Independent Bank Business Model Canvas

Business Model Canvas: Regional bank strategy, revenue and growth playbook for investors

Unlock the full strategic blueprint behind Independent Bank’s business model in a concise, actionable format that spotlights value propositions, revenue streams, and competitive levers. This in-depth Business Model Canvas reveals how the bank acquires customers, manages risk, and scales profitably. Ideal for investors, advisors, and executives seeking a ready-to-use tool—download the complete canvas to benchmark, plan, and capitalize on opportunities.

Partnerships

Correspondent banks

Partnering with larger correspondent banks expands payment clearing, foreign exchange, and liquidity access, tapping global rails that in 2024 routed roughly 40 million SWIFT messages per day. These relationships enable wire processing, check clearing, and interbank settlements at scale, lowering per-transaction friction and cost. They enhance service reliability for clients and provide contingency liquidity and settlement support during stressed market conditions.

Fintech and core providers

Alliances with core banking, digital banking, and fintech vendors power online and mobile capabilities and enabled many banks to cut feature rollout times by roughly 30%, according to industry benchmarks in 2024. These partners accelerate security upgrades and data integrations while joint roadmaps keep customer experiences modern and competitive. Outsourcing lowers build costs versus fully in‑house development, often reducing upfront spend by double‑digit percentages.

Payment networks

Membership in card and payment networks (Visa ~3.9 billion cards 2023, Mastercard ~2.8 billion cards) enables debit issuance and merchant services, expanding customer access and interchange income. Network partnerships provide ATM interoperability and support real-time rails to speed settlements and reduce float. They drive interchange revenue opportunities and broader acceptance, while compliance and network branding bolster trust and usage.

Broker-dealers and insurers

Strategic ties with broker-dealers and insurance carriers expand Independent Bank's wealth and insurance offerings, leveraging 2024 U.S. brokerage assets exceeding $25 trillion to access scale. Partners supply product shelves, underwriting and advisory tools, enabling co-branded solutions that deepen wallet share among retail and business clients. Revenue-sharing arrangements, often in the 10-40% range depending on product, align incentives around client outcomes.

- Product shelves & underwriting

- Advisory tools & distribution

- Co-branded wallet-share gains

- Revenue-share aligns incentives

Community and civic groups

Local nonprofits, chambers, and municipalities anchor community engagement, and in 2024 partnerships expanded outreach to support financial literacy, small-business growth, and CRA initiatives. These collaborations build brand goodwill and drive grassroots acquisition through events, workshops, and referral networks. Insights from civic groups directly inform localized product features and branch placement strategies.

- Local nonprofits

- Chambers of commerce

- Municipal partnerships

- Financial literacy programs

- Small-business support

- CRA alignment

Ecosystem: 40M SWIFT msgs, 30% faster rollouts, 3.9B/2.8B cards, $25T

Independent Bank leverages correspondent banks (SWIFT ~40M msgs/day in 2024) for clearing, FX and contingency liquidity; fintech/core vendors cut feature rollout ~30% in 2024 and lower build costs; card networks (Visa 3.9B, Mastercard 2.8B cards) drive interchange and real‑time rails; broker/insurer partners tap ~$25T US brokerage scale for product shelves and revenue‑share (10–40%).

| Partner | 2024/2023 Metric | Impact |

|---|---|---|

| Correspondent banks | SWIFT ~40M msgs/day (2024) | Clearing, liquidity |

| Fintech/core vendors | ~30% faster rollouts (2024) | Speed, lower cost |

| Card networks | Visa 3.9B / MC 2.8B (2023) | Interchange, acceptance |

| Broker/insurer | US brokerage ~$25T (2024) | Product expansion, rev‑share |

What is included in the product

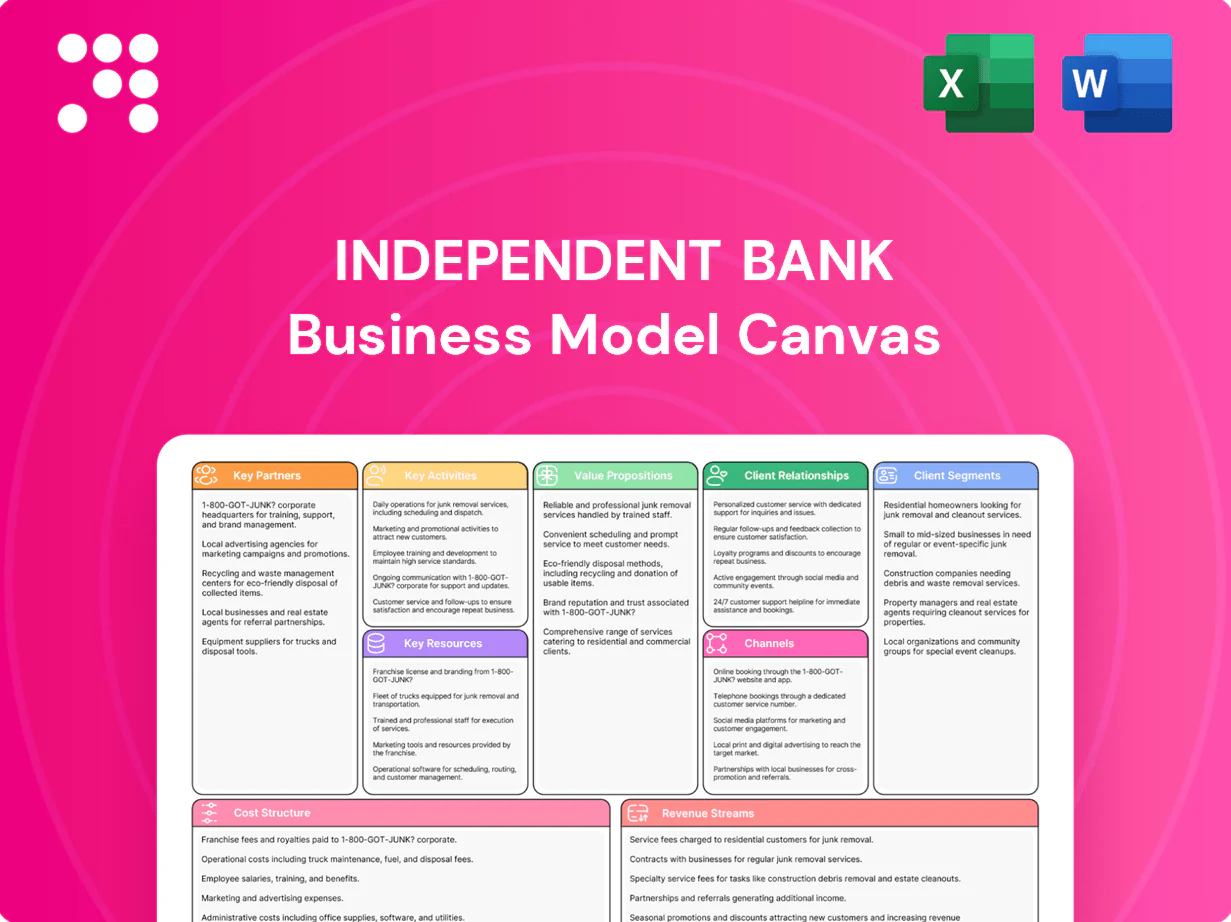

A ready-to-use Business Model Canvas for an Independent Bank outlining customer segments, channels, value propositions, revenue streams, key activities and partners, with competitive analysis, risks, and strategic insights for presentations and funding discussions.

High-level view of an independent bank’s business model with editable cells to quickly map revenue streams, risks, and customer segments. Great for boardrooms or teams—shareable, concise, and saves hours of structuring strategic analysis for faster decision-making.

Activities

Deposit gathering

Deposit gathering secures low-cost funding for lending and liquidity, supporting banks amid roughly $18 trillion in U.S. deposits in 2024. Activities include product design, pricing ladders, and targeted campaign segmentation to optimize deposit mix and duration. Relationship management and service quality reduce churn, while digital onboarding and automated KYC cut account opening time and acquisition costs.

Credit underwriting

Rigorous credit underwriting assesses risk across consumer, mortgage and commercial loans, reflecting stressed-rate dynamics with the US prime at 8.50% and industry net interest margin ~3.2% in 2024. Processes include detailed financial analysis, collateral valuation and scenario stress testing to quantify losses. Strong credit policy governance and limits kept noncurrent loan rates near 0.9% in 2024. Continuous monitoring enables early detection and remediation of emerging credit issues.

Wealth and insurance advice

Advisors deliver planning, investment management, and insurance solutions through client discovery, portfolio construction, and policy placement, supporting clients across retail and high-net-worth segments. Compliance and fiduciary oversight—aligned with SEC and state rules—ensure suitability and recordkeeping. Continuous reviews realign strategies to life events and markets; global wealth reached about 470 trillion USD in 2024.

Digital experience delivery

Maintaining secure, intuitive web and mobile banking is essential; in 2024 roughly 82% of US consumers used mobile banking, driving prioritization of UX, releases, cybersecurity, and 99.95% uptime SLAs. Teams deploy data-driven A/B testing and analytics to boost adoption and cross-sell, while API-led architectures cut partner integration times and speed innovation.

- 82% mobile banking adoption (2024)

- 99.95% uptime target

- Data-driven A/B testing for cross-sell

- API integrations for faster partner connectivity

Regulatory compliance

Regulatory compliance in banking covers BSA/AML, CRA, privacy, and safety-and-soundness through continuous monitoring, mandatory reporting, staff training, and regular audits to limit legal and operational risk.

Model risk management and governance frameworks cut exposure to losses and control failures; large-bank stress testing (CCAR) covered 23 firms in 2024, underscoring supervisory rigor.

Proactive regulator engagement preserves licenses while handling over 1.5 million SAR filings annually reported to FinCEN, driving resourcing and tech investments.

- Monitoring, reporting, audits

- Training, policy updates

- Model risk governance

- Regulator engagement, license upkeep

Deposit-led funding: US deposits $18T, NIM 3.2%, mobile 82%

Deposit gathering secures low-cost funding (US deposits ~$18T in 2024) and optimizes mix; NIM ~3.2% and prime 8.50%. Rigorous underwriting limits noncurrent loans (~0.9%) via stress testing and governance. Digital channels (82% mobile adoption) and 99.95% uptime enable acquisition and cross-sell. Compliance and SAR reporting (~1.5M filings) plus CCAR (23 firms) sustain licenses.

| Metric | 2024 |

|---|---|

| US deposits | $18T |

| NIM | ~3.2% |

| Prime rate | 8.50% |

| Mobile adoption | 82% |

| Noncurrent loans | 0.9% |

| SAR filings | 1.5M |

Preview Before You Purchase

Business Model Canvas

The Independent Bank Business Model Canvas previewed here is the exact document you'll receive after purchase. It's not a mockup or sample but the full deliverable structured and formatted as shown. Upon order you'll get the same ready-to-edit file in Word and Excel, with all content included—no surprises.

Business Model Canvas: Regional bank strategy, revenue and growth playbook for investors

Unlock the full strategic blueprint behind Independent Bank’s business model in a concise, actionable format that spotlights value propositions, revenue streams, and competitive levers. This in-depth Business Model Canvas reveals how the bank acquires customers, manages risk, and scales profitably. Ideal for investors, advisors, and executives seeking a ready-to-use tool—download the complete canvas to benchmark, plan, and capitalize on opportunities.

Partnerships

Correspondent banks

Partnering with larger correspondent banks expands payment clearing, foreign exchange, and liquidity access, tapping global rails that in 2024 routed roughly 40 million SWIFT messages per day. These relationships enable wire processing, check clearing, and interbank settlements at scale, lowering per-transaction friction and cost. They enhance service reliability for clients and provide contingency liquidity and settlement support during stressed market conditions.

Fintech and core providers

Alliances with core banking, digital banking, and fintech vendors power online and mobile capabilities and enabled many banks to cut feature rollout times by roughly 30%, according to industry benchmarks in 2024. These partners accelerate security upgrades and data integrations while joint roadmaps keep customer experiences modern and competitive. Outsourcing lowers build costs versus fully in‑house development, often reducing upfront spend by double‑digit percentages.

Payment networks

Membership in card and payment networks (Visa ~3.9 billion cards 2023, Mastercard ~2.8 billion cards) enables debit issuance and merchant services, expanding customer access and interchange income. Network partnerships provide ATM interoperability and support real-time rails to speed settlements and reduce float. They drive interchange revenue opportunities and broader acceptance, while compliance and network branding bolster trust and usage.

Broker-dealers and insurers

Strategic ties with broker-dealers and insurance carriers expand Independent Bank's wealth and insurance offerings, leveraging 2024 U.S. brokerage assets exceeding $25 trillion to access scale. Partners supply product shelves, underwriting and advisory tools, enabling co-branded solutions that deepen wallet share among retail and business clients. Revenue-sharing arrangements, often in the 10-40% range depending on product, align incentives around client outcomes.

- Product shelves & underwriting

- Advisory tools & distribution

- Co-branded wallet-share gains

- Revenue-share aligns incentives

Community and civic groups

Local nonprofits, chambers, and municipalities anchor community engagement, and in 2024 partnerships expanded outreach to support financial literacy, small-business growth, and CRA initiatives. These collaborations build brand goodwill and drive grassroots acquisition through events, workshops, and referral networks. Insights from civic groups directly inform localized product features and branch placement strategies.

- Local nonprofits

- Chambers of commerce

- Municipal partnerships

- Financial literacy programs

- Small-business support

- CRA alignment

Ecosystem: 40M SWIFT msgs, 30% faster rollouts, 3.9B/2.8B cards, $25T

Independent Bank leverages correspondent banks (SWIFT ~40M msgs/day in 2024) for clearing, FX and contingency liquidity; fintech/core vendors cut feature rollout ~30% in 2024 and lower build costs; card networks (Visa 3.9B, Mastercard 2.8B cards) drive interchange and real‑time rails; broker/insurer partners tap ~$25T US brokerage scale for product shelves and revenue‑share (10–40%).

| Partner | 2024/2023 Metric | Impact |

|---|---|---|

| Correspondent banks | SWIFT ~40M msgs/day (2024) | Clearing, liquidity |

| Fintech/core vendors | ~30% faster rollouts (2024) | Speed, lower cost |

| Card networks | Visa 3.9B / MC 2.8B (2023) | Interchange, acceptance |

| Broker/insurer | US brokerage ~$25T (2024) | Product expansion, rev‑share |

What is included in the product

A ready-to-use Business Model Canvas for an Independent Bank outlining customer segments, channels, value propositions, revenue streams, key activities and partners, with competitive analysis, risks, and strategic insights for presentations and funding discussions.

High-level view of an independent bank’s business model with editable cells to quickly map revenue streams, risks, and customer segments. Great for boardrooms or teams—shareable, concise, and saves hours of structuring strategic analysis for faster decision-making.

Activities

Deposit gathering

Deposit gathering secures low-cost funding for lending and liquidity, supporting banks amid roughly $18 trillion in U.S. deposits in 2024. Activities include product design, pricing ladders, and targeted campaign segmentation to optimize deposit mix and duration. Relationship management and service quality reduce churn, while digital onboarding and automated KYC cut account opening time and acquisition costs.

Credit underwriting

Rigorous credit underwriting assesses risk across consumer, mortgage and commercial loans, reflecting stressed-rate dynamics with the US prime at 8.50% and industry net interest margin ~3.2% in 2024. Processes include detailed financial analysis, collateral valuation and scenario stress testing to quantify losses. Strong credit policy governance and limits kept noncurrent loan rates near 0.9% in 2024. Continuous monitoring enables early detection and remediation of emerging credit issues.

Wealth and insurance advice

Advisors deliver planning, investment management, and insurance solutions through client discovery, portfolio construction, and policy placement, supporting clients across retail and high-net-worth segments. Compliance and fiduciary oversight—aligned with SEC and state rules—ensure suitability and recordkeeping. Continuous reviews realign strategies to life events and markets; global wealth reached about 470 trillion USD in 2024.

Digital experience delivery

Maintaining secure, intuitive web and mobile banking is essential; in 2024 roughly 82% of US consumers used mobile banking, driving prioritization of UX, releases, cybersecurity, and 99.95% uptime SLAs. Teams deploy data-driven A/B testing and analytics to boost adoption and cross-sell, while API-led architectures cut partner integration times and speed innovation.

- 82% mobile banking adoption (2024)

- 99.95% uptime target

- Data-driven A/B testing for cross-sell

- API integrations for faster partner connectivity

Regulatory compliance

Regulatory compliance in banking covers BSA/AML, CRA, privacy, and safety-and-soundness through continuous monitoring, mandatory reporting, staff training, and regular audits to limit legal and operational risk.

Model risk management and governance frameworks cut exposure to losses and control failures; large-bank stress testing (CCAR) covered 23 firms in 2024, underscoring supervisory rigor.

Proactive regulator engagement preserves licenses while handling over 1.5 million SAR filings annually reported to FinCEN, driving resourcing and tech investments.

- Monitoring, reporting, audits

- Training, policy updates

- Model risk governance

- Regulator engagement, license upkeep

Deposit-led funding: US deposits $18T, NIM 3.2%, mobile 82%

Deposit gathering secures low-cost funding (US deposits ~$18T in 2024) and optimizes mix; NIM ~3.2% and prime 8.50%. Rigorous underwriting limits noncurrent loans (~0.9%) via stress testing and governance. Digital channels (82% mobile adoption) and 99.95% uptime enable acquisition and cross-sell. Compliance and SAR reporting (~1.5M filings) plus CCAR (23 firms) sustain licenses.

| Metric | 2024 |

|---|---|

| US deposits | $18T |

| NIM | ~3.2% |

| Prime rate | 8.50% |

| Mobile adoption | 82% |

| Noncurrent loans | 0.9% |

| SAR filings | 1.5M |

Preview Before You Purchase

Business Model Canvas

The Independent Bank Business Model Canvas previewed here is the exact document you'll receive after purchase. It's not a mockup or sample but the full deliverable structured and formatted as shown. Upon order you'll get the same ready-to-edit file in Word and Excel, with all content included—no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas: Regional bank strategy, revenue and growth playbook for investors

Unlock the full strategic blueprint behind Independent Bank’s business model in a concise, actionable format that spotlights value propositions, revenue streams, and competitive levers. This in-depth Business Model Canvas reveals how the bank acquires customers, manages risk, and scales profitably. Ideal for investors, advisors, and executives seeking a ready-to-use tool—download the complete canvas to benchmark, plan, and capitalize on opportunities.

Partnerships

Correspondent banks

Partnering with larger correspondent banks expands payment clearing, foreign exchange, and liquidity access, tapping global rails that in 2024 routed roughly 40 million SWIFT messages per day. These relationships enable wire processing, check clearing, and interbank settlements at scale, lowering per-transaction friction and cost. They enhance service reliability for clients and provide contingency liquidity and settlement support during stressed market conditions.

Fintech and core providers

Alliances with core banking, digital banking, and fintech vendors power online and mobile capabilities and enabled many banks to cut feature rollout times by roughly 30%, according to industry benchmarks in 2024. These partners accelerate security upgrades and data integrations while joint roadmaps keep customer experiences modern and competitive. Outsourcing lowers build costs versus fully in‑house development, often reducing upfront spend by double‑digit percentages.

Payment networks

Membership in card and payment networks (Visa ~3.9 billion cards 2023, Mastercard ~2.8 billion cards) enables debit issuance and merchant services, expanding customer access and interchange income. Network partnerships provide ATM interoperability and support real-time rails to speed settlements and reduce float. They drive interchange revenue opportunities and broader acceptance, while compliance and network branding bolster trust and usage.

Broker-dealers and insurers

Strategic ties with broker-dealers and insurance carriers expand Independent Bank's wealth and insurance offerings, leveraging 2024 U.S. brokerage assets exceeding $25 trillion to access scale. Partners supply product shelves, underwriting and advisory tools, enabling co-branded solutions that deepen wallet share among retail and business clients. Revenue-sharing arrangements, often in the 10-40% range depending on product, align incentives around client outcomes.

- Product shelves & underwriting

- Advisory tools & distribution

- Co-branded wallet-share gains

- Revenue-share aligns incentives

Community and civic groups

Local nonprofits, chambers, and municipalities anchor community engagement, and in 2024 partnerships expanded outreach to support financial literacy, small-business growth, and CRA initiatives. These collaborations build brand goodwill and drive grassroots acquisition through events, workshops, and referral networks. Insights from civic groups directly inform localized product features and branch placement strategies.

- Local nonprofits

- Chambers of commerce

- Municipal partnerships

- Financial literacy programs

- Small-business support

- CRA alignment

Ecosystem: 40M SWIFT msgs, 30% faster rollouts, 3.9B/2.8B cards, $25T

Independent Bank leverages correspondent banks (SWIFT ~40M msgs/day in 2024) for clearing, FX and contingency liquidity; fintech/core vendors cut feature rollout ~30% in 2024 and lower build costs; card networks (Visa 3.9B, Mastercard 2.8B cards) drive interchange and real‑time rails; broker/insurer partners tap ~$25T US brokerage scale for product shelves and revenue‑share (10–40%).

| Partner | 2024/2023 Metric | Impact |

|---|---|---|

| Correspondent banks | SWIFT ~40M msgs/day (2024) | Clearing, liquidity |

| Fintech/core vendors | ~30% faster rollouts (2024) | Speed, lower cost |

| Card networks | Visa 3.9B / MC 2.8B (2023) | Interchange, acceptance |

| Broker/insurer | US brokerage ~$25T (2024) | Product expansion, rev‑share |

What is included in the product

A ready-to-use Business Model Canvas for an Independent Bank outlining customer segments, channels, value propositions, revenue streams, key activities and partners, with competitive analysis, risks, and strategic insights for presentations and funding discussions.

High-level view of an independent bank’s business model with editable cells to quickly map revenue streams, risks, and customer segments. Great for boardrooms or teams—shareable, concise, and saves hours of structuring strategic analysis for faster decision-making.

Activities

Deposit gathering

Deposit gathering secures low-cost funding for lending and liquidity, supporting banks amid roughly $18 trillion in U.S. deposits in 2024. Activities include product design, pricing ladders, and targeted campaign segmentation to optimize deposit mix and duration. Relationship management and service quality reduce churn, while digital onboarding and automated KYC cut account opening time and acquisition costs.

Credit underwriting

Rigorous credit underwriting assesses risk across consumer, mortgage and commercial loans, reflecting stressed-rate dynamics with the US prime at 8.50% and industry net interest margin ~3.2% in 2024. Processes include detailed financial analysis, collateral valuation and scenario stress testing to quantify losses. Strong credit policy governance and limits kept noncurrent loan rates near 0.9% in 2024. Continuous monitoring enables early detection and remediation of emerging credit issues.

Wealth and insurance advice

Advisors deliver planning, investment management, and insurance solutions through client discovery, portfolio construction, and policy placement, supporting clients across retail and high-net-worth segments. Compliance and fiduciary oversight—aligned with SEC and state rules—ensure suitability and recordkeeping. Continuous reviews realign strategies to life events and markets; global wealth reached about 470 trillion USD in 2024.

Digital experience delivery

Maintaining secure, intuitive web and mobile banking is essential; in 2024 roughly 82% of US consumers used mobile banking, driving prioritization of UX, releases, cybersecurity, and 99.95% uptime SLAs. Teams deploy data-driven A/B testing and analytics to boost adoption and cross-sell, while API-led architectures cut partner integration times and speed innovation.

- 82% mobile banking adoption (2024)

- 99.95% uptime target

- Data-driven A/B testing for cross-sell

- API integrations for faster partner connectivity

Regulatory compliance

Regulatory compliance in banking covers BSA/AML, CRA, privacy, and safety-and-soundness through continuous monitoring, mandatory reporting, staff training, and regular audits to limit legal and operational risk.

Model risk management and governance frameworks cut exposure to losses and control failures; large-bank stress testing (CCAR) covered 23 firms in 2024, underscoring supervisory rigor.

Proactive regulator engagement preserves licenses while handling over 1.5 million SAR filings annually reported to FinCEN, driving resourcing and tech investments.

- Monitoring, reporting, audits

- Training, policy updates

- Model risk governance

- Regulator engagement, license upkeep

Deposit-led funding: US deposits $18T, NIM 3.2%, mobile 82%

Deposit gathering secures low-cost funding (US deposits ~$18T in 2024) and optimizes mix; NIM ~3.2% and prime 8.50%. Rigorous underwriting limits noncurrent loans (~0.9%) via stress testing and governance. Digital channels (82% mobile adoption) and 99.95% uptime enable acquisition and cross-sell. Compliance and SAR reporting (~1.5M filings) plus CCAR (23 firms) sustain licenses.

| Metric | 2024 |

|---|---|

| US deposits | $18T |

| NIM | ~3.2% |

| Prime rate | 8.50% |

| Mobile adoption | 82% |

| Noncurrent loans | 0.9% |

| SAR filings | 1.5M |

Preview Before You Purchase

Business Model Canvas

The Independent Bank Business Model Canvas previewed here is the exact document you'll receive after purchase. It's not a mockup or sample but the full deliverable structured and formatted as shown. Upon order you'll get the same ready-to-edit file in Word and Excel, with all content included—no surprises.