitigate supplier leverage.

- FSC, REACH, WEEE/RoHS restrict supplier eligibility

- Compliant vendors may charge premiums

- Retif scale + compliance widen supplier base

- Sustainability partnerships lock better terms

Diversified sourcing (>200), ~20% private-label and ESG squeeze digital-signage margins

Retif sources from over 200 manufacturers, limiting single‑supplier leverage while private‑label SKUs (~20%) reduce dependency. Specialized suppliers (digital signage market ~22 billion USD in 2024) and proprietary POS components sustain pockets of strong bargaining power. 2024 input‑price volatility enabled supplier pass‑throughs, pressuring margins. ESG rules (FSC, REACH, WEEE, RoHS) shrink qualified supplier pools and can command premiums.

| Metric | Value | Implication |

|---|---|---|

| Manufacturers | >200 | Low single‑vendor risk |

| Private‑label share | ~20% | Mitigates supplier power |

| Digital signage market (2024) | $22bn | Supplier scale advantage |

What is included in the product

Tailored exclusively for Retif Group, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive forces and strategic risks to pricing, margins and market share.

A one-sheet Porter's Five Forces for Retif Group that highlights competitive pressures, supplier/buyer leverage and substitution risk—ready to drop into presentations; customize scores and scenarios without macros to quickly guide strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Fragmented SME base

Many retail SMEs buy small baskets, limiting individual bargaining power; across the EU SMEs represent 99.8% of enterprises (Eurostat 2023), concentrating buyers but not large orders. Convenience, expert advice and next‑day delivery often trump pure price in procurement decisions. Retif’s wide assortment and services raise perceived value and margin resilience. Churn is addressed through loyalty schemes and bundled offers to increase repeat purchase frequency.

Large chain buyers

Large multi-site retailers increase bargaining power by running centralized RFPs, demanding volume rebates and tight SLAs, and unbundling categories across suppliers to optimize price and service. These behaviors force margin pressure and contract complexity for suppliers. Retif mitigates risk through turnkey rollout capability and pan-European delivery, while integrated design-to-install solutions create operational stickiness and higher switching costs.

Low switching costs

For standard packaging and generic fixtures buyers can switch readily, putting downward pressure on Retif Group margins as over 60% of procurement decisions in 2024 involved online price comparison, amplifying transparency and competition. Differentiated designs, private-label SKUs and bundled post-sale services increase perceived uniqueness and raise switching costs. Subscription or automated replenishment models further lock in customers and stabilize recurring revenue.

Price sensitivity

Retailers under margin pressure emphasize total cost of ownership, with European homewares margins reported near 25–30% in 2024, shifting focus from headline price to lifecycle cost. Promotions and tiered assortments address budget bands, and ROI cases showing 8–12% lift in sell-through and measurable labor-efficiency gains have reduced headline discounting. Demonstrating impact on sell-through and labor efficiency reframes value and lowers discount intensity.

- tco-focus

- tiered-assortments

- sell-through+8–12%

- lower-discounts

Service expectations

Customers demand design support, quick delivery, installation and after-sales; Statista 2024 reports 73% of EU shoppers prioritize fast delivery, making service-level guarantees potent negotiation levers. Superior execution lets Retif capture selective price premiums; service failures rapidly erode loyalty and amplify buyer power.

- Design support: differentiator

- Delivery SLA: negotiation tool

- After-sales: retention driver

Homewares: 25–30% margins; 60% price checks lift loyalty

Retail SMEs (99.8% of EU firms, Eurostat 2023) limit single-buyer scale but drive aggregate volume; 60% of 2024 purchases used online price comparison, raising price transparency. Service SLAs (73% prioritize fast delivery, Statista 2024) and design/installation raise switching costs. Homewares margins ~25–30% (2024); sell-through lifts of 8–12% justify premium pricing.

| Metric | Value |

|---|---|

| SME share | 99.8% |

| Price comparison | 60% (2024) |

| Fast delivery importance | 73% (2024) |

Preview the Actual Deliverable

Retif Group Porter's Five Forces Analysis

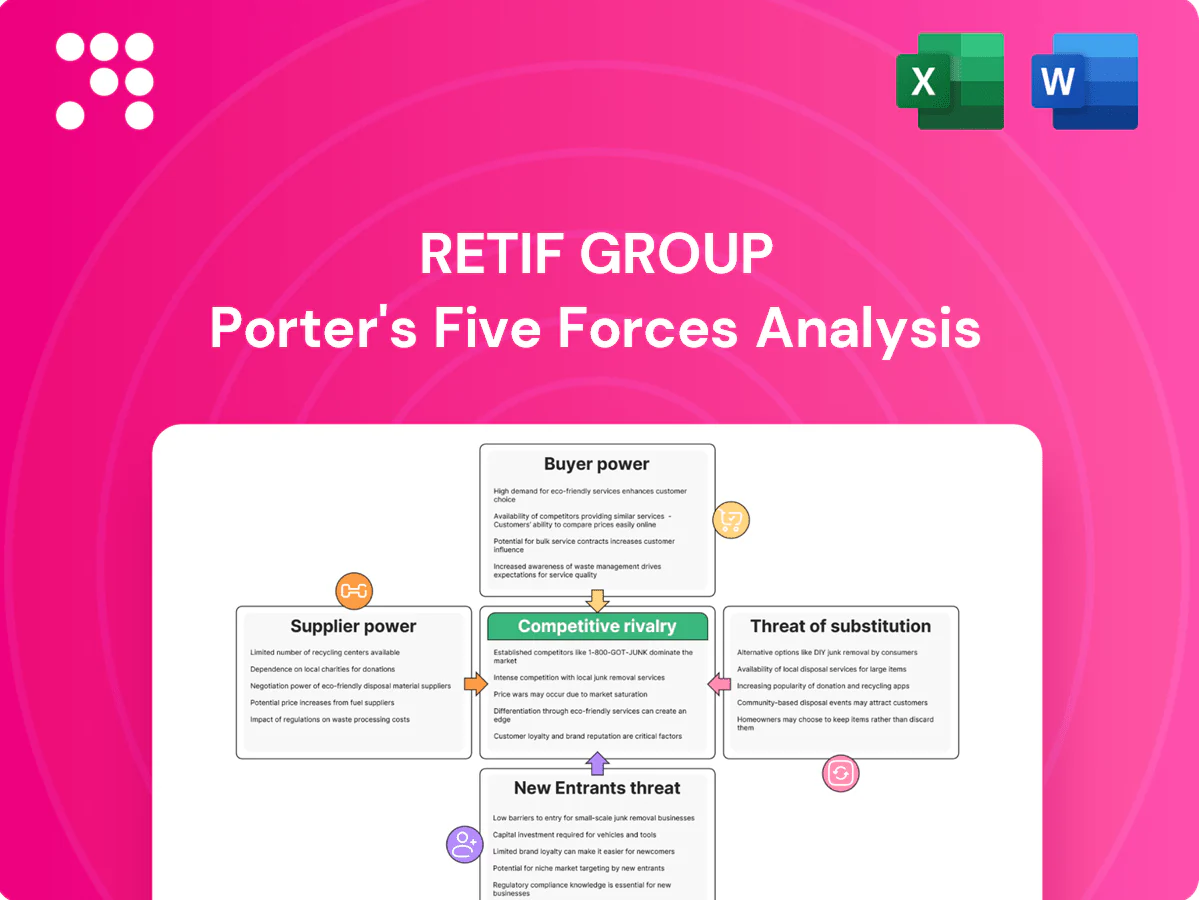

This preview shows the complete Retif Group Porter's Five Forces Analysis and is the exact document you'll receive after purchase. It contains the full assessment of competitive rivalry, supplier and buyer power, and the threats of substitutes and new entrants. The file is professionally formatted and ready for immediate download and use.

Don't Miss the Bigger Picture

Retif Group faces moderate buyer power, concentrated suppliers for specialty products, and persistent rivalry from regional retailers, while substitutes and regulatory shifts subtly reshape margins. This snapshot highlights key pressures but leaves out force-by-force metrics and strategic options. Unlock the full Porter’s Five Forces Analysis to see ratings, visuals, and tailored recommendations for Retif Group.

Suppliers Bargaining Power

Diverse supplier base

Retif sources from a diversified base—over 200 manufacturers across fixtures, packaging, displays and POS hardware—diluting single-vendor leverage and enabling competitive bidding and dual-sourcing for most categories. Niche custom fabricators and branded POS vendors still command localized pricing power in specialized segments. Active vendor management and expanding private-label ranges (roughly 20% of merchandising SKUs) mitigate concentrated nodes.

Specialized components

Specialized components for custom shopfittings, digital signage and POS peripherals raise switching costs and lead times, with the digital signage market ~22 billion USD in 2024 highlighting scale and supplier leverage. Certification, compatibility and integration requirements reinforce certain suppliers’ influence, especially for proprietary POS systems. Framework agreements and industry standardization can reduce dependency, while modular designs further mitigate supplier lock-in.

Input price volatility

Input-price volatility remains high in 2024 as steel, aluminum, plastics, paper and electronics continue to track commodity and chip cycles, allowing suppliers to pass through costs and squeeze margins. Suppliers increasingly shifted price risk to buyers in 2024, pressuring gross margins for distributors like Retif. Hedging, should-cost models and multi-year contracts implemented in 2024 stabilize pricing and supply. Value engineering preserves price points while maintaining function and protects unit economics.

Logistics and lead-time risk

Global supply chains expose Retif to volatile freight rates, port congestion and geopolitical shocks; 2024 saw freight rates normalize versus 2021 peaks but congestion and red‑sea risks still cause episodic spikes that give logistics providers leverage in tight markets.

- Suppliers control logistics windows → higher bargaining power

- Nearshoring/regional warehousing → lowers lead‑time risk

- Vendor‑managed inventory → smooths supply variability

- Safety stocks → buffer against shipment disruption

ESG and compliance

ESG certifications such as FSC for paper and EU rules like REACH, WEEE and RoHS narrow qualified supplier pools, increasing supplier bargaining power as compliant vendors can command price premiums. Retif’s scale and internal compliance programs expand its qualified supplier pipeline over time, while strategic sustainability partnerships help secure longer-term, favorable terms and mitigate supplier leverage.

- FSC, REACH, WEEE/RoHS restrict supplier eligibility

- Compliant vendors may charge premiums

- Retif scale + compliance widen supplier base

- Sustainability partnerships lock better terms

Diversified sourcing (>200), ~20% private-label and ESG squeeze digital-signage margins

Retif sources from over 200 manufacturers, limiting single‑supplier leverage while private‑label SKUs (~20%) reduce dependency. Specialized suppliers (digital signage market ~22 billion USD in 2024) and proprietary POS components sustain pockets of strong bargaining power. 2024 input‑price volatility enabled supplier pass‑throughs, pressuring margins. ESG rules (FSC, REACH, WEEE, RoHS) shrink qualified supplier pools and can command premiums.

| Metric | Value | Implication |

|---|---|---|

| Manufacturers | >200 | Low single‑vendor risk |

| Private‑label share | ~20% | Mitigates supplier power |

| Digital signage market (2024) | $22bn | Supplier scale advantage |

What is included in the product

Tailored exclusively for Retif Group, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive forces and strategic risks to pricing, margins and market share.

A one-sheet Porter's Five Forces for Retif Group that highlights competitive pressures, supplier/buyer leverage and substitution risk—ready to drop into presentations; customize scores and scenarios without macros to quickly guide strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Fragmented SME base

Many retail SMEs buy small baskets, limiting individual bargaining power; across the EU SMEs represent 99.8% of enterprises (Eurostat 2023), concentrating buyers but not large orders. Convenience, expert advice and next‑day delivery often trump pure price in procurement decisions. Retif’s wide assortment and services raise perceived value and margin resilience. Churn is addressed through loyalty schemes and bundled offers to increase repeat purchase frequency.

Large chain buyers

Large multi-site retailers increase bargaining power by running centralized RFPs, demanding volume rebates and tight SLAs, and unbundling categories across suppliers to optimize price and service. These behaviors force margin pressure and contract complexity for suppliers. Retif mitigates risk through turnkey rollout capability and pan-European delivery, while integrated design-to-install solutions create operational stickiness and higher switching costs.

Low switching costs

For standard packaging and generic fixtures buyers can switch readily, putting downward pressure on Retif Group margins as over 60% of procurement decisions in 2024 involved online price comparison, amplifying transparency and competition. Differentiated designs, private-label SKUs and bundled post-sale services increase perceived uniqueness and raise switching costs. Subscription or automated replenishment models further lock in customers and stabilize recurring revenue.

Price sensitivity

Retailers under margin pressure emphasize total cost of ownership, with European homewares margins reported near 25–30% in 2024, shifting focus from headline price to lifecycle cost. Promotions and tiered assortments address budget bands, and ROI cases showing 8–12% lift in sell-through and measurable labor-efficiency gains have reduced headline discounting. Demonstrating impact on sell-through and labor efficiency reframes value and lowers discount intensity.

- tco-focus

- tiered-assortments

- sell-through+8–12%

- lower-discounts

Service expectations

Customers demand design support, quick delivery, installation and after-sales; Statista 2024 reports 73% of EU shoppers prioritize fast delivery, making service-level guarantees potent negotiation levers. Superior execution lets Retif capture selective price premiums; service failures rapidly erode loyalty and amplify buyer power.

- Design support: differentiator

- Delivery SLA: negotiation tool

- After-sales: retention driver

Homewares: 25–30% margins; 60% price checks lift loyalty

Retail SMEs (99.8% of EU firms, Eurostat 2023) limit single-buyer scale but drive aggregate volume; 60% of 2024 purchases used online price comparison, raising price transparency. Service SLAs (73% prioritize fast delivery, Statista 2024) and design/installation raise switching costs. Homewares margins ~25–30% (2024); sell-through lifts of 8–12% justify premium pricing.

| Metric | Value |

|---|---|

| SME share | 99.8% |

| Price comparison | 60% (2024) |

| Fast delivery importance | 73% (2024) |

Preview the Actual Deliverable

Retif Group Porter's Five Forces Analysis

This preview shows the complete Retif Group Porter's Five Forces Analysis and is the exact document you'll receive after purchase. It contains the full assessment of competitive rivalry, supplier and buyer power, and the threats of substitutes and new entrants. The file is professionally formatted and ready for immediate download and use.

Description

Don't Miss the Bigger Picture

Retif Group faces moderate buyer power, concentrated suppliers for specialty products, and persistent rivalry from regional retailers, while substitutes and regulatory shifts subtly reshape margins. This snapshot highlights key pressures but leaves out force-by-force metrics and strategic options. Unlock the full Porter’s Five Forces Analysis to see ratings, visuals, and tailored recommendations for Retif Group.

Suppliers Bargaining Power

Diverse supplier base

Retif sources from a diversified base—over 200 manufacturers across fixtures, packaging, displays and POS hardware—diluting single-vendor leverage and enabling competitive bidding and dual-sourcing for most categories. Niche custom fabricators and branded POS vendors still command localized pricing power in specialized segments. Active vendor management and expanding private-label ranges (roughly 20% of merchandising SKUs) mitigate concentrated nodes.

Specialized components

Specialized components for custom shopfittings, digital signage and POS peripherals raise switching costs and lead times, with the digital signage market ~22 billion USD in 2024 highlighting scale and supplier leverage. Certification, compatibility and integration requirements reinforce certain suppliers’ influence, especially for proprietary POS systems. Framework agreements and industry standardization can reduce dependency, while modular designs further mitigate supplier lock-in.

Input price volatility

Input-price volatility remains high in 2024 as steel, aluminum, plastics, paper and electronics continue to track commodity and chip cycles, allowing suppliers to pass through costs and squeeze margins. Suppliers increasingly shifted price risk to buyers in 2024, pressuring gross margins for distributors like Retif. Hedging, should-cost models and multi-year contracts implemented in 2024 stabilize pricing and supply. Value engineering preserves price points while maintaining function and protects unit economics.

Logistics and lead-time risk

Global supply chains expose Retif to volatile freight rates, port congestion and geopolitical shocks; 2024 saw freight rates normalize versus 2021 peaks but congestion and red‑sea risks still cause episodic spikes that give logistics providers leverage in tight markets.

- Suppliers control logistics windows → higher bargaining power

- Nearshoring/regional warehousing → lowers lead‑time risk

- Vendor‑managed inventory → smooths supply variability

- Safety stocks → buffer against shipment disruption

ESG and compliance

ESG certifications such as FSC for paper and EU rules like REACH, WEEE and RoHS narrow qualified supplier pools, increasing supplier bargaining power as compliant vendors can command price premiums. Retif’s scale and internal compliance programs expand its qualified supplier pipeline over time, while strategic sustainability partnerships help secure longer-term, favorable terms and mitigate supplier leverage.

- FSC, REACH, WEEE/RoHS restrict supplier eligibility

- Compliant vendors may charge premiums

- Retif scale + compliance widen supplier base

- Sustainability partnerships lock better terms

Diversified sourcing (>200), ~20% private-label and ESG squeeze digital-signage margins

Retif sources from over 200 manufacturers, limiting single‑supplier leverage while private‑label SKUs (~20%) reduce dependency. Specialized suppliers (digital signage market ~22 billion USD in 2024) and proprietary POS components sustain pockets of strong bargaining power. 2024 input‑price volatility enabled supplier pass‑throughs, pressuring margins. ESG rules (FSC, REACH, WEEE, RoHS) shrink qualified supplier pools and can command premiums.

| Metric | Value | Implication |

|---|---|---|

| Manufacturers | >200 | Low single‑vendor risk |

| Private‑label share | ~20% | Mitigates supplier power |

| Digital signage market (2024) | $22bn | Supplier scale advantage |

What is included in the product

Tailored exclusively for Retif Group, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive forces and strategic risks to pricing, margins and market share.

A one-sheet Porter's Five Forces for Retif Group that highlights competitive pressures, supplier/buyer leverage and substitution risk—ready to drop into presentations; customize scores and scenarios without macros to quickly guide strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Fragmented SME base

Many retail SMEs buy small baskets, limiting individual bargaining power; across the EU SMEs represent 99.8% of enterprises (Eurostat 2023), concentrating buyers but not large orders. Convenience, expert advice and next‑day delivery often trump pure price in procurement decisions. Retif’s wide assortment and services raise perceived value and margin resilience. Churn is addressed through loyalty schemes and bundled offers to increase repeat purchase frequency.

Large chain buyers

Large multi-site retailers increase bargaining power by running centralized RFPs, demanding volume rebates and tight SLAs, and unbundling categories across suppliers to optimize price and service. These behaviors force margin pressure and contract complexity for suppliers. Retif mitigates risk through turnkey rollout capability and pan-European delivery, while integrated design-to-install solutions create operational stickiness and higher switching costs.

Low switching costs

For standard packaging and generic fixtures buyers can switch readily, putting downward pressure on Retif Group margins as over 60% of procurement decisions in 2024 involved online price comparison, amplifying transparency and competition. Differentiated designs, private-label SKUs and bundled post-sale services increase perceived uniqueness and raise switching costs. Subscription or automated replenishment models further lock in customers and stabilize recurring revenue.

Price sensitivity

Retailers under margin pressure emphasize total cost of ownership, with European homewares margins reported near 25–30% in 2024, shifting focus from headline price to lifecycle cost. Promotions and tiered assortments address budget bands, and ROI cases showing 8–12% lift in sell-through and measurable labor-efficiency gains have reduced headline discounting. Demonstrating impact on sell-through and labor efficiency reframes value and lowers discount intensity.

- tco-focus

- tiered-assortments

- sell-through+8–12%

- lower-discounts

Service expectations

Customers demand design support, quick delivery, installation and after-sales; Statista 2024 reports 73% of EU shoppers prioritize fast delivery, making service-level guarantees potent negotiation levers. Superior execution lets Retif capture selective price premiums; service failures rapidly erode loyalty and amplify buyer power.

- Design support: differentiator

- Delivery SLA: negotiation tool

- After-sales: retention driver

Homewares: 25–30% margins; 60% price checks lift loyalty

Retail SMEs (99.8% of EU firms, Eurostat 2023) limit single-buyer scale but drive aggregate volume; 60% of 2024 purchases used online price comparison, raising price transparency. Service SLAs (73% prioritize fast delivery, Statista 2024) and design/installation raise switching costs. Homewares margins ~25–30% (2024); sell-through lifts of 8–12% justify premium pricing.

| Metric | Value |

|---|---|

| SME share | 99.8% |

| Price comparison | 60% (2024) |

| Fast delivery importance | 73% (2024) |

Preview the Actual Deliverable

Retif Group Porter's Five Forces Analysis

This preview shows the complete Retif Group Porter's Five Forces Analysis and is the exact document you'll receive after purchase. It contains the full assessment of competitive rivalry, supplier and buyer power, and the threats of substitutes and new entrants. The file is professionally formatted and ready for immediate download and use.