Revvity SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Revvity SWOT Analysis highlights core strengths in diagnostics and life-science tools, alongside market risks and growth opportunities in precision medicine. Want the full picture with actionable insights and financial context? Purchase the complete SWOT for an editable, investor-ready report to plan, pitch, or invest with confidence.

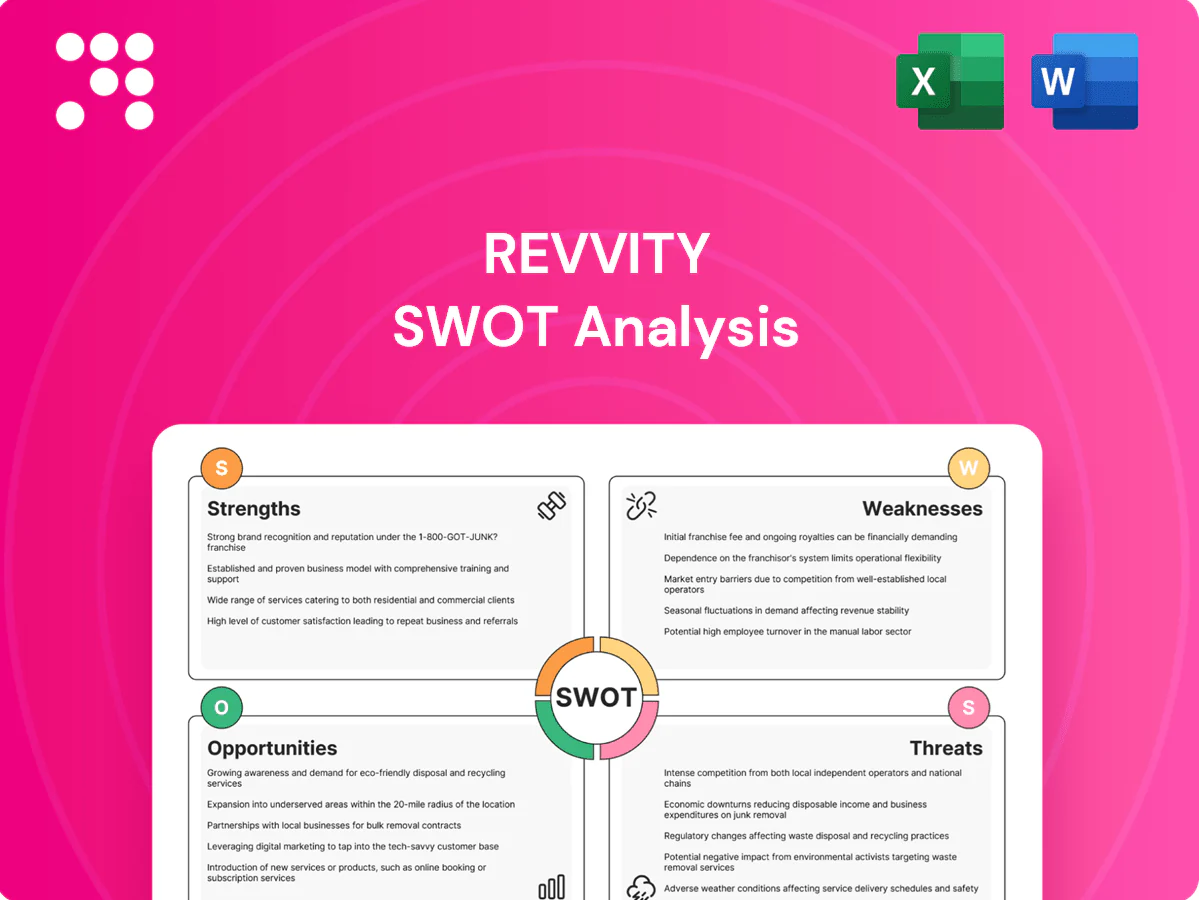

Strengths

Broad, end-to-end life sciences portfolio

Revvity offers reagents, instruments, software and services across discovery-to-diagnostics, creating one-stop coverage that supported cross-selling into pharma, diagnostics, academic and government accounts and helped drive FY2024 revenue of about $4.1B; this breadth deepens account penetration, raises switching costs, and enables bundled workflow solutions rather than isolated point products.

Strong positions in genomics, proteomics, imaging

Revvity’s capabilities across NGS, assay reagents, protein analysis and high‑content imaging align with a multi‑omics market growing ~15% CAGR to 2030; Revvity reported roughly $4.2B revenue in FY2024, with consumables/services driving majority recurring sales, supporting premium pricing, sticky workflows and platform standardization across labs.

Recurring consumables and services revenue

Revvity's large installed base drives repeat reagent and kit purchases, with consumables and services representing over 50% of reported FY2024 revenue of about $3.6 billion, underpinning steady aftermarket demand. Services and software subscriptions deliver higher-margin, predictable cashflows, cushioning macro volatility versus pure capital-equipment peers. This recurring mix boosts customer lifetime value and retention, improving revenue visibility.

Global, diversified customer footprint

Revvity's exposure across pharma, diagnostics labs, academia and government lowers customer concentration risk and smooths demand cycles while geographic diversity spreads regulatory and funding risk across regions; its global distribution and service networks enable cross-market leverage and local teams accelerate adoption and technical support.

- Sector mix: pharma/diagnostics/academia/gov

- Geographic spread reduces single-market risk

- Global distribution + local service = faster adoption

Integrated hardware–software–services solutions

Combining instruments with analytics and informatics creates differentiated workflows that streamline lab processes, while integrated data improves outcomes and speeds decision-making across research and diagnostic use cases. Services augment customer capacity and regulatory compliance, embedding Revvity into critical workflows and raising barriers to entry through recurring revenue and platform stickiness.

- Integrated workflows

- Faster, data-driven decisions

- Services = capacity + compliance

- High switching costs, embedded platform

Multi-omics platform; $4.1B, >50% recurring sales

Revvity generated about $4.1B revenue in FY2024, with consumables and services accounting for over 50% of sales, driving recurring, higher‑margin cashflows. Its integrated instruments, reagents, software and services create sticky workflows and strong cross‑selling across pharma, diagnostics, academia and government. Exposure to a multi‑omics market growing ~15% CAGR to 2030 supports platform demand and pricing power.

| Metric | Value |

|---|---|

| FY2024 revenue | $4.1B |

| Consumables & services | >50% |

| Multi‑omics CAGR (to 2030) | ~15% |

What is included in the product

Provides a concise strategic assessment of Revvity’s internal strengths and weaknesses and external opportunities and threats to inform competitive positioning and growth strategy.

Provides a concise Revvity SWOT matrix for fast alignment across R&D-driven units; visual, editable formatting streamlines strategic updates and creates stakeholder-ready summaries for quick decision-making.

Weaknesses

Exposure to R&D and capital spending cycles

Revvity is exposed to cyclical academic grants and biopharma budgets—U.S. federal R&D via NIH hovers near $49 billion, creating boom‑and‑bust funding windows. Capital equipment orders are lumpy and tied to grant/fiscal timing, so slowdowns elongate sales cycles and defer upgrades. That variability pressures revenue visibility and reduces factory utilization, increasing working capital strain.

Regulatory complexity in diagnostics

Clinical diagnostics face rigorous validation and approvals—FDA 510(k) review is targeted at 90 days while complex pathways and PMAs can extend well beyond a year—raising time-to-market and development costs. Evolving IVDR requirements (full transition by May 2027) and stricter post-market surveillance and quality systems increase ongoing burden and can delay launches, ceding share to faster competitors.

Portfolio integration and focus challenges

Managing a wide catalog risks operational complexity, increasing costs and slow time-to-market as platforms and SKUs multiply. Ensuring interoperability across instruments and software demands sustained investment in R&D and engineering. Product overlap can dilute R&D focus and marketing clarity, and integration missteps have the potential to erode customer experience and retention.

High capital intensity and long sales cycles

- Demo/pilot cycles: 6–12 months

- Higher inventory and install capex

- Extended qualification increases time-to-revenue

- Near-term margin and cash-flow pressure

Dependence on key technologies and suppliers

Revvity depends on limited sources for critical components and reagents, creating single‑point vulnerabilities where supply disruptions can halt production or delay shipments. Rapid technology shifts risk making current platforms obsolete, and vendor concentration increases bargaining leverage against Revvity.

- Single‑source reagents risk

- Production/shipment delays

- Platform obsolescence

- Vendor concentration → bargaining risk

Grant volatility, 6-12m sales cycles, IVDR May 2027, supplier concentration risk

Revvity faces boom‑and‑bust grant cycles (U.S. NIH ≈ $49B in 2024) and lumpy capital orders that elongate 6–12‑month sales cycles, pressuring revenue visibility and utilization. Regulatory complexity (IVDR full effect by May 2027; FDA pathways often >90 days) raises time‑to‑market and costs. Supplier concentration and single‑source reagents amplify production and delivery risk.

| Metric | Value |

|---|---|

| NIH funding (2024) | $49B |

| Demo/pilot cycle | 6–12 months |

| IVDR deadline | May 2027 |

Preview Before You Purchase

Revvity SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version.

You're viewing a live preview of the real file—buy to download the full, structured report immediately.

Dive Deeper Into the Company’s Strategic Blueprint

Revvity SWOT Analysis highlights core strengths in diagnostics and life-science tools, alongside market risks and growth opportunities in precision medicine. Want the full picture with actionable insights and financial context? Purchase the complete SWOT for an editable, investor-ready report to plan, pitch, or invest with confidence.

Strengths

Broad, end-to-end life sciences portfolio

Revvity offers reagents, instruments, software and services across discovery-to-diagnostics, creating one-stop coverage that supported cross-selling into pharma, diagnostics, academic and government accounts and helped drive FY2024 revenue of about $4.1B; this breadth deepens account penetration, raises switching costs, and enables bundled workflow solutions rather than isolated point products.

Strong positions in genomics, proteomics, imaging

Revvity’s capabilities across NGS, assay reagents, protein analysis and high‑content imaging align with a multi‑omics market growing ~15% CAGR to 2030; Revvity reported roughly $4.2B revenue in FY2024, with consumables/services driving majority recurring sales, supporting premium pricing, sticky workflows and platform standardization across labs.

Recurring consumables and services revenue

Revvity's large installed base drives repeat reagent and kit purchases, with consumables and services representing over 50% of reported FY2024 revenue of about $3.6 billion, underpinning steady aftermarket demand. Services and software subscriptions deliver higher-margin, predictable cashflows, cushioning macro volatility versus pure capital-equipment peers. This recurring mix boosts customer lifetime value and retention, improving revenue visibility.

Global, diversified customer footprint

Revvity's exposure across pharma, diagnostics labs, academia and government lowers customer concentration risk and smooths demand cycles while geographic diversity spreads regulatory and funding risk across regions; its global distribution and service networks enable cross-market leverage and local teams accelerate adoption and technical support.

- Sector mix: pharma/diagnostics/academia/gov

- Geographic spread reduces single-market risk

- Global distribution + local service = faster adoption

Integrated hardware–software–services solutions

Combining instruments with analytics and informatics creates differentiated workflows that streamline lab processes, while integrated data improves outcomes and speeds decision-making across research and diagnostic use cases. Services augment customer capacity and regulatory compliance, embedding Revvity into critical workflows and raising barriers to entry through recurring revenue and platform stickiness.

- Integrated workflows

- Faster, data-driven decisions

- Services = capacity + compliance

- High switching costs, embedded platform

Multi-omics platform; $4.1B, >50% recurring sales

Revvity generated about $4.1B revenue in FY2024, with consumables and services accounting for over 50% of sales, driving recurring, higher‑margin cashflows. Its integrated instruments, reagents, software and services create sticky workflows and strong cross‑selling across pharma, diagnostics, academia and government. Exposure to a multi‑omics market growing ~15% CAGR to 2030 supports platform demand and pricing power.

| Metric | Value |

|---|---|

| FY2024 revenue | $4.1B |

| Consumables & services | >50% |

| Multi‑omics CAGR (to 2030) | ~15% |

What is included in the product

Provides a concise strategic assessment of Revvity’s internal strengths and weaknesses and external opportunities and threats to inform competitive positioning and growth strategy.

Provides a concise Revvity SWOT matrix for fast alignment across R&D-driven units; visual, editable formatting streamlines strategic updates and creates stakeholder-ready summaries for quick decision-making.

Weaknesses

Exposure to R&D and capital spending cycles

Revvity is exposed to cyclical academic grants and biopharma budgets—U.S. federal R&D via NIH hovers near $49 billion, creating boom‑and‑bust funding windows. Capital equipment orders are lumpy and tied to grant/fiscal timing, so slowdowns elongate sales cycles and defer upgrades. That variability pressures revenue visibility and reduces factory utilization, increasing working capital strain.

Regulatory complexity in diagnostics

Clinical diagnostics face rigorous validation and approvals—FDA 510(k) review is targeted at 90 days while complex pathways and PMAs can extend well beyond a year—raising time-to-market and development costs. Evolving IVDR requirements (full transition by May 2027) and stricter post-market surveillance and quality systems increase ongoing burden and can delay launches, ceding share to faster competitors.

Portfolio integration and focus challenges

Managing a wide catalog risks operational complexity, increasing costs and slow time-to-market as platforms and SKUs multiply. Ensuring interoperability across instruments and software demands sustained investment in R&D and engineering. Product overlap can dilute R&D focus and marketing clarity, and integration missteps have the potential to erode customer experience and retention.

High capital intensity and long sales cycles

- Demo/pilot cycles: 6–12 months

- Higher inventory and install capex

- Extended qualification increases time-to-revenue

- Near-term margin and cash-flow pressure

Dependence on key technologies and suppliers

Revvity depends on limited sources for critical components and reagents, creating single‑point vulnerabilities where supply disruptions can halt production or delay shipments. Rapid technology shifts risk making current platforms obsolete, and vendor concentration increases bargaining leverage against Revvity.

- Single‑source reagents risk

- Production/shipment delays

- Platform obsolescence

- Vendor concentration → bargaining risk

Grant volatility, 6-12m sales cycles, IVDR May 2027, supplier concentration risk

Revvity faces boom‑and‑bust grant cycles (U.S. NIH ≈ $49B in 2024) and lumpy capital orders that elongate 6–12‑month sales cycles, pressuring revenue visibility and utilization. Regulatory complexity (IVDR full effect by May 2027; FDA pathways often >90 days) raises time‑to‑market and costs. Supplier concentration and single‑source reagents amplify production and delivery risk.

| Metric | Value |

|---|---|

| NIH funding (2024) | $49B |

| Demo/pilot cycle | 6–12 months |

| IVDR deadline | May 2027 |

Preview Before You Purchase

Revvity SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version.

You're viewing a live preview of the real file—buy to download the full, structured report immediately.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Revvity SWOT Analysis highlights core strengths in diagnostics and life-science tools, alongside market risks and growth opportunities in precision medicine. Want the full picture with actionable insights and financial context? Purchase the complete SWOT for an editable, investor-ready report to plan, pitch, or invest with confidence.

Strengths

Broad, end-to-end life sciences portfolio

Revvity offers reagents, instruments, software and services across discovery-to-diagnostics, creating one-stop coverage that supported cross-selling into pharma, diagnostics, academic and government accounts and helped drive FY2024 revenue of about $4.1B; this breadth deepens account penetration, raises switching costs, and enables bundled workflow solutions rather than isolated point products.

Strong positions in genomics, proteomics, imaging

Revvity’s capabilities across NGS, assay reagents, protein analysis and high‑content imaging align with a multi‑omics market growing ~15% CAGR to 2030; Revvity reported roughly $4.2B revenue in FY2024, with consumables/services driving majority recurring sales, supporting premium pricing, sticky workflows and platform standardization across labs.

Recurring consumables and services revenue

Revvity's large installed base drives repeat reagent and kit purchases, with consumables and services representing over 50% of reported FY2024 revenue of about $3.6 billion, underpinning steady aftermarket demand. Services and software subscriptions deliver higher-margin, predictable cashflows, cushioning macro volatility versus pure capital-equipment peers. This recurring mix boosts customer lifetime value and retention, improving revenue visibility.

Global, diversified customer footprint

Revvity's exposure across pharma, diagnostics labs, academia and government lowers customer concentration risk and smooths demand cycles while geographic diversity spreads regulatory and funding risk across regions; its global distribution and service networks enable cross-market leverage and local teams accelerate adoption and technical support.

- Sector mix: pharma/diagnostics/academia/gov

- Geographic spread reduces single-market risk

- Global distribution + local service = faster adoption

Integrated hardware–software–services solutions

Combining instruments with analytics and informatics creates differentiated workflows that streamline lab processes, while integrated data improves outcomes and speeds decision-making across research and diagnostic use cases. Services augment customer capacity and regulatory compliance, embedding Revvity into critical workflows and raising barriers to entry through recurring revenue and platform stickiness.

- Integrated workflows

- Faster, data-driven decisions

- Services = capacity + compliance

- High switching costs, embedded platform

Multi-omics platform; $4.1B, >50% recurring sales

Revvity generated about $4.1B revenue in FY2024, with consumables and services accounting for over 50% of sales, driving recurring, higher‑margin cashflows. Its integrated instruments, reagents, software and services create sticky workflows and strong cross‑selling across pharma, diagnostics, academia and government. Exposure to a multi‑omics market growing ~15% CAGR to 2030 supports platform demand and pricing power.

| Metric | Value |

|---|---|

| FY2024 revenue | $4.1B |

| Consumables & services | >50% |

| Multi‑omics CAGR (to 2030) | ~15% |

What is included in the product

Provides a concise strategic assessment of Revvity’s internal strengths and weaknesses and external opportunities and threats to inform competitive positioning and growth strategy.

Provides a concise Revvity SWOT matrix for fast alignment across R&D-driven units; visual, editable formatting streamlines strategic updates and creates stakeholder-ready summaries for quick decision-making.

Weaknesses

Exposure to R&D and capital spending cycles

Revvity is exposed to cyclical academic grants and biopharma budgets—U.S. federal R&D via NIH hovers near $49 billion, creating boom‑and‑bust funding windows. Capital equipment orders are lumpy and tied to grant/fiscal timing, so slowdowns elongate sales cycles and defer upgrades. That variability pressures revenue visibility and reduces factory utilization, increasing working capital strain.

Regulatory complexity in diagnostics

Clinical diagnostics face rigorous validation and approvals—FDA 510(k) review is targeted at 90 days while complex pathways and PMAs can extend well beyond a year—raising time-to-market and development costs. Evolving IVDR requirements (full transition by May 2027) and stricter post-market surveillance and quality systems increase ongoing burden and can delay launches, ceding share to faster competitors.

Portfolio integration and focus challenges

Managing a wide catalog risks operational complexity, increasing costs and slow time-to-market as platforms and SKUs multiply. Ensuring interoperability across instruments and software demands sustained investment in R&D and engineering. Product overlap can dilute R&D focus and marketing clarity, and integration missteps have the potential to erode customer experience and retention.

High capital intensity and long sales cycles

- Demo/pilot cycles: 6–12 months

- Higher inventory and install capex

- Extended qualification increases time-to-revenue

- Near-term margin and cash-flow pressure

Dependence on key technologies and suppliers

Revvity depends on limited sources for critical components and reagents, creating single‑point vulnerabilities where supply disruptions can halt production or delay shipments. Rapid technology shifts risk making current platforms obsolete, and vendor concentration increases bargaining leverage against Revvity.

- Single‑source reagents risk

- Production/shipment delays

- Platform obsolescence

- Vendor concentration → bargaining risk

Grant volatility, 6-12m sales cycles, IVDR May 2027, supplier concentration risk

Revvity faces boom‑and‑bust grant cycles (U.S. NIH ≈ $49B in 2024) and lumpy capital orders that elongate 6–12‑month sales cycles, pressuring revenue visibility and utilization. Regulatory complexity (IVDR full effect by May 2027; FDA pathways often >90 days) raises time‑to‑market and costs. Supplier concentration and single‑source reagents amplify production and delivery risk.

| Metric | Value |

|---|---|

| NIH funding (2024) | $49B |

| Demo/pilot cycle | 6–12 months |

| IVDR deadline | May 2027 |

Preview Before You Purchase

Revvity SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version.

You're viewing a live preview of the real file—buy to download the full, structured report immediately.