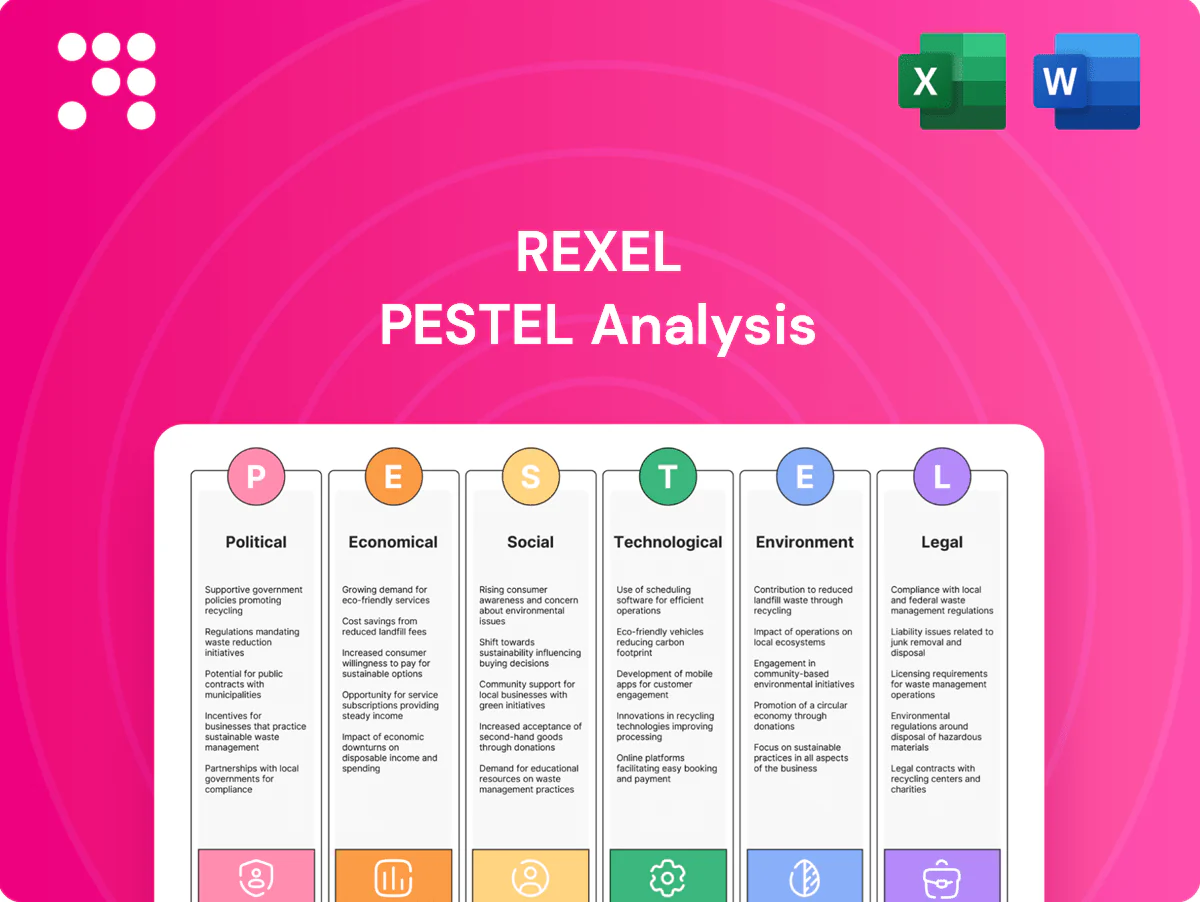

Rexel PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE analysis of Rexel: uncover how political, economic, social, technological, legal and environmental forces shape its operations and growth prospects. Ideal for investors, consultants and strategists, this concise briefing highlights key risks and opportunities. Purchase the full, editable report for the complete data-driven breakdown.

Political factors

Energy transition policies and incentives

National and regional incentives — notably the US Inflation Reduction Act with roughly $369 billion in clean energy tax credits and the EU Fit for 55 target of 55% emissions reduction by 2030 — boost demand for Rexel’s electrification, renewables and efficiency products.

Rapid shifts in subsidy schemes can reallocate project pipelines, while policy stability enables multi‑year contracting with utilities and contractors; global EVs reached about 14% of car sales in 2023, underscoring sustained electrification demand.

Regulatory volatility forces Rexel to maintain agile assortments and dynamic pricing to protect margins and capture re‑scoped project opportunities.

Public infrastructure and grid investment

Government-backed programs such as the US Bipartisan Infrastructure Law (1.2 trillion USD) and EU NextGenerationEU (806.9 billion EUR) expand demand for cables, switchgear and automation, boosting Rexel order pipelines; procurement rules and local-content clauses increasingly dictate supplier selection. Lengthy public approval cycles delay revenue recognition, while proactive engagement with authorities can secure multi-year framework agreements.

Trade policy, tariffs, and localization

Tariffs on electrical components—notably US Section 301 duties of up to 25% on many Chinese electronics—raise landed costs and compress Rexel margins. Localization pushes and public procurement rules incentivize regional sourcing or assembly, shifting sourcing to EMEA/NA hubs. Customs backlogs and import/export controls create supply continuity risks and inventory buildup. Strategic vendor diversification and dual-sourcing lower policy exposure and cost volatility.

Geopolitical supply chain disruptions

Geopolitical conflicts and sanctions have disrupted semiconductors and copper supply chains, with copper trading near US$9,500/ton in 2024 and chip lead times remaining elevated after spiking above 20 weeks in 2021–22. Logistics rerouting has raised distribution costs and extended lead times, pressuring Rexel to meet customer demand for reliable availability on critical electrical projects. Scenario planning and diversified sourcing preserve service levels and limit margin volatility.

- Impact: semiconductors, copper

- Data: copper ~US$9,500/t (2024); chip lead times elevated post-2021

- Response: logistics reroute, scenario planning, diversified sourcing

Workforce and vocational training support

Public funding levels for skilled trades shape installer capacity and product pull-through; World Economic Forum estimates 44% of workers will need reskilling by 2025, increasing demand for funded training. Strong apprenticeship ecosystems accelerate adoption of advanced systems by supplying certified installers. Policy gaps create execution bottlenecks for large programs, while partnerships with training bodies can mitigate shortages.

- Public funding influences installer supply

- 44% reskilling need by 2025 (WEF)

- Apprenticeships speed tech adoption

- Policy gaps = execution risks

- Partnerships reduce shortages

Policy and infrastructure spending drive electrification demand amid copper, tariff and labor risks

Policy-driven clean‑energy funding (US IRA $369B; EU Fit for 55 = 55% by 2030) and infrastructure spending (US $1.2T; NextGenerationEU €806.9B) materially expand Rexel demand for electrification, cables and automation. Tariffs and localization (US Section 301 duties up to 25%) raise landed costs; copper ~US$9,500/t (2024) and EVs ~14% of car sales (2023) heighten supply and margin risk. Skilled‑trade funding/44% reskilling need (WEF 2020) affect installer capacity and execution.

| Item | Key figure |

|---|---|

| US IRA | $369B |

| EU Fit for 55 | −55% by 2030 |

| Infra spending | US $1.2T / €806.9B |

| Copper (2024) | ~$9,500/t |

| EV sales (2023) | ~14% |

What is included in the product

Explores how macro-environmental factors uniquely affect Rexel across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and regional regulatory context; designed for executives and investors to identify threats, opportunities and inform forward-looking strategy.

Concise, visually segmented Rexel PESTLE summary that’s easy to drop into presentations or planning sessions, editable for region- or business-specific notes and quickly shareable for team alignment.

Economic factors

Construction and industrial cycle sensitivity

Residential, commercial and industrial activity drive Rexel's core electrical product demand, with 2024 group sales around €18.3bn highlighting exposure to construction cycles. Slowdowns delay projects and compress volumes while upcycles lift assortments and margins. Backlog visibility of several weeks to months helps balance inventory and working capital. Diversification across end-markets reduces cyclicality and smooths revenue swings.

Interest rates and financing conditions

Higher interest rates—ECB deposit rate around 4% and US fed funds near 5% in 2024–25—pressure real estate development and capex decisions, prompting customers to defer upgrades or choose retrofits over new builds. Supplier financing and extended credit terms become competitive levers as distributors vie for volume. For Rexel, cash discipline and tight working capital control are critical to protect margins and liquidity.

Commodity and input price volatility

Copper, aluminum and plastics swings materially affect supplier pricing and customer budgets: LME copper near USD 9,000/t and aluminum around USD 2,200/t in 2024, while polymer feedstock surged ~15% year-on-year. Rapid moves force Rexel to adopt dynamic pricing and active hedging to protect margins. Transparent surcharges can preserve margin but may reduce demand elasticity. Coordinated category management limits exposure across procurement and sales.

Foreign exchange and global footprint

Rexel’s multi-currency footprint—present in 26 countries with ~2,100 branches—creates translation and transaction risks that can make reported FY2024 sales (€16.3bn) swing independently of underlying demand; FX moves in 2024 materially altered reported growth versus organic trends. Local sourcing and regional inventory reduced import exposure, while a formal hedging framework helped stabilize gross margins through 2024.

- FX exposure: multi-currency operations, 26 countries

- Scale: ~2,100 branches

- FY2024 sales: €16.3bn

- Mitigants: local sourcing, hedging framework stabilizing gross margin

Inflation and logistics costs

Inflation in logistics — freight, warehousing and labor — has pressured Rexel’s operating expenses, even as euro area inflation eased to about 2.5% in 2024 (Eurostat); productivity gains and automation investments are being used to offset margin compression. Customers increasingly demand value engineering and total cost of ownership savings, while service differentiation supports pricing power and contract retention.

- Freight & warehousing inflation pressure

- Automation and productivity to offset costs

- Customer focus on TCO and value engineering

- Service-led pricing resilience

Policy and infrastructure spending drive electrification demand amid copper, tariff and labor risks

Rexel's demand tracks construction and industrial cycles, with FY2024 sales ~€16.3–18.3bn and ~2,100 branches across 26 countries. Higher rates (ECB ~4%, Fed ~5% in 2024–25) and input swings (copper ~USD9,000/t, aluminum ~USD2,200/t) pressure capex and margins, forcing dynamic pricing and hedging. Logistics inflation (~2.5% euro area) drives automation and TCO-led service selling.

| Metric | 2024 |

|---|---|

| Sales | €16.3–18.3bn |

| Branches/Countries | 2,100 / 26 |

| ECB / Fed | ~4% / ~5% |

| Copper / Aluminum | USD9,000/t / USD2,200/t |

Preview Before You Purchase

Rexel PESTLE Analysis

The preview shown here is the exact Rexel PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The file contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or edits; download the final report immediately after payment.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE analysis of Rexel: uncover how political, economic, social, technological, legal and environmental forces shape its operations and growth prospects. Ideal for investors, consultants and strategists, this concise briefing highlights key risks and opportunities. Purchase the full, editable report for the complete data-driven breakdown.

Political factors

Energy transition policies and incentives

National and regional incentives — notably the US Inflation Reduction Act with roughly $369 billion in clean energy tax credits and the EU Fit for 55 target of 55% emissions reduction by 2030 — boost demand for Rexel’s electrification, renewables and efficiency products.

Rapid shifts in subsidy schemes can reallocate project pipelines, while policy stability enables multi‑year contracting with utilities and contractors; global EVs reached about 14% of car sales in 2023, underscoring sustained electrification demand.

Regulatory volatility forces Rexel to maintain agile assortments and dynamic pricing to protect margins and capture re‑scoped project opportunities.

Public infrastructure and grid investment

Government-backed programs such as the US Bipartisan Infrastructure Law (1.2 trillion USD) and EU NextGenerationEU (806.9 billion EUR) expand demand for cables, switchgear and automation, boosting Rexel order pipelines; procurement rules and local-content clauses increasingly dictate supplier selection. Lengthy public approval cycles delay revenue recognition, while proactive engagement with authorities can secure multi-year framework agreements.

Trade policy, tariffs, and localization

Tariffs on electrical components—notably US Section 301 duties of up to 25% on many Chinese electronics—raise landed costs and compress Rexel margins. Localization pushes and public procurement rules incentivize regional sourcing or assembly, shifting sourcing to EMEA/NA hubs. Customs backlogs and import/export controls create supply continuity risks and inventory buildup. Strategic vendor diversification and dual-sourcing lower policy exposure and cost volatility.

Geopolitical supply chain disruptions

Geopolitical conflicts and sanctions have disrupted semiconductors and copper supply chains, with copper trading near US$9,500/ton in 2024 and chip lead times remaining elevated after spiking above 20 weeks in 2021–22. Logistics rerouting has raised distribution costs and extended lead times, pressuring Rexel to meet customer demand for reliable availability on critical electrical projects. Scenario planning and diversified sourcing preserve service levels and limit margin volatility.

- Impact: semiconductors, copper

- Data: copper ~US$9,500/t (2024); chip lead times elevated post-2021

- Response: logistics reroute, scenario planning, diversified sourcing

Workforce and vocational training support

Public funding levels for skilled trades shape installer capacity and product pull-through; World Economic Forum estimates 44% of workers will need reskilling by 2025, increasing demand for funded training. Strong apprenticeship ecosystems accelerate adoption of advanced systems by supplying certified installers. Policy gaps create execution bottlenecks for large programs, while partnerships with training bodies can mitigate shortages.

- Public funding influences installer supply

- 44% reskilling need by 2025 (WEF)

- Apprenticeships speed tech adoption

- Policy gaps = execution risks

- Partnerships reduce shortages

Policy and infrastructure spending drive electrification demand amid copper, tariff and labor risks

Policy-driven clean‑energy funding (US IRA $369B; EU Fit for 55 = 55% by 2030) and infrastructure spending (US $1.2T; NextGenerationEU €806.9B) materially expand Rexel demand for electrification, cables and automation. Tariffs and localization (US Section 301 duties up to 25%) raise landed costs; copper ~US$9,500/t (2024) and EVs ~14% of car sales (2023) heighten supply and margin risk. Skilled‑trade funding/44% reskilling need (WEF 2020) affect installer capacity and execution.

| Item | Key figure |

|---|---|

| US IRA | $369B |

| EU Fit for 55 | −55% by 2030 |

| Infra spending | US $1.2T / €806.9B |

| Copper (2024) | ~$9,500/t |

| EV sales (2023) | ~14% |

What is included in the product

Explores how macro-environmental factors uniquely affect Rexel across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and regional regulatory context; designed for executives and investors to identify threats, opportunities and inform forward-looking strategy.

Concise, visually segmented Rexel PESTLE summary that’s easy to drop into presentations or planning sessions, editable for region- or business-specific notes and quickly shareable for team alignment.

Economic factors

Construction and industrial cycle sensitivity

Residential, commercial and industrial activity drive Rexel's core electrical product demand, with 2024 group sales around €18.3bn highlighting exposure to construction cycles. Slowdowns delay projects and compress volumes while upcycles lift assortments and margins. Backlog visibility of several weeks to months helps balance inventory and working capital. Diversification across end-markets reduces cyclicality and smooths revenue swings.

Interest rates and financing conditions

Higher interest rates—ECB deposit rate around 4% and US fed funds near 5% in 2024–25—pressure real estate development and capex decisions, prompting customers to defer upgrades or choose retrofits over new builds. Supplier financing and extended credit terms become competitive levers as distributors vie for volume. For Rexel, cash discipline and tight working capital control are critical to protect margins and liquidity.

Commodity and input price volatility

Copper, aluminum and plastics swings materially affect supplier pricing and customer budgets: LME copper near USD 9,000/t and aluminum around USD 2,200/t in 2024, while polymer feedstock surged ~15% year-on-year. Rapid moves force Rexel to adopt dynamic pricing and active hedging to protect margins. Transparent surcharges can preserve margin but may reduce demand elasticity. Coordinated category management limits exposure across procurement and sales.

Foreign exchange and global footprint

Rexel’s multi-currency footprint—present in 26 countries with ~2,100 branches—creates translation and transaction risks that can make reported FY2024 sales (€16.3bn) swing independently of underlying demand; FX moves in 2024 materially altered reported growth versus organic trends. Local sourcing and regional inventory reduced import exposure, while a formal hedging framework helped stabilize gross margins through 2024.

- FX exposure: multi-currency operations, 26 countries

- Scale: ~2,100 branches

- FY2024 sales: €16.3bn

- Mitigants: local sourcing, hedging framework stabilizing gross margin

Inflation and logistics costs

Inflation in logistics — freight, warehousing and labor — has pressured Rexel’s operating expenses, even as euro area inflation eased to about 2.5% in 2024 (Eurostat); productivity gains and automation investments are being used to offset margin compression. Customers increasingly demand value engineering and total cost of ownership savings, while service differentiation supports pricing power and contract retention.

- Freight & warehousing inflation pressure

- Automation and productivity to offset costs

- Customer focus on TCO and value engineering

- Service-led pricing resilience

Policy and infrastructure spending drive electrification demand amid copper, tariff and labor risks

Rexel's demand tracks construction and industrial cycles, with FY2024 sales ~€16.3–18.3bn and ~2,100 branches across 26 countries. Higher rates (ECB ~4%, Fed ~5% in 2024–25) and input swings (copper ~USD9,000/t, aluminum ~USD2,200/t) pressure capex and margins, forcing dynamic pricing and hedging. Logistics inflation (~2.5% euro area) drives automation and TCO-led service selling.

| Metric | 2024 |

|---|---|

| Sales | €16.3–18.3bn |

| Branches/Countries | 2,100 / 26 |

| ECB / Fed | ~4% / ~5% |

| Copper / Aluminum | USD9,000/t / USD2,200/t |

Preview Before You Purchase

Rexel PESTLE Analysis

The preview shown here is the exact Rexel PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The file contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or edits; download the final report immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE analysis of Rexel: uncover how political, economic, social, technological, legal and environmental forces shape its operations and growth prospects. Ideal for investors, consultants and strategists, this concise briefing highlights key risks and opportunities. Purchase the full, editable report for the complete data-driven breakdown.

Political factors

Energy transition policies and incentives

National and regional incentives — notably the US Inflation Reduction Act with roughly $369 billion in clean energy tax credits and the EU Fit for 55 target of 55% emissions reduction by 2030 — boost demand for Rexel’s electrification, renewables and efficiency products.

Rapid shifts in subsidy schemes can reallocate project pipelines, while policy stability enables multi‑year contracting with utilities and contractors; global EVs reached about 14% of car sales in 2023, underscoring sustained electrification demand.

Regulatory volatility forces Rexel to maintain agile assortments and dynamic pricing to protect margins and capture re‑scoped project opportunities.

Public infrastructure and grid investment

Government-backed programs such as the US Bipartisan Infrastructure Law (1.2 trillion USD) and EU NextGenerationEU (806.9 billion EUR) expand demand for cables, switchgear and automation, boosting Rexel order pipelines; procurement rules and local-content clauses increasingly dictate supplier selection. Lengthy public approval cycles delay revenue recognition, while proactive engagement with authorities can secure multi-year framework agreements.

Trade policy, tariffs, and localization

Tariffs on electrical components—notably US Section 301 duties of up to 25% on many Chinese electronics—raise landed costs and compress Rexel margins. Localization pushes and public procurement rules incentivize regional sourcing or assembly, shifting sourcing to EMEA/NA hubs. Customs backlogs and import/export controls create supply continuity risks and inventory buildup. Strategic vendor diversification and dual-sourcing lower policy exposure and cost volatility.

Geopolitical supply chain disruptions

Geopolitical conflicts and sanctions have disrupted semiconductors and copper supply chains, with copper trading near US$9,500/ton in 2024 and chip lead times remaining elevated after spiking above 20 weeks in 2021–22. Logistics rerouting has raised distribution costs and extended lead times, pressuring Rexel to meet customer demand for reliable availability on critical electrical projects. Scenario planning and diversified sourcing preserve service levels and limit margin volatility.

- Impact: semiconductors, copper

- Data: copper ~US$9,500/t (2024); chip lead times elevated post-2021

- Response: logistics reroute, scenario planning, diversified sourcing

Workforce and vocational training support

Public funding levels for skilled trades shape installer capacity and product pull-through; World Economic Forum estimates 44% of workers will need reskilling by 2025, increasing demand for funded training. Strong apprenticeship ecosystems accelerate adoption of advanced systems by supplying certified installers. Policy gaps create execution bottlenecks for large programs, while partnerships with training bodies can mitigate shortages.

- Public funding influences installer supply

- 44% reskilling need by 2025 (WEF)

- Apprenticeships speed tech adoption

- Policy gaps = execution risks

- Partnerships reduce shortages

Policy and infrastructure spending drive electrification demand amid copper, tariff and labor risks

Policy-driven clean‑energy funding (US IRA $369B; EU Fit for 55 = 55% by 2030) and infrastructure spending (US $1.2T; NextGenerationEU €806.9B) materially expand Rexel demand for electrification, cables and automation. Tariffs and localization (US Section 301 duties up to 25%) raise landed costs; copper ~US$9,500/t (2024) and EVs ~14% of car sales (2023) heighten supply and margin risk. Skilled‑trade funding/44% reskilling need (WEF 2020) affect installer capacity and execution.

| Item | Key figure |

|---|---|

| US IRA | $369B |

| EU Fit for 55 | −55% by 2030 |

| Infra spending | US $1.2T / €806.9B |

| Copper (2024) | ~$9,500/t |

| EV sales (2023) | ~14% |

What is included in the product

Explores how macro-environmental factors uniquely affect Rexel across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and regional regulatory context; designed for executives and investors to identify threats, opportunities and inform forward-looking strategy.

Concise, visually segmented Rexel PESTLE summary that’s easy to drop into presentations or planning sessions, editable for region- or business-specific notes and quickly shareable for team alignment.

Economic factors

Construction and industrial cycle sensitivity

Residential, commercial and industrial activity drive Rexel's core electrical product demand, with 2024 group sales around €18.3bn highlighting exposure to construction cycles. Slowdowns delay projects and compress volumes while upcycles lift assortments and margins. Backlog visibility of several weeks to months helps balance inventory and working capital. Diversification across end-markets reduces cyclicality and smooths revenue swings.

Interest rates and financing conditions

Higher interest rates—ECB deposit rate around 4% and US fed funds near 5% in 2024–25—pressure real estate development and capex decisions, prompting customers to defer upgrades or choose retrofits over new builds. Supplier financing and extended credit terms become competitive levers as distributors vie for volume. For Rexel, cash discipline and tight working capital control are critical to protect margins and liquidity.

Commodity and input price volatility

Copper, aluminum and plastics swings materially affect supplier pricing and customer budgets: LME copper near USD 9,000/t and aluminum around USD 2,200/t in 2024, while polymer feedstock surged ~15% year-on-year. Rapid moves force Rexel to adopt dynamic pricing and active hedging to protect margins. Transparent surcharges can preserve margin but may reduce demand elasticity. Coordinated category management limits exposure across procurement and sales.

Foreign exchange and global footprint

Rexel’s multi-currency footprint—present in 26 countries with ~2,100 branches—creates translation and transaction risks that can make reported FY2024 sales (€16.3bn) swing independently of underlying demand; FX moves in 2024 materially altered reported growth versus organic trends. Local sourcing and regional inventory reduced import exposure, while a formal hedging framework helped stabilize gross margins through 2024.

- FX exposure: multi-currency operations, 26 countries

- Scale: ~2,100 branches

- FY2024 sales: €16.3bn

- Mitigants: local sourcing, hedging framework stabilizing gross margin

Inflation and logistics costs

Inflation in logistics — freight, warehousing and labor — has pressured Rexel’s operating expenses, even as euro area inflation eased to about 2.5% in 2024 (Eurostat); productivity gains and automation investments are being used to offset margin compression. Customers increasingly demand value engineering and total cost of ownership savings, while service differentiation supports pricing power and contract retention.

- Freight & warehousing inflation pressure

- Automation and productivity to offset costs

- Customer focus on TCO and value engineering

- Service-led pricing resilience

Policy and infrastructure spending drive electrification demand amid copper, tariff and labor risks

Rexel's demand tracks construction and industrial cycles, with FY2024 sales ~€16.3–18.3bn and ~2,100 branches across 26 countries. Higher rates (ECB ~4%, Fed ~5% in 2024–25) and input swings (copper ~USD9,000/t, aluminum ~USD2,200/t) pressure capex and margins, forcing dynamic pricing and hedging. Logistics inflation (~2.5% euro area) drives automation and TCO-led service selling.

| Metric | 2024 |

|---|---|

| Sales | €16.3–18.3bn |

| Branches/Countries | 2,100 / 26 |

| ECB / Fed | ~4% / ~5% |

| Copper / Aluminum | USD9,000/t / USD2,200/t |

Preview Before You Purchase

Rexel PESTLE Analysis

The preview shown here is the exact Rexel PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The file contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or edits; download the final report immediately after payment.