Rite Aid Boston Consulting Group Matrix

Unlock Strategic Clarity

Rite Aid’s BCG Matrix spotlight shows where its product lines are winning, where they’re bleeding margin, and which bets need a rethink — a quick snapshot that already sparks idea. Want the full playbook? Purchase the complete BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel files. Save time, present confidently, and start reallocating capital where it actually pays off.

Stars

Regional high-script pharmacies

In several Northeast and West Coast pockets, Rite Aid (ticker RAD) holds solid prescription share and steady foot traffic across roughly 2,000 stores, positioning those locations as Stars in the BCG matrix. These stores can grow further with population shifts and favorable payer contracts, while expanding immunizations and clinical consults—services that increased industry uptake into 2024. Maintain convenient hours and local marketing to protect the moat so they mature into cash cows as growth cools.

In‑store immunization engine

Vaccine demand remains sticky beyond COVID with routine influenza, newly available RSV adult vaccines (FDA approvals in 2023) and shingles continuing to drive foot traffic, making in‑store immunization a Stars business for Rite Aid given pharmacy workflow, trust and access that enable rapid uptake. The category grows but ties up working capital in staffing and vaccine inventory. Stay visible, keep appointment UX simple, and keep rolling.

Specialty & complex therapies access

High-touch meds (oncology, autoimmune) are a Stars lane for Rite Aid: specialty drugs made up about 50% of US drug spend in 2024 while prescription volume remains small, driving higher margin density and attractive market growth (industry CAGR ~7–8%). Prior authorization support, adherence programs and home/clinic delivery create material switching costs. Double down on payor contracts and care-team coordination to win local share.

Digital Rx refills + curbside/rapid pickup

Behavior has shifted: consumers demand fast, low-friction refills and Rite Aid’s Digital Rx (app refills + text updates + same-day curbside/rapid pickup) is driving repeat scripts; industry-tracking showed digital refill volume up ~24% year-over-year in 2024 while same-day pickup adoption reached roughly 35% of pharmacy pickups. Growth is running ahead of the core front store; keep the UX clean, tighten cycle times, and market aggressively to capture share.

- Tag: digital-growth ~24% YOY (2024)

- Tag: same-day pickup ~35% of pharmacy pickups (2024)

- Tag: drivers app refills + texts + rapid pickup

- Tag: priorities UX simplification, faster cycles, heavy marketing

PBM clinical programs via Elixir

PBM clinical programs via Elixir sit in the Stars quadrant as 2024 payer and employer demand for MTM, adherence and opioid stewardship accelerated, driving higher utilization of clinical services; when programs perform they measurably lift outcomes and retention across plan populations. Standing up analytics and dedicated account service is capital- and cash-hungry, with upfront investment risks. Worth the fuel if it secures multi‑year contracts and improved rebate economics.

2,000 high-share stores drive growth: +24% digital refills, 35% same-day — scale specialty/PBM

Rite Aid’s Stars: ~2,000 high-share stores in NE/West drive growth via immunizations and digital refills (+24% YOY in 2024) with same-day pickup ~35% of pickups. Specialty drugs (≈50% of US drug spend in 2024) and PBM clinical services (industry CAGR ~7–8%) are high-margin, high-growth but capital‑intensive; prioritize payor contracts, UX and staffing to convert to cash cows.

| Category | 2024 metric | Priority |

|---|---|---|

| High-share stores | ~2,000 stores | Local marketing, hours |

| Digital/refills | +24% YOY; same-day 35% | UX, cycle time |

| Specialty drugs | ≈50% US drug spend | Payor deals, adherence |

| PBM clinical | Rising RFPs; CAGR 7–8% | Analytics, contracts |

What is included in the product

Comprehensive BCG Matrix for Rite Aid, outlining Stars, Cash Cows, Question Marks, Dogs with investment and divestment guidance.

One-page Rite Aid BCG Matrix highlighting pain points per unit for fast executive decisions

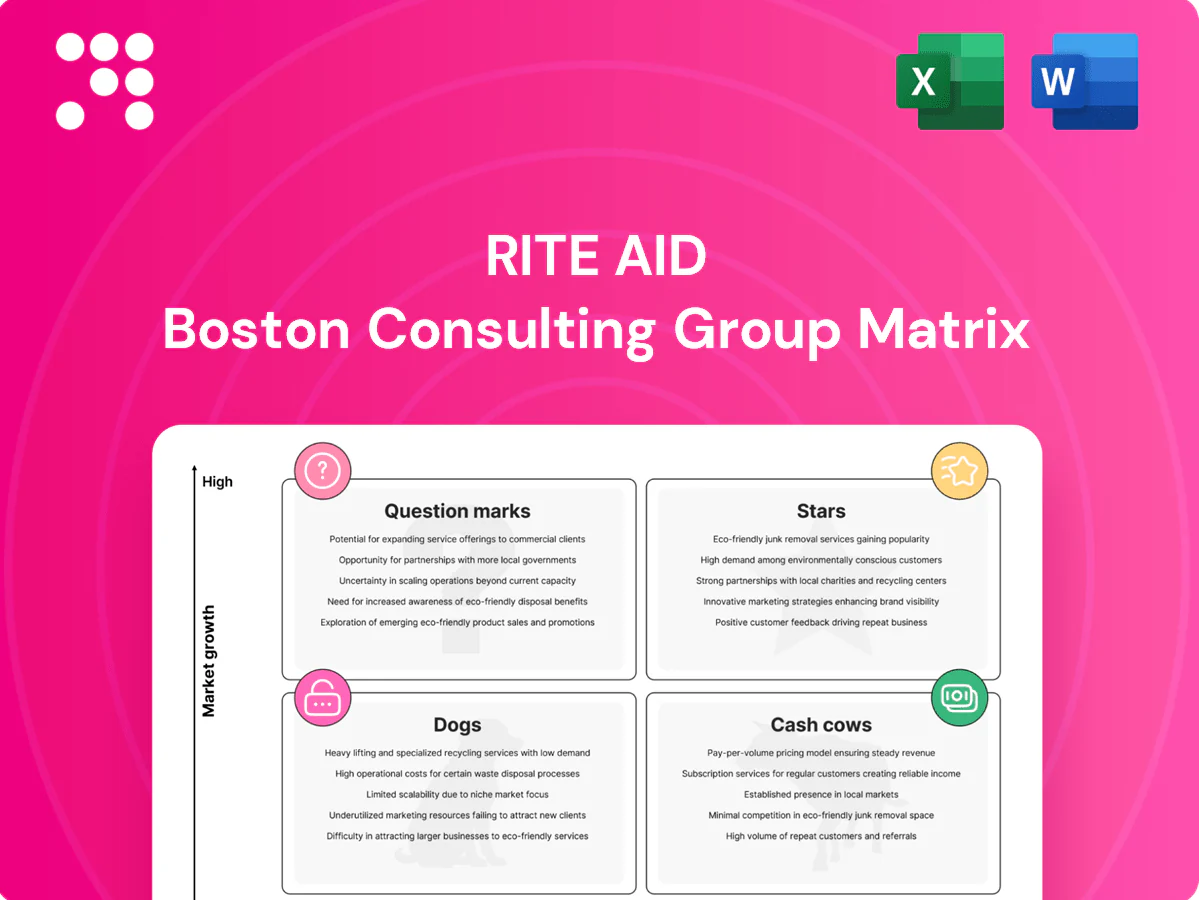

Cash Cows

Core prescription fills in mature markets

Core prescription fills for chronic meds—diabetes (about 34 million Americans with diagnosed diabetes), hypertension (roughly 45% of adults) and high cholesterol—deliver predictable, recurring demand and defensible margins. Low-growth but stable volumes drive steady contribution with efficient labor; minimal promotion needed. Operational excellence—better scheduling, higher inventory turns and sync programs—is where incremental margin is captured.

Front‑store OTC essentials

Front-store OTC essentials—pain relief, cough/cold, allergy, first aid—deliver steady, low-education demand with higher gross margins than prescription fill margins and strong basket attach on trip missions; prioritize price-match on key SKUs, merchandise via endcaps over paid media, tighten planograms and cull slow movers to free working capital while protecting front-end cash cows.

Private‑label health & beauty

Private‑label health & beauty delivers higher gross margins (typically 20–30% vs 10–15% for national brands) with acceptable velocity, letting Rite Aid convert steady sales into cash flow. Shoppers trade down but remain loyal when quality holds, supporting modest category growth (low‑single digits annually) while spinning free cash. Action: expand winning SKUs, trim duplication, and keep packaging national‑brand sharp to sustain margin capture.

Seasonal flu vaccinations

Seasonal flu vaccinations are an annual, predictable cash cow for Rite Aid, with the US market distributing roughly 170 million doses in recent seasons (2022–24 trend), making operations routine and marketing lift light as consumer habit drives uptake and repeat store visits.

They support scripts and larger baskets; standardizing staffing and procurement can raise margin per dose by tightening labor hours and negotiating vial/ingredient pricing.

- Predictable annual demand

- Habit-driven, low marketing spend

- Drives scripts and basket size

- Optimize staffing/procurement to boost cash per dose

Loyalty members’ repeat baskets

Loyalty members generate repeat baskets that give Rite Aid known customers, known trips and lower acquisition cost; 2024 reporting highlights flat same-store traffic but solid margin-per-visit from pharmacy mix and front-end sales, enabling targeted offers without expensive mass media. Nurture via simple rewards and fewer, better promos to preserve margin and frequency.

- Known customers / known trips

- Lower acquisition cost; targeted offers

- Flat-ish growth 2024; solid margin per visit

- Nurture: simple rewards, fewer better promos

Stable Rx+OTC cash; private margins 20-30%, 170M doses

Core chronic prescriptions (diabetes ~34M diagnosed; hypertension ~45% of adults) and routine OTCs deliver steady, low-growth cash flow with predictable margins and minimal promo spend. Private-label HBA (margins ~20–30% vs national 10–15%) and seasonal flu (US ~170M doses 2022–24) add high-margin, habitual revenue; loyalty keeps trips known with flat 2024 traffic.

| Segment | Fact |

|---|---|

| Diabetes | ~34 million diagnosed (US) |

| Hypertension | ~45% of adults |

| Flu vaccines | ~170 million doses (2022–24) |

| Private label | Margins ~20–30% vs 10–15% |

What You See Is What You Get

Rite Aid BCG Matrix

The file you're previewing is the final Rite Aid BCG Matrix you'll receive after purchase—no watermarks, no placeholders, just the finished analysis. It maps Stars, Cash Cows, Question Marks and Dogs for Rite Aid with clear visuals and actionable insights. Buy once and download immediately; the document is fully editable, presentation-ready, and designed for direct use in strategy meetings or investor decks.

Unlock Strategic Clarity

Rite Aid’s BCG Matrix spotlight shows where its product lines are winning, where they’re bleeding margin, and which bets need a rethink — a quick snapshot that already sparks idea. Want the full playbook? Purchase the complete BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel files. Save time, present confidently, and start reallocating capital where it actually pays off.

Stars

Regional high-script pharmacies

In several Northeast and West Coast pockets, Rite Aid (ticker RAD) holds solid prescription share and steady foot traffic across roughly 2,000 stores, positioning those locations as Stars in the BCG matrix. These stores can grow further with population shifts and favorable payer contracts, while expanding immunizations and clinical consults—services that increased industry uptake into 2024. Maintain convenient hours and local marketing to protect the moat so they mature into cash cows as growth cools.

In‑store immunization engine

Vaccine demand remains sticky beyond COVID with routine influenza, newly available RSV adult vaccines (FDA approvals in 2023) and shingles continuing to drive foot traffic, making in‑store immunization a Stars business for Rite Aid given pharmacy workflow, trust and access that enable rapid uptake. The category grows but ties up working capital in staffing and vaccine inventory. Stay visible, keep appointment UX simple, and keep rolling.

Specialty & complex therapies access

High-touch meds (oncology, autoimmune) are a Stars lane for Rite Aid: specialty drugs made up about 50% of US drug spend in 2024 while prescription volume remains small, driving higher margin density and attractive market growth (industry CAGR ~7–8%). Prior authorization support, adherence programs and home/clinic delivery create material switching costs. Double down on payor contracts and care-team coordination to win local share.

Digital Rx refills + curbside/rapid pickup

Behavior has shifted: consumers demand fast, low-friction refills and Rite Aid’s Digital Rx (app refills + text updates + same-day curbside/rapid pickup) is driving repeat scripts; industry-tracking showed digital refill volume up ~24% year-over-year in 2024 while same-day pickup adoption reached roughly 35% of pharmacy pickups. Growth is running ahead of the core front store; keep the UX clean, tighten cycle times, and market aggressively to capture share.

- Tag: digital-growth ~24% YOY (2024)

- Tag: same-day pickup ~35% of pharmacy pickups (2024)

- Tag: drivers app refills + texts + rapid pickup

- Tag: priorities UX simplification, faster cycles, heavy marketing

PBM clinical programs via Elixir

PBM clinical programs via Elixir sit in the Stars quadrant as 2024 payer and employer demand for MTM, adherence and opioid stewardship accelerated, driving higher utilization of clinical services; when programs perform they measurably lift outcomes and retention across plan populations. Standing up analytics and dedicated account service is capital- and cash-hungry, with upfront investment risks. Worth the fuel if it secures multi‑year contracts and improved rebate economics.

2,000 high-share stores drive growth: +24% digital refills, 35% same-day — scale specialty/PBM

Rite Aid’s Stars: ~2,000 high-share stores in NE/West drive growth via immunizations and digital refills (+24% YOY in 2024) with same-day pickup ~35% of pickups. Specialty drugs (≈50% of US drug spend in 2024) and PBM clinical services (industry CAGR ~7–8%) are high-margin, high-growth but capital‑intensive; prioritize payor contracts, UX and staffing to convert to cash cows.

| Category | 2024 metric | Priority |

|---|---|---|

| High-share stores | ~2,000 stores | Local marketing, hours |

| Digital/refills | +24% YOY; same-day 35% | UX, cycle time |

| Specialty drugs | ≈50% US drug spend | Payor deals, adherence |

| PBM clinical | Rising RFPs; CAGR 7–8% | Analytics, contracts |

What is included in the product

Comprehensive BCG Matrix for Rite Aid, outlining Stars, Cash Cows, Question Marks, Dogs with investment and divestment guidance.

One-page Rite Aid BCG Matrix highlighting pain points per unit for fast executive decisions

Cash Cows

Core prescription fills in mature markets

Core prescription fills for chronic meds—diabetes (about 34 million Americans with diagnosed diabetes), hypertension (roughly 45% of adults) and high cholesterol—deliver predictable, recurring demand and defensible margins. Low-growth but stable volumes drive steady contribution with efficient labor; minimal promotion needed. Operational excellence—better scheduling, higher inventory turns and sync programs—is where incremental margin is captured.

Front‑store OTC essentials

Front-store OTC essentials—pain relief, cough/cold, allergy, first aid—deliver steady, low-education demand with higher gross margins than prescription fill margins and strong basket attach on trip missions; prioritize price-match on key SKUs, merchandise via endcaps over paid media, tighten planograms and cull slow movers to free working capital while protecting front-end cash cows.

Private‑label health & beauty

Private‑label health & beauty delivers higher gross margins (typically 20–30% vs 10–15% for national brands) with acceptable velocity, letting Rite Aid convert steady sales into cash flow. Shoppers trade down but remain loyal when quality holds, supporting modest category growth (low‑single digits annually) while spinning free cash. Action: expand winning SKUs, trim duplication, and keep packaging national‑brand sharp to sustain margin capture.

Seasonal flu vaccinations

Seasonal flu vaccinations are an annual, predictable cash cow for Rite Aid, with the US market distributing roughly 170 million doses in recent seasons (2022–24 trend), making operations routine and marketing lift light as consumer habit drives uptake and repeat store visits.

They support scripts and larger baskets; standardizing staffing and procurement can raise margin per dose by tightening labor hours and negotiating vial/ingredient pricing.

- Predictable annual demand

- Habit-driven, low marketing spend

- Drives scripts and basket size

- Optimize staffing/procurement to boost cash per dose

Loyalty members’ repeat baskets

Loyalty members generate repeat baskets that give Rite Aid known customers, known trips and lower acquisition cost; 2024 reporting highlights flat same-store traffic but solid margin-per-visit from pharmacy mix and front-end sales, enabling targeted offers without expensive mass media. Nurture via simple rewards and fewer, better promos to preserve margin and frequency.

- Known customers / known trips

- Lower acquisition cost; targeted offers

- Flat-ish growth 2024; solid margin per visit

- Nurture: simple rewards, fewer better promos

Stable Rx+OTC cash; private margins 20-30%, 170M doses

Core chronic prescriptions (diabetes ~34M diagnosed; hypertension ~45% of adults) and routine OTCs deliver steady, low-growth cash flow with predictable margins and minimal promo spend. Private-label HBA (margins ~20–30% vs national 10–15%) and seasonal flu (US ~170M doses 2022–24) add high-margin, habitual revenue; loyalty keeps trips known with flat 2024 traffic.

| Segment | Fact |

|---|---|

| Diabetes | ~34 million diagnosed (US) |

| Hypertension | ~45% of adults |

| Flu vaccines | ~170 million doses (2022–24) |

| Private label | Margins ~20–30% vs 10–15% |

What You See Is What You Get

Rite Aid BCG Matrix

The file you're previewing is the final Rite Aid BCG Matrix you'll receive after purchase—no watermarks, no placeholders, just the finished analysis. It maps Stars, Cash Cows, Question Marks and Dogs for Rite Aid with clear visuals and actionable insights. Buy once and download immediately; the document is fully editable, presentation-ready, and designed for direct use in strategy meetings or investor decks.

Original: $10.00

-65%$10.00

$3.50Description

Unlock Strategic Clarity

Rite Aid’s BCG Matrix spotlight shows where its product lines are winning, where they’re bleeding margin, and which bets need a rethink — a quick snapshot that already sparks idea. Want the full playbook? Purchase the complete BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel files. Save time, present confidently, and start reallocating capital where it actually pays off.

Stars

Regional high-script pharmacies

In several Northeast and West Coast pockets, Rite Aid (ticker RAD) holds solid prescription share and steady foot traffic across roughly 2,000 stores, positioning those locations as Stars in the BCG matrix. These stores can grow further with population shifts and favorable payer contracts, while expanding immunizations and clinical consults—services that increased industry uptake into 2024. Maintain convenient hours and local marketing to protect the moat so they mature into cash cows as growth cools.

In‑store immunization engine

Vaccine demand remains sticky beyond COVID with routine influenza, newly available RSV adult vaccines (FDA approvals in 2023) and shingles continuing to drive foot traffic, making in‑store immunization a Stars business for Rite Aid given pharmacy workflow, trust and access that enable rapid uptake. The category grows but ties up working capital in staffing and vaccine inventory. Stay visible, keep appointment UX simple, and keep rolling.

Specialty & complex therapies access

High-touch meds (oncology, autoimmune) are a Stars lane for Rite Aid: specialty drugs made up about 50% of US drug spend in 2024 while prescription volume remains small, driving higher margin density and attractive market growth (industry CAGR ~7–8%). Prior authorization support, adherence programs and home/clinic delivery create material switching costs. Double down on payor contracts and care-team coordination to win local share.

Digital Rx refills + curbside/rapid pickup

Behavior has shifted: consumers demand fast, low-friction refills and Rite Aid’s Digital Rx (app refills + text updates + same-day curbside/rapid pickup) is driving repeat scripts; industry-tracking showed digital refill volume up ~24% year-over-year in 2024 while same-day pickup adoption reached roughly 35% of pharmacy pickups. Growth is running ahead of the core front store; keep the UX clean, tighten cycle times, and market aggressively to capture share.

- Tag: digital-growth ~24% YOY (2024)

- Tag: same-day pickup ~35% of pharmacy pickups (2024)

- Tag: drivers app refills + texts + rapid pickup

- Tag: priorities UX simplification, faster cycles, heavy marketing

PBM clinical programs via Elixir

PBM clinical programs via Elixir sit in the Stars quadrant as 2024 payer and employer demand for MTM, adherence and opioid stewardship accelerated, driving higher utilization of clinical services; when programs perform they measurably lift outcomes and retention across plan populations. Standing up analytics and dedicated account service is capital- and cash-hungry, with upfront investment risks. Worth the fuel if it secures multi‑year contracts and improved rebate economics.

2,000 high-share stores drive growth: +24% digital refills, 35% same-day — scale specialty/PBM

Rite Aid’s Stars: ~2,000 high-share stores in NE/West drive growth via immunizations and digital refills (+24% YOY in 2024) with same-day pickup ~35% of pickups. Specialty drugs (≈50% of US drug spend in 2024) and PBM clinical services (industry CAGR ~7–8%) are high-margin, high-growth but capital‑intensive; prioritize payor contracts, UX and staffing to convert to cash cows.

| Category | 2024 metric | Priority |

|---|---|---|

| High-share stores | ~2,000 stores | Local marketing, hours |

| Digital/refills | +24% YOY; same-day 35% | UX, cycle time |

| Specialty drugs | ≈50% US drug spend | Payor deals, adherence |

| PBM clinical | Rising RFPs; CAGR 7–8% | Analytics, contracts |

What is included in the product

Comprehensive BCG Matrix for Rite Aid, outlining Stars, Cash Cows, Question Marks, Dogs with investment and divestment guidance.

One-page Rite Aid BCG Matrix highlighting pain points per unit for fast executive decisions

Cash Cows

Core prescription fills in mature markets

Core prescription fills for chronic meds—diabetes (about 34 million Americans with diagnosed diabetes), hypertension (roughly 45% of adults) and high cholesterol—deliver predictable, recurring demand and defensible margins. Low-growth but stable volumes drive steady contribution with efficient labor; minimal promotion needed. Operational excellence—better scheduling, higher inventory turns and sync programs—is where incremental margin is captured.

Front‑store OTC essentials

Front-store OTC essentials—pain relief, cough/cold, allergy, first aid—deliver steady, low-education demand with higher gross margins than prescription fill margins and strong basket attach on trip missions; prioritize price-match on key SKUs, merchandise via endcaps over paid media, tighten planograms and cull slow movers to free working capital while protecting front-end cash cows.

Private‑label health & beauty

Private‑label health & beauty delivers higher gross margins (typically 20–30% vs 10–15% for national brands) with acceptable velocity, letting Rite Aid convert steady sales into cash flow. Shoppers trade down but remain loyal when quality holds, supporting modest category growth (low‑single digits annually) while spinning free cash. Action: expand winning SKUs, trim duplication, and keep packaging national‑brand sharp to sustain margin capture.

Seasonal flu vaccinations

Seasonal flu vaccinations are an annual, predictable cash cow for Rite Aid, with the US market distributing roughly 170 million doses in recent seasons (2022–24 trend), making operations routine and marketing lift light as consumer habit drives uptake and repeat store visits.

They support scripts and larger baskets; standardizing staffing and procurement can raise margin per dose by tightening labor hours and negotiating vial/ingredient pricing.

- Predictable annual demand

- Habit-driven, low marketing spend

- Drives scripts and basket size

- Optimize staffing/procurement to boost cash per dose

Loyalty members’ repeat baskets

Loyalty members generate repeat baskets that give Rite Aid known customers, known trips and lower acquisition cost; 2024 reporting highlights flat same-store traffic but solid margin-per-visit from pharmacy mix and front-end sales, enabling targeted offers without expensive mass media. Nurture via simple rewards and fewer, better promos to preserve margin and frequency.

- Known customers / known trips

- Lower acquisition cost; targeted offers

- Flat-ish growth 2024; solid margin per visit

- Nurture: simple rewards, fewer better promos

Stable Rx+OTC cash; private margins 20-30%, 170M doses

Core chronic prescriptions (diabetes ~34M diagnosed; hypertension ~45% of adults) and routine OTCs deliver steady, low-growth cash flow with predictable margins and minimal promo spend. Private-label HBA (margins ~20–30% vs national 10–15%) and seasonal flu (US ~170M doses 2022–24) add high-margin, habitual revenue; loyalty keeps trips known with flat 2024 traffic.

| Segment | Fact |

|---|---|

| Diabetes | ~34 million diagnosed (US) |

| Hypertension | ~45% of adults |

| Flu vaccines | ~170 million doses (2022–24) |

| Private label | Margins ~20–30% vs 10–15% |

What You See Is What You Get

Rite Aid BCG Matrix

The file you're previewing is the final Rite Aid BCG Matrix you'll receive after purchase—no watermarks, no placeholders, just the finished analysis. It maps Stars, Cash Cows, Question Marks and Dogs for Rite Aid with clear visuals and actionable insights. Buy once and download immediately; the document is fully editable, presentation-ready, and designed for direct use in strategy meetings or investor decks.