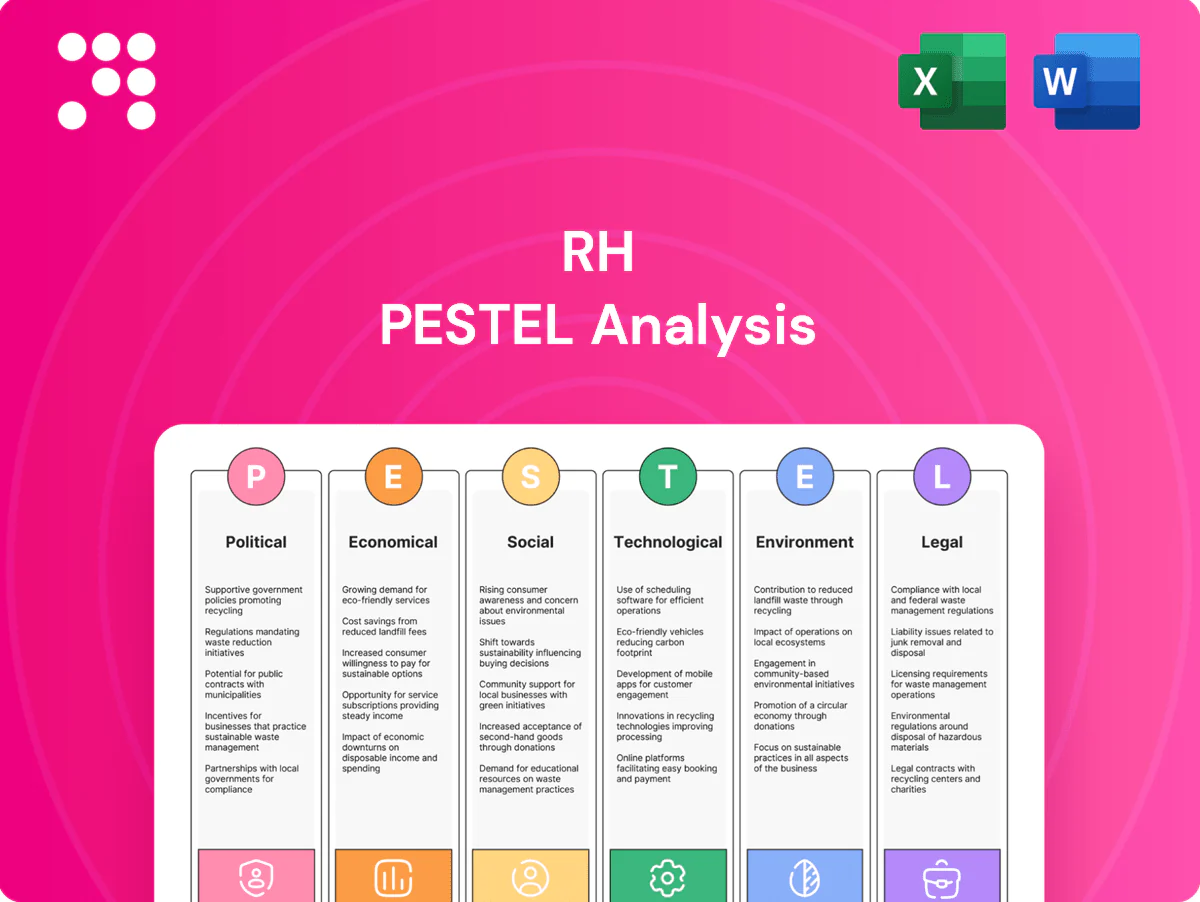

RH PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our RH PESTLE Analysis—concise, data-driven insights on political, economic, social, technological, legal and environmental forces shaping RH’s future; perfect for investors and strategists. Purchase the full report for the complete, editable breakdown and actionable recommendations you can use now.

Political factors

Tariffs on furniture imports

U.S. Section 301 tariffs affecting roughly $370 billion of Chinese goods and EU retaliatory measures, with common rates between 7.5% and 25%, directly raise landed costs for RH’s wood furniture, lighting, and textiles. RH may need to reprice products, re-source from SEA or Latin America, or deploy hedges to protect margins. Persistent trade tensions lengthen lead times and increase inventory risk, so ongoing tariff monitoring and supplier diversification are strategic necessities.

Geopolitical supply chain risks

Political instability in key sourcing regions since 2024 has disrupted timber, metals and fabric availability for furniture makers, pushing RH to re-evaluate lead times. Port congestion and sanction regimes have forced rerouting and added freight premiums, especially after Red Sea transit risks escalated in 2024. RH’s multi-country vendor base must be stress-tested with contingency capacity and scenario plans. Expanded insurance coverage and dual‑sourcing materially reduce disruption severity.

Local zoning and permitting

Opening large-format galleries hinges on municipal approvals, heritage rules, and neighborhood plans; ULI/industry averages show entitlement timelines commonly span 12–24 months in major US/UK cities. Delays increase capex carry costs (construction financing ~7% in 2024–25, ~0.58% monthly), eroding IRR and risking market timing. Community benefit agreements typically add 1–3% in design, traffic, or sustainability obligations. Early stakeholder engagement can cut entitlement time by up to 30%.

Tax policy and incentives

Shifts in corporate tax rates (US federal rate 21%) and changes to capital allowances materially alter RH store rollout ROI and capital allocation, while state+local sales taxes averaging 7.12% (2023) and nexus rules from South Dakota v. Wayfair affect pricing and online margins; targeted local incentives, often in the low‑millions, can materially improve gallery economics and scenario planning helps cushion after‑tax earnings volatility.

- tax-rate: 21% federal

- sales-tax: avg 7.12% (2023)

- local-incentives: low‑millions typical

- planning: scenario stress for after-tax earnings

Labor and immigration policy

Interior design talent and skilled craftspeople are highly sensitive to visa rules; USCIS pending inventory exceeded 6 million in 2023, signaling potential delays for sponsored hires. Federal minimum wage remains $7.25 while state-level increases and benefits mandates in 2024–25 raise store and distribution labor costs and margins. Policy shifts could tighten talent supply in key metros, so workforce planning must build compliance and retention buffers.

- visa backlog: USCIS >6M (2023)

- wage floor: federal $7.25, state hikes through 2024–25

- cost impact: higher labor/benefits raise operating expenses

- action: plan compliance, retention, metro talent sourcing

Tariffs and EU duties raise landed costs; dual-sourcing, hedging and incentives compress ROI

Section 301 tariffs on ~370B USD of Chinese goods and EU retaliatory rates (7.5–25%) raise RH’s landed costs, prompting repricing, re‑sourcing or hedging. Post‑2024 transit, port and sanction risks lengthen lead times; dual‑sourcing and insurance reduce exposure. Entitlement (12–24m) and ~7% capex finance (2024–25) compress gallery ROI; local incentives (low‑millions) can offset.

| Item | Value |

|---|---|

| Tariffs | ~370B USD |

| EU rates | 7.5–25% |

| Capex finance | ~7% (2024–25) |

| Entitlement | 12–24 months |

| Fed tax | 21% |

| Sales tax avg | 7.12% (2023) |

| USCIS backlog | >6M (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact RH, with data-backed trends, forward-looking insights, and industry-specific subpoints to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios.

A concise, visually segmented RH PESTLE summary for quick reference in meetings or presentations; editable for local context and easily dropped into decks to align teams and support external risk discussions.

Economic factors

Housing cycle sensitivity

Luxury home furnishing demand tracks home sales, renovations and new builds; NAR recorded about 3.83 million existing-home sales in 2024 and elevated borrowing costs (30-year fixed around 7% in 2024 per Freddie Mac) depressed big-ticket conversion. Upcycles lift basket sizes, and RH offsets cyclicality with design services and trade programs. Geographic mix and urban versus suburban exposure shape local sensitivity.

Interest rates and wealth effects

Elevated policy rates (federal funds ~5.25–5.50%) and 30-year mortgage rates near 7% have damped purchase and refinance activity, though RH’s affluent cohort remains more resilient to rate shocks. Equity-driven wealth effects and bonus cycles—after strong 2024 equity gains—drive discretionary spend variability. RH should tailor promotions and financing (longer terms, promo APRs) to macro swings. Dynamic pricing and inventory-led markdown control can protect gross margins.

Input and freight cost volatility

Lumber futures swung more than 60% in 2020–22 and metal and textile input volatility continues to pressure gross margins, often moving unit costs by mid-single-digit to low-double-digit percentages. Ocean freight rates collapsed from 2021 peaks (over 80% decline by 2023–24), but last-mile surcharges still materially inflate costs for bulky items. Long-dated purchase orders amplify exposure to these swings; hedging, forwards, and nearshoring are proven levers to stabilize unit economics.

FX and international expansion

FX swings alter RH sourcing costs and foreign gallery profitability, making price localization and natural hedges essential to limit translation risk; RH must adjust assortment and pricing to local elasticity while using treasury to pace hedging with rollout cadence.

- Currency impact: sourcing and margins

- Price localization: reduces translation exposure

- Assortment/pricing: match local elasticity

- Treasury: align hedging with expansion timeline

Affluent consumer confidence

Affluent consumer confidence directly steers RH project scope and pace, with RH reporting roughly $3.0B net revenue in fiscal 2024 as wealthy buyers fund larger remodels and installations; global millionaires reached about 64 million in 2024, underpinning demand. Macroevents commonly pause redecorations or large installs, but curated, limited launches and exclusivity help sustain spend in softer periods; clienteling and private appointments lift conversion rates among HNW clients.

- High-net-worth demand: global millionaires ~64M (2024)

- RH scale: ~ $3.0B net revenue (FY2024)

- Risk: macroevents delay big projects

- Mitigation: curated launches, exclusivity, clienteling, private appointments

Tariffs and EU duties raise landed costs; dual-sourcing, hedging and incentives compress ROI

Luxury-furnishing demand tied to housing cycles (3.83M existing-home sales 2024) and rates (30y ~7%, fed funds 5.25–5.50%), but RH’s affluent base (global millionaires ~64M) and $3.0B FY2024 revenue cushion volatility. Input and freight swings compress margins; nearshoring, hedges and dynamic pricing mitigate. FX and geography require price localization and staged hedging.

| Metric | 2024/2025 |

|---|---|

| Existing-home sales | 3.83M (2024) |

| 30y mortgage | ~7% (2024) |

| Global millionaires | ~64M (2024) |

| RH revenue | $3.0B (FY2024) |

Preview Before You Purchase

RH PESTLE Analysis

The preview shown here is the exact RH PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the file you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured report.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our RH PESTLE Analysis—concise, data-driven insights on political, economic, social, technological, legal and environmental forces shaping RH’s future; perfect for investors and strategists. Purchase the full report for the complete, editable breakdown and actionable recommendations you can use now.

Political factors

Tariffs on furniture imports

U.S. Section 301 tariffs affecting roughly $370 billion of Chinese goods and EU retaliatory measures, with common rates between 7.5% and 25%, directly raise landed costs for RH’s wood furniture, lighting, and textiles. RH may need to reprice products, re-source from SEA or Latin America, or deploy hedges to protect margins. Persistent trade tensions lengthen lead times and increase inventory risk, so ongoing tariff monitoring and supplier diversification are strategic necessities.

Geopolitical supply chain risks

Political instability in key sourcing regions since 2024 has disrupted timber, metals and fabric availability for furniture makers, pushing RH to re-evaluate lead times. Port congestion and sanction regimes have forced rerouting and added freight premiums, especially after Red Sea transit risks escalated in 2024. RH’s multi-country vendor base must be stress-tested with contingency capacity and scenario plans. Expanded insurance coverage and dual‑sourcing materially reduce disruption severity.

Local zoning and permitting

Opening large-format galleries hinges on municipal approvals, heritage rules, and neighborhood plans; ULI/industry averages show entitlement timelines commonly span 12–24 months in major US/UK cities. Delays increase capex carry costs (construction financing ~7% in 2024–25, ~0.58% monthly), eroding IRR and risking market timing. Community benefit agreements typically add 1–3% in design, traffic, or sustainability obligations. Early stakeholder engagement can cut entitlement time by up to 30%.

Tax policy and incentives

Shifts in corporate tax rates (US federal rate 21%) and changes to capital allowances materially alter RH store rollout ROI and capital allocation, while state+local sales taxes averaging 7.12% (2023) and nexus rules from South Dakota v. Wayfair affect pricing and online margins; targeted local incentives, often in the low‑millions, can materially improve gallery economics and scenario planning helps cushion after‑tax earnings volatility.

- tax-rate: 21% federal

- sales-tax: avg 7.12% (2023)

- local-incentives: low‑millions typical

- planning: scenario stress for after-tax earnings

Labor and immigration policy

Interior design talent and skilled craftspeople are highly sensitive to visa rules; USCIS pending inventory exceeded 6 million in 2023, signaling potential delays for sponsored hires. Federal minimum wage remains $7.25 while state-level increases and benefits mandates in 2024–25 raise store and distribution labor costs and margins. Policy shifts could tighten talent supply in key metros, so workforce planning must build compliance and retention buffers.

- visa backlog: USCIS >6M (2023)

- wage floor: federal $7.25, state hikes through 2024–25

- cost impact: higher labor/benefits raise operating expenses

- action: plan compliance, retention, metro talent sourcing

Tariffs and EU duties raise landed costs; dual-sourcing, hedging and incentives compress ROI

Section 301 tariffs on ~370B USD of Chinese goods and EU retaliatory rates (7.5–25%) raise RH’s landed costs, prompting repricing, re‑sourcing or hedging. Post‑2024 transit, port and sanction risks lengthen lead times; dual‑sourcing and insurance reduce exposure. Entitlement (12–24m) and ~7% capex finance (2024–25) compress gallery ROI; local incentives (low‑millions) can offset.

| Item | Value |

|---|---|

| Tariffs | ~370B USD |

| EU rates | 7.5–25% |

| Capex finance | ~7% (2024–25) |

| Entitlement | 12–24 months |

| Fed tax | 21% |

| Sales tax avg | 7.12% (2023) |

| USCIS backlog | >6M (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact RH, with data-backed trends, forward-looking insights, and industry-specific subpoints to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios.

A concise, visually segmented RH PESTLE summary for quick reference in meetings or presentations; editable for local context and easily dropped into decks to align teams and support external risk discussions.

Economic factors

Housing cycle sensitivity

Luxury home furnishing demand tracks home sales, renovations and new builds; NAR recorded about 3.83 million existing-home sales in 2024 and elevated borrowing costs (30-year fixed around 7% in 2024 per Freddie Mac) depressed big-ticket conversion. Upcycles lift basket sizes, and RH offsets cyclicality with design services and trade programs. Geographic mix and urban versus suburban exposure shape local sensitivity.

Interest rates and wealth effects

Elevated policy rates (federal funds ~5.25–5.50%) and 30-year mortgage rates near 7% have damped purchase and refinance activity, though RH’s affluent cohort remains more resilient to rate shocks. Equity-driven wealth effects and bonus cycles—after strong 2024 equity gains—drive discretionary spend variability. RH should tailor promotions and financing (longer terms, promo APRs) to macro swings. Dynamic pricing and inventory-led markdown control can protect gross margins.

Input and freight cost volatility

Lumber futures swung more than 60% in 2020–22 and metal and textile input volatility continues to pressure gross margins, often moving unit costs by mid-single-digit to low-double-digit percentages. Ocean freight rates collapsed from 2021 peaks (over 80% decline by 2023–24), but last-mile surcharges still materially inflate costs for bulky items. Long-dated purchase orders amplify exposure to these swings; hedging, forwards, and nearshoring are proven levers to stabilize unit economics.

FX and international expansion

FX swings alter RH sourcing costs and foreign gallery profitability, making price localization and natural hedges essential to limit translation risk; RH must adjust assortment and pricing to local elasticity while using treasury to pace hedging with rollout cadence.

- Currency impact: sourcing and margins

- Price localization: reduces translation exposure

- Assortment/pricing: match local elasticity

- Treasury: align hedging with expansion timeline

Affluent consumer confidence

Affluent consumer confidence directly steers RH project scope and pace, with RH reporting roughly $3.0B net revenue in fiscal 2024 as wealthy buyers fund larger remodels and installations; global millionaires reached about 64 million in 2024, underpinning demand. Macroevents commonly pause redecorations or large installs, but curated, limited launches and exclusivity help sustain spend in softer periods; clienteling and private appointments lift conversion rates among HNW clients.

- High-net-worth demand: global millionaires ~64M (2024)

- RH scale: ~ $3.0B net revenue (FY2024)

- Risk: macroevents delay big projects

- Mitigation: curated launches, exclusivity, clienteling, private appointments

Tariffs and EU duties raise landed costs; dual-sourcing, hedging and incentives compress ROI

Luxury-furnishing demand tied to housing cycles (3.83M existing-home sales 2024) and rates (30y ~7%, fed funds 5.25–5.50%), but RH’s affluent base (global millionaires ~64M) and $3.0B FY2024 revenue cushion volatility. Input and freight swings compress margins; nearshoring, hedges and dynamic pricing mitigate. FX and geography require price localization and staged hedging.

| Metric | 2024/2025 |

|---|---|

| Existing-home sales | 3.83M (2024) |

| 30y mortgage | ~7% (2024) |

| Global millionaires | ~64M (2024) |

| RH revenue | $3.0B (FY2024) |

Preview Before You Purchase

RH PESTLE Analysis

The preview shown here is the exact RH PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the file you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured report.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our RH PESTLE Analysis—concise, data-driven insights on political, economic, social, technological, legal and environmental forces shaping RH’s future; perfect for investors and strategists. Purchase the full report for the complete, editable breakdown and actionable recommendations you can use now.

Political factors

Tariffs on furniture imports

U.S. Section 301 tariffs affecting roughly $370 billion of Chinese goods and EU retaliatory measures, with common rates between 7.5% and 25%, directly raise landed costs for RH’s wood furniture, lighting, and textiles. RH may need to reprice products, re-source from SEA or Latin America, or deploy hedges to protect margins. Persistent trade tensions lengthen lead times and increase inventory risk, so ongoing tariff monitoring and supplier diversification are strategic necessities.

Geopolitical supply chain risks

Political instability in key sourcing regions since 2024 has disrupted timber, metals and fabric availability for furniture makers, pushing RH to re-evaluate lead times. Port congestion and sanction regimes have forced rerouting and added freight premiums, especially after Red Sea transit risks escalated in 2024. RH’s multi-country vendor base must be stress-tested with contingency capacity and scenario plans. Expanded insurance coverage and dual‑sourcing materially reduce disruption severity.

Local zoning and permitting

Opening large-format galleries hinges on municipal approvals, heritage rules, and neighborhood plans; ULI/industry averages show entitlement timelines commonly span 12–24 months in major US/UK cities. Delays increase capex carry costs (construction financing ~7% in 2024–25, ~0.58% monthly), eroding IRR and risking market timing. Community benefit agreements typically add 1–3% in design, traffic, or sustainability obligations. Early stakeholder engagement can cut entitlement time by up to 30%.

Tax policy and incentives

Shifts in corporate tax rates (US federal rate 21%) and changes to capital allowances materially alter RH store rollout ROI and capital allocation, while state+local sales taxes averaging 7.12% (2023) and nexus rules from South Dakota v. Wayfair affect pricing and online margins; targeted local incentives, often in the low‑millions, can materially improve gallery economics and scenario planning helps cushion after‑tax earnings volatility.

- tax-rate: 21% federal

- sales-tax: avg 7.12% (2023)

- local-incentives: low‑millions typical

- planning: scenario stress for after-tax earnings

Labor and immigration policy

Interior design talent and skilled craftspeople are highly sensitive to visa rules; USCIS pending inventory exceeded 6 million in 2023, signaling potential delays for sponsored hires. Federal minimum wage remains $7.25 while state-level increases and benefits mandates in 2024–25 raise store and distribution labor costs and margins. Policy shifts could tighten talent supply in key metros, so workforce planning must build compliance and retention buffers.

- visa backlog: USCIS >6M (2023)

- wage floor: federal $7.25, state hikes through 2024–25

- cost impact: higher labor/benefits raise operating expenses

- action: plan compliance, retention, metro talent sourcing

Tariffs and EU duties raise landed costs; dual-sourcing, hedging and incentives compress ROI

Section 301 tariffs on ~370B USD of Chinese goods and EU retaliatory rates (7.5–25%) raise RH’s landed costs, prompting repricing, re‑sourcing or hedging. Post‑2024 transit, port and sanction risks lengthen lead times; dual‑sourcing and insurance reduce exposure. Entitlement (12–24m) and ~7% capex finance (2024–25) compress gallery ROI; local incentives (low‑millions) can offset.

| Item | Value |

|---|---|

| Tariffs | ~370B USD |

| EU rates | 7.5–25% |

| Capex finance | ~7% (2024–25) |

| Entitlement | 12–24 months |

| Fed tax | 21% |

| Sales tax avg | 7.12% (2023) |

| USCIS backlog | >6M (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact RH, with data-backed trends, forward-looking insights, and industry-specific subpoints to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios.

A concise, visually segmented RH PESTLE summary for quick reference in meetings or presentations; editable for local context and easily dropped into decks to align teams and support external risk discussions.

Economic factors

Housing cycle sensitivity

Luxury home furnishing demand tracks home sales, renovations and new builds; NAR recorded about 3.83 million existing-home sales in 2024 and elevated borrowing costs (30-year fixed around 7% in 2024 per Freddie Mac) depressed big-ticket conversion. Upcycles lift basket sizes, and RH offsets cyclicality with design services and trade programs. Geographic mix and urban versus suburban exposure shape local sensitivity.

Interest rates and wealth effects

Elevated policy rates (federal funds ~5.25–5.50%) and 30-year mortgage rates near 7% have damped purchase and refinance activity, though RH’s affluent cohort remains more resilient to rate shocks. Equity-driven wealth effects and bonus cycles—after strong 2024 equity gains—drive discretionary spend variability. RH should tailor promotions and financing (longer terms, promo APRs) to macro swings. Dynamic pricing and inventory-led markdown control can protect gross margins.

Input and freight cost volatility

Lumber futures swung more than 60% in 2020–22 and metal and textile input volatility continues to pressure gross margins, often moving unit costs by mid-single-digit to low-double-digit percentages. Ocean freight rates collapsed from 2021 peaks (over 80% decline by 2023–24), but last-mile surcharges still materially inflate costs for bulky items. Long-dated purchase orders amplify exposure to these swings; hedging, forwards, and nearshoring are proven levers to stabilize unit economics.

FX and international expansion

FX swings alter RH sourcing costs and foreign gallery profitability, making price localization and natural hedges essential to limit translation risk; RH must adjust assortment and pricing to local elasticity while using treasury to pace hedging with rollout cadence.

- Currency impact: sourcing and margins

- Price localization: reduces translation exposure

- Assortment/pricing: match local elasticity

- Treasury: align hedging with expansion timeline

Affluent consumer confidence

Affluent consumer confidence directly steers RH project scope and pace, with RH reporting roughly $3.0B net revenue in fiscal 2024 as wealthy buyers fund larger remodels and installations; global millionaires reached about 64 million in 2024, underpinning demand. Macroevents commonly pause redecorations or large installs, but curated, limited launches and exclusivity help sustain spend in softer periods; clienteling and private appointments lift conversion rates among HNW clients.

- High-net-worth demand: global millionaires ~64M (2024)

- RH scale: ~ $3.0B net revenue (FY2024)

- Risk: macroevents delay big projects

- Mitigation: curated launches, exclusivity, clienteling, private appointments

Tariffs and EU duties raise landed costs; dual-sourcing, hedging and incentives compress ROI

Luxury-furnishing demand tied to housing cycles (3.83M existing-home sales 2024) and rates (30y ~7%, fed funds 5.25–5.50%), but RH’s affluent base (global millionaires ~64M) and $3.0B FY2024 revenue cushion volatility. Input and freight swings compress margins; nearshoring, hedges and dynamic pricing mitigate. FX and geography require price localization and staged hedging.

| Metric | 2024/2025 |

|---|---|

| Existing-home sales | 3.83M (2024) |

| 30y mortgage | ~7% (2024) |

| Global millionaires | ~64M (2024) |

| RH revenue | $3.0B (FY2024) |

Preview Before You Purchase

RH PESTLE Analysis

The preview shown here is the exact RH PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the file you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured report.