Ricoh PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Ricoh—three to five-second insights into how political, economic, and technological forces shape its outlook. Discover regulatory and environmental risks alongside market opportunities. This concise briefing is ideal for investors and strategists. Purchase the full analysis for the complete, actionable breakdown ready for immediate use.

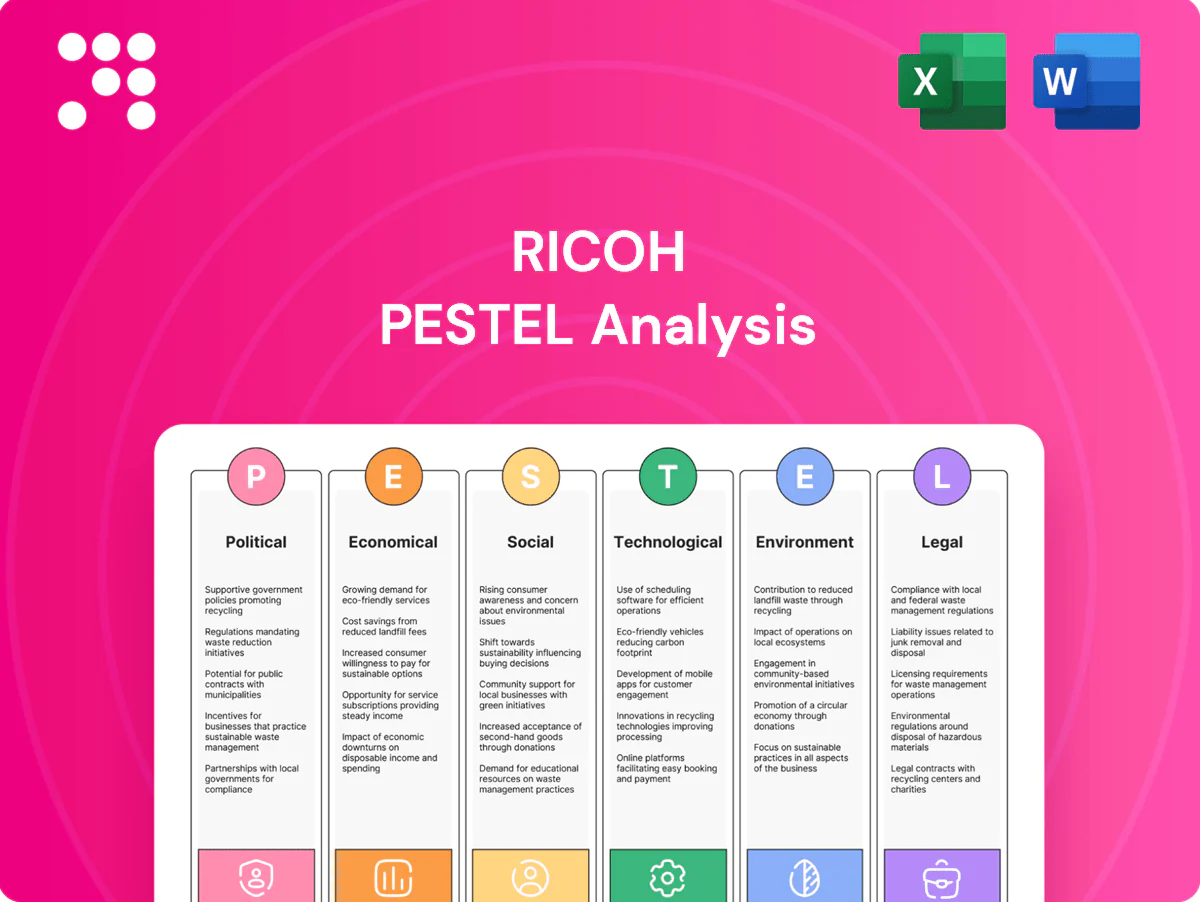

Political factors

Trade policy and tariffs

As a Japan-headquartered exporter, Ricoh is exposed to tariff shifts between the US, EU, China and regional blocs such as RCEP (15 members) and CPTPP, with US Section 301 tariffs remaining up to 25% on some Chinese-origin goods. Component-level duties can materially alter Ricoh’s bill of materials and pricing power. Proactive sourcing diversification and regional manufacturing (ASEAN, North America) buffer shocks, and ongoing geopolitics may force localized product variants.

Government digitization agendas

EU and national government digitization drives — with public procurement ≈14% of EU GDP (~€2 trillion/year) — boost demand for managed print and IT services, and winning framework contracts often creates multi-year revenue streams. Procurement thresholds and national preferences strongly shape vendor selection, while compliance with Directive 2014/55/EU on e-invoicing and eIDAS secure ID/workflow standards is essential for public-sector deals.

Industrial policy and subsidies

Incentives for advanced manufacturing, semiconductors and green tech can materially lower Ricoh’s capex and R&D burden; US CHIPS incentives include about $52 billion and the EU Chips/industrial plans mobilize up to €43 billion. Competing OEMs securing grants could intensify price pressure. Monitoring grant programs across Japan, the EU and North America is strategic, and compliance plus co-innovation partnerships improve eligibility.

Political stability and supply chain

Political instability in key logistics corridors can delay critical parts and raise freight costs, so Ricoh leverages multi-country assembly footprints to reduce single-country risk and preserve service levels for enterprise clients. Inventory buffers and dual-sourcing enhance resilience while scenario planning underpins contractual SLAs.

- Multi-country assembly

- Inventory buffers

- Dual-sourcing

- Scenario planning for SLAs

Public procurement standards

Public procurement standards now push security certifications and sustainability criteria into tenders, with EU public procurement representing roughly 14% of EU GDP and the Corporate Sustainability Reporting Directive expanding coverage to about 50,000 firms by 2024. Meeting local content rules and transparent ESG reporting raises political acceptance and bid success, while secure-by-design and low-carbon devices improve procurement scoring.

- security-certification: ISO/IEC 27001

- sustainability: CSRD ~50,000 firms (2024)

- procurement-weight: public spend ~14% EU GDP

- differentiation: secure-by-design, low-carbon devices

Tariffs, subsidies and CSRD reshape supply chains: regional manufacturing and dual-sourcing prevail

Ricoh faces tariff risk (US Section 301 up to 25%) and supply-chain disruption from geopolitical tensions; regional manufacturing (ASEAN, NA) and dual-sourcing mitigate impact. EU public procurement (~14% GDP ≈€2tn/year) and CSRD (~50,000 firms, 2024) raise security and sustainability requirements. Subsidy races (US CHIPS $52bn, EU chips €43bn) affect competitor cost structures and bidding.

| Metric | Value |

|---|---|

| EU public spend | ~14% GDP ≈€2tn/yr |

| CSRD coverage | ~50,000 firms (2024) |

| US tariffs | Section 301 up to 25% |

| Chips subsidies | US $52bn / EU €43bn |

What is included in the product

Explores how macro-environmental forces uniquely impact Ricoh across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific dynamics. Designed for executives and advisors, it highlights threats, opportunities, forward-looking scenarios, and ready-to-use insights for strategy, funding, and operational planning.

A concise, visually segmented Ricoh PESTLE summary that streamlines external risk assessment for meetings and planning, easily editable for region- or business-specific notes and drop-in ready for presentations or team alignment.

Economic factors

Print demand cyclicality

Hardware refresh cycles and page volumes soften in downturns—Ricoh reported FY2024 revenue of about 1,523.6 billion yen as device demand dipped, but services/subscriptions (around 55% of sales) smoothed revenue streams; value selling on productivity and TCO offsets lower utilization, while outcome-based contracts helped sustain operating margin near 4.6% in FY2024.

Currency volatility (JPY, USD, EUR)

FX swings (USD/JPY ~140–155 in 2023–24; EUR/USD ~1.05–1.10 in 2024) affect Ricoh export pricing, imported component costs and repatriated earnings, changing margins and translation results. Natural hedges (local sourcing, matching FX cashflows) and financial instruments (forwards, options) are used to mitigate impact. Pricing corridors reduce list-price churn, while transparent FX clauses stabilize long-term contracts.

Inflation and input costs

Materials, energy and freight inflation—despite easing from 2021–22 peaks—continue to compress Ricoh margins, with global headline inflation around 3% in 2024 (IMF) and container freight rates roughly 50% below 2021 peaks yet still adding per-unit cost pressure.

Design-to-cost and BOM optimization are primary levers to restore margins, cutting component spend and supplier complexity; targeted parts rationalization can reduce bill-of-material costs by double-digit percentages in device programs.

Higher service route density and remote diagnostics lower field-service hours and onsite visits, reducing service costs materially; combined with tiered hardware and subscription offerings Ricoh can preserve affordability for core customers while protecting premium mix and ASPs.

SMB vs enterprise mix

SMB spend is highly sensitive to credit and macro outlook, while enterprise budgets are slower-moving and stickier; Gartner reported global IT spending at about $4.7 trillion in 2024, with enterprises driving multi-year contracts. Channel programs and financing solutions help sustain SMB velocity, and enterprise deals favor integrated IT and security solutions; a balanced SMB/enterprise mix smooths revenue volatility.

- SMB sensitivity: credit, macro

- Enterprise: slower-moving, multi-year

- Channels/financing sustain SMB

- Enterprise favors integrated IT/security

- Balanced mix reduces volatility

Digital transformation investment

Enterprises are allocating significant budgets to cloud migration, workflow automation and data security as public cloud spending exceeded $600 billion in 2023 and continues double-digit growth into 2024–25; Ricoh’s IT services and document solutions map directly to those spend priorities. Cross-selling hardware into managed services increases customer lifetime value and Ricoh's ability to demonstrate ROI accelerates deal closure and recurring revenue adoption.

Tariffs, subsidies and CSRD reshape supply chains: regional manufacturing and dual-sourcing prevail

Ricoh's FY2024 revenue ≈1,523.6bn yen with services ≈55% smoothing cyclic device demand; operating margin ~4.6%. FX (USD/JPY ~140–155 in 2023–24) and materials/energy inflation (~3% global 2024) pressure margins; BOM optimization and service density cut costs. Enterprise IT spend ~$4.7T (2024) and >$600bn public cloud (2023) support cross-sell into managed services.

| Metric | Value |

|---|---|

| FY2024 revenue | 1,523.6bn JPY |

| Services % | ~55% |

| Op margin | ~4.6% |

| Global IT spend | $4.7T (2024) |

Full Version Awaits

Ricoh PESTLE Analysis

The Ricoh PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the final, downloadable file.

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Ricoh—three to five-second insights into how political, economic, and technological forces shape its outlook. Discover regulatory and environmental risks alongside market opportunities. This concise briefing is ideal for investors and strategists. Purchase the full analysis for the complete, actionable breakdown ready for immediate use.

Political factors

Trade policy and tariffs

As a Japan-headquartered exporter, Ricoh is exposed to tariff shifts between the US, EU, China and regional blocs such as RCEP (15 members) and CPTPP, with US Section 301 tariffs remaining up to 25% on some Chinese-origin goods. Component-level duties can materially alter Ricoh’s bill of materials and pricing power. Proactive sourcing diversification and regional manufacturing (ASEAN, North America) buffer shocks, and ongoing geopolitics may force localized product variants.

Government digitization agendas

EU and national government digitization drives — with public procurement ≈14% of EU GDP (~€2 trillion/year) — boost demand for managed print and IT services, and winning framework contracts often creates multi-year revenue streams. Procurement thresholds and national preferences strongly shape vendor selection, while compliance with Directive 2014/55/EU on e-invoicing and eIDAS secure ID/workflow standards is essential for public-sector deals.

Industrial policy and subsidies

Incentives for advanced manufacturing, semiconductors and green tech can materially lower Ricoh’s capex and R&D burden; US CHIPS incentives include about $52 billion and the EU Chips/industrial plans mobilize up to €43 billion. Competing OEMs securing grants could intensify price pressure. Monitoring grant programs across Japan, the EU and North America is strategic, and compliance plus co-innovation partnerships improve eligibility.

Political stability and supply chain

Political instability in key logistics corridors can delay critical parts and raise freight costs, so Ricoh leverages multi-country assembly footprints to reduce single-country risk and preserve service levels for enterprise clients. Inventory buffers and dual-sourcing enhance resilience while scenario planning underpins contractual SLAs.

- Multi-country assembly

- Inventory buffers

- Dual-sourcing

- Scenario planning for SLAs

Public procurement standards

Public procurement standards now push security certifications and sustainability criteria into tenders, with EU public procurement representing roughly 14% of EU GDP and the Corporate Sustainability Reporting Directive expanding coverage to about 50,000 firms by 2024. Meeting local content rules and transparent ESG reporting raises political acceptance and bid success, while secure-by-design and low-carbon devices improve procurement scoring.

- security-certification: ISO/IEC 27001

- sustainability: CSRD ~50,000 firms (2024)

- procurement-weight: public spend ~14% EU GDP

- differentiation: secure-by-design, low-carbon devices

Tariffs, subsidies and CSRD reshape supply chains: regional manufacturing and dual-sourcing prevail

Ricoh faces tariff risk (US Section 301 up to 25%) and supply-chain disruption from geopolitical tensions; regional manufacturing (ASEAN, NA) and dual-sourcing mitigate impact. EU public procurement (~14% GDP ≈€2tn/year) and CSRD (~50,000 firms, 2024) raise security and sustainability requirements. Subsidy races (US CHIPS $52bn, EU chips €43bn) affect competitor cost structures and bidding.

| Metric | Value |

|---|---|

| EU public spend | ~14% GDP ≈€2tn/yr |

| CSRD coverage | ~50,000 firms (2024) |

| US tariffs | Section 301 up to 25% |

| Chips subsidies | US $52bn / EU €43bn |

What is included in the product

Explores how macro-environmental forces uniquely impact Ricoh across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific dynamics. Designed for executives and advisors, it highlights threats, opportunities, forward-looking scenarios, and ready-to-use insights for strategy, funding, and operational planning.

A concise, visually segmented Ricoh PESTLE summary that streamlines external risk assessment for meetings and planning, easily editable for region- or business-specific notes and drop-in ready for presentations or team alignment.

Economic factors

Print demand cyclicality

Hardware refresh cycles and page volumes soften in downturns—Ricoh reported FY2024 revenue of about 1,523.6 billion yen as device demand dipped, but services/subscriptions (around 55% of sales) smoothed revenue streams; value selling on productivity and TCO offsets lower utilization, while outcome-based contracts helped sustain operating margin near 4.6% in FY2024.

Currency volatility (JPY, USD, EUR)

FX swings (USD/JPY ~140–155 in 2023–24; EUR/USD ~1.05–1.10 in 2024) affect Ricoh export pricing, imported component costs and repatriated earnings, changing margins and translation results. Natural hedges (local sourcing, matching FX cashflows) and financial instruments (forwards, options) are used to mitigate impact. Pricing corridors reduce list-price churn, while transparent FX clauses stabilize long-term contracts.

Inflation and input costs

Materials, energy and freight inflation—despite easing from 2021–22 peaks—continue to compress Ricoh margins, with global headline inflation around 3% in 2024 (IMF) and container freight rates roughly 50% below 2021 peaks yet still adding per-unit cost pressure.

Design-to-cost and BOM optimization are primary levers to restore margins, cutting component spend and supplier complexity; targeted parts rationalization can reduce bill-of-material costs by double-digit percentages in device programs.

Higher service route density and remote diagnostics lower field-service hours and onsite visits, reducing service costs materially; combined with tiered hardware and subscription offerings Ricoh can preserve affordability for core customers while protecting premium mix and ASPs.

SMB vs enterprise mix

SMB spend is highly sensitive to credit and macro outlook, while enterprise budgets are slower-moving and stickier; Gartner reported global IT spending at about $4.7 trillion in 2024, with enterprises driving multi-year contracts. Channel programs and financing solutions help sustain SMB velocity, and enterprise deals favor integrated IT and security solutions; a balanced SMB/enterprise mix smooths revenue volatility.

- SMB sensitivity: credit, macro

- Enterprise: slower-moving, multi-year

- Channels/financing sustain SMB

- Enterprise favors integrated IT/security

- Balanced mix reduces volatility

Digital transformation investment

Enterprises are allocating significant budgets to cloud migration, workflow automation and data security as public cloud spending exceeded $600 billion in 2023 and continues double-digit growth into 2024–25; Ricoh’s IT services and document solutions map directly to those spend priorities. Cross-selling hardware into managed services increases customer lifetime value and Ricoh's ability to demonstrate ROI accelerates deal closure and recurring revenue adoption.

Tariffs, subsidies and CSRD reshape supply chains: regional manufacturing and dual-sourcing prevail

Ricoh's FY2024 revenue ≈1,523.6bn yen with services ≈55% smoothing cyclic device demand; operating margin ~4.6%. FX (USD/JPY ~140–155 in 2023–24) and materials/energy inflation (~3% global 2024) pressure margins; BOM optimization and service density cut costs. Enterprise IT spend ~$4.7T (2024) and >$600bn public cloud (2023) support cross-sell into managed services.

| Metric | Value |

|---|---|

| FY2024 revenue | 1,523.6bn JPY |

| Services % | ~55% |

| Op margin | ~4.6% |

| Global IT spend | $4.7T (2024) |

Full Version Awaits

Ricoh PESTLE Analysis

The Ricoh PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the final, downloadable file.

Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Ricoh—three to five-second insights into how political, economic, and technological forces shape its outlook. Discover regulatory and environmental risks alongside market opportunities. This concise briefing is ideal for investors and strategists. Purchase the full analysis for the complete, actionable breakdown ready for immediate use.

Political factors

Trade policy and tariffs

As a Japan-headquartered exporter, Ricoh is exposed to tariff shifts between the US, EU, China and regional blocs such as RCEP (15 members) and CPTPP, with US Section 301 tariffs remaining up to 25% on some Chinese-origin goods. Component-level duties can materially alter Ricoh’s bill of materials and pricing power. Proactive sourcing diversification and regional manufacturing (ASEAN, North America) buffer shocks, and ongoing geopolitics may force localized product variants.

Government digitization agendas

EU and national government digitization drives — with public procurement ≈14% of EU GDP (~€2 trillion/year) — boost demand for managed print and IT services, and winning framework contracts often creates multi-year revenue streams. Procurement thresholds and national preferences strongly shape vendor selection, while compliance with Directive 2014/55/EU on e-invoicing and eIDAS secure ID/workflow standards is essential for public-sector deals.

Industrial policy and subsidies

Incentives for advanced manufacturing, semiconductors and green tech can materially lower Ricoh’s capex and R&D burden; US CHIPS incentives include about $52 billion and the EU Chips/industrial plans mobilize up to €43 billion. Competing OEMs securing grants could intensify price pressure. Monitoring grant programs across Japan, the EU and North America is strategic, and compliance plus co-innovation partnerships improve eligibility.

Political stability and supply chain

Political instability in key logistics corridors can delay critical parts and raise freight costs, so Ricoh leverages multi-country assembly footprints to reduce single-country risk and preserve service levels for enterprise clients. Inventory buffers and dual-sourcing enhance resilience while scenario planning underpins contractual SLAs.

- Multi-country assembly

- Inventory buffers

- Dual-sourcing

- Scenario planning for SLAs

Public procurement standards

Public procurement standards now push security certifications and sustainability criteria into tenders, with EU public procurement representing roughly 14% of EU GDP and the Corporate Sustainability Reporting Directive expanding coverage to about 50,000 firms by 2024. Meeting local content rules and transparent ESG reporting raises political acceptance and bid success, while secure-by-design and low-carbon devices improve procurement scoring.

- security-certification: ISO/IEC 27001

- sustainability: CSRD ~50,000 firms (2024)

- procurement-weight: public spend ~14% EU GDP

- differentiation: secure-by-design, low-carbon devices

Tariffs, subsidies and CSRD reshape supply chains: regional manufacturing and dual-sourcing prevail

Ricoh faces tariff risk (US Section 301 up to 25%) and supply-chain disruption from geopolitical tensions; regional manufacturing (ASEAN, NA) and dual-sourcing mitigate impact. EU public procurement (~14% GDP ≈€2tn/year) and CSRD (~50,000 firms, 2024) raise security and sustainability requirements. Subsidy races (US CHIPS $52bn, EU chips €43bn) affect competitor cost structures and bidding.

| Metric | Value |

|---|---|

| EU public spend | ~14% GDP ≈€2tn/yr |

| CSRD coverage | ~50,000 firms (2024) |

| US tariffs | Section 301 up to 25% |

| Chips subsidies | US $52bn / EU €43bn |

What is included in the product

Explores how macro-environmental forces uniquely impact Ricoh across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific dynamics. Designed for executives and advisors, it highlights threats, opportunities, forward-looking scenarios, and ready-to-use insights for strategy, funding, and operational planning.

A concise, visually segmented Ricoh PESTLE summary that streamlines external risk assessment for meetings and planning, easily editable for region- or business-specific notes and drop-in ready for presentations or team alignment.

Economic factors

Print demand cyclicality

Hardware refresh cycles and page volumes soften in downturns—Ricoh reported FY2024 revenue of about 1,523.6 billion yen as device demand dipped, but services/subscriptions (around 55% of sales) smoothed revenue streams; value selling on productivity and TCO offsets lower utilization, while outcome-based contracts helped sustain operating margin near 4.6% in FY2024.

Currency volatility (JPY, USD, EUR)

FX swings (USD/JPY ~140–155 in 2023–24; EUR/USD ~1.05–1.10 in 2024) affect Ricoh export pricing, imported component costs and repatriated earnings, changing margins and translation results. Natural hedges (local sourcing, matching FX cashflows) and financial instruments (forwards, options) are used to mitigate impact. Pricing corridors reduce list-price churn, while transparent FX clauses stabilize long-term contracts.

Inflation and input costs

Materials, energy and freight inflation—despite easing from 2021–22 peaks—continue to compress Ricoh margins, with global headline inflation around 3% in 2024 (IMF) and container freight rates roughly 50% below 2021 peaks yet still adding per-unit cost pressure.

Design-to-cost and BOM optimization are primary levers to restore margins, cutting component spend and supplier complexity; targeted parts rationalization can reduce bill-of-material costs by double-digit percentages in device programs.

Higher service route density and remote diagnostics lower field-service hours and onsite visits, reducing service costs materially; combined with tiered hardware and subscription offerings Ricoh can preserve affordability for core customers while protecting premium mix and ASPs.

SMB vs enterprise mix

SMB spend is highly sensitive to credit and macro outlook, while enterprise budgets are slower-moving and stickier; Gartner reported global IT spending at about $4.7 trillion in 2024, with enterprises driving multi-year contracts. Channel programs and financing solutions help sustain SMB velocity, and enterprise deals favor integrated IT and security solutions; a balanced SMB/enterprise mix smooths revenue volatility.

- SMB sensitivity: credit, macro

- Enterprise: slower-moving, multi-year

- Channels/financing sustain SMB

- Enterprise favors integrated IT/security

- Balanced mix reduces volatility

Digital transformation investment

Enterprises are allocating significant budgets to cloud migration, workflow automation and data security as public cloud spending exceeded $600 billion in 2023 and continues double-digit growth into 2024–25; Ricoh’s IT services and document solutions map directly to those spend priorities. Cross-selling hardware into managed services increases customer lifetime value and Ricoh's ability to demonstrate ROI accelerates deal closure and recurring revenue adoption.

Tariffs, subsidies and CSRD reshape supply chains: regional manufacturing and dual-sourcing prevail

Ricoh's FY2024 revenue ≈1,523.6bn yen with services ≈55% smoothing cyclic device demand; operating margin ~4.6%. FX (USD/JPY ~140–155 in 2023–24) and materials/energy inflation (~3% global 2024) pressure margins; BOM optimization and service density cut costs. Enterprise IT spend ~$4.7T (2024) and >$600bn public cloud (2023) support cross-sell into managed services.

| Metric | Value |

|---|---|

| FY2024 revenue | 1,523.6bn JPY |

| Services % | ~55% |

| Op margin | ~4.6% |

| Global IT spend | $4.7T (2024) |

Full Version Awaits

Ricoh PESTLE Analysis

The Ricoh PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the final, downloadable file.