Rite Aid Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

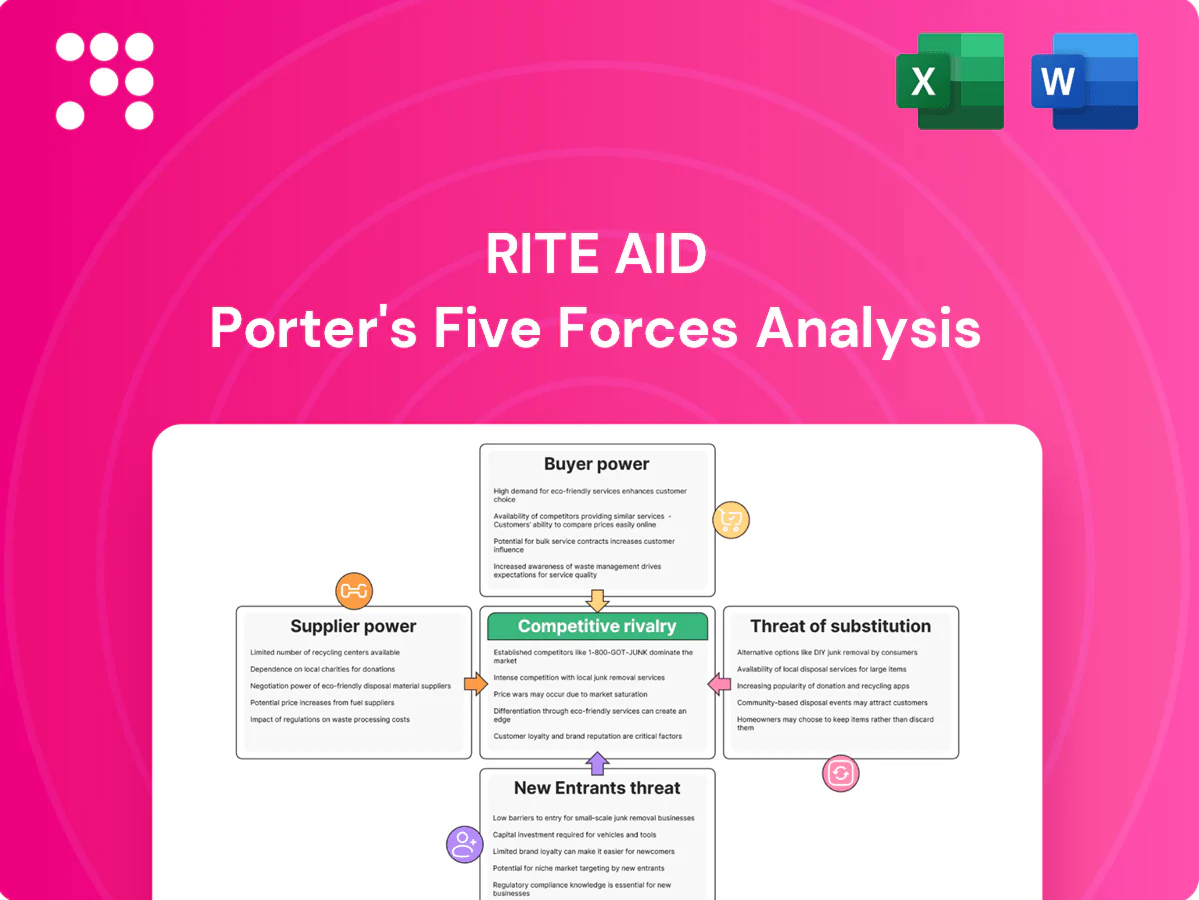

Rite Aid faces intense rivalry from national chains and tight margins that compress profitability. Supplier leverage is moderate, buyers are price-sensitive, and threats from new entrants and digital substitutes shape strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Rite Aid’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

Brand-name drug makers remain few and wield pricing power via patents and limited substitutes, keeping brand drugs responsible for the majority of pharmacy spend. Rite Aid, with roughly $21.6 billion revenue in 2022 and weakened scale after its Oct 2023 Chapter 11 filing, has less negotiation leverage than CVS and Walgreens. List-price pressure is partly offset by rebates funneled through its PBM Elixir, but net costs still hinge on formulary placements and rebate dynamics.

Supplier Power 2

Generic manufacturers supply roughly 90% of US prescriptions, a fragmentation that tempers individual supplier leverage for retailers like Rite Aid. However, periodic shortages and FDA actions have repeatedly spiked prices and cut availability, especially for sterile injectables. Consolidation among manufacturers of certain molecules raises dependency risk. Multi-sourcing and expanding private label assortments materially mitigate exposure.

Supplier Power 3

Drug wholesalers are highly concentrated—McKesson, AmerisourceBergen and Cardinal account for roughly 85%–90% of U.S. pharmaceutical distribution in 2024—giving them substantial channel leverage over retailers like Rite Aid. Long-term distribution agreements determine pricing, service levels and working capital terms, materially affecting Rite Aid’s gross margins and cash flow. Meaningful switching costs from IT integration, logistics and supplier credit terms further elevate supplier power over Rite Aid.

Supplier Power 4

Medical device, beauty, and CPG national brands exert strong leverage over Rite Aid, driving traffic yet demanding favorable placement and contributing roughly 60-70% of category sales; private-label assortment, which can deliver ~15-25% higher gross margins, provides counter-leverage and margin relief. Seasonal and health events (eg flu season, allergy spikes) temporarily boost supplier bargaining power and promotional spend, shifting short-term terms.

- Supplier placement pressure: national brands dominate 60-70% of category sales

- Private-label margin lift: ~15-25% higher gross margin vs national brands

- Promotional spend: national brands push promotional allowances and slotting fees

- Seasonality: flu/allergy peaks tighten supplier terms temporarily

Supplier Power 5

Regulatory controls by FDA and DEA on controlled substances tighten supply flexibility, where enforcement actions have historically triggered short-term stockouts and higher compliance costs for pharmacy chains. Elixir, acquired by Rite Aid in 2021, provides formulary steering and some leverage but covers a limited PBM population relative to national plans. Clinical and legal limits—mandated checks, prescription monitoring programs—still cap Rite Aid’s negotiating room with suppliers.

- Rite Aid stores ~2,000 nationwide (2024)

- Elixir acquisition 2021 strengthens but does not negate supplier power

- DEA/FDA enforcement risks drive compliance costs and supply disruption

High supplier concentration (85-90%) compresses margins; private-label and PBM provide relief

Supplier power is high: brand drug patents and concentrated wholesalers (McKesson, AmerisourceBergen, Cardinal ~85–90% distribution) constrain Rite Aid (2022 revenue $21.6B; ~2,000 stores). Generics (~90% prescriptions) dilute individual leverage but shortages raise risk. Private-label (~15–25% higher gross margin) and PBM Elixir partially offset supplier pressure.

| Metric | Value |

|---|---|

| Revenue (2022) | $21.6B |

| Wholesaler share (2024) | 85–90% |

| Generics share | ~90% |

| Stores (2024) | ~2,000 |

| Private-label margin lift | 15–25% |

What is included in the product

Tailored Porter's Five Forces analysis for Rite Aid that uncovers competitive pressures, supplier and buyer bargaining power, threat of substitutes and new entrants, and identifies disruptive trends and strategic levers affecting its pricing, margins, and market share.

A clear, one-sheet summary of Rite Aid's five forces—perfect for quick decision-making and slide-ready decks that pinpoint competitive pain points and strategic levers.

Customers Bargaining Power

Buyer Power 1

Health plan sponsors and PBMs wield strong pricing and reimbursement power; the three largest PBMs control roughly 80% of U.S. retail prescription claims, steering formulary placement and rebates that determine volume. Network inclusion and preferred tiers directly dictate script flow to pharmacies. Rite Aid’s in-house PBM, Elixir, provides some leverage but competes with larger PBMs for contracts. Plan sponsor switches can rapidly reassign scripts and revenues.

Buyer Power 2

In 2024 buyer power is elevated: consumers remain highly price sensitive on front-end items and increasingly on prescriptions due to price-transparency tools and apps; Rite Aid’s Wellness+ loyalty adds stickiness but provides limited pricing insulation; growth of high-deductible plans shifts more prescriptions to out-of-pocket comparison shopping; proximity and convenience mitigate some price pressure for store visits.

Buyer Power 3

Large employer groups and government programs negotiate aggressively, with Medicare/Medicaid representing roughly one-third of retail prescription volume and compressing pharmacy margins; industry DIR fees exceeded about $8 billion in recent years, heightening buyer leverage; Rite Aid cited reimbursement pressure in FY2024 that tightened margins, and contract renewals can swing profitability by several percentage points of EBITDA.

Buyer Power 4

Prescribers shape pharmacy choice via e-prescribing defaults and counseling; Surescripts reported over 95% of U.S. prescriptions were e-prescribed in 2024, increasing referral leverage. Health system-owned pharmacies steer patients in-network, raising customer bargaining power. Rite Aid must deepen provider ties and expand clinical services (immunizations, point-of-care testing) to boost referral stickiness and retain fills.

- Prescriber defaults: high impact

- 95% e-prescribing (Surescripts 2024)

- Health systems steer in-network

- Clinical services increase retention

Buyer Power 5

Digital channels raise price transparency and make switching easier, with Amazon Pharmacy (launched 2020) and mail-order services intensifying buyer leverage. Coupon apps and mail-order alternatives push down margins and increase price sensitivity. Same-day and delivery options are now table stakes; failure to match convenience risks demand erosion for Rite Aid.

- Buyer Power: 5

- Amazon Pharmacy launched 2020

- Same-day delivery expected by consumers

Top‑3 PBMs control ~80%; DIR fees >$8B squeeze margins

PBMs/front‑end buyers exert strong pricing power; top three PBMs process ~80% of U.S. retail scripts, steering rebates and volume. Medicare/Medicaid account for ~1/3 of retail Rx and DIR fees exceeded ~$8B, compressing margins. E‑prescribing reached ~95% in 2024, boosting prescriber influence; Amazon Pharmacy and mail‑order increase price transparency and switching.

| Metric | 2024 |

|---|---|

| Top‑3 PBM share | ~80% |

| Medicare/Medicaid share | ~33% |

| DIR fees (annual) | ~$8B+ |

| E‑prescribing | ~95% |

Full Version Awaits

Rite Aid Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Rite Aid assesses competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, highlighting strategic risks and opportunities for investors and managers. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

A Must-Have Tool for Decision-Makers

Rite Aid faces intense rivalry from national chains and tight margins that compress profitability. Supplier leverage is moderate, buyers are price-sensitive, and threats from new entrants and digital substitutes shape strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Rite Aid’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

Brand-name drug makers remain few and wield pricing power via patents and limited substitutes, keeping brand drugs responsible for the majority of pharmacy spend. Rite Aid, with roughly $21.6 billion revenue in 2022 and weakened scale after its Oct 2023 Chapter 11 filing, has less negotiation leverage than CVS and Walgreens. List-price pressure is partly offset by rebates funneled through its PBM Elixir, but net costs still hinge on formulary placements and rebate dynamics.

Supplier Power 2

Generic manufacturers supply roughly 90% of US prescriptions, a fragmentation that tempers individual supplier leverage for retailers like Rite Aid. However, periodic shortages and FDA actions have repeatedly spiked prices and cut availability, especially for sterile injectables. Consolidation among manufacturers of certain molecules raises dependency risk. Multi-sourcing and expanding private label assortments materially mitigate exposure.

Supplier Power 3

Drug wholesalers are highly concentrated—McKesson, AmerisourceBergen and Cardinal account for roughly 85%–90% of U.S. pharmaceutical distribution in 2024—giving them substantial channel leverage over retailers like Rite Aid. Long-term distribution agreements determine pricing, service levels and working capital terms, materially affecting Rite Aid’s gross margins and cash flow. Meaningful switching costs from IT integration, logistics and supplier credit terms further elevate supplier power over Rite Aid.

Supplier Power 4

Medical device, beauty, and CPG national brands exert strong leverage over Rite Aid, driving traffic yet demanding favorable placement and contributing roughly 60-70% of category sales; private-label assortment, which can deliver ~15-25% higher gross margins, provides counter-leverage and margin relief. Seasonal and health events (eg flu season, allergy spikes) temporarily boost supplier bargaining power and promotional spend, shifting short-term terms.

- Supplier placement pressure: national brands dominate 60-70% of category sales

- Private-label margin lift: ~15-25% higher gross margin vs national brands

- Promotional spend: national brands push promotional allowances and slotting fees

- Seasonality: flu/allergy peaks tighten supplier terms temporarily

Supplier Power 5

Regulatory controls by FDA and DEA on controlled substances tighten supply flexibility, where enforcement actions have historically triggered short-term stockouts and higher compliance costs for pharmacy chains. Elixir, acquired by Rite Aid in 2021, provides formulary steering and some leverage but covers a limited PBM population relative to national plans. Clinical and legal limits—mandated checks, prescription monitoring programs—still cap Rite Aid’s negotiating room with suppliers.

- Rite Aid stores ~2,000 nationwide (2024)

- Elixir acquisition 2021 strengthens but does not negate supplier power

- DEA/FDA enforcement risks drive compliance costs and supply disruption

High supplier concentration (85-90%) compresses margins; private-label and PBM provide relief

Supplier power is high: brand drug patents and concentrated wholesalers (McKesson, AmerisourceBergen, Cardinal ~85–90% distribution) constrain Rite Aid (2022 revenue $21.6B; ~2,000 stores). Generics (~90% prescriptions) dilute individual leverage but shortages raise risk. Private-label (~15–25% higher gross margin) and PBM Elixir partially offset supplier pressure.

| Metric | Value |

|---|---|

| Revenue (2022) | $21.6B |

| Wholesaler share (2024) | 85–90% |

| Generics share | ~90% |

| Stores (2024) | ~2,000 |

| Private-label margin lift | 15–25% |

What is included in the product

Tailored Porter's Five Forces analysis for Rite Aid that uncovers competitive pressures, supplier and buyer bargaining power, threat of substitutes and new entrants, and identifies disruptive trends and strategic levers affecting its pricing, margins, and market share.

A clear, one-sheet summary of Rite Aid's five forces—perfect for quick decision-making and slide-ready decks that pinpoint competitive pain points and strategic levers.

Customers Bargaining Power

Buyer Power 1

Health plan sponsors and PBMs wield strong pricing and reimbursement power; the three largest PBMs control roughly 80% of U.S. retail prescription claims, steering formulary placement and rebates that determine volume. Network inclusion and preferred tiers directly dictate script flow to pharmacies. Rite Aid’s in-house PBM, Elixir, provides some leverage but competes with larger PBMs for contracts. Plan sponsor switches can rapidly reassign scripts and revenues.

Buyer Power 2

In 2024 buyer power is elevated: consumers remain highly price sensitive on front-end items and increasingly on prescriptions due to price-transparency tools and apps; Rite Aid’s Wellness+ loyalty adds stickiness but provides limited pricing insulation; growth of high-deductible plans shifts more prescriptions to out-of-pocket comparison shopping; proximity and convenience mitigate some price pressure for store visits.

Buyer Power 3

Large employer groups and government programs negotiate aggressively, with Medicare/Medicaid representing roughly one-third of retail prescription volume and compressing pharmacy margins; industry DIR fees exceeded about $8 billion in recent years, heightening buyer leverage; Rite Aid cited reimbursement pressure in FY2024 that tightened margins, and contract renewals can swing profitability by several percentage points of EBITDA.

Buyer Power 4

Prescribers shape pharmacy choice via e-prescribing defaults and counseling; Surescripts reported over 95% of U.S. prescriptions were e-prescribed in 2024, increasing referral leverage. Health system-owned pharmacies steer patients in-network, raising customer bargaining power. Rite Aid must deepen provider ties and expand clinical services (immunizations, point-of-care testing) to boost referral stickiness and retain fills.

- Prescriber defaults: high impact

- 95% e-prescribing (Surescripts 2024)

- Health systems steer in-network

- Clinical services increase retention

Buyer Power 5

Digital channels raise price transparency and make switching easier, with Amazon Pharmacy (launched 2020) and mail-order services intensifying buyer leverage. Coupon apps and mail-order alternatives push down margins and increase price sensitivity. Same-day and delivery options are now table stakes; failure to match convenience risks demand erosion for Rite Aid.

- Buyer Power: 5

- Amazon Pharmacy launched 2020

- Same-day delivery expected by consumers

Top‑3 PBMs control ~80%; DIR fees >$8B squeeze margins

PBMs/front‑end buyers exert strong pricing power; top three PBMs process ~80% of U.S. retail scripts, steering rebates and volume. Medicare/Medicaid account for ~1/3 of retail Rx and DIR fees exceeded ~$8B, compressing margins. E‑prescribing reached ~95% in 2024, boosting prescriber influence; Amazon Pharmacy and mail‑order increase price transparency and switching.

| Metric | 2024 |

|---|---|

| Top‑3 PBM share | ~80% |

| Medicare/Medicaid share | ~33% |

| DIR fees (annual) | ~$8B+ |

| E‑prescribing | ~95% |

Full Version Awaits

Rite Aid Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Rite Aid assesses competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, highlighting strategic risks and opportunities for investors and managers. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Rite Aid faces intense rivalry from national chains and tight margins that compress profitability. Supplier leverage is moderate, buyers are price-sensitive, and threats from new entrants and digital substitutes shape strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Rite Aid’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

Brand-name drug makers remain few and wield pricing power via patents and limited substitutes, keeping brand drugs responsible for the majority of pharmacy spend. Rite Aid, with roughly $21.6 billion revenue in 2022 and weakened scale after its Oct 2023 Chapter 11 filing, has less negotiation leverage than CVS and Walgreens. List-price pressure is partly offset by rebates funneled through its PBM Elixir, but net costs still hinge on formulary placements and rebate dynamics.

Supplier Power 2

Generic manufacturers supply roughly 90% of US prescriptions, a fragmentation that tempers individual supplier leverage for retailers like Rite Aid. However, periodic shortages and FDA actions have repeatedly spiked prices and cut availability, especially for sterile injectables. Consolidation among manufacturers of certain molecules raises dependency risk. Multi-sourcing and expanding private label assortments materially mitigate exposure.

Supplier Power 3

Drug wholesalers are highly concentrated—McKesson, AmerisourceBergen and Cardinal account for roughly 85%–90% of U.S. pharmaceutical distribution in 2024—giving them substantial channel leverage over retailers like Rite Aid. Long-term distribution agreements determine pricing, service levels and working capital terms, materially affecting Rite Aid’s gross margins and cash flow. Meaningful switching costs from IT integration, logistics and supplier credit terms further elevate supplier power over Rite Aid.

Supplier Power 4

Medical device, beauty, and CPG national brands exert strong leverage over Rite Aid, driving traffic yet demanding favorable placement and contributing roughly 60-70% of category sales; private-label assortment, which can deliver ~15-25% higher gross margins, provides counter-leverage and margin relief. Seasonal and health events (eg flu season, allergy spikes) temporarily boost supplier bargaining power and promotional spend, shifting short-term terms.

- Supplier placement pressure: national brands dominate 60-70% of category sales

- Private-label margin lift: ~15-25% higher gross margin vs national brands

- Promotional spend: national brands push promotional allowances and slotting fees

- Seasonality: flu/allergy peaks tighten supplier terms temporarily

Supplier Power 5

Regulatory controls by FDA and DEA on controlled substances tighten supply flexibility, where enforcement actions have historically triggered short-term stockouts and higher compliance costs for pharmacy chains. Elixir, acquired by Rite Aid in 2021, provides formulary steering and some leverage but covers a limited PBM population relative to national plans. Clinical and legal limits—mandated checks, prescription monitoring programs—still cap Rite Aid’s negotiating room with suppliers.

- Rite Aid stores ~2,000 nationwide (2024)

- Elixir acquisition 2021 strengthens but does not negate supplier power

- DEA/FDA enforcement risks drive compliance costs and supply disruption

High supplier concentration (85-90%) compresses margins; private-label and PBM provide relief

Supplier power is high: brand drug patents and concentrated wholesalers (McKesson, AmerisourceBergen, Cardinal ~85–90% distribution) constrain Rite Aid (2022 revenue $21.6B; ~2,000 stores). Generics (~90% prescriptions) dilute individual leverage but shortages raise risk. Private-label (~15–25% higher gross margin) and PBM Elixir partially offset supplier pressure.

| Metric | Value |

|---|---|

| Revenue (2022) | $21.6B |

| Wholesaler share (2024) | 85–90% |

| Generics share | ~90% |

| Stores (2024) | ~2,000 |

| Private-label margin lift | 15–25% |

What is included in the product

Tailored Porter's Five Forces analysis for Rite Aid that uncovers competitive pressures, supplier and buyer bargaining power, threat of substitutes and new entrants, and identifies disruptive trends and strategic levers affecting its pricing, margins, and market share.

A clear, one-sheet summary of Rite Aid's five forces—perfect for quick decision-making and slide-ready decks that pinpoint competitive pain points and strategic levers.

Customers Bargaining Power

Buyer Power 1

Health plan sponsors and PBMs wield strong pricing and reimbursement power; the three largest PBMs control roughly 80% of U.S. retail prescription claims, steering formulary placement and rebates that determine volume. Network inclusion and preferred tiers directly dictate script flow to pharmacies. Rite Aid’s in-house PBM, Elixir, provides some leverage but competes with larger PBMs for contracts. Plan sponsor switches can rapidly reassign scripts and revenues.

Buyer Power 2

In 2024 buyer power is elevated: consumers remain highly price sensitive on front-end items and increasingly on prescriptions due to price-transparency tools and apps; Rite Aid’s Wellness+ loyalty adds stickiness but provides limited pricing insulation; growth of high-deductible plans shifts more prescriptions to out-of-pocket comparison shopping; proximity and convenience mitigate some price pressure for store visits.

Buyer Power 3

Large employer groups and government programs negotiate aggressively, with Medicare/Medicaid representing roughly one-third of retail prescription volume and compressing pharmacy margins; industry DIR fees exceeded about $8 billion in recent years, heightening buyer leverage; Rite Aid cited reimbursement pressure in FY2024 that tightened margins, and contract renewals can swing profitability by several percentage points of EBITDA.

Buyer Power 4

Prescribers shape pharmacy choice via e-prescribing defaults and counseling; Surescripts reported over 95% of U.S. prescriptions were e-prescribed in 2024, increasing referral leverage. Health system-owned pharmacies steer patients in-network, raising customer bargaining power. Rite Aid must deepen provider ties and expand clinical services (immunizations, point-of-care testing) to boost referral stickiness and retain fills.

- Prescriber defaults: high impact

- 95% e-prescribing (Surescripts 2024)

- Health systems steer in-network

- Clinical services increase retention

Buyer Power 5

Digital channels raise price transparency and make switching easier, with Amazon Pharmacy (launched 2020) and mail-order services intensifying buyer leverage. Coupon apps and mail-order alternatives push down margins and increase price sensitivity. Same-day and delivery options are now table stakes; failure to match convenience risks demand erosion for Rite Aid.

- Buyer Power: 5

- Amazon Pharmacy launched 2020

- Same-day delivery expected by consumers

Top‑3 PBMs control ~80%; DIR fees >$8B squeeze margins

PBMs/front‑end buyers exert strong pricing power; top three PBMs process ~80% of U.S. retail scripts, steering rebates and volume. Medicare/Medicaid account for ~1/3 of retail Rx and DIR fees exceeded ~$8B, compressing margins. E‑prescribing reached ~95% in 2024, boosting prescriber influence; Amazon Pharmacy and mail‑order increase price transparency and switching.

| Metric | 2024 |

|---|---|

| Top‑3 PBM share | ~80% |

| Medicare/Medicaid share | ~33% |

| DIR fees (annual) | ~$8B+ |

| E‑prescribing | ~95% |

Full Version Awaits

Rite Aid Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Rite Aid assesses competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, highlighting strategic risks and opportunities for investors and managers. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.