RHB Bank Porter's Five Forces Analysis

Don't Miss the Bigger Picture

RHB Bank faces moderate competitive rivalry, evolving regulatory pressures, and rising digital challengers that are reshaping margins and customer loyalty; supplier and buyer power vary across retail and corporate segments. This snapshot highlights key tensions—unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and strategic recommendations tailored to RHB Bank.

Suppliers Bargaining Power

Diverse funding providers

In 2024 RHB’s raw material—funds—comes from deposits, wholesale debt and interbank lines, with retail deposits fragmented and limiting individual supplier leverage. Large corporates and institutional lenders retain pricing power, pushing up margins. During tighter liquidity cycles in 2024 wholesale funding costs rose and covenants tightened, compressing net interest margins and constraining loan growth.

Core tech and platform vendors

RHB depends on core banking systems, cloud infrastructure and cybersecurity providers, with platform migration typically costing tens of millions of MYR and exposing operations to material implementation risk. Incumbent vendors therefore hold moderate bargaining power. Use of multi-vendor strategies and open APIs limits absolute lock-in. Heightened 2024 regulatory resilience expectations further raise vendor compliance requirements and total cost of ownership.

Specialist talent and compliance

Skilled risk, data and compliance professionals remain scarce for RHB, with 2024 industry surveys indicating about 60–65% of APAC banks reporting critical talent gaps in these areas. Wage inflation and poaching have pushed specialist salaries up an estimated 7–12% year-on-year in 2023–24, elevating supplier power. Outsourcing to managed service providers mitigates hiring risk but creates dependency and adds oversight costs (~5–8% of program spend), requiring sustained capability-building to rebalance bargaining dynamics.

Payment networks and rails

Payment networks, card schemes and national switches set fees and technical standards that create high certification and compliance costs for RHB, and network effects give these suppliers leverage over pricing and access. Domestic rails like DuitNow and FAST lower cross-border costs but force ongoing investment to meet instant-payments and security mandates. Revisions to interchange or switching fees materially affect card unit economics and merchant acquiring margins.

- Card schemes: set certification, interchange and network fees

- National rails: require compliance investment despite lowering execution costs

- Switches: standards and certification amplify supplier leverage

Data, analytics, and credit bureaus

Third-party data from CCRIS (Bank Negara), CTOS and RAMCI fuels RHB’s underwriting, KYC and personalization, making these bureaus influential in credit decisioning.

Unique datasets and proprietary scoring models create switching costs for banks, but multiple bureaus and alternative data providers limit any single supplier’s dominance.

Data localization and consent rules in Malaysia increase compliance overhead and cap long-term supplier entrenchment.

- Suppliers: CCRIS, CTOS, RAMCI

- Power drivers: proprietary scores, data uniqueness

- Checks: alternative data, competing bureaus, regulation

APAC banks face margin squeeze as talent gaps and costly platform migrations bite

Suppliers exert moderate power: retail deposits are fragmented while wholesale lenders and payment networks pressure pricing, compressing margins. Core platform migrations cost tens of millions MYR and vendors hold leverage; talent gaps affect 60–65% of APAC banks, lifting specialist pay 7–12% (2023–24) and outsourcing oversight costs ~5–8% of spend.

| Driver | 2024 metric |

|---|---|

| Talent gaps | 60–65% |

| Salary inflation | +7–12% |

| Outsourcing oversight | ~5–8% of spend |

| Migration cost | tens of millions MYR |

What is included in the product

Tailored Porter's Five Forces analysis for RHB Bank revealing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and strategic levers to defend market share and profitability.

Clear, one-sheet Porter's Five Forces for RHB Bank that highlights competitive pressures and relief strategies—ready to drop into decks for fast, confident decisions.

Customers Bargaining Power

Multi-banked retail customers

Multi-banked retail customers increasingly compare rates and fees across apps, heightening price sensitivity; low switching frictions in payments and deposits amplify their bargaining power, while loyalty depends on UX, rewards and ecosystem tie-ins, and churn risk rises sharply if RHB’s digital experience lags peer offerings.

SME and corporate negotiators

Larger SME and corporate negotiators routinely bundle cash management, lending and markets services to demand discounts, with Malaysian SMEs representing 98.5% of business establishments and contributing roughly 38% of GDP in 2024. Mandate-based services and syndications intensify fee competition, while deeper relationships and sector expertise can justify pricing premia; complex needs increase client stickiness but also negotiation leverage.

Transparency and comparison tools

Aggregators and comparison sites expose pricing and service quality, with studies showing about 77% of consumers consult online reviews before financial purchases, intensifying price sensitivity. This transparency has compressed spreads in commoditized products, often by as much as 50 basis points in competitive markets. Reviews and social proof raise acquisition costs through higher service expectations and churn. RHB must differentiate on value, speed, and advisory quality to defend margins.

Wealth and insurance clients

Affluent and insurance clients demand tailored portfolios, shoppable fees and open-architecture products and can reallocate assets rapidly to chase performance or cut costs; advisory quality and platform breadth partially offset this bargaining power, while performance shortfalls prompt repricing pressure or outflows.

- Tailored portfolios

- Shoppable fees

- Open architecture

- Advisory mitigates churn

Digital service expectations

RHB faces customers demanding instant onboarding, 24/7 support and seamless omni‑channel journeys, where service-level agreements such as 99.9% uptime and sub‑1 minute live response time are becoming the competitive baseline in 2024. Any friction drives rapid switching to competitors or fintechs, with industry observations showing up to 30% higher churn when digital UX gaps exist. Continuous feature delivery and rapid API-led enhancements steadily erode buyer leverage born of UX shortfalls.

- instant onboarding

- 24/7 support

- omni-channel

- SLA = 99.9% uptime, <1 min response

- continuous delivery reduces churn

Customers hold price power: 77% consult reviews; SMEs cut spreads 50bps

Customers wield strong price and service leverage: retail multi-banked users and 77% who consult reviews drive price sensitivity and up to 30% higher churn when UX lags. SMEs (98.5% of firms; ~38% of 2024 GDP) bundle services to extract discounts, compressing spreads by as much as 50 bps. Affluent clients demand open-architecture advice, raising retention risk if performance or fees slip.

| Metric | 2024 Value | Impact |

|---|---|---|

| SME share of firms / GDP | 98.5% / ~38% | High negotiation power |

| Consumers consulting reviews | 77% | Increases price transparency |

| Spread compression | Up to 50 bps | Margin pressure |

| Churn increase with poor UX | Up to 30% | Revenue at risk |

| SLA expectations | 99.9% uptime; <1 min response | Operational demand |

Preview the Actual Deliverable

RHB Bank Porter's Five Forces Analysis

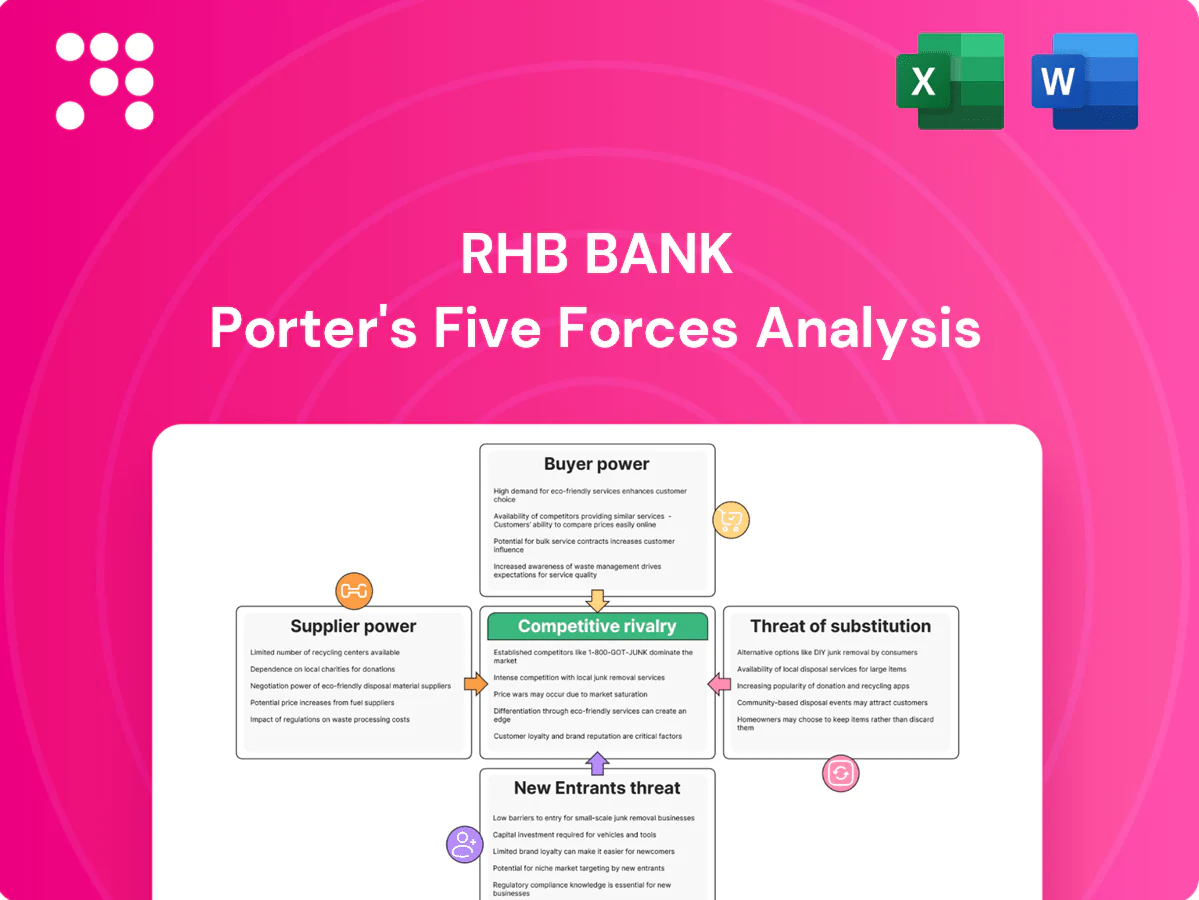

This preview shows the exact RHB Bank Porter's Five Forces analysis you'll receive immediately after purchase—fully written, formatted, and ready to use. It contains the complete assessment of competitive rivalry, buyer and supplier power, threats of new entry and substitutes, and clear strategic implications. No placeholders or samples; download access is instant.

Don't Miss the Bigger Picture

RHB Bank faces moderate competitive rivalry, evolving regulatory pressures, and rising digital challengers that are reshaping margins and customer loyalty; supplier and buyer power vary across retail and corporate segments. This snapshot highlights key tensions—unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and strategic recommendations tailored to RHB Bank.

Suppliers Bargaining Power

Diverse funding providers

In 2024 RHB’s raw material—funds—comes from deposits, wholesale debt and interbank lines, with retail deposits fragmented and limiting individual supplier leverage. Large corporates and institutional lenders retain pricing power, pushing up margins. During tighter liquidity cycles in 2024 wholesale funding costs rose and covenants tightened, compressing net interest margins and constraining loan growth.

Core tech and platform vendors

RHB depends on core banking systems, cloud infrastructure and cybersecurity providers, with platform migration typically costing tens of millions of MYR and exposing operations to material implementation risk. Incumbent vendors therefore hold moderate bargaining power. Use of multi-vendor strategies and open APIs limits absolute lock-in. Heightened 2024 regulatory resilience expectations further raise vendor compliance requirements and total cost of ownership.

Specialist talent and compliance

Skilled risk, data and compliance professionals remain scarce for RHB, with 2024 industry surveys indicating about 60–65% of APAC banks reporting critical talent gaps in these areas. Wage inflation and poaching have pushed specialist salaries up an estimated 7–12% year-on-year in 2023–24, elevating supplier power. Outsourcing to managed service providers mitigates hiring risk but creates dependency and adds oversight costs (~5–8% of program spend), requiring sustained capability-building to rebalance bargaining dynamics.

Payment networks and rails

Payment networks, card schemes and national switches set fees and technical standards that create high certification and compliance costs for RHB, and network effects give these suppliers leverage over pricing and access. Domestic rails like DuitNow and FAST lower cross-border costs but force ongoing investment to meet instant-payments and security mandates. Revisions to interchange or switching fees materially affect card unit economics and merchant acquiring margins.

- Card schemes: set certification, interchange and network fees

- National rails: require compliance investment despite lowering execution costs

- Switches: standards and certification amplify supplier leverage

Data, analytics, and credit bureaus

Third-party data from CCRIS (Bank Negara), CTOS and RAMCI fuels RHB’s underwriting, KYC and personalization, making these bureaus influential in credit decisioning.

Unique datasets and proprietary scoring models create switching costs for banks, but multiple bureaus and alternative data providers limit any single supplier’s dominance.

Data localization and consent rules in Malaysia increase compliance overhead and cap long-term supplier entrenchment.

- Suppliers: CCRIS, CTOS, RAMCI

- Power drivers: proprietary scores, data uniqueness

- Checks: alternative data, competing bureaus, regulation

APAC banks face margin squeeze as talent gaps and costly platform migrations bite

Suppliers exert moderate power: retail deposits are fragmented while wholesale lenders and payment networks pressure pricing, compressing margins. Core platform migrations cost tens of millions MYR and vendors hold leverage; talent gaps affect 60–65% of APAC banks, lifting specialist pay 7–12% (2023–24) and outsourcing oversight costs ~5–8% of spend.

| Driver | 2024 metric |

|---|---|

| Talent gaps | 60–65% |

| Salary inflation | +7–12% |

| Outsourcing oversight | ~5–8% of spend |

| Migration cost | tens of millions MYR |

What is included in the product

Tailored Porter's Five Forces analysis for RHB Bank revealing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and strategic levers to defend market share and profitability.

Clear, one-sheet Porter's Five Forces for RHB Bank that highlights competitive pressures and relief strategies—ready to drop into decks for fast, confident decisions.

Customers Bargaining Power

Multi-banked retail customers

Multi-banked retail customers increasingly compare rates and fees across apps, heightening price sensitivity; low switching frictions in payments and deposits amplify their bargaining power, while loyalty depends on UX, rewards and ecosystem tie-ins, and churn risk rises sharply if RHB’s digital experience lags peer offerings.

SME and corporate negotiators

Larger SME and corporate negotiators routinely bundle cash management, lending and markets services to demand discounts, with Malaysian SMEs representing 98.5% of business establishments and contributing roughly 38% of GDP in 2024. Mandate-based services and syndications intensify fee competition, while deeper relationships and sector expertise can justify pricing premia; complex needs increase client stickiness but also negotiation leverage.

Transparency and comparison tools

Aggregators and comparison sites expose pricing and service quality, with studies showing about 77% of consumers consult online reviews before financial purchases, intensifying price sensitivity. This transparency has compressed spreads in commoditized products, often by as much as 50 basis points in competitive markets. Reviews and social proof raise acquisition costs through higher service expectations and churn. RHB must differentiate on value, speed, and advisory quality to defend margins.

Wealth and insurance clients

Affluent and insurance clients demand tailored portfolios, shoppable fees and open-architecture products and can reallocate assets rapidly to chase performance or cut costs; advisory quality and platform breadth partially offset this bargaining power, while performance shortfalls prompt repricing pressure or outflows.

- Tailored portfolios

- Shoppable fees

- Open architecture

- Advisory mitigates churn

Digital service expectations

RHB faces customers demanding instant onboarding, 24/7 support and seamless omni‑channel journeys, where service-level agreements such as 99.9% uptime and sub‑1 minute live response time are becoming the competitive baseline in 2024. Any friction drives rapid switching to competitors or fintechs, with industry observations showing up to 30% higher churn when digital UX gaps exist. Continuous feature delivery and rapid API-led enhancements steadily erode buyer leverage born of UX shortfalls.

- instant onboarding

- 24/7 support

- omni-channel

- SLA = 99.9% uptime, <1 min response

- continuous delivery reduces churn

Customers hold price power: 77% consult reviews; SMEs cut spreads 50bps

Customers wield strong price and service leverage: retail multi-banked users and 77% who consult reviews drive price sensitivity and up to 30% higher churn when UX lags. SMEs (98.5% of firms; ~38% of 2024 GDP) bundle services to extract discounts, compressing spreads by as much as 50 bps. Affluent clients demand open-architecture advice, raising retention risk if performance or fees slip.

| Metric | 2024 Value | Impact |

|---|---|---|

| SME share of firms / GDP | 98.5% / ~38% | High negotiation power |

| Consumers consulting reviews | 77% | Increases price transparency |

| Spread compression | Up to 50 bps | Margin pressure |

| Churn increase with poor UX | Up to 30% | Revenue at risk |

| SLA expectations | 99.9% uptime; <1 min response | Operational demand |

Preview the Actual Deliverable

RHB Bank Porter's Five Forces Analysis

This preview shows the exact RHB Bank Porter's Five Forces analysis you'll receive immediately after purchase—fully written, formatted, and ready to use. It contains the complete assessment of competitive rivalry, buyer and supplier power, threats of new entry and substitutes, and clear strategic implications. No placeholders or samples; download access is instant.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

RHB Bank faces moderate competitive rivalry, evolving regulatory pressures, and rising digital challengers that are reshaping margins and customer loyalty; supplier and buyer power vary across retail and corporate segments. This snapshot highlights key tensions—unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and strategic recommendations tailored to RHB Bank.

Suppliers Bargaining Power

Diverse funding providers

In 2024 RHB’s raw material—funds—comes from deposits, wholesale debt and interbank lines, with retail deposits fragmented and limiting individual supplier leverage. Large corporates and institutional lenders retain pricing power, pushing up margins. During tighter liquidity cycles in 2024 wholesale funding costs rose and covenants tightened, compressing net interest margins and constraining loan growth.

Core tech and platform vendors

RHB depends on core banking systems, cloud infrastructure and cybersecurity providers, with platform migration typically costing tens of millions of MYR and exposing operations to material implementation risk. Incumbent vendors therefore hold moderate bargaining power. Use of multi-vendor strategies and open APIs limits absolute lock-in. Heightened 2024 regulatory resilience expectations further raise vendor compliance requirements and total cost of ownership.

Specialist talent and compliance

Skilled risk, data and compliance professionals remain scarce for RHB, with 2024 industry surveys indicating about 60–65% of APAC banks reporting critical talent gaps in these areas. Wage inflation and poaching have pushed specialist salaries up an estimated 7–12% year-on-year in 2023–24, elevating supplier power. Outsourcing to managed service providers mitigates hiring risk but creates dependency and adds oversight costs (~5–8% of program spend), requiring sustained capability-building to rebalance bargaining dynamics.

Payment networks and rails

Payment networks, card schemes and national switches set fees and technical standards that create high certification and compliance costs for RHB, and network effects give these suppliers leverage over pricing and access. Domestic rails like DuitNow and FAST lower cross-border costs but force ongoing investment to meet instant-payments and security mandates. Revisions to interchange or switching fees materially affect card unit economics and merchant acquiring margins.

- Card schemes: set certification, interchange and network fees

- National rails: require compliance investment despite lowering execution costs

- Switches: standards and certification amplify supplier leverage

Data, analytics, and credit bureaus

Third-party data from CCRIS (Bank Negara), CTOS and RAMCI fuels RHB’s underwriting, KYC and personalization, making these bureaus influential in credit decisioning.

Unique datasets and proprietary scoring models create switching costs for banks, but multiple bureaus and alternative data providers limit any single supplier’s dominance.

Data localization and consent rules in Malaysia increase compliance overhead and cap long-term supplier entrenchment.

- Suppliers: CCRIS, CTOS, RAMCI

- Power drivers: proprietary scores, data uniqueness

- Checks: alternative data, competing bureaus, regulation

APAC banks face margin squeeze as talent gaps and costly platform migrations bite

Suppliers exert moderate power: retail deposits are fragmented while wholesale lenders and payment networks pressure pricing, compressing margins. Core platform migrations cost tens of millions MYR and vendors hold leverage; talent gaps affect 60–65% of APAC banks, lifting specialist pay 7–12% (2023–24) and outsourcing oversight costs ~5–8% of spend.

| Driver | 2024 metric |

|---|---|

| Talent gaps | 60–65% |

| Salary inflation | +7–12% |

| Outsourcing oversight | ~5–8% of spend |

| Migration cost | tens of millions MYR |

What is included in the product

Tailored Porter's Five Forces analysis for RHB Bank revealing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and strategic levers to defend market share and profitability.

Clear, one-sheet Porter's Five Forces for RHB Bank that highlights competitive pressures and relief strategies—ready to drop into decks for fast, confident decisions.

Customers Bargaining Power

Multi-banked retail customers

Multi-banked retail customers increasingly compare rates and fees across apps, heightening price sensitivity; low switching frictions in payments and deposits amplify their bargaining power, while loyalty depends on UX, rewards and ecosystem tie-ins, and churn risk rises sharply if RHB’s digital experience lags peer offerings.

SME and corporate negotiators

Larger SME and corporate negotiators routinely bundle cash management, lending and markets services to demand discounts, with Malaysian SMEs representing 98.5% of business establishments and contributing roughly 38% of GDP in 2024. Mandate-based services and syndications intensify fee competition, while deeper relationships and sector expertise can justify pricing premia; complex needs increase client stickiness but also negotiation leverage.

Transparency and comparison tools

Aggregators and comparison sites expose pricing and service quality, with studies showing about 77% of consumers consult online reviews before financial purchases, intensifying price sensitivity. This transparency has compressed spreads in commoditized products, often by as much as 50 basis points in competitive markets. Reviews and social proof raise acquisition costs through higher service expectations and churn. RHB must differentiate on value, speed, and advisory quality to defend margins.

Wealth and insurance clients

Affluent and insurance clients demand tailored portfolios, shoppable fees and open-architecture products and can reallocate assets rapidly to chase performance or cut costs; advisory quality and platform breadth partially offset this bargaining power, while performance shortfalls prompt repricing pressure or outflows.

- Tailored portfolios

- Shoppable fees

- Open architecture

- Advisory mitigates churn

Digital service expectations

RHB faces customers demanding instant onboarding, 24/7 support and seamless omni‑channel journeys, where service-level agreements such as 99.9% uptime and sub‑1 minute live response time are becoming the competitive baseline in 2024. Any friction drives rapid switching to competitors or fintechs, with industry observations showing up to 30% higher churn when digital UX gaps exist. Continuous feature delivery and rapid API-led enhancements steadily erode buyer leverage born of UX shortfalls.

- instant onboarding

- 24/7 support

- omni-channel

- SLA = 99.9% uptime, <1 min response

- continuous delivery reduces churn

Customers hold price power: 77% consult reviews; SMEs cut spreads 50bps

Customers wield strong price and service leverage: retail multi-banked users and 77% who consult reviews drive price sensitivity and up to 30% higher churn when UX lags. SMEs (98.5% of firms; ~38% of 2024 GDP) bundle services to extract discounts, compressing spreads by as much as 50 bps. Affluent clients demand open-architecture advice, raising retention risk if performance or fees slip.

| Metric | 2024 Value | Impact |

|---|---|---|

| SME share of firms / GDP | 98.5% / ~38% | High negotiation power |

| Consumers consulting reviews | 77% | Increases price transparency |

| Spread compression | Up to 50 bps | Margin pressure |

| Churn increase with poor UX | Up to 30% | Revenue at risk |

| SLA expectations | 99.9% uptime; <1 min response | Operational demand |

Preview the Actual Deliverable

RHB Bank Porter's Five Forces Analysis

This preview shows the exact RHB Bank Porter's Five Forces analysis you'll receive immediately after purchase—fully written, formatted, and ready to use. It contains the complete assessment of competitive rivalry, buyer and supplier power, threats of new entry and substitutes, and clear strategic implications. No placeholders or samples; download access is instant.