Reinsurance Group of America PESTLE Analysis

Skip the Research. Get the Strategy.

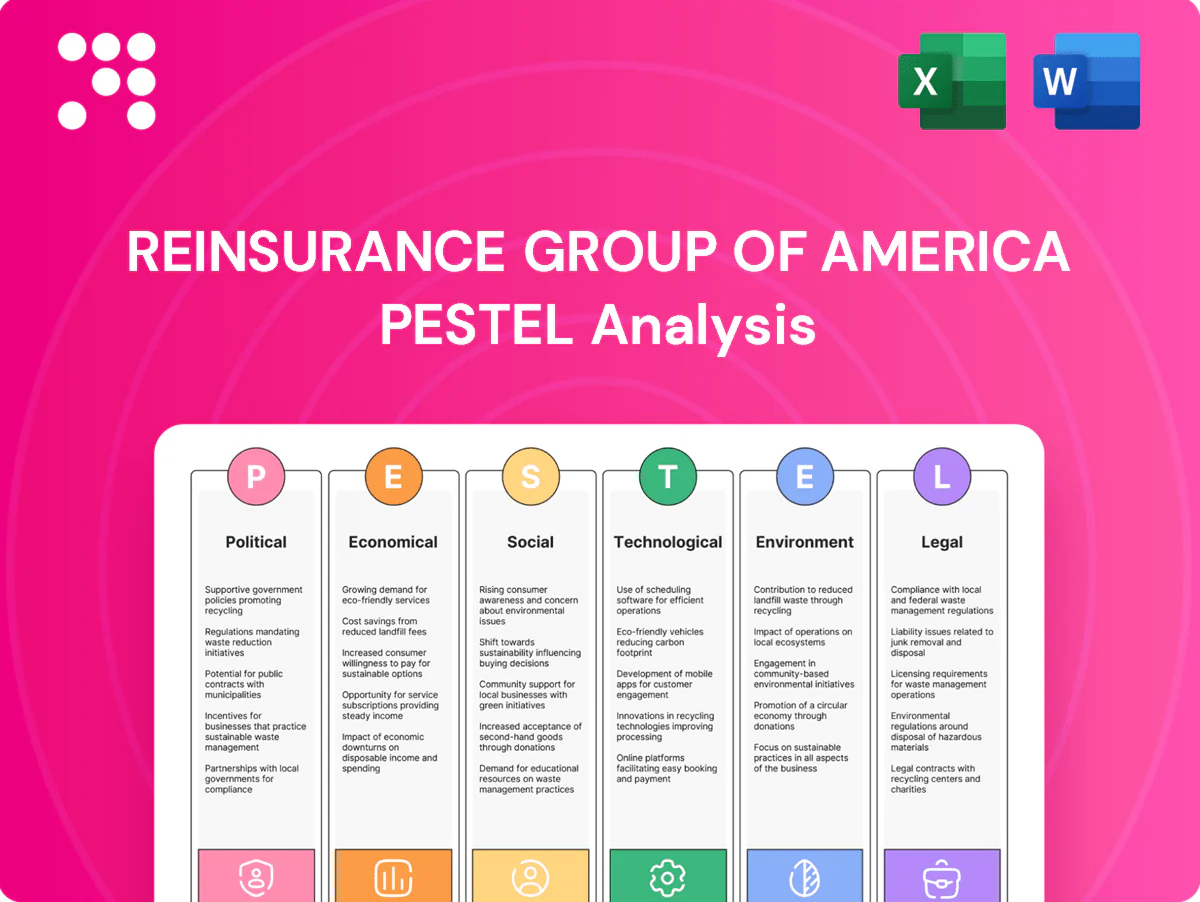

Our PESTLE analysis for Reinsurance Group of America pinpoints political, economic, regulatory, technological, social, and environmental forces shaping its risk and growth profile. Clear, actionable insights reveal where capital and strategy should be focused. Purchase the full report to access deep-dive evidence, forecasts, and ready-to-use strategic recommendations.

Political factors

Cross-border regulatory alignment

Operating in more than 30 jurisdictions, RGA faces divergent supervisory priorities and approval timelines that can take months to years; political shifts can tighten prudential expectations such as capital buffers and liquidity reporting. Harmonization under IAIS frameworks aids consistency, but local implementation remains uneven across the EU, US, Bermuda and APAC. Strategic capital deployment must explicitly account for these regulatory frictions.

Health policy and public programs

Government health reforms alter morbidity trends, product demand and pricing bases; US national health expenditures reached $4.5 trillion in 2022 (18.3% of GDP), and Medicaid expansion has added roughly 20 million enrollees since ACA enactment, changing risk pools. Subsidies or public schemes can crowd in/out private coverage, shifting reinsurance volumes. Pandemic preparedness investments after COVID-19 have increased focus on catastrophe aggregation, so RGA must adapt underwriting and product partnerships accordingly.

Geopolitical risk and sanctions

Conflicts and expanding sanctions regimes strain cedent balance sheets, complicate claims logistics and currency convertibility, and can force RGA to adjust treaty terms; IMF projected global GDP growth at about 3.2% in 2024, signaling uneven recovery across sanction-hit regions. Political instability can disrupt data flows and compliance processes, increasing operational risk. Market exits or exclusions may be required, concentrating exposure elsewhere, so robust scenario governance for accumulations is essential.

Trade and investment policies

Trade and investment barriers such as localization mandates, foreign reinsurer restrictions and limits on capital repatriation materially shape RGA’s footprint, affecting treaty placement and capital efficiency; RGA operates in 25+ markets, so policy reversals create tangible execution risk for ongoing longevity and capital programs.

- Barriers: localization mandates

- Limits: capital repatriation

- Opportunities: financial-center incentives

- Risk: policy reversals

Public sentiment and policymaker scrutiny

Life and health reinsurance are politically sensitive after crises and disasters, because pricing, claims handling and perceived fairness attract regulator and public scrutiny, raising reputational and intervention risks for Reinsurance Group of America.

- Regulatory oversight: scrutiny on pricing and claims

- Reputational risk: public sentiment after disasters

- Populist pressure: potential caps or mandated benefits

- Stakeholder alignment: communications and outcomes

Regulatory fragmentation across 30+ markets and US $4.5T health spend reshape reinsurance

RGA faces divergent prudential regimes across 30+ jurisdictions, lengthening approvals and raising capital/liquidity demands. Government health reforms and US health spend of $4.5T (2022) plus ~20M Medicaid enrollees shift morbidity, pricing and reinsurance volumes. Sanctions, trade limits and capital-repatriation rules across 25+ markets concentrate exposure amid IMF 2024 GDP growth ~3.2%.

| Factor | Metric |

|---|---|

| Jurisdictions | 30+ |

| US health spend (2022) | $4.5T |

| IMF 2024 GDP | ~3.2% |

What is included in the product

Explores how macro-environmental factors uniquely affect Reinsurance Group of America across Political, Economic, Social, Technological, Environmental and Legal dimensions, with sections backed by current data and trends to identify threats and opportunities for executives, consultants and investors.

A concise, visually segmented PESTLE summary for Reinsurance Group of America that quickly aligns teams on external risks and market positioning, is easy to drop into presentations, and allows annotation for specific regions or business lines.

Economic factors

Interest rate and yield curve dynamics

Discount rates determine reserve valuation, pricing and ALM for RGA; mid-2025 U.S. 10-year yields near 4.1% and policy rates around 5.25–5.50% raise discount rates and boost investment income while increasing lapse risk. Curve shape alters lapse timing, hedging costs and reinsurance demand, and RGA’s capital and financial solutions are sensitive to prevailing rate regimes.

Inflation and medical cost trends

General inflation and a medical care services CPI up ~4.5% in 2024 have elevated claims severity and expense ratios for RGA, while hospital and provider cost pressures (hospital services ~5.5% YoY) worsen morbidity lines. Benefit indexation and rising provider charges strain pricing adequacy, which hinges on pass-through mechanisms and contract terms. Vigilant experience monitoring and rapid repricing are critical to restore margin.

Economic cycles and employment

Employment and income levels strongly influence life insurance uptake and lapses; US unemployment averaged 3.7% in 2024, constraining new sales in weak segments. Economic downturns historically raised surrenders (notably during the 2020 pandemic) and increase adverse selection as policyholders cash out. Cedents seek capital relief and risk transfer in stress periods, and RGA can capture countercyclical demand with tailored treaties and capital solutions.

Capital market capacity and retrocession

Capital market capacity and retrocession availability directly constrain RGA’s risk appetite, with tighter markets in 2022–24 reducing cedable limits and raising retro costs; investor demand for insurance-linked structures shapes capacity for longevity and mortality transfers, while spread volatility has complicated synthetic financing and hedging. Prudent limit management remains central to preserving earnings stability.

- Retro availability: affects cedable limits

- Investor sentiment: drives ILS demand for longevity/mortality

- Spread volatility: raises financing costs

- Limit management: preserves earnings

Emerging market growth

Rising middle classes in Asia, Latin America and Africa are widening life and health protection gaps, with Swiss Re Institute estimating a global protection gap in the tens of trillions USD (latest sigma reports through 2023–24 highlight the scale), creating major new addressable markets for RGA.

Currency volatility and macro risk across EMs—notably 2023–24 inflation and FX swings—complicate pricing and solvency management, increasing capital and re-pricing needs for RGA's underwriting.

Local partnerships in distribution and data (insurtechs, bancassurance) unlock scale and customer insight; geographic diversification across EMs bolsters RGA’s portfolio resilience and growth optionality.

- Protection gap: tens of trillions USD (Swiss Re sigma, 2023–24)

- EM macro risk: elevated 2023–24 inflation/FX volatility

- Distribution: insurtech/bancassurance partnerships unlock data

- Diversification: EM exposure improves portfolio resilience

Regulatory fragmentation across 30+ markets and US $4.5T health spend reshape reinsurance

Higher rates (US 10y ~4.1%, policy ~5.25–5.50% mid‑2025) boost investment income but raise lapse and hedging costs; medical inflation (~4.5% in 2024) increases claims severity and expense ratios. Low unemployment (3.7% in 2024) limits new sales; EM FX/inflation volatility and constrained retrocapacity tighten capital and pricing. Large protection gap (tens of trillions USD) drives long‑term growth opportunity.

| Metric | Value (2024–mid‑2025) |

|---|---|

| US 10y yield | ~4.1% |

| Policy/Fed rate | 5.25–5.50% |

| Medical care CPI | ~4.5% |

| Unemployment (US) | 3.7% |

| Protection gap | Tens of trillions USD |

Preview Before You Purchase

Reinsurance Group of America PESTLE Analysis

The preview shown here is the exact Reinsurance Group of America PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content, layout, and insights visible in this sample are the final document delivered upon checkout.

Skip the Research. Get the Strategy.

Our PESTLE analysis for Reinsurance Group of America pinpoints political, economic, regulatory, technological, social, and environmental forces shaping its risk and growth profile. Clear, actionable insights reveal where capital and strategy should be focused. Purchase the full report to access deep-dive evidence, forecasts, and ready-to-use strategic recommendations.

Political factors

Cross-border regulatory alignment

Operating in more than 30 jurisdictions, RGA faces divergent supervisory priorities and approval timelines that can take months to years; political shifts can tighten prudential expectations such as capital buffers and liquidity reporting. Harmonization under IAIS frameworks aids consistency, but local implementation remains uneven across the EU, US, Bermuda and APAC. Strategic capital deployment must explicitly account for these regulatory frictions.

Health policy and public programs

Government health reforms alter morbidity trends, product demand and pricing bases; US national health expenditures reached $4.5 trillion in 2022 (18.3% of GDP), and Medicaid expansion has added roughly 20 million enrollees since ACA enactment, changing risk pools. Subsidies or public schemes can crowd in/out private coverage, shifting reinsurance volumes. Pandemic preparedness investments after COVID-19 have increased focus on catastrophe aggregation, so RGA must adapt underwriting and product partnerships accordingly.

Geopolitical risk and sanctions

Conflicts and expanding sanctions regimes strain cedent balance sheets, complicate claims logistics and currency convertibility, and can force RGA to adjust treaty terms; IMF projected global GDP growth at about 3.2% in 2024, signaling uneven recovery across sanction-hit regions. Political instability can disrupt data flows and compliance processes, increasing operational risk. Market exits or exclusions may be required, concentrating exposure elsewhere, so robust scenario governance for accumulations is essential.

Trade and investment policies

Trade and investment barriers such as localization mandates, foreign reinsurer restrictions and limits on capital repatriation materially shape RGA’s footprint, affecting treaty placement and capital efficiency; RGA operates in 25+ markets, so policy reversals create tangible execution risk for ongoing longevity and capital programs.

- Barriers: localization mandates

- Limits: capital repatriation

- Opportunities: financial-center incentives

- Risk: policy reversals

Public sentiment and policymaker scrutiny

Life and health reinsurance are politically sensitive after crises and disasters, because pricing, claims handling and perceived fairness attract regulator and public scrutiny, raising reputational and intervention risks for Reinsurance Group of America.

- Regulatory oversight: scrutiny on pricing and claims

- Reputational risk: public sentiment after disasters

- Populist pressure: potential caps or mandated benefits

- Stakeholder alignment: communications and outcomes

Regulatory fragmentation across 30+ markets and US $4.5T health spend reshape reinsurance

RGA faces divergent prudential regimes across 30+ jurisdictions, lengthening approvals and raising capital/liquidity demands. Government health reforms and US health spend of $4.5T (2022) plus ~20M Medicaid enrollees shift morbidity, pricing and reinsurance volumes. Sanctions, trade limits and capital-repatriation rules across 25+ markets concentrate exposure amid IMF 2024 GDP growth ~3.2%.

| Factor | Metric |

|---|---|

| Jurisdictions | 30+ |

| US health spend (2022) | $4.5T |

| IMF 2024 GDP | ~3.2% |

What is included in the product

Explores how macro-environmental factors uniquely affect Reinsurance Group of America across Political, Economic, Social, Technological, Environmental and Legal dimensions, with sections backed by current data and trends to identify threats and opportunities for executives, consultants and investors.

A concise, visually segmented PESTLE summary for Reinsurance Group of America that quickly aligns teams on external risks and market positioning, is easy to drop into presentations, and allows annotation for specific regions or business lines.

Economic factors

Interest rate and yield curve dynamics

Discount rates determine reserve valuation, pricing and ALM for RGA; mid-2025 U.S. 10-year yields near 4.1% and policy rates around 5.25–5.50% raise discount rates and boost investment income while increasing lapse risk. Curve shape alters lapse timing, hedging costs and reinsurance demand, and RGA’s capital and financial solutions are sensitive to prevailing rate regimes.

Inflation and medical cost trends

General inflation and a medical care services CPI up ~4.5% in 2024 have elevated claims severity and expense ratios for RGA, while hospital and provider cost pressures (hospital services ~5.5% YoY) worsen morbidity lines. Benefit indexation and rising provider charges strain pricing adequacy, which hinges on pass-through mechanisms and contract terms. Vigilant experience monitoring and rapid repricing are critical to restore margin.

Economic cycles and employment

Employment and income levels strongly influence life insurance uptake and lapses; US unemployment averaged 3.7% in 2024, constraining new sales in weak segments. Economic downturns historically raised surrenders (notably during the 2020 pandemic) and increase adverse selection as policyholders cash out. Cedents seek capital relief and risk transfer in stress periods, and RGA can capture countercyclical demand with tailored treaties and capital solutions.

Capital market capacity and retrocession

Capital market capacity and retrocession availability directly constrain RGA’s risk appetite, with tighter markets in 2022–24 reducing cedable limits and raising retro costs; investor demand for insurance-linked structures shapes capacity for longevity and mortality transfers, while spread volatility has complicated synthetic financing and hedging. Prudent limit management remains central to preserving earnings stability.

- Retro availability: affects cedable limits

- Investor sentiment: drives ILS demand for longevity/mortality

- Spread volatility: raises financing costs

- Limit management: preserves earnings

Emerging market growth

Rising middle classes in Asia, Latin America and Africa are widening life and health protection gaps, with Swiss Re Institute estimating a global protection gap in the tens of trillions USD (latest sigma reports through 2023–24 highlight the scale), creating major new addressable markets for RGA.

Currency volatility and macro risk across EMs—notably 2023–24 inflation and FX swings—complicate pricing and solvency management, increasing capital and re-pricing needs for RGA's underwriting.

Local partnerships in distribution and data (insurtechs, bancassurance) unlock scale and customer insight; geographic diversification across EMs bolsters RGA’s portfolio resilience and growth optionality.

- Protection gap: tens of trillions USD (Swiss Re sigma, 2023–24)

- EM macro risk: elevated 2023–24 inflation/FX volatility

- Distribution: insurtech/bancassurance partnerships unlock data

- Diversification: EM exposure improves portfolio resilience

Regulatory fragmentation across 30+ markets and US $4.5T health spend reshape reinsurance

Higher rates (US 10y ~4.1%, policy ~5.25–5.50% mid‑2025) boost investment income but raise lapse and hedging costs; medical inflation (~4.5% in 2024) increases claims severity and expense ratios. Low unemployment (3.7% in 2024) limits new sales; EM FX/inflation volatility and constrained retrocapacity tighten capital and pricing. Large protection gap (tens of trillions USD) drives long‑term growth opportunity.

| Metric | Value (2024–mid‑2025) |

|---|---|

| US 10y yield | ~4.1% |

| Policy/Fed rate | 5.25–5.50% |

| Medical care CPI | ~4.5% |

| Unemployment (US) | 3.7% |

| Protection gap | Tens of trillions USD |

Preview Before You Purchase

Reinsurance Group of America PESTLE Analysis

The preview shown here is the exact Reinsurance Group of America PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content, layout, and insights visible in this sample are the final document delivered upon checkout.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Our PESTLE analysis for Reinsurance Group of America pinpoints political, economic, regulatory, technological, social, and environmental forces shaping its risk and growth profile. Clear, actionable insights reveal where capital and strategy should be focused. Purchase the full report to access deep-dive evidence, forecasts, and ready-to-use strategic recommendations.

Political factors

Cross-border regulatory alignment

Operating in more than 30 jurisdictions, RGA faces divergent supervisory priorities and approval timelines that can take months to years; political shifts can tighten prudential expectations such as capital buffers and liquidity reporting. Harmonization under IAIS frameworks aids consistency, but local implementation remains uneven across the EU, US, Bermuda and APAC. Strategic capital deployment must explicitly account for these regulatory frictions.

Health policy and public programs

Government health reforms alter morbidity trends, product demand and pricing bases; US national health expenditures reached $4.5 trillion in 2022 (18.3% of GDP), and Medicaid expansion has added roughly 20 million enrollees since ACA enactment, changing risk pools. Subsidies or public schemes can crowd in/out private coverage, shifting reinsurance volumes. Pandemic preparedness investments after COVID-19 have increased focus on catastrophe aggregation, so RGA must adapt underwriting and product partnerships accordingly.

Geopolitical risk and sanctions

Conflicts and expanding sanctions regimes strain cedent balance sheets, complicate claims logistics and currency convertibility, and can force RGA to adjust treaty terms; IMF projected global GDP growth at about 3.2% in 2024, signaling uneven recovery across sanction-hit regions. Political instability can disrupt data flows and compliance processes, increasing operational risk. Market exits or exclusions may be required, concentrating exposure elsewhere, so robust scenario governance for accumulations is essential.

Trade and investment policies

Trade and investment barriers such as localization mandates, foreign reinsurer restrictions and limits on capital repatriation materially shape RGA’s footprint, affecting treaty placement and capital efficiency; RGA operates in 25+ markets, so policy reversals create tangible execution risk for ongoing longevity and capital programs.

- Barriers: localization mandates

- Limits: capital repatriation

- Opportunities: financial-center incentives

- Risk: policy reversals

Public sentiment and policymaker scrutiny

Life and health reinsurance are politically sensitive after crises and disasters, because pricing, claims handling and perceived fairness attract regulator and public scrutiny, raising reputational and intervention risks for Reinsurance Group of America.

- Regulatory oversight: scrutiny on pricing and claims

- Reputational risk: public sentiment after disasters

- Populist pressure: potential caps or mandated benefits

- Stakeholder alignment: communications and outcomes

Regulatory fragmentation across 30+ markets and US $4.5T health spend reshape reinsurance

RGA faces divergent prudential regimes across 30+ jurisdictions, lengthening approvals and raising capital/liquidity demands. Government health reforms and US health spend of $4.5T (2022) plus ~20M Medicaid enrollees shift morbidity, pricing and reinsurance volumes. Sanctions, trade limits and capital-repatriation rules across 25+ markets concentrate exposure amid IMF 2024 GDP growth ~3.2%.

| Factor | Metric |

|---|---|

| Jurisdictions | 30+ |

| US health spend (2022) | $4.5T |

| IMF 2024 GDP | ~3.2% |

What is included in the product

Explores how macro-environmental factors uniquely affect Reinsurance Group of America across Political, Economic, Social, Technological, Environmental and Legal dimensions, with sections backed by current data and trends to identify threats and opportunities for executives, consultants and investors.

A concise, visually segmented PESTLE summary for Reinsurance Group of America that quickly aligns teams on external risks and market positioning, is easy to drop into presentations, and allows annotation for specific regions or business lines.

Economic factors

Interest rate and yield curve dynamics

Discount rates determine reserve valuation, pricing and ALM for RGA; mid-2025 U.S. 10-year yields near 4.1% and policy rates around 5.25–5.50% raise discount rates and boost investment income while increasing lapse risk. Curve shape alters lapse timing, hedging costs and reinsurance demand, and RGA’s capital and financial solutions are sensitive to prevailing rate regimes.

Inflation and medical cost trends

General inflation and a medical care services CPI up ~4.5% in 2024 have elevated claims severity and expense ratios for RGA, while hospital and provider cost pressures (hospital services ~5.5% YoY) worsen morbidity lines. Benefit indexation and rising provider charges strain pricing adequacy, which hinges on pass-through mechanisms and contract terms. Vigilant experience monitoring and rapid repricing are critical to restore margin.

Economic cycles and employment

Employment and income levels strongly influence life insurance uptake and lapses; US unemployment averaged 3.7% in 2024, constraining new sales in weak segments. Economic downturns historically raised surrenders (notably during the 2020 pandemic) and increase adverse selection as policyholders cash out. Cedents seek capital relief and risk transfer in stress periods, and RGA can capture countercyclical demand with tailored treaties and capital solutions.

Capital market capacity and retrocession

Capital market capacity and retrocession availability directly constrain RGA’s risk appetite, with tighter markets in 2022–24 reducing cedable limits and raising retro costs; investor demand for insurance-linked structures shapes capacity for longevity and mortality transfers, while spread volatility has complicated synthetic financing and hedging. Prudent limit management remains central to preserving earnings stability.

- Retro availability: affects cedable limits

- Investor sentiment: drives ILS demand for longevity/mortality

- Spread volatility: raises financing costs

- Limit management: preserves earnings

Emerging market growth

Rising middle classes in Asia, Latin America and Africa are widening life and health protection gaps, with Swiss Re Institute estimating a global protection gap in the tens of trillions USD (latest sigma reports through 2023–24 highlight the scale), creating major new addressable markets for RGA.

Currency volatility and macro risk across EMs—notably 2023–24 inflation and FX swings—complicate pricing and solvency management, increasing capital and re-pricing needs for RGA's underwriting.

Local partnerships in distribution and data (insurtechs, bancassurance) unlock scale and customer insight; geographic diversification across EMs bolsters RGA’s portfolio resilience and growth optionality.

- Protection gap: tens of trillions USD (Swiss Re sigma, 2023–24)

- EM macro risk: elevated 2023–24 inflation/FX volatility

- Distribution: insurtech/bancassurance partnerships unlock data

- Diversification: EM exposure improves portfolio resilience

Regulatory fragmentation across 30+ markets and US $4.5T health spend reshape reinsurance

Higher rates (US 10y ~4.1%, policy ~5.25–5.50% mid‑2025) boost investment income but raise lapse and hedging costs; medical inflation (~4.5% in 2024) increases claims severity and expense ratios. Low unemployment (3.7% in 2024) limits new sales; EM FX/inflation volatility and constrained retrocapacity tighten capital and pricing. Large protection gap (tens of trillions USD) drives long‑term growth opportunity.

| Metric | Value (2024–mid‑2025) |

|---|---|

| US 10y yield | ~4.1% |

| Policy/Fed rate | 5.25–5.50% |

| Medical care CPI | ~4.5% |

| Unemployment (US) | 3.7% |

| Protection gap | Tens of trillions USD |

Preview Before You Purchase

Reinsurance Group of America PESTLE Analysis

The preview shown here is the exact Reinsurance Group of America PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content, layout, and insights visible in this sample are the final document delivered upon checkout.