Ribbon SWOT Analysis

Your Strategic Toolkit Starts Here

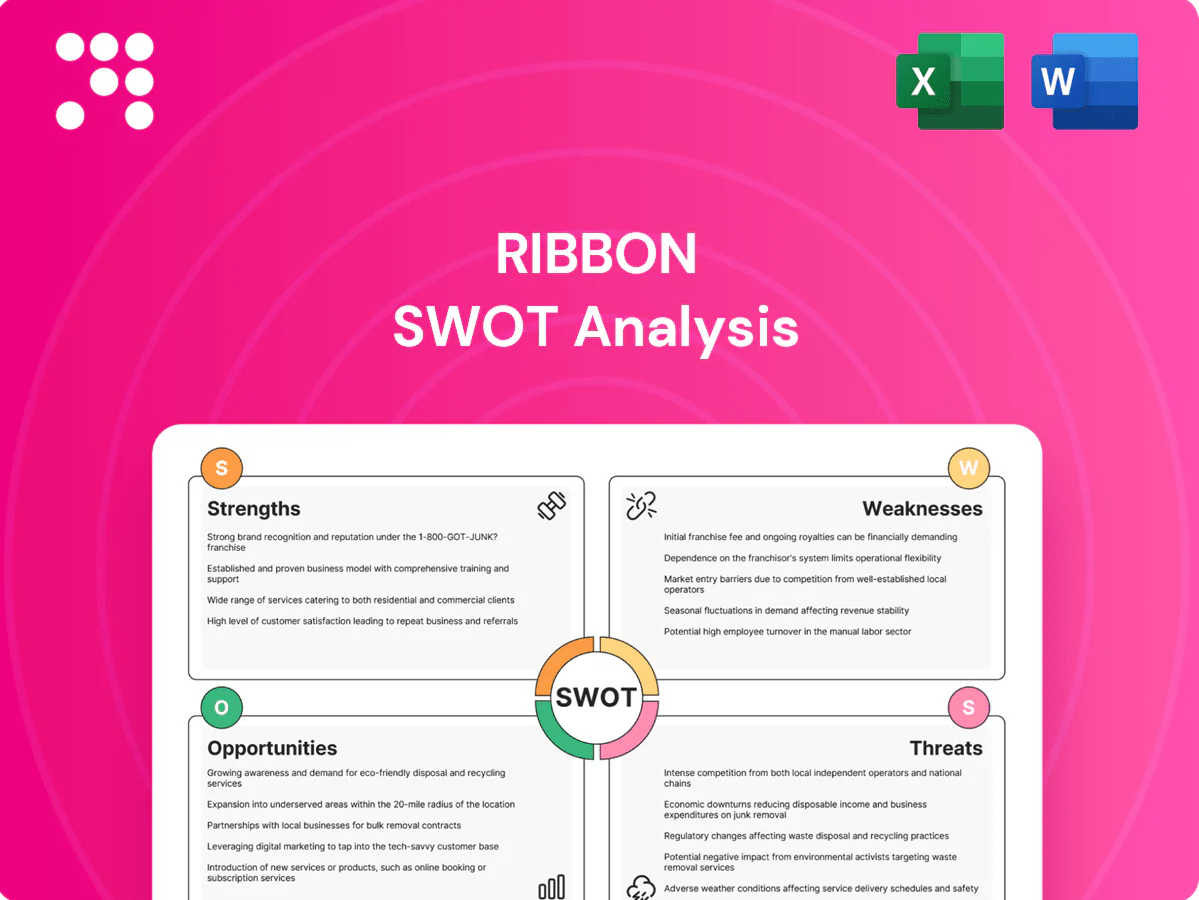

Ribbon’s SWOT snapshot highlights its competitive edges, market threats, and untapped growth levers in clear, actionable terms. Want the full strategic picture with financial context and implementation steps? Purchase the complete SWOT analysis for a professionally formatted, editable report and Excel tools to plan, pitch, or invest with confidence.

Strengths

End-to-end portfolio breadth

Hardware, software, and cloud options let Ribbon support on-prem, hybrid, and cloud-native deployments, reducing vendor sprawl and increasing wallet share per customer by enabling consolidated sourcing; this simplifies migrations from legacy to cloud-native environments and makes cross-selling across voice, IP, and optical domains significantly easier.

Real-time communications expertise

Ribbon’s heritage in secure, carrier-grade voice and video—backed by reported FY2024 revenue of $372.8M—underpins reliability for telcos; deep protocol and interop expertise across multi-vendor networks strengthens credibility, shortens sales cycles with large carriers and enterprises, and supports higher-margin maintenance and services attach.

Secure-by-design positioning

Security is embedded across session, data, and management layers, aligning with enterprise demand as Gartner projected global security and risk management spending of about 188.3 billion USD in 2024. Critical infrastructure clients value this for compliance and resilience, driving higher contract win rates in regulated sectors. A strong security posture differentiates Ribbon from best-effort cloud entrants and raises switching costs, helping mitigate churn.

IP optical networking capabilities

Ownership of IP routing and optical transport lets Ribbon address both packet and photonic layers, expanding TAM in an optical transport market estimated at about $11B in 2024 and with global IP traffic growing roughly 22% CAGR into 2027; this aligns with bandwidth demand from 5G, cloud and video.

- Layer convergence: expands TAM

- 22% IP traffic CAGR into 2027

- $11B optical market (2024)

- Creates multi-year refresh/upgrade pathways

Diverse global customer base

Diverse global customer base anchors Ribbon’s revenue across service providers, enterprises and critical infrastructure, reducing exposure to any single vertical and smoothing regional cycle volatility in 2024. Multi-segment exposure increases referenceability across telco, enterprise UC and critical networks and enables tailored go-to-market motions by customer type and geography. This mix supports recurring licensing, professional services and appliance sales streams.

- Serves service providers, enterprises, critical infrastructure

- Geographic spread reduces local cycle risk

- Cross-vertical references boost sales motion

- Enables tailored GTM and recurring revenue mix

Hardware-to-cloud portfolio grows wallet share; FY2024 revenue $372.8M

Ribbon's hardware, software and cloud portfolio enables on‑prem, hybrid and cloud‑native deployments, increasing wallet share and easing legacy migrations. FY2024 revenue was $372.8M, underpinned by carrier‑grade voice/video and multi‑vendor interoperability. Embedded security aligns with 2024 global SRM spend of $188.3B, raising loyalty with regulated clients. IP/optical portfolio targets an ~$11B optical market and 22% IP traffic CAGR into 2027.

| Metric | Value |

|---|---|

| FY2024 revenue | $372.8M |

| Global SRM spend (2024) | $188.3B |

| Optical market (2024) | $11B |

| IP traffic CAGR | ~22% to 2027 |

What is included in the product

Provides a concise SWOT assessment of Ribbon, outlining its internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making.

Ribbon SWOT Analysis delivers a prioritized, ribbon-style SWOT layout that highlights key pain points and accelerates alignment across teams for faster, focused decision-making.

Weaknesses

Exposure to telco capex cycles

Large portions of Ribbon's revenue depend on service-provider capex, so budget pauses or priority shifts by carriers can delay orders and elongate sales cycles, often turning quarters of expected revenue into multi-quarter timing variances. Forecasting becomes harder and inventory risk rises as unsold units accumulate, pressuring margins during telco downturns and amplifying working-capital strain.

Intense competition from larger vendors

Intense competition from Cisco, Nokia, Huawei and others across adjacent domains squeezes Ribbon’s addressable markets; Cisco reported roughly $57B in FY2024, Nokia about €22–25B in 2024, and Huawei reported revenues north of $90B in 2024, underscoring scale gaps. Scale advantages let incumbents pressure pricing and offer bundled deals, eroding Ribbon’s margin and deal win-rate. Larger vendors’ marketing share-of-voice and entrenched partner ecosystems often default to incumbents, limiting Ribbon’s reach and channel access.

Legacy product mix drag

Declining TDM and on-prem telephony portfolios dilute growth optics as customers migrate to cloud voice and software-defined networking. Migration to cloud-native offerings tends to compress near-term revenue recognition as services replace high-margin appliance sales. Ongoing support and RMA obligations for legacy systems tie up engineering and field resources. This support burden can slow innovation velocity in priority growth areas like cloud session border controllers and CPaaS.

Complex integration requirements

Complex, multi-domain integrations demand deep interoperability and services, often extending deployments and cash conversion cycles; Gartner notes ~70% of digital transformations face significant delays or failures (2024), and bespoke builds increase post-sales support burdens, constraining scalability absent strong automation and standardized tooling.

- Integration depth → higher professional services

- Longer timelines → slower cash conversion

- Custom builds → elevated support load

- Scalability limited without automation

Customer concentration risk

Large carrier accounts can represent outsized revenue portions; Ribbon reported $364.2 million in revenue for FY2024, with a concentrated customer base meaning a lost RFP or consolidation can materially impact results, pricing leverage often favors top buyers, and multi-year renewal cliffs create quarter-to-quarter revenue volatility.

- Top-line pressure from customer concentration

- Lost RFPs can swing quarterly results

- Pricing leverage favors large carriers

- Renewal cliffs drive revenue volatility

Carrier capex dependence, long sales cycles and legacy integrations compress margins

Ribbon's revenue (364.2M FY2024) is highly dependent on carrier capex, creating elongated sales cycles and inventory risk. Scale gaps vs Cisco (~57B 2024), Nokia (22–25B 2024) and Huawei (>90B 2024) compress pricing and channel access. Legacy TDM support and complex integrations slow cloud transition and cash conversion, increasing post-sales service load.

| Metric | Value (2024) |

|---|---|

| Ribbon revenue | 364.2M |

| Cisco | ~57B |

| Nokia | €22–25B |

| Huawei | >90B |

Preview Before You Purchase

Ribbon SWOT Analysis

This is the actual Ribbon SWOT analysis you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full, editable report and reflects the final structure and insights. The complete document is unlocked immediately after payment.

Your Strategic Toolkit Starts Here

Ribbon’s SWOT snapshot highlights its competitive edges, market threats, and untapped growth levers in clear, actionable terms. Want the full strategic picture with financial context and implementation steps? Purchase the complete SWOT analysis for a professionally formatted, editable report and Excel tools to plan, pitch, or invest with confidence.

Strengths

End-to-end portfolio breadth

Hardware, software, and cloud options let Ribbon support on-prem, hybrid, and cloud-native deployments, reducing vendor sprawl and increasing wallet share per customer by enabling consolidated sourcing; this simplifies migrations from legacy to cloud-native environments and makes cross-selling across voice, IP, and optical domains significantly easier.

Real-time communications expertise

Ribbon’s heritage in secure, carrier-grade voice and video—backed by reported FY2024 revenue of $372.8M—underpins reliability for telcos; deep protocol and interop expertise across multi-vendor networks strengthens credibility, shortens sales cycles with large carriers and enterprises, and supports higher-margin maintenance and services attach.

Secure-by-design positioning

Security is embedded across session, data, and management layers, aligning with enterprise demand as Gartner projected global security and risk management spending of about 188.3 billion USD in 2024. Critical infrastructure clients value this for compliance and resilience, driving higher contract win rates in regulated sectors. A strong security posture differentiates Ribbon from best-effort cloud entrants and raises switching costs, helping mitigate churn.

IP optical networking capabilities

Ownership of IP routing and optical transport lets Ribbon address both packet and photonic layers, expanding TAM in an optical transport market estimated at about $11B in 2024 and with global IP traffic growing roughly 22% CAGR into 2027; this aligns with bandwidth demand from 5G, cloud and video.

- Layer convergence: expands TAM

- 22% IP traffic CAGR into 2027

- $11B optical market (2024)

- Creates multi-year refresh/upgrade pathways

Diverse global customer base

Diverse global customer base anchors Ribbon’s revenue across service providers, enterprises and critical infrastructure, reducing exposure to any single vertical and smoothing regional cycle volatility in 2024. Multi-segment exposure increases referenceability across telco, enterprise UC and critical networks and enables tailored go-to-market motions by customer type and geography. This mix supports recurring licensing, professional services and appliance sales streams.

- Serves service providers, enterprises, critical infrastructure

- Geographic spread reduces local cycle risk

- Cross-vertical references boost sales motion

- Enables tailored GTM and recurring revenue mix

Hardware-to-cloud portfolio grows wallet share; FY2024 revenue $372.8M

Ribbon's hardware, software and cloud portfolio enables on‑prem, hybrid and cloud‑native deployments, increasing wallet share and easing legacy migrations. FY2024 revenue was $372.8M, underpinned by carrier‑grade voice/video and multi‑vendor interoperability. Embedded security aligns with 2024 global SRM spend of $188.3B, raising loyalty with regulated clients. IP/optical portfolio targets an ~$11B optical market and 22% IP traffic CAGR into 2027.

| Metric | Value |

|---|---|

| FY2024 revenue | $372.8M |

| Global SRM spend (2024) | $188.3B |

| Optical market (2024) | $11B |

| IP traffic CAGR | ~22% to 2027 |

What is included in the product

Provides a concise SWOT assessment of Ribbon, outlining its internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making.

Ribbon SWOT Analysis delivers a prioritized, ribbon-style SWOT layout that highlights key pain points and accelerates alignment across teams for faster, focused decision-making.

Weaknesses

Exposure to telco capex cycles

Large portions of Ribbon's revenue depend on service-provider capex, so budget pauses or priority shifts by carriers can delay orders and elongate sales cycles, often turning quarters of expected revenue into multi-quarter timing variances. Forecasting becomes harder and inventory risk rises as unsold units accumulate, pressuring margins during telco downturns and amplifying working-capital strain.

Intense competition from larger vendors

Intense competition from Cisco, Nokia, Huawei and others across adjacent domains squeezes Ribbon’s addressable markets; Cisco reported roughly $57B in FY2024, Nokia about €22–25B in 2024, and Huawei reported revenues north of $90B in 2024, underscoring scale gaps. Scale advantages let incumbents pressure pricing and offer bundled deals, eroding Ribbon’s margin and deal win-rate. Larger vendors’ marketing share-of-voice and entrenched partner ecosystems often default to incumbents, limiting Ribbon’s reach and channel access.

Legacy product mix drag

Declining TDM and on-prem telephony portfolios dilute growth optics as customers migrate to cloud voice and software-defined networking. Migration to cloud-native offerings tends to compress near-term revenue recognition as services replace high-margin appliance sales. Ongoing support and RMA obligations for legacy systems tie up engineering and field resources. This support burden can slow innovation velocity in priority growth areas like cloud session border controllers and CPaaS.

Complex integration requirements

Complex, multi-domain integrations demand deep interoperability and services, often extending deployments and cash conversion cycles; Gartner notes ~70% of digital transformations face significant delays or failures (2024), and bespoke builds increase post-sales support burdens, constraining scalability absent strong automation and standardized tooling.

- Integration depth → higher professional services

- Longer timelines → slower cash conversion

- Custom builds → elevated support load

- Scalability limited without automation

Customer concentration risk

Large carrier accounts can represent outsized revenue portions; Ribbon reported $364.2 million in revenue for FY2024, with a concentrated customer base meaning a lost RFP or consolidation can materially impact results, pricing leverage often favors top buyers, and multi-year renewal cliffs create quarter-to-quarter revenue volatility.

- Top-line pressure from customer concentration

- Lost RFPs can swing quarterly results

- Pricing leverage favors large carriers

- Renewal cliffs drive revenue volatility

Carrier capex dependence, long sales cycles and legacy integrations compress margins

Ribbon's revenue (364.2M FY2024) is highly dependent on carrier capex, creating elongated sales cycles and inventory risk. Scale gaps vs Cisco (~57B 2024), Nokia (22–25B 2024) and Huawei (>90B 2024) compress pricing and channel access. Legacy TDM support and complex integrations slow cloud transition and cash conversion, increasing post-sales service load.

| Metric | Value (2024) |

|---|---|

| Ribbon revenue | 364.2M |

| Cisco | ~57B |

| Nokia | €22–25B |

| Huawei | >90B |

Preview Before You Purchase

Ribbon SWOT Analysis

This is the actual Ribbon SWOT analysis you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full, editable report and reflects the final structure and insights. The complete document is unlocked immediately after payment.

Description

Your Strategic Toolkit Starts Here

Ribbon’s SWOT snapshot highlights its competitive edges, market threats, and untapped growth levers in clear, actionable terms. Want the full strategic picture with financial context and implementation steps? Purchase the complete SWOT analysis for a professionally formatted, editable report and Excel tools to plan, pitch, or invest with confidence.

Strengths

End-to-end portfolio breadth

Hardware, software, and cloud options let Ribbon support on-prem, hybrid, and cloud-native deployments, reducing vendor sprawl and increasing wallet share per customer by enabling consolidated sourcing; this simplifies migrations from legacy to cloud-native environments and makes cross-selling across voice, IP, and optical domains significantly easier.

Real-time communications expertise

Ribbon’s heritage in secure, carrier-grade voice and video—backed by reported FY2024 revenue of $372.8M—underpins reliability for telcos; deep protocol and interop expertise across multi-vendor networks strengthens credibility, shortens sales cycles with large carriers and enterprises, and supports higher-margin maintenance and services attach.

Secure-by-design positioning

Security is embedded across session, data, and management layers, aligning with enterprise demand as Gartner projected global security and risk management spending of about 188.3 billion USD in 2024. Critical infrastructure clients value this for compliance and resilience, driving higher contract win rates in regulated sectors. A strong security posture differentiates Ribbon from best-effort cloud entrants and raises switching costs, helping mitigate churn.

IP optical networking capabilities

Ownership of IP routing and optical transport lets Ribbon address both packet and photonic layers, expanding TAM in an optical transport market estimated at about $11B in 2024 and with global IP traffic growing roughly 22% CAGR into 2027; this aligns with bandwidth demand from 5G, cloud and video.

- Layer convergence: expands TAM

- 22% IP traffic CAGR into 2027

- $11B optical market (2024)

- Creates multi-year refresh/upgrade pathways

Diverse global customer base

Diverse global customer base anchors Ribbon’s revenue across service providers, enterprises and critical infrastructure, reducing exposure to any single vertical and smoothing regional cycle volatility in 2024. Multi-segment exposure increases referenceability across telco, enterprise UC and critical networks and enables tailored go-to-market motions by customer type and geography. This mix supports recurring licensing, professional services and appliance sales streams.

- Serves service providers, enterprises, critical infrastructure

- Geographic spread reduces local cycle risk

- Cross-vertical references boost sales motion

- Enables tailored GTM and recurring revenue mix

Hardware-to-cloud portfolio grows wallet share; FY2024 revenue $372.8M

Ribbon's hardware, software and cloud portfolio enables on‑prem, hybrid and cloud‑native deployments, increasing wallet share and easing legacy migrations. FY2024 revenue was $372.8M, underpinned by carrier‑grade voice/video and multi‑vendor interoperability. Embedded security aligns with 2024 global SRM spend of $188.3B, raising loyalty with regulated clients. IP/optical portfolio targets an ~$11B optical market and 22% IP traffic CAGR into 2027.

| Metric | Value |

|---|---|

| FY2024 revenue | $372.8M |

| Global SRM spend (2024) | $188.3B |

| Optical market (2024) | $11B |

| IP traffic CAGR | ~22% to 2027 |

What is included in the product

Provides a concise SWOT assessment of Ribbon, outlining its internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making.

Ribbon SWOT Analysis delivers a prioritized, ribbon-style SWOT layout that highlights key pain points and accelerates alignment across teams for faster, focused decision-making.

Weaknesses

Exposure to telco capex cycles

Large portions of Ribbon's revenue depend on service-provider capex, so budget pauses or priority shifts by carriers can delay orders and elongate sales cycles, often turning quarters of expected revenue into multi-quarter timing variances. Forecasting becomes harder and inventory risk rises as unsold units accumulate, pressuring margins during telco downturns and amplifying working-capital strain.

Intense competition from larger vendors

Intense competition from Cisco, Nokia, Huawei and others across adjacent domains squeezes Ribbon’s addressable markets; Cisco reported roughly $57B in FY2024, Nokia about €22–25B in 2024, and Huawei reported revenues north of $90B in 2024, underscoring scale gaps. Scale advantages let incumbents pressure pricing and offer bundled deals, eroding Ribbon’s margin and deal win-rate. Larger vendors’ marketing share-of-voice and entrenched partner ecosystems often default to incumbents, limiting Ribbon’s reach and channel access.

Legacy product mix drag

Declining TDM and on-prem telephony portfolios dilute growth optics as customers migrate to cloud voice and software-defined networking. Migration to cloud-native offerings tends to compress near-term revenue recognition as services replace high-margin appliance sales. Ongoing support and RMA obligations for legacy systems tie up engineering and field resources. This support burden can slow innovation velocity in priority growth areas like cloud session border controllers and CPaaS.

Complex integration requirements

Complex, multi-domain integrations demand deep interoperability and services, often extending deployments and cash conversion cycles; Gartner notes ~70% of digital transformations face significant delays or failures (2024), and bespoke builds increase post-sales support burdens, constraining scalability absent strong automation and standardized tooling.

- Integration depth → higher professional services

- Longer timelines → slower cash conversion

- Custom builds → elevated support load

- Scalability limited without automation

Customer concentration risk

Large carrier accounts can represent outsized revenue portions; Ribbon reported $364.2 million in revenue for FY2024, with a concentrated customer base meaning a lost RFP or consolidation can materially impact results, pricing leverage often favors top buyers, and multi-year renewal cliffs create quarter-to-quarter revenue volatility.

- Top-line pressure from customer concentration

- Lost RFPs can swing quarterly results

- Pricing leverage favors large carriers

- Renewal cliffs drive revenue volatility

Carrier capex dependence, long sales cycles and legacy integrations compress margins

Ribbon's revenue (364.2M FY2024) is highly dependent on carrier capex, creating elongated sales cycles and inventory risk. Scale gaps vs Cisco (~57B 2024), Nokia (22–25B 2024) and Huawei (>90B 2024) compress pricing and channel access. Legacy TDM support and complex integrations slow cloud transition and cash conversion, increasing post-sales service load.

| Metric | Value (2024) |

|---|---|

| Ribbon revenue | 364.2M |

| Cisco | ~57B |

| Nokia | €22–25B |

| Huawei | >90B |

Preview Before You Purchase

Ribbon SWOT Analysis

This is the actual Ribbon SWOT analysis you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full, editable report and reflects the final structure and insights. The complete document is unlocked immediately after payment.