RHB Bank Business Model Canvas

Business Model Canvas: Strategic Blueprint for a Retail Bank

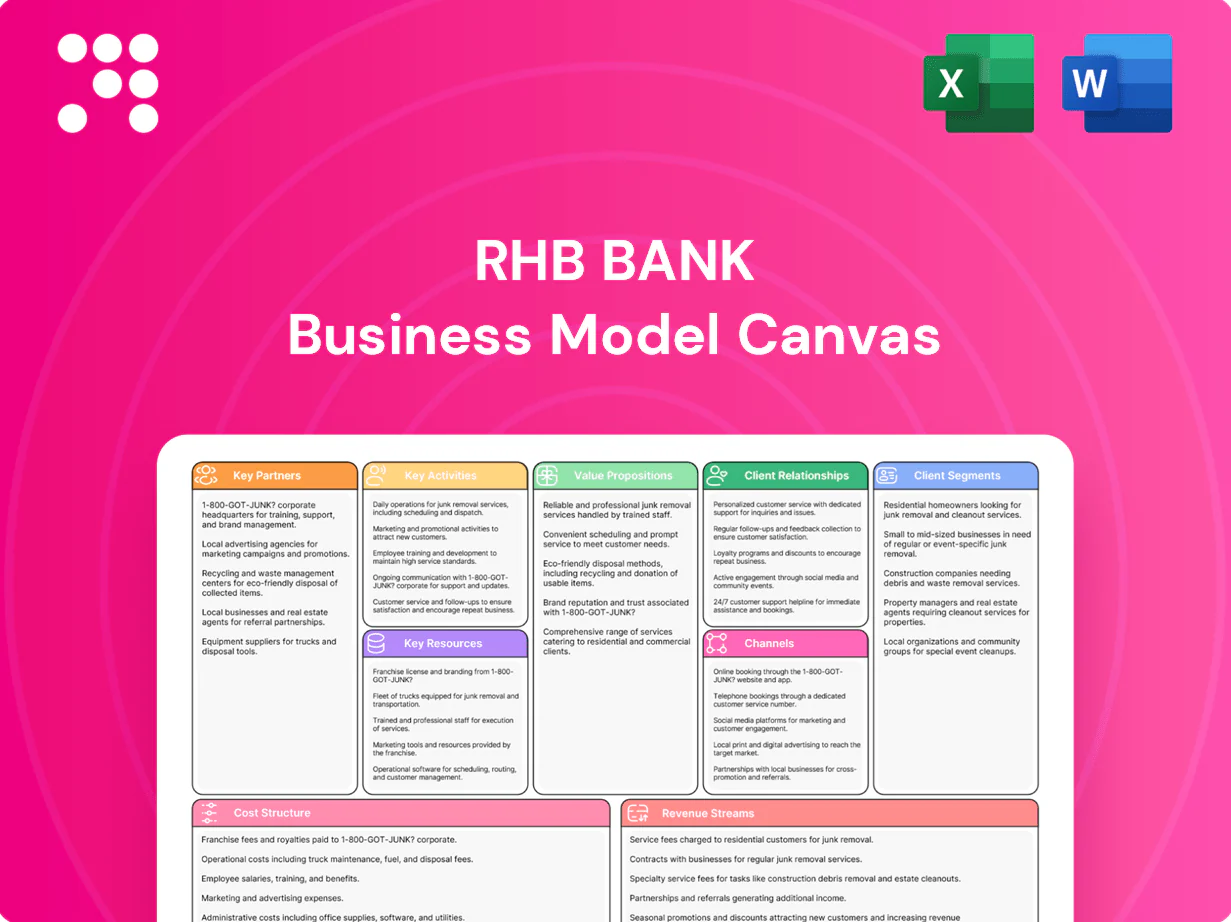

Unlock the strategic blueprint behind RHB Bank with a concise Business Model Canvas that maps its value propositions, customer segments, channels, revenue streams and key partners. This snapshot reveals how RHB captures market share and manages costs. Download the full Word/Excel canvas to benchmark, strategize, or craft investor-ready presentations.

Partnerships

Regulators and payment networks

Partnerships with Bank Negara Malaysia and other regulators ensure RHB holds required licenses, meets capital and AML standards and maintains market stability under ongoing 2024 supervision. Ties with Visa, Mastercard and national rails enable card issuance and seamless transactions—Visa and Mastercard handle over 600 billion transactions annually (2023–24). These links cut payment and remittance friction and underpin real-time payments and expanding open banking services.

Fintech and technology providers

RHB collaborates with fintechs for digital onboarding, eKYC, analytics and embedded finance while core banking, cloud, cybersecurity and API vendors power scalable platforms; digital channels accounted for over 50% of RHB transactions in 2024. Partnerships accelerate innovation and cut time-to-market, lowering unit costs and measurably improving customer experience through faster onboarding and personalized services.

Bancassurance and asset management partners

Tie-ups with insurers and fund managers expand RHB’s wealth and protection suite, with co-designed life, general and takaful solutions across segments; 2024 bancassurance initiatives drove double-digit fee income growth and lifted cross-sell rates, while revenue-sharing models boosted recurring fees. Customers receive integrated advice and seamless claims/transactions through branch, digital and advisor channels.

Correspondent and trade finance banks

Global correspondent and trade finance banks enable RHB to execute cross-border payments, FX and documentary trade efficiently; ICC estimates a global trade finance gap of about 1.7 trillion USD, underscoring demand for such corridors. Shared risk and syndication let RHB participate in larger corporate deals while limiting single-bank exposure. Network access improves speed, corridor coverage, pricing, limits and settlement reliability for RHB clients.

- coverage: expanded corridors and faster settlement

- risk: syndication reduces single-bank exposure

- pricing: better FX and fee terms for clients

- limits: higher facility sizes for corporates

Corporate, SME, and ecosystem partners

Alliances with marketplaces, payroll platforms and supply-chain anchors enable embedded banking at RHB, driving in-app payments, instant payroll access and supplier financing; pilots in 2024 showed merchant transaction volumes rising ~25% and active SME users up ~18% YoY. Co-marketing with merchants and property developers accelerates customer acquisition, while consented data-sharing personalizes offers and credit pricing. These ecosystems increase stickiness and uplift fee and interchange revenue through higher transaction frequency.

- embedded-banking: merchant transactions +25% (pilot 2024)

- SME-engagement: active users +18% YoY (2024)

- co-marketing: lower CAC via merchant channels

- data-consent: personalized offers, better risk pricing

Partnerships drive card & real-time payments; digital >50% txns, trade gap ~$1.7T

RHB’s key partnerships secure licensing/compliance, enable card and real-time payments, accelerate digital services and expand wealth, trade and embedded-banking reach; digital channels >50% of transactions (2024), Visa/Mastercard >600bn txns (2023–24), trade finance gap ~$1.7T (ICC). Partnerships cut costs, speed launches, raise cross-sell and fee income while reducing single-bank risk via syndication.

| Partner Type | Role | 2024 Metric |

|---|---|---|

| Regulators | Licensing, AML, supervision | Ongoing 2024 oversight |

| Card networks | Card issuance, rails | >600bn txns (2023–24) |

| Fintechs/Cloud | Onboarding, APIs | Digital >50% txns (2024) |

| Marketplaces/SME | Embedded banking | Merchant +25% pilot; SME +18% YoY |

What is included in the product

A comprehensive Business Model Canvas for RHB Bank outlining customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations, competitive advantages and SWOT-linked insights for strategic planning and investor presentations.

High-level snapshot of RHB Bank's business model designed to quickly relieve pain points — editable cells clarify value propositions, customer segments, revenue streams and operational gaps for fast decision-making and team alignment.

Activities

Lending and credit underwriting

Origination spans mortgages, auto, personal, SME, corporate and Islamic financing, with RHB handling a broad loan book across retail and wholesale segments. Risk-based pricing and prudent underwriting kept the 2024 group NPL ratio around 1.6%, balancing returns and asset quality. Continuous monitoring and portfolio stress-testing maintain credit discipline. Data-led credit models in 2024 improved approval speed and hit higher predictive accuracy for defaults.

Deposit gathering and payments

RHB, ranked among Malaysia’s top five banks by assets in 2024, grows funding via current, savings and term deposits at competitive rates to lower funding costs. Cards, QR, instant transfers and merchant acquiring drive retail and SME transaction volumes and fee income. Cash management and treasury solutions anchor corporate relationships and deepen balances. Ongoing payment innovation lifts engagement and recurring non‑interest income.

Treasury, risk, and balance sheet management

ALM at RHB optimizes liquidity, interest-rate and FX risks through active gap management and an LCR of 138% in 2024, supporting stable funding. Securities investments and hedging (RM 36.4bn of government and high-grade debt in 2024) smooth earnings and reduce volatility. Robust governance and compliance align with Bank Negara standards and a CET1 ratio of 15.0% in 2024. Regular stress testing and provisioning (coverage ~115%) protect capital.

Wealth, insurance, and investment banking

Wealth, insurance, and investment banking advisory at RHB covers unit trusts, structured products, and protection solutions, aligning portfolio construction with client risk profiles. Bancassurance distribution complements savings and retirement goals through integrated life and takaful offerings. ECM, DCM, and M&A services support corporate clients with capital raising and strategic transactions. Fee-based activities broaden non-interest income streams and reduce reliance on net interest margins.

- Advisory: unit trusts, structured products, protection

- Bancassurance: savings and retirement alignment

- Investment banking: ECM, DCM, M&A support

- Revenue: fee-based diversification

Digital transformation and analytics

Mobile-first journeys streamline onboarding and service, reducing friction and increasing activation rates while APIs enable partnerships and embedded finance to expand distribution and fee income. Advanced analytics power personalization, real-time fraud detection, and predictive collections, improving conversion and loss mitigation. Agile delivery shortens time-to-market for digital products and iterative improvements.

- Mobile-first onboarding

- API partnerships & embedded finance

- Advanced analytics: personalization, fraud, collections

- Agile delivery for faster rollouts

Diversified lending, 1.6% NPL, LCR 138%, CET1 15%

Origination across mortgages, auto, personal, SME, corporate and Islamic financing; 2024 group NPL ~1.6% with data-led credit models improving default prediction. Funding via CASA and term deposits, payment rails and merchant acquiring drive fee income and deposit growth. ALM: LCR 138%, CET1 15.0%, securities RM36.4bn; provisioning coverage ~115%.

| Metric | 2024 |

|---|---|

| NPL ratio | 1.6% |

| LCR | 138% |

| CET1 | 15.0% |

| Securities | RM36.4bn |

| Prov. coverage | ~115% |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual RHB Bank Business Model Canvas you will receive—no mockups or samples. After purchase you'll get the complete, editable file exactly as shown, ready for presentation or editing. What you see is what you’ll own.

Business Model Canvas: Strategic Blueprint for a Retail Bank

Unlock the strategic blueprint behind RHB Bank with a concise Business Model Canvas that maps its value propositions, customer segments, channels, revenue streams and key partners. This snapshot reveals how RHB captures market share and manages costs. Download the full Word/Excel canvas to benchmark, strategize, or craft investor-ready presentations.

Partnerships

Regulators and payment networks

Partnerships with Bank Negara Malaysia and other regulators ensure RHB holds required licenses, meets capital and AML standards and maintains market stability under ongoing 2024 supervision. Ties with Visa, Mastercard and national rails enable card issuance and seamless transactions—Visa and Mastercard handle over 600 billion transactions annually (2023–24). These links cut payment and remittance friction and underpin real-time payments and expanding open banking services.

Fintech and technology providers

RHB collaborates with fintechs for digital onboarding, eKYC, analytics and embedded finance while core banking, cloud, cybersecurity and API vendors power scalable platforms; digital channels accounted for over 50% of RHB transactions in 2024. Partnerships accelerate innovation and cut time-to-market, lowering unit costs and measurably improving customer experience through faster onboarding and personalized services.

Bancassurance and asset management partners

Tie-ups with insurers and fund managers expand RHB’s wealth and protection suite, with co-designed life, general and takaful solutions across segments; 2024 bancassurance initiatives drove double-digit fee income growth and lifted cross-sell rates, while revenue-sharing models boosted recurring fees. Customers receive integrated advice and seamless claims/transactions through branch, digital and advisor channels.

Correspondent and trade finance banks

Global correspondent and trade finance banks enable RHB to execute cross-border payments, FX and documentary trade efficiently; ICC estimates a global trade finance gap of about 1.7 trillion USD, underscoring demand for such corridors. Shared risk and syndication let RHB participate in larger corporate deals while limiting single-bank exposure. Network access improves speed, corridor coverage, pricing, limits and settlement reliability for RHB clients.

- coverage: expanded corridors and faster settlement

- risk: syndication reduces single-bank exposure

- pricing: better FX and fee terms for clients

- limits: higher facility sizes for corporates

Corporate, SME, and ecosystem partners

Alliances with marketplaces, payroll platforms and supply-chain anchors enable embedded banking at RHB, driving in-app payments, instant payroll access and supplier financing; pilots in 2024 showed merchant transaction volumes rising ~25% and active SME users up ~18% YoY. Co-marketing with merchants and property developers accelerates customer acquisition, while consented data-sharing personalizes offers and credit pricing. These ecosystems increase stickiness and uplift fee and interchange revenue through higher transaction frequency.

- embedded-banking: merchant transactions +25% (pilot 2024)

- SME-engagement: active users +18% YoY (2024)

- co-marketing: lower CAC via merchant channels

- data-consent: personalized offers, better risk pricing

Partnerships drive card & real-time payments; digital >50% txns, trade gap ~$1.7T

RHB’s key partnerships secure licensing/compliance, enable card and real-time payments, accelerate digital services and expand wealth, trade and embedded-banking reach; digital channels >50% of transactions (2024), Visa/Mastercard >600bn txns (2023–24), trade finance gap ~$1.7T (ICC). Partnerships cut costs, speed launches, raise cross-sell and fee income while reducing single-bank risk via syndication.

| Partner Type | Role | 2024 Metric |

|---|---|---|

| Regulators | Licensing, AML, supervision | Ongoing 2024 oversight |

| Card networks | Card issuance, rails | >600bn txns (2023–24) |

| Fintechs/Cloud | Onboarding, APIs | Digital >50% txns (2024) |

| Marketplaces/SME | Embedded banking | Merchant +25% pilot; SME +18% YoY |

What is included in the product

A comprehensive Business Model Canvas for RHB Bank outlining customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations, competitive advantages and SWOT-linked insights for strategic planning and investor presentations.

High-level snapshot of RHB Bank's business model designed to quickly relieve pain points — editable cells clarify value propositions, customer segments, revenue streams and operational gaps for fast decision-making and team alignment.

Activities

Lending and credit underwriting

Origination spans mortgages, auto, personal, SME, corporate and Islamic financing, with RHB handling a broad loan book across retail and wholesale segments. Risk-based pricing and prudent underwriting kept the 2024 group NPL ratio around 1.6%, balancing returns and asset quality. Continuous monitoring and portfolio stress-testing maintain credit discipline. Data-led credit models in 2024 improved approval speed and hit higher predictive accuracy for defaults.

Deposit gathering and payments

RHB, ranked among Malaysia’s top five banks by assets in 2024, grows funding via current, savings and term deposits at competitive rates to lower funding costs. Cards, QR, instant transfers and merchant acquiring drive retail and SME transaction volumes and fee income. Cash management and treasury solutions anchor corporate relationships and deepen balances. Ongoing payment innovation lifts engagement and recurring non‑interest income.

Treasury, risk, and balance sheet management

ALM at RHB optimizes liquidity, interest-rate and FX risks through active gap management and an LCR of 138% in 2024, supporting stable funding. Securities investments and hedging (RM 36.4bn of government and high-grade debt in 2024) smooth earnings and reduce volatility. Robust governance and compliance align with Bank Negara standards and a CET1 ratio of 15.0% in 2024. Regular stress testing and provisioning (coverage ~115%) protect capital.

Wealth, insurance, and investment banking

Wealth, insurance, and investment banking advisory at RHB covers unit trusts, structured products, and protection solutions, aligning portfolio construction with client risk profiles. Bancassurance distribution complements savings and retirement goals through integrated life and takaful offerings. ECM, DCM, and M&A services support corporate clients with capital raising and strategic transactions. Fee-based activities broaden non-interest income streams and reduce reliance on net interest margins.

- Advisory: unit trusts, structured products, protection

- Bancassurance: savings and retirement alignment

- Investment banking: ECM, DCM, M&A support

- Revenue: fee-based diversification

Digital transformation and analytics

Mobile-first journeys streamline onboarding and service, reducing friction and increasing activation rates while APIs enable partnerships and embedded finance to expand distribution and fee income. Advanced analytics power personalization, real-time fraud detection, and predictive collections, improving conversion and loss mitigation. Agile delivery shortens time-to-market for digital products and iterative improvements.

- Mobile-first onboarding

- API partnerships & embedded finance

- Advanced analytics: personalization, fraud, collections

- Agile delivery for faster rollouts

Diversified lending, 1.6% NPL, LCR 138%, CET1 15%

Origination across mortgages, auto, personal, SME, corporate and Islamic financing; 2024 group NPL ~1.6% with data-led credit models improving default prediction. Funding via CASA and term deposits, payment rails and merchant acquiring drive fee income and deposit growth. ALM: LCR 138%, CET1 15.0%, securities RM36.4bn; provisioning coverage ~115%.

| Metric | 2024 |

|---|---|

| NPL ratio | 1.6% |

| LCR | 138% |

| CET1 | 15.0% |

| Securities | RM36.4bn |

| Prov. coverage | ~115% |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual RHB Bank Business Model Canvas you will receive—no mockups or samples. After purchase you'll get the complete, editable file exactly as shown, ready for presentation or editing. What you see is what you’ll own.

Description

Business Model Canvas: Strategic Blueprint for a Retail Bank

Unlock the strategic blueprint behind RHB Bank with a concise Business Model Canvas that maps its value propositions, customer segments, channels, revenue streams and key partners. This snapshot reveals how RHB captures market share and manages costs. Download the full Word/Excel canvas to benchmark, strategize, or craft investor-ready presentations.

Partnerships

Regulators and payment networks

Partnerships with Bank Negara Malaysia and other regulators ensure RHB holds required licenses, meets capital and AML standards and maintains market stability under ongoing 2024 supervision. Ties with Visa, Mastercard and national rails enable card issuance and seamless transactions—Visa and Mastercard handle over 600 billion transactions annually (2023–24). These links cut payment and remittance friction and underpin real-time payments and expanding open banking services.

Fintech and technology providers

RHB collaborates with fintechs for digital onboarding, eKYC, analytics and embedded finance while core banking, cloud, cybersecurity and API vendors power scalable platforms; digital channels accounted for over 50% of RHB transactions in 2024. Partnerships accelerate innovation and cut time-to-market, lowering unit costs and measurably improving customer experience through faster onboarding and personalized services.

Bancassurance and asset management partners

Tie-ups with insurers and fund managers expand RHB’s wealth and protection suite, with co-designed life, general and takaful solutions across segments; 2024 bancassurance initiatives drove double-digit fee income growth and lifted cross-sell rates, while revenue-sharing models boosted recurring fees. Customers receive integrated advice and seamless claims/transactions through branch, digital and advisor channels.

Correspondent and trade finance banks

Global correspondent and trade finance banks enable RHB to execute cross-border payments, FX and documentary trade efficiently; ICC estimates a global trade finance gap of about 1.7 trillion USD, underscoring demand for such corridors. Shared risk and syndication let RHB participate in larger corporate deals while limiting single-bank exposure. Network access improves speed, corridor coverage, pricing, limits and settlement reliability for RHB clients.

- coverage: expanded corridors and faster settlement

- risk: syndication reduces single-bank exposure

- pricing: better FX and fee terms for clients

- limits: higher facility sizes for corporates

Corporate, SME, and ecosystem partners

Alliances with marketplaces, payroll platforms and supply-chain anchors enable embedded banking at RHB, driving in-app payments, instant payroll access and supplier financing; pilots in 2024 showed merchant transaction volumes rising ~25% and active SME users up ~18% YoY. Co-marketing with merchants and property developers accelerates customer acquisition, while consented data-sharing personalizes offers and credit pricing. These ecosystems increase stickiness and uplift fee and interchange revenue through higher transaction frequency.

- embedded-banking: merchant transactions +25% (pilot 2024)

- SME-engagement: active users +18% YoY (2024)

- co-marketing: lower CAC via merchant channels

- data-consent: personalized offers, better risk pricing

Partnerships drive card & real-time payments; digital >50% txns, trade gap ~$1.7T

RHB’s key partnerships secure licensing/compliance, enable card and real-time payments, accelerate digital services and expand wealth, trade and embedded-banking reach; digital channels >50% of transactions (2024), Visa/Mastercard >600bn txns (2023–24), trade finance gap ~$1.7T (ICC). Partnerships cut costs, speed launches, raise cross-sell and fee income while reducing single-bank risk via syndication.

| Partner Type | Role | 2024 Metric |

|---|---|---|

| Regulators | Licensing, AML, supervision | Ongoing 2024 oversight |

| Card networks | Card issuance, rails | >600bn txns (2023–24) |

| Fintechs/Cloud | Onboarding, APIs | Digital >50% txns (2024) |

| Marketplaces/SME | Embedded banking | Merchant +25% pilot; SME +18% YoY |

What is included in the product

A comprehensive Business Model Canvas for RHB Bank outlining customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations, competitive advantages and SWOT-linked insights for strategic planning and investor presentations.

High-level snapshot of RHB Bank's business model designed to quickly relieve pain points — editable cells clarify value propositions, customer segments, revenue streams and operational gaps for fast decision-making and team alignment.

Activities

Lending and credit underwriting

Origination spans mortgages, auto, personal, SME, corporate and Islamic financing, with RHB handling a broad loan book across retail and wholesale segments. Risk-based pricing and prudent underwriting kept the 2024 group NPL ratio around 1.6%, balancing returns and asset quality. Continuous monitoring and portfolio stress-testing maintain credit discipline. Data-led credit models in 2024 improved approval speed and hit higher predictive accuracy for defaults.

Deposit gathering and payments

RHB, ranked among Malaysia’s top five banks by assets in 2024, grows funding via current, savings and term deposits at competitive rates to lower funding costs. Cards, QR, instant transfers and merchant acquiring drive retail and SME transaction volumes and fee income. Cash management and treasury solutions anchor corporate relationships and deepen balances. Ongoing payment innovation lifts engagement and recurring non‑interest income.

Treasury, risk, and balance sheet management

ALM at RHB optimizes liquidity, interest-rate and FX risks through active gap management and an LCR of 138% in 2024, supporting stable funding. Securities investments and hedging (RM 36.4bn of government and high-grade debt in 2024) smooth earnings and reduce volatility. Robust governance and compliance align with Bank Negara standards and a CET1 ratio of 15.0% in 2024. Regular stress testing and provisioning (coverage ~115%) protect capital.

Wealth, insurance, and investment banking

Wealth, insurance, and investment banking advisory at RHB covers unit trusts, structured products, and protection solutions, aligning portfolio construction with client risk profiles. Bancassurance distribution complements savings and retirement goals through integrated life and takaful offerings. ECM, DCM, and M&A services support corporate clients with capital raising and strategic transactions. Fee-based activities broaden non-interest income streams and reduce reliance on net interest margins.

- Advisory: unit trusts, structured products, protection

- Bancassurance: savings and retirement alignment

- Investment banking: ECM, DCM, M&A support

- Revenue: fee-based diversification

Digital transformation and analytics

Mobile-first journeys streamline onboarding and service, reducing friction and increasing activation rates while APIs enable partnerships and embedded finance to expand distribution and fee income. Advanced analytics power personalization, real-time fraud detection, and predictive collections, improving conversion and loss mitigation. Agile delivery shortens time-to-market for digital products and iterative improvements.

- Mobile-first onboarding

- API partnerships & embedded finance

- Advanced analytics: personalization, fraud, collections

- Agile delivery for faster rollouts

Diversified lending, 1.6% NPL, LCR 138%, CET1 15%

Origination across mortgages, auto, personal, SME, corporate and Islamic financing; 2024 group NPL ~1.6% with data-led credit models improving default prediction. Funding via CASA and term deposits, payment rails and merchant acquiring drive fee income and deposit growth. ALM: LCR 138%, CET1 15.0%, securities RM36.4bn; provisioning coverage ~115%.

| Metric | 2024 |

|---|---|

| NPL ratio | 1.6% |

| LCR | 138% |

| CET1 | 15.0% |

| Securities | RM36.4bn |

| Prov. coverage | ~115% |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual RHB Bank Business Model Canvas you will receive—no mockups or samples. After purchase you'll get the complete, editable file exactly as shown, ready for presentation or editing. What you see is what you’ll own.