Rogers Communications Boston Consulting Group Matrix

See the Bigger Picture

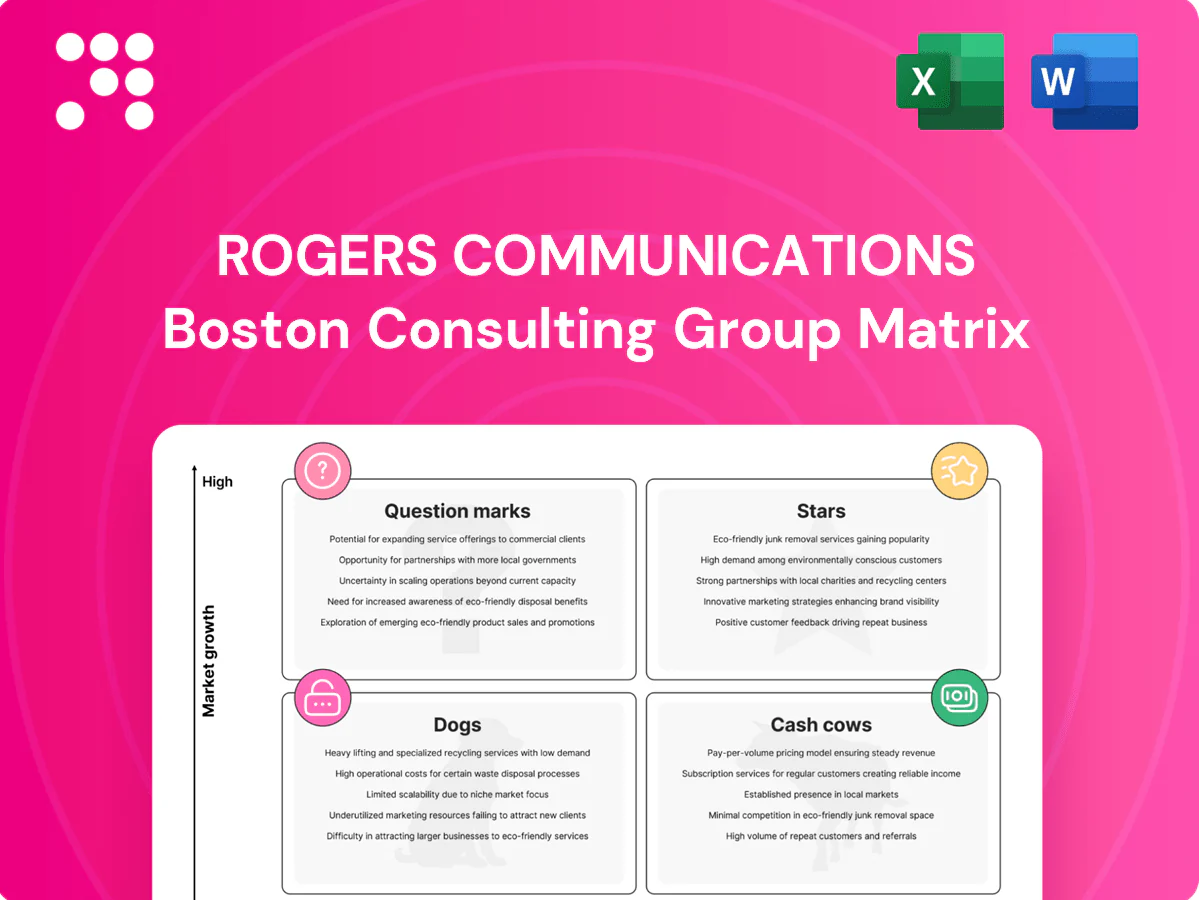

Rogers Communications’ BCG Matrix snapshot shows which services are driving growth and which are bleeding cash — think wireless and media carving out Stars while legacy lines wobble as Question Marks. You’ll get a quick sense of market share versus growth, and where leadership should double down or divest. This preview is useful, but the full BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-use strategy playbook. Purchase the complete report for Word and Excel deliverables and act with confidence.

Stars

5G wireless leadership

Rogers’ postpaid 5G base grew double-digit year-over-year in 2024, supported by network investments that keep it in the top tier of Canadian carriers. The company continues heavy capex — roughly CAD 1.2 billion quarterly in 2024 — yet this investment drives leadership and premium ARPU near CAD 66. High market share meets expanding data usage each quarter, so keep feeding it: this is the engine.

Converged bundles (mobile + Ignite)

Bundling wireless with Ignite locks households and lifts lifetime value by lowering churn and increasing cross‑sell; Rogers, as part of Canada’s Big Three that account for roughly 90% of wireless market share, uses aggressive promos to nudge uptake. Churn drops and market share inches up with each smart promotion; growth remains healthy as more Canadians take the all‑in deal. It’s promotional‑heavy now, but positions bundles to become tomorrow’s cash cows.

Sportsnet digital (DTC)

Live sports streaming via Sportsnet digital (DTC) is gaining subscribers and attention as linear ratings soften, leveraging a strong brand and a content flywheel that drives high engagement. Rights remain costly—Rogers’ landmark 12-year NHL rights commitment of C$5.232 billion underscores cash-in equals cash-out today. If scale holds while growth moderates, Sportsnet DTC can flip into a cash cow.

Enterprise mobility & IoT

Large enterprise accounts rely on Rogers for secure mobility, unified device management and connected assets; the IoT stack is moving beyond connectivity into managed solutions as global IoT connections reached about 14.4 billion in 2024 (Statista). Rogers maintains a solid share in a category growing double digits, warranting continued investment in platforms and vertical plays.

- Focus: secure mobility & device mgmt

- Trend: connectivity → solutions

- Data: ~14.4B IoT connections (2024)

- Action: invest in platforms + verticals

Wholesale roaming and network partnerships

Inflow from roaming and selective wholesale deals is rising alongside 5G traffic and travel recovery, with UNWTO reporting international arrivals at about 88% of 2019 levels in 2023.

It benefits from Rogers’ footprint and quality perception—Rogers states its 5G network reaches roughly 97% of Canadians—supporting attractive wholesale demand.

Margins are strong today and scale from higher 5G usage and device upgrades can compound returns.

- Roaming growth: travel ~88% of 2019 (UNWTO)

- Coverage: Rogers 5G ~97% population

- Outcome: good margins, scalable 5G tailwinds

5G postpaid up double-digit; ARPU CAD66, capex ~CAD1.2B

Rogers’ 5G postpaid grew double‑digit YoY in 2024, supporting premium ARPU ~CAD66 and quarterly capex ≈CAD1.2B. Bundles cut churn and boost LTV; Sportsnet DTC scales while NHL rights cost C$5.232B (12yr). Enterprise IoT and wholesale 5G (coverage ~97%) drive margin upside.

| Metric | 2024 | Note |

|---|---|---|

| ARPU | CAD66 | wireless premium |

| Capex/qtr | CAD1.2B | network build |

| 5G coverage | 97% | population |

| NHL rights | C$5.232B | 12yr |

What is included in the product

Clear BCG breakdown of Rogers’ units: Stars to invest, Cash Cows to milk, Question Marks to prioritize, Dogs to divest, trend context.

One-page BCG matrix placing Rogers business units into quadrants to pinpoint growth, cash cows and problem areas for fast decisions

Cash Cows

Residential internet (Ignite)

Residential internet (Ignite) is a mature, high‑penetration cash cow for Rogers, reporting over 3 million residential high‑speed internet subscribers in 2024 and delivering steady ARPU while generating strong free cash flow.

Upgrades to higher tiers add incremental margin without massive capital spend, churn remains manageable—particularly in bundles—and management can milk cash flows while tightening cost‑to‑serve.

Legacy wireless base (voice/SMS)

Rogers legacy wireless voice/SMS remains a cash cow: the non‑data segment is flat but reliable, serving over 10 million subscribers and accounting for roughly half of wireless revenue in 2024. Low incremental investment and predictable cash flow sustain margins; upsell paths to data and bundled services exist yet even without them it covers fixed costs. Priorities: maintain service quality and automate support to preserve churn and margin.

Linear carriage fees (Sportsnet/TV)

Linear carriage fees from Sportsnet and TV continue to deliver steady cash flow for Rogers, with the company reporting consolidated revenue of CAD 15.3 billion in fiscal 2024, helping offset audience shifts to streaming.

As a mature, negotiated revenue line, carriage provides predictable margin and requires far less promotion compared with digital channels.

Rogers uses these proceeds to fund higher-growth digital and streaming bets while maintaining balance-sheet stability.

Business wireline (internet & VPN)

Corporate connectivity (internet & VPN) is a stickier, contract-driven cash cow for Rogers—enterprise contracts typically span 3–5 years; growth ran low single-digits in 2024 while EBITDA margins remained above company average due to efficient delivery and scale.

- Hold base: preserve high retention enterprise book

- Cross-sell: upsell SD-WAN/security where low cost

- Capex: upgrades incremental, not transformative

Home phone (bundled)

Home phone units continue to decline but remain a reliable cash generator inside Rogers bundles; Rogers’ 2024 investor materials confirm focus shifts toward wireless/broadband while retaining legacy voice for revenue stability.

Marketing and innovation spend is minimal, margins stay dependable and cost-to-serve has fallen as OSS/BSS modernizations progressed through 2024.

Harvest carefully to squeeze cash without disrupting bundle churn or accelerating defections.

- Declining units, steady bundle cash

- Minimal marketing & innovation

- Dependable margin, lower cost-to-serve (2024 modernizations)

- Harvest strategy to avoid bundle churn

Ignite growth, durable cashflows: >3M subs, >10M wireless, CAD 15.3B

Residential Ignite: >3M subs (2024), steady ARPU, strong FCF.

Legacy wireless voice/SMS: >10M subs, ~50% of wireless revenue (2024), low incremental capex.

Carriage & enterprise: CAD 15.3B consolidated rev (2024); enterprise low‑single‑digit growth, EBITDA > company average.

| Line | 2024 |

|---|---|

| Ignite subs | >3M |

| Wireless voice | >10M / ~50% rev |

| Revenue | CAD 15.3B |

Full Transparency, Always

Rogers Communications BCG Matrix

The file you're previewing is the final Rogers Communications BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report tailored to Rogers' portfolio. It arrives exactly as shown, ready for editing, printing, or pitching to stakeholders. Buy once, download instantly, and use it in your strategic planning with confidence.

See the Bigger Picture

Rogers Communications’ BCG Matrix snapshot shows which services are driving growth and which are bleeding cash — think wireless and media carving out Stars while legacy lines wobble as Question Marks. You’ll get a quick sense of market share versus growth, and where leadership should double down or divest. This preview is useful, but the full BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-use strategy playbook. Purchase the complete report for Word and Excel deliverables and act with confidence.

Stars

5G wireless leadership

Rogers’ postpaid 5G base grew double-digit year-over-year in 2024, supported by network investments that keep it in the top tier of Canadian carriers. The company continues heavy capex — roughly CAD 1.2 billion quarterly in 2024 — yet this investment drives leadership and premium ARPU near CAD 66. High market share meets expanding data usage each quarter, so keep feeding it: this is the engine.

Converged bundles (mobile + Ignite)

Bundling wireless with Ignite locks households and lifts lifetime value by lowering churn and increasing cross‑sell; Rogers, as part of Canada’s Big Three that account for roughly 90% of wireless market share, uses aggressive promos to nudge uptake. Churn drops and market share inches up with each smart promotion; growth remains healthy as more Canadians take the all‑in deal. It’s promotional‑heavy now, but positions bundles to become tomorrow’s cash cows.

Sportsnet digital (DTC)

Live sports streaming via Sportsnet digital (DTC) is gaining subscribers and attention as linear ratings soften, leveraging a strong brand and a content flywheel that drives high engagement. Rights remain costly—Rogers’ landmark 12-year NHL rights commitment of C$5.232 billion underscores cash-in equals cash-out today. If scale holds while growth moderates, Sportsnet DTC can flip into a cash cow.

Enterprise mobility & IoT

Large enterprise accounts rely on Rogers for secure mobility, unified device management and connected assets; the IoT stack is moving beyond connectivity into managed solutions as global IoT connections reached about 14.4 billion in 2024 (Statista). Rogers maintains a solid share in a category growing double digits, warranting continued investment in platforms and vertical plays.

- Focus: secure mobility & device mgmt

- Trend: connectivity → solutions

- Data: ~14.4B IoT connections (2024)

- Action: invest in platforms + verticals

Wholesale roaming and network partnerships

Inflow from roaming and selective wholesale deals is rising alongside 5G traffic and travel recovery, with UNWTO reporting international arrivals at about 88% of 2019 levels in 2023.

It benefits from Rogers’ footprint and quality perception—Rogers states its 5G network reaches roughly 97% of Canadians—supporting attractive wholesale demand.

Margins are strong today and scale from higher 5G usage and device upgrades can compound returns.

- Roaming growth: travel ~88% of 2019 (UNWTO)

- Coverage: Rogers 5G ~97% population

- Outcome: good margins, scalable 5G tailwinds

5G postpaid up double-digit; ARPU CAD66, capex ~CAD1.2B

Rogers’ 5G postpaid grew double‑digit YoY in 2024, supporting premium ARPU ~CAD66 and quarterly capex ≈CAD1.2B. Bundles cut churn and boost LTV; Sportsnet DTC scales while NHL rights cost C$5.232B (12yr). Enterprise IoT and wholesale 5G (coverage ~97%) drive margin upside.

| Metric | 2024 | Note |

|---|---|---|

| ARPU | CAD66 | wireless premium |

| Capex/qtr | CAD1.2B | network build |

| 5G coverage | 97% | population |

| NHL rights | C$5.232B | 12yr |

What is included in the product

Clear BCG breakdown of Rogers’ units: Stars to invest, Cash Cows to milk, Question Marks to prioritize, Dogs to divest, trend context.

One-page BCG matrix placing Rogers business units into quadrants to pinpoint growth, cash cows and problem areas for fast decisions

Cash Cows

Residential internet (Ignite)

Residential internet (Ignite) is a mature, high‑penetration cash cow for Rogers, reporting over 3 million residential high‑speed internet subscribers in 2024 and delivering steady ARPU while generating strong free cash flow.

Upgrades to higher tiers add incremental margin without massive capital spend, churn remains manageable—particularly in bundles—and management can milk cash flows while tightening cost‑to‑serve.

Legacy wireless base (voice/SMS)

Rogers legacy wireless voice/SMS remains a cash cow: the non‑data segment is flat but reliable, serving over 10 million subscribers and accounting for roughly half of wireless revenue in 2024. Low incremental investment and predictable cash flow sustain margins; upsell paths to data and bundled services exist yet even without them it covers fixed costs. Priorities: maintain service quality and automate support to preserve churn and margin.

Linear carriage fees (Sportsnet/TV)

Linear carriage fees from Sportsnet and TV continue to deliver steady cash flow for Rogers, with the company reporting consolidated revenue of CAD 15.3 billion in fiscal 2024, helping offset audience shifts to streaming.

As a mature, negotiated revenue line, carriage provides predictable margin and requires far less promotion compared with digital channels.

Rogers uses these proceeds to fund higher-growth digital and streaming bets while maintaining balance-sheet stability.

Business wireline (internet & VPN)

Corporate connectivity (internet & VPN) is a stickier, contract-driven cash cow for Rogers—enterprise contracts typically span 3–5 years; growth ran low single-digits in 2024 while EBITDA margins remained above company average due to efficient delivery and scale.

- Hold base: preserve high retention enterprise book

- Cross-sell: upsell SD-WAN/security where low cost

- Capex: upgrades incremental, not transformative

Home phone (bundled)

Home phone units continue to decline but remain a reliable cash generator inside Rogers bundles; Rogers’ 2024 investor materials confirm focus shifts toward wireless/broadband while retaining legacy voice for revenue stability.

Marketing and innovation spend is minimal, margins stay dependable and cost-to-serve has fallen as OSS/BSS modernizations progressed through 2024.

Harvest carefully to squeeze cash without disrupting bundle churn or accelerating defections.

- Declining units, steady bundle cash

- Minimal marketing & innovation

- Dependable margin, lower cost-to-serve (2024 modernizations)

- Harvest strategy to avoid bundle churn

Ignite growth, durable cashflows: >3M subs, >10M wireless, CAD 15.3B

Residential Ignite: >3M subs (2024), steady ARPU, strong FCF.

Legacy wireless voice/SMS: >10M subs, ~50% of wireless revenue (2024), low incremental capex.

Carriage & enterprise: CAD 15.3B consolidated rev (2024); enterprise low‑single‑digit growth, EBITDA > company average.

| Line | 2024 |

|---|---|

| Ignite subs | >3M |

| Wireless voice | >10M / ~50% rev |

| Revenue | CAD 15.3B |

Full Transparency, Always

Rogers Communications BCG Matrix

The file you're previewing is the final Rogers Communications BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report tailored to Rogers' portfolio. It arrives exactly as shown, ready for editing, printing, or pitching to stakeholders. Buy once, download instantly, and use it in your strategic planning with confidence.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

Rogers Communications’ BCG Matrix snapshot shows which services are driving growth and which are bleeding cash — think wireless and media carving out Stars while legacy lines wobble as Question Marks. You’ll get a quick sense of market share versus growth, and where leadership should double down or divest. This preview is useful, but the full BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-use strategy playbook. Purchase the complete report for Word and Excel deliverables and act with confidence.

Stars

5G wireless leadership

Rogers’ postpaid 5G base grew double-digit year-over-year in 2024, supported by network investments that keep it in the top tier of Canadian carriers. The company continues heavy capex — roughly CAD 1.2 billion quarterly in 2024 — yet this investment drives leadership and premium ARPU near CAD 66. High market share meets expanding data usage each quarter, so keep feeding it: this is the engine.

Converged bundles (mobile + Ignite)

Bundling wireless with Ignite locks households and lifts lifetime value by lowering churn and increasing cross‑sell; Rogers, as part of Canada’s Big Three that account for roughly 90% of wireless market share, uses aggressive promos to nudge uptake. Churn drops and market share inches up with each smart promotion; growth remains healthy as more Canadians take the all‑in deal. It’s promotional‑heavy now, but positions bundles to become tomorrow’s cash cows.

Sportsnet digital (DTC)

Live sports streaming via Sportsnet digital (DTC) is gaining subscribers and attention as linear ratings soften, leveraging a strong brand and a content flywheel that drives high engagement. Rights remain costly—Rogers’ landmark 12-year NHL rights commitment of C$5.232 billion underscores cash-in equals cash-out today. If scale holds while growth moderates, Sportsnet DTC can flip into a cash cow.

Enterprise mobility & IoT

Large enterprise accounts rely on Rogers for secure mobility, unified device management and connected assets; the IoT stack is moving beyond connectivity into managed solutions as global IoT connections reached about 14.4 billion in 2024 (Statista). Rogers maintains a solid share in a category growing double digits, warranting continued investment in platforms and vertical plays.

- Focus: secure mobility & device mgmt

- Trend: connectivity → solutions

- Data: ~14.4B IoT connections (2024)

- Action: invest in platforms + verticals

Wholesale roaming and network partnerships

Inflow from roaming and selective wholesale deals is rising alongside 5G traffic and travel recovery, with UNWTO reporting international arrivals at about 88% of 2019 levels in 2023.

It benefits from Rogers’ footprint and quality perception—Rogers states its 5G network reaches roughly 97% of Canadians—supporting attractive wholesale demand.

Margins are strong today and scale from higher 5G usage and device upgrades can compound returns.

- Roaming growth: travel ~88% of 2019 (UNWTO)

- Coverage: Rogers 5G ~97% population

- Outcome: good margins, scalable 5G tailwinds

5G postpaid up double-digit; ARPU CAD66, capex ~CAD1.2B

Rogers’ 5G postpaid grew double‑digit YoY in 2024, supporting premium ARPU ~CAD66 and quarterly capex ≈CAD1.2B. Bundles cut churn and boost LTV; Sportsnet DTC scales while NHL rights cost C$5.232B (12yr). Enterprise IoT and wholesale 5G (coverage ~97%) drive margin upside.

| Metric | 2024 | Note |

|---|---|---|

| ARPU | CAD66 | wireless premium |

| Capex/qtr | CAD1.2B | network build |

| 5G coverage | 97% | population |

| NHL rights | C$5.232B | 12yr |

What is included in the product

Clear BCG breakdown of Rogers’ units: Stars to invest, Cash Cows to milk, Question Marks to prioritize, Dogs to divest, trend context.

One-page BCG matrix placing Rogers business units into quadrants to pinpoint growth, cash cows and problem areas for fast decisions

Cash Cows

Residential internet (Ignite)

Residential internet (Ignite) is a mature, high‑penetration cash cow for Rogers, reporting over 3 million residential high‑speed internet subscribers in 2024 and delivering steady ARPU while generating strong free cash flow.

Upgrades to higher tiers add incremental margin without massive capital spend, churn remains manageable—particularly in bundles—and management can milk cash flows while tightening cost‑to‑serve.

Legacy wireless base (voice/SMS)

Rogers legacy wireless voice/SMS remains a cash cow: the non‑data segment is flat but reliable, serving over 10 million subscribers and accounting for roughly half of wireless revenue in 2024. Low incremental investment and predictable cash flow sustain margins; upsell paths to data and bundled services exist yet even without them it covers fixed costs. Priorities: maintain service quality and automate support to preserve churn and margin.

Linear carriage fees (Sportsnet/TV)

Linear carriage fees from Sportsnet and TV continue to deliver steady cash flow for Rogers, with the company reporting consolidated revenue of CAD 15.3 billion in fiscal 2024, helping offset audience shifts to streaming.

As a mature, negotiated revenue line, carriage provides predictable margin and requires far less promotion compared with digital channels.

Rogers uses these proceeds to fund higher-growth digital and streaming bets while maintaining balance-sheet stability.

Business wireline (internet & VPN)

Corporate connectivity (internet & VPN) is a stickier, contract-driven cash cow for Rogers—enterprise contracts typically span 3–5 years; growth ran low single-digits in 2024 while EBITDA margins remained above company average due to efficient delivery and scale.

- Hold base: preserve high retention enterprise book

- Cross-sell: upsell SD-WAN/security where low cost

- Capex: upgrades incremental, not transformative

Home phone (bundled)

Home phone units continue to decline but remain a reliable cash generator inside Rogers bundles; Rogers’ 2024 investor materials confirm focus shifts toward wireless/broadband while retaining legacy voice for revenue stability.

Marketing and innovation spend is minimal, margins stay dependable and cost-to-serve has fallen as OSS/BSS modernizations progressed through 2024.

Harvest carefully to squeeze cash without disrupting bundle churn or accelerating defections.

- Declining units, steady bundle cash

- Minimal marketing & innovation

- Dependable margin, lower cost-to-serve (2024 modernizations)

- Harvest strategy to avoid bundle churn

Ignite growth, durable cashflows: >3M subs, >10M wireless, CAD 15.3B

Residential Ignite: >3M subs (2024), steady ARPU, strong FCF.

Legacy wireless voice/SMS: >10M subs, ~50% of wireless revenue (2024), low incremental capex.

Carriage & enterprise: CAD 15.3B consolidated rev (2024); enterprise low‑single‑digit growth, EBITDA > company average.

| Line | 2024 |

|---|---|

| Ignite subs | >3M |

| Wireless voice | >10M / ~50% rev |

| Revenue | CAD 15.3B |

Full Transparency, Always

Rogers Communications BCG Matrix

The file you're previewing is the final Rogers Communications BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report tailored to Rogers' portfolio. It arrives exactly as shown, ready for editing, printing, or pitching to stakeholders. Buy once, download instantly, and use it in your strategic planning with confidence.