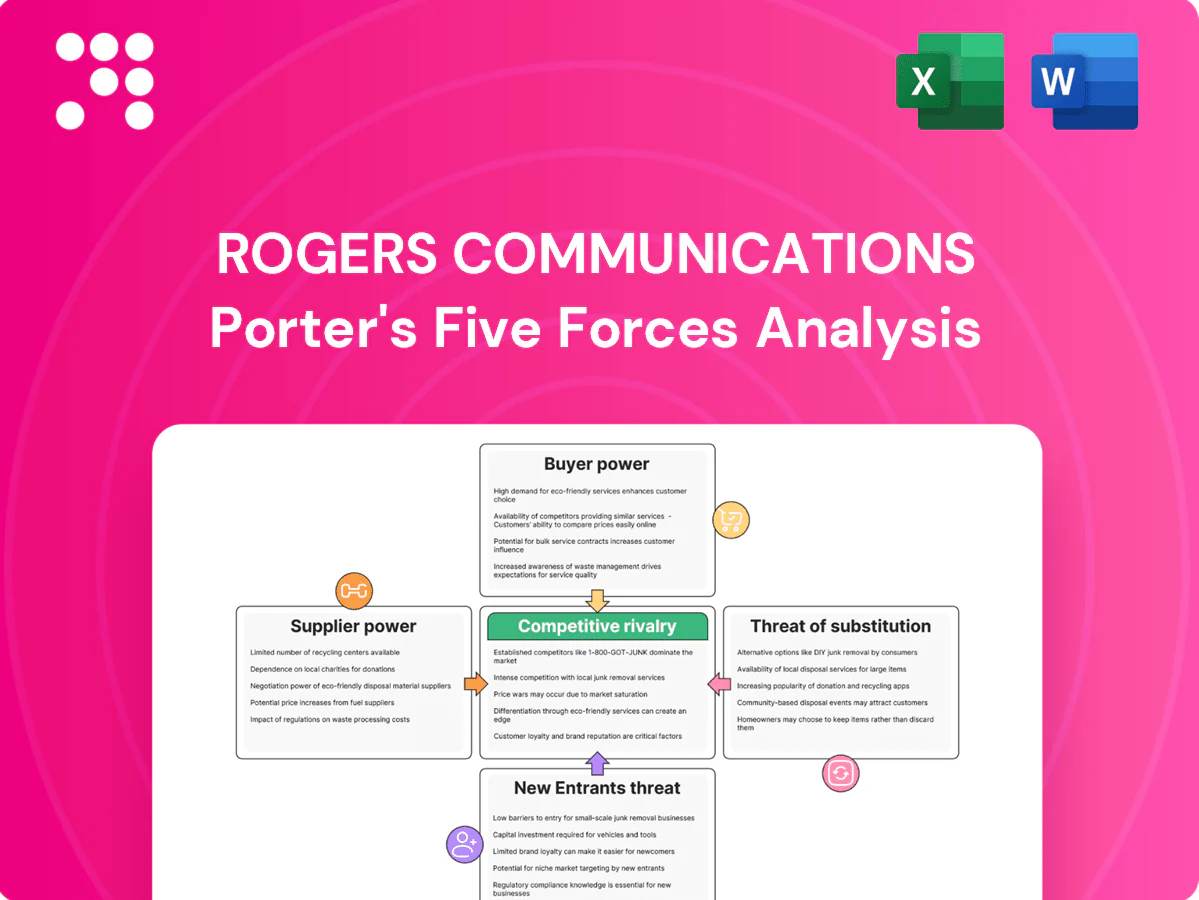

Rogers Communications Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Rogers Communications faces intense competitive rivalry, shifting buyer power, and rising substitute threats as streaming and MVNOs reshape telecom economics. Supplier leverage and regulatory scrutiny further compress margins and strategic options. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Rogers’s competitive dynamics and actionable implications in detail.

Suppliers Bargaining Power

5G gear duopoly

Rogers depends heavily on a narrow 5G RAN supplier base—primarily Ericsson and Nokia—concentrating bargaining power with vendors. Limited alternatives after Huawei restrictions and Dell'Oro data showing Ericsson and Nokia holding the majority of RAN revenue in 2024 reduce switching options and raise integration risk. Contract lock-ins and proprietary interfaces elevate switching costs, letting vendors influence pricing, upgrade cadence, and support terms.

Handset OEM dependence

Flagship Apple and Samsung devices remain must-carry, giving OEMs leverage on margins, marketing and subsidy structures; inventory allocation in launch windows can constrain Rogers’ sales despite Rogers’ ~10.3 million wireless subscribers (2024). Carrier scale and co-marketing budgets temper OEM power, while GSMA-reported eSIM growth (over 1 billion eSIM-capable devices by 2023) marginally shifts activation control toward OEMs.

Spectrum and rights holders

Government-controlled spectrum auctions and licence conditions act as a de facto supplier with strong pricing power over Rogers, determining capex timing and renewal costs. Content rights owners and studios extract significant fees for TV and streaming bundles; Rogers’ exposure to sports is partly hedged by its 37.5% stake in Maple Leaf Sports & Entertainment and its involvement in the landmark 12-year, CAD 5.2 billion NHL rights framework. Regulatory terms and renewal cycles materially influence Rogers’ cost structure and capital allocation.

Towers, fiber, and backhaul

Tower landlords, utility pole owners and fiber wholesalers extract rents where Rogers lacks owned infrastructure, and site access, make-ready work and municipal permits often add 6–18 months of delay and material incremental costs; long-term leases (typical 15–20 years) limit operational flexibility while securing coverage. Network sharing in rural areas can materially mitigate this supplier power.

- Lease terms: 15–20 years

- Permitting delays: 6–18 months

- Mitigation: rural network sharing agreements

Cloud and software platforms

Core IT, billing, and cloud partners exert strong supplier power at Rogers through long implementations and mission-critical integrations that embed vendors into operations; vendor roadmaps and licensing models directly influence ongoing opex. Multiyear contracts and data gravity create high switching costs, while hybrid-cloud strategies and growing in-house engineering capability lower reliance on any single vendor.

- Long implementations

- Vendor roadmaps → opex

- Multiyear contracts

- Data gravity = switching barrier

- Hybrid-cloud + in-house = less single-vendor risk

Supplier power: concentrated RAN vendors, long leases, carrier 10.3M subs

Supplier power is high: Ericsson and Nokia supply the bulk of 5G RAN (majority of 2024 RAN revenue), raising switching costs and pricing leverage. OEMs (Apple, Samsung) and content rights holders push margins; Rogers had ~10.3M wireless subs (2024). Tower/fiber landlords, long leases (15–20 years) and permitting delays (6–18 months) further strengthen suppliers.

| Supplier | Impact |

|---|---|

| RAN vendors | Majority 2024 RAN revenue |

| Leases/permits | 15–20y / 6–18m |

What is included in the product

Tailored Porter’s Five Forces analysis for Rogers Communications, uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive technologies and regulatory risks that shape profitability.

One-sheet Porter's Five Forces for Rogers Communications—quickly spot regulatory, competitive, and supplier pressures to relieve strategic blind spots and speed boardroom decisions.

Customers Bargaining Power

Consumer price sensitivity

Households routinely compare plans across the Big 3 and challengers, keeping Rogers ARPU under pressure during promotional periods; the Big 3 control roughly 90% of the Canadian wireless market, intensifying competition. Economic downturns deepen downgrades and cord-cutting, while transparent comparison sites raise buyer information and switching. Bundled discounts and device financing mitigate direct price cuts.

Enterprise and government

Enterprise and government customers extract strong leverage from custom SLAs and volume discounts, often driving multi-year RFP processes that intensify carrier competition. Switching costs exist but are managed around device refresh cycles and MDM platforms, reducing lock-in. Rogers’ focus on private 5G and IoT solutions in 2024 creates differentiation levers that can blunt pure price negotiations.

Switching costs and churn

Number portability and growing eSIM adoption (≈25% in Canada by 2024) lower friction and raise buyer power, while device financing balances (~CAD 1.6bn) plus bundle pricing and loyalty perks create exit barriers. Rogers manages churn (postpaid churn ≈0.95% in 2024) with retention offers that compress margins. Service quality and nationwide coverage remain primary stickiness drivers.

Bundling expectations

Customers now expect meaningful discounts across wireless, internet, TV and home phone, with Canadian bundle penetration >60% in 2024; failure to deliver perceived bundle value prompts switching or downgrades, pressuring margins. Deeper cross-sell increases household lifetime value—industry estimates show ~25% uplift in LTV for multi-product customers in 2024—but concentrates negotiation power per household. Media content packaging (exclusive sports/news) materially shifts perceived bundle value and retention.

- Bundle penetration: >60% (Canada, 2024)

- LTV uplift: ~25% for multi-product households (2024)

- Higher negotiation leverage per household due to cross-sell depth

- Content packaging drives perceived bundle value

Digital service alternatives

OTT apps enable users to replace voice/SMS and TV, shifting bargaining power to buyers as cord-cutting rises; Rogers still holds ≈30% Canadian wireless market share (2024) but faces content substitution pressure. Rivals' FWA and fiber offers let consumers renegotiate plans, while BYOD options reduce device lock-in. Enhanced CX and self-service tools can win back some leverage.

- OTT substitution — higher buyer leverage

- FWA/fiber availability — easier plan renegotiation

- BYOD — lowers switching costs

- Customer experience/self-service — restores provider control

Buyers hold leverage: Big 3 ≈90%, eSIM ≈25%

Customers wield elevated bargaining power: Big 3 control ≈90% of wireless but Rogers holds ≈30% (2024), eSIM adoption ≈25% and number portability lower switching friction, while device financing balances ≈CAD 1.6bn and postpaid churn ≈0.95% keep retention central; bundle penetration >60% and ~25% LTV uplift for multi-product households concentrate negotiation leverage.

| Metric | 2024 |

|---|---|

| Big 3 market share | ≈90% |

| Rogers wireless share | ≈30% |

| eSIM adoption | ≈25% |

| Device financing balance | ≈CAD 1.6bn |

| Postpaid churn | ≈0.95% |

| Bundle penetration | >60% |

| LTV uplift (multi-product) | ≈25% |

Preview Before You Purchase

Rogers Communications Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Rogers Communications Porter's Five Forces analysis evaluates intense competitive rivalry in Canadian telecoms, moderate buyer power offset by bundled services, limited supplier leverage for network equipment, manageable threat of substitutes, and high barriers to entry due to infrastructure and regulation. Use-ready and fully formatted.

Don't Miss the Bigger Picture

Rogers Communications faces intense competitive rivalry, shifting buyer power, and rising substitute threats as streaming and MVNOs reshape telecom economics. Supplier leverage and regulatory scrutiny further compress margins and strategic options. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Rogers’s competitive dynamics and actionable implications in detail.

Suppliers Bargaining Power

5G gear duopoly

Rogers depends heavily on a narrow 5G RAN supplier base—primarily Ericsson and Nokia—concentrating bargaining power with vendors. Limited alternatives after Huawei restrictions and Dell'Oro data showing Ericsson and Nokia holding the majority of RAN revenue in 2024 reduce switching options and raise integration risk. Contract lock-ins and proprietary interfaces elevate switching costs, letting vendors influence pricing, upgrade cadence, and support terms.

Handset OEM dependence

Flagship Apple and Samsung devices remain must-carry, giving OEMs leverage on margins, marketing and subsidy structures; inventory allocation in launch windows can constrain Rogers’ sales despite Rogers’ ~10.3 million wireless subscribers (2024). Carrier scale and co-marketing budgets temper OEM power, while GSMA-reported eSIM growth (over 1 billion eSIM-capable devices by 2023) marginally shifts activation control toward OEMs.

Spectrum and rights holders

Government-controlled spectrum auctions and licence conditions act as a de facto supplier with strong pricing power over Rogers, determining capex timing and renewal costs. Content rights owners and studios extract significant fees for TV and streaming bundles; Rogers’ exposure to sports is partly hedged by its 37.5% stake in Maple Leaf Sports & Entertainment and its involvement in the landmark 12-year, CAD 5.2 billion NHL rights framework. Regulatory terms and renewal cycles materially influence Rogers’ cost structure and capital allocation.

Towers, fiber, and backhaul

Tower landlords, utility pole owners and fiber wholesalers extract rents where Rogers lacks owned infrastructure, and site access, make-ready work and municipal permits often add 6–18 months of delay and material incremental costs; long-term leases (typical 15–20 years) limit operational flexibility while securing coverage. Network sharing in rural areas can materially mitigate this supplier power.

- Lease terms: 15–20 years

- Permitting delays: 6–18 months

- Mitigation: rural network sharing agreements

Cloud and software platforms

Core IT, billing, and cloud partners exert strong supplier power at Rogers through long implementations and mission-critical integrations that embed vendors into operations; vendor roadmaps and licensing models directly influence ongoing opex. Multiyear contracts and data gravity create high switching costs, while hybrid-cloud strategies and growing in-house engineering capability lower reliance on any single vendor.

- Long implementations

- Vendor roadmaps → opex

- Multiyear contracts

- Data gravity = switching barrier

- Hybrid-cloud + in-house = less single-vendor risk

Supplier power: concentrated RAN vendors, long leases, carrier 10.3M subs

Supplier power is high: Ericsson and Nokia supply the bulk of 5G RAN (majority of 2024 RAN revenue), raising switching costs and pricing leverage. OEMs (Apple, Samsung) and content rights holders push margins; Rogers had ~10.3M wireless subs (2024). Tower/fiber landlords, long leases (15–20 years) and permitting delays (6–18 months) further strengthen suppliers.

| Supplier | Impact |

|---|---|

| RAN vendors | Majority 2024 RAN revenue |

| Leases/permits | 15–20y / 6–18m |

What is included in the product

Tailored Porter’s Five Forces analysis for Rogers Communications, uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive technologies and regulatory risks that shape profitability.

One-sheet Porter's Five Forces for Rogers Communications—quickly spot regulatory, competitive, and supplier pressures to relieve strategic blind spots and speed boardroom decisions.

Customers Bargaining Power

Consumer price sensitivity

Households routinely compare plans across the Big 3 and challengers, keeping Rogers ARPU under pressure during promotional periods; the Big 3 control roughly 90% of the Canadian wireless market, intensifying competition. Economic downturns deepen downgrades and cord-cutting, while transparent comparison sites raise buyer information and switching. Bundled discounts and device financing mitigate direct price cuts.

Enterprise and government

Enterprise and government customers extract strong leverage from custom SLAs and volume discounts, often driving multi-year RFP processes that intensify carrier competition. Switching costs exist but are managed around device refresh cycles and MDM platforms, reducing lock-in. Rogers’ focus on private 5G and IoT solutions in 2024 creates differentiation levers that can blunt pure price negotiations.

Switching costs and churn

Number portability and growing eSIM adoption (≈25% in Canada by 2024) lower friction and raise buyer power, while device financing balances (~CAD 1.6bn) plus bundle pricing and loyalty perks create exit barriers. Rogers manages churn (postpaid churn ≈0.95% in 2024) with retention offers that compress margins. Service quality and nationwide coverage remain primary stickiness drivers.

Bundling expectations

Customers now expect meaningful discounts across wireless, internet, TV and home phone, with Canadian bundle penetration >60% in 2024; failure to deliver perceived bundle value prompts switching or downgrades, pressuring margins. Deeper cross-sell increases household lifetime value—industry estimates show ~25% uplift in LTV for multi-product customers in 2024—but concentrates negotiation power per household. Media content packaging (exclusive sports/news) materially shifts perceived bundle value and retention.

- Bundle penetration: >60% (Canada, 2024)

- LTV uplift: ~25% for multi-product households (2024)

- Higher negotiation leverage per household due to cross-sell depth

- Content packaging drives perceived bundle value

Digital service alternatives

OTT apps enable users to replace voice/SMS and TV, shifting bargaining power to buyers as cord-cutting rises; Rogers still holds ≈30% Canadian wireless market share (2024) but faces content substitution pressure. Rivals' FWA and fiber offers let consumers renegotiate plans, while BYOD options reduce device lock-in. Enhanced CX and self-service tools can win back some leverage.

- OTT substitution — higher buyer leverage

- FWA/fiber availability — easier plan renegotiation

- BYOD — lowers switching costs

- Customer experience/self-service — restores provider control

Buyers hold leverage: Big 3 ≈90%, eSIM ≈25%

Customers wield elevated bargaining power: Big 3 control ≈90% of wireless but Rogers holds ≈30% (2024), eSIM adoption ≈25% and number portability lower switching friction, while device financing balances ≈CAD 1.6bn and postpaid churn ≈0.95% keep retention central; bundle penetration >60% and ~25% LTV uplift for multi-product households concentrate negotiation leverage.

| Metric | 2024 |

|---|---|

| Big 3 market share | ≈90% |

| Rogers wireless share | ≈30% |

| eSIM adoption | ≈25% |

| Device financing balance | ≈CAD 1.6bn |

| Postpaid churn | ≈0.95% |

| Bundle penetration | >60% |

| LTV uplift (multi-product) | ≈25% |

Preview Before You Purchase

Rogers Communications Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Rogers Communications Porter's Five Forces analysis evaluates intense competitive rivalry in Canadian telecoms, moderate buyer power offset by bundled services, limited supplier leverage for network equipment, manageable threat of substitutes, and high barriers to entry due to infrastructure and regulation. Use-ready and fully formatted.

Description

Don't Miss the Bigger Picture

Rogers Communications faces intense competitive rivalry, shifting buyer power, and rising substitute threats as streaming and MVNOs reshape telecom economics. Supplier leverage and regulatory scrutiny further compress margins and strategic options. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Rogers’s competitive dynamics and actionable implications in detail.

Suppliers Bargaining Power

5G gear duopoly

Rogers depends heavily on a narrow 5G RAN supplier base—primarily Ericsson and Nokia—concentrating bargaining power with vendors. Limited alternatives after Huawei restrictions and Dell'Oro data showing Ericsson and Nokia holding the majority of RAN revenue in 2024 reduce switching options and raise integration risk. Contract lock-ins and proprietary interfaces elevate switching costs, letting vendors influence pricing, upgrade cadence, and support terms.

Handset OEM dependence

Flagship Apple and Samsung devices remain must-carry, giving OEMs leverage on margins, marketing and subsidy structures; inventory allocation in launch windows can constrain Rogers’ sales despite Rogers’ ~10.3 million wireless subscribers (2024). Carrier scale and co-marketing budgets temper OEM power, while GSMA-reported eSIM growth (over 1 billion eSIM-capable devices by 2023) marginally shifts activation control toward OEMs.

Spectrum and rights holders

Government-controlled spectrum auctions and licence conditions act as a de facto supplier with strong pricing power over Rogers, determining capex timing and renewal costs. Content rights owners and studios extract significant fees for TV and streaming bundles; Rogers’ exposure to sports is partly hedged by its 37.5% stake in Maple Leaf Sports & Entertainment and its involvement in the landmark 12-year, CAD 5.2 billion NHL rights framework. Regulatory terms and renewal cycles materially influence Rogers’ cost structure and capital allocation.

Towers, fiber, and backhaul

Tower landlords, utility pole owners and fiber wholesalers extract rents where Rogers lacks owned infrastructure, and site access, make-ready work and municipal permits often add 6–18 months of delay and material incremental costs; long-term leases (typical 15–20 years) limit operational flexibility while securing coverage. Network sharing in rural areas can materially mitigate this supplier power.

- Lease terms: 15–20 years

- Permitting delays: 6–18 months

- Mitigation: rural network sharing agreements

Cloud and software platforms

Core IT, billing, and cloud partners exert strong supplier power at Rogers through long implementations and mission-critical integrations that embed vendors into operations; vendor roadmaps and licensing models directly influence ongoing opex. Multiyear contracts and data gravity create high switching costs, while hybrid-cloud strategies and growing in-house engineering capability lower reliance on any single vendor.

- Long implementations

- Vendor roadmaps → opex

- Multiyear contracts

- Data gravity = switching barrier

- Hybrid-cloud + in-house = less single-vendor risk

Supplier power: concentrated RAN vendors, long leases, carrier 10.3M subs

Supplier power is high: Ericsson and Nokia supply the bulk of 5G RAN (majority of 2024 RAN revenue), raising switching costs and pricing leverage. OEMs (Apple, Samsung) and content rights holders push margins; Rogers had ~10.3M wireless subs (2024). Tower/fiber landlords, long leases (15–20 years) and permitting delays (6–18 months) further strengthen suppliers.

| Supplier | Impact |

|---|---|

| RAN vendors | Majority 2024 RAN revenue |

| Leases/permits | 15–20y / 6–18m |

What is included in the product

Tailored Porter’s Five Forces analysis for Rogers Communications, uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive technologies and regulatory risks that shape profitability.

One-sheet Porter's Five Forces for Rogers Communications—quickly spot regulatory, competitive, and supplier pressures to relieve strategic blind spots and speed boardroom decisions.

Customers Bargaining Power

Consumer price sensitivity

Households routinely compare plans across the Big 3 and challengers, keeping Rogers ARPU under pressure during promotional periods; the Big 3 control roughly 90% of the Canadian wireless market, intensifying competition. Economic downturns deepen downgrades and cord-cutting, while transparent comparison sites raise buyer information and switching. Bundled discounts and device financing mitigate direct price cuts.

Enterprise and government

Enterprise and government customers extract strong leverage from custom SLAs and volume discounts, often driving multi-year RFP processes that intensify carrier competition. Switching costs exist but are managed around device refresh cycles and MDM platforms, reducing lock-in. Rogers’ focus on private 5G and IoT solutions in 2024 creates differentiation levers that can blunt pure price negotiations.

Switching costs and churn

Number portability and growing eSIM adoption (≈25% in Canada by 2024) lower friction and raise buyer power, while device financing balances (~CAD 1.6bn) plus bundle pricing and loyalty perks create exit barriers. Rogers manages churn (postpaid churn ≈0.95% in 2024) with retention offers that compress margins. Service quality and nationwide coverage remain primary stickiness drivers.

Bundling expectations

Customers now expect meaningful discounts across wireless, internet, TV and home phone, with Canadian bundle penetration >60% in 2024; failure to deliver perceived bundle value prompts switching or downgrades, pressuring margins. Deeper cross-sell increases household lifetime value—industry estimates show ~25% uplift in LTV for multi-product customers in 2024—but concentrates negotiation power per household. Media content packaging (exclusive sports/news) materially shifts perceived bundle value and retention.

- Bundle penetration: >60% (Canada, 2024)

- LTV uplift: ~25% for multi-product households (2024)

- Higher negotiation leverage per household due to cross-sell depth

- Content packaging drives perceived bundle value

Digital service alternatives

OTT apps enable users to replace voice/SMS and TV, shifting bargaining power to buyers as cord-cutting rises; Rogers still holds ≈30% Canadian wireless market share (2024) but faces content substitution pressure. Rivals' FWA and fiber offers let consumers renegotiate plans, while BYOD options reduce device lock-in. Enhanced CX and self-service tools can win back some leverage.

- OTT substitution — higher buyer leverage

- FWA/fiber availability — easier plan renegotiation

- BYOD — lowers switching costs

- Customer experience/self-service — restores provider control

Buyers hold leverage: Big 3 ≈90%, eSIM ≈25%

Customers wield elevated bargaining power: Big 3 control ≈90% of wireless but Rogers holds ≈30% (2024), eSIM adoption ≈25% and number portability lower switching friction, while device financing balances ≈CAD 1.6bn and postpaid churn ≈0.95% keep retention central; bundle penetration >60% and ~25% LTV uplift for multi-product households concentrate negotiation leverage.

| Metric | 2024 |

|---|---|

| Big 3 market share | ≈90% |

| Rogers wireless share | ≈30% |

| eSIM adoption | ≈25% |

| Device financing balance | ≈CAD 1.6bn |

| Postpaid churn | ≈0.95% |

| Bundle penetration | >60% |

| LTV uplift (multi-product) | ≈25% |

Preview Before You Purchase

Rogers Communications Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Rogers Communications Porter's Five Forces analysis evaluates intense competitive rivalry in Canadian telecoms, moderate buyer power offset by bundled services, limited supplier leverage for network equipment, manageable threat of substitutes, and high barriers to entry due to infrastructure and regulation. Use-ready and fully formatted.