Rongsheng Petrochemical Boston Consulting Group Matrix

Actionable Strategy Starts Here

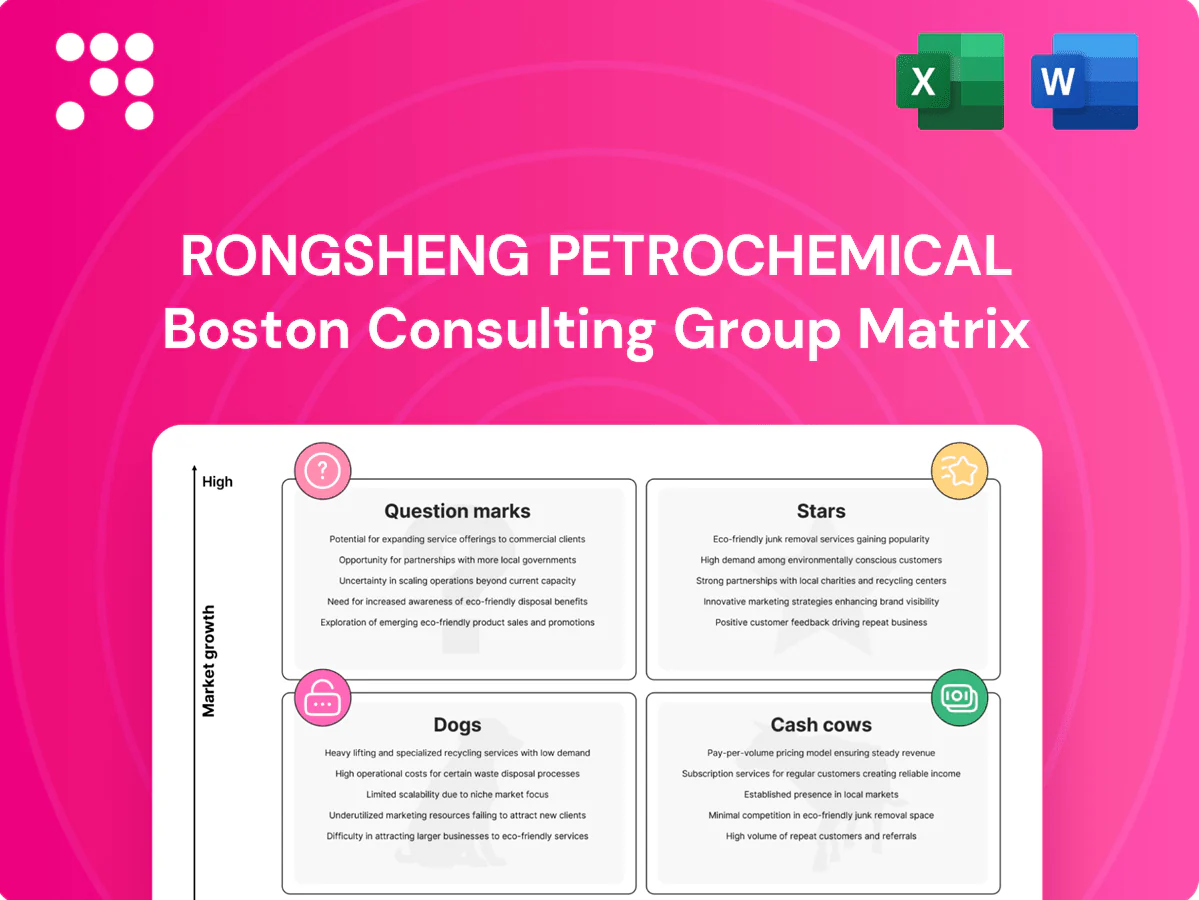

Quick look: Rongsheng Petrochemical’s BCG Matrix shows which product lines are driving growth, which are steady cash cows, and which need a rethink—Stars, Cash Cows, Question Marks, and Dogs all appear. This snapshot teases strategic moves, but the full BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and clear resource-allocation advice. Buy the complete report to get an editable Word analysis plus an Excel summary you can use in board decks and investor meetings. Purchase now for instant access and start making sharper decisions today.

Stars

Integrated PTA leadership

PTA sits at the heart of Rongsheng’s chain, where scale and full integration secure a leading market share as textiles and packaging demand expand. It pulls PX volume internally and feeds downstream polyester, keeping throughput high and utilization steady. Growth requires heavy capex, but the integrated flywheel supports sustained investment. Defend share now so the star later converts into a robust cash generator.

Paraxylene (PX) to polyester chain

Owning the PX–PTA–polyester path is a textbook star: Rongsheng’s integrated chain sits in a structurally growing pool with China accounting for roughly 60% of global PX demand in 2024, supporting high market share and volume-driven margins. Integration trims feedstock volatility and boosts pricing power by internalizing PX-to-PTA conversion and polyester yields. It’s capital hungry—aromatics and downstream debottlenecking require multi-hundred-million-dollar projects. Continue investing in yield improvements, energy efficiency and logistics to lock in leadership.

Refining–chemicals complex scale

The large, modern refining–chemicals platform in Zhoushan underpins advantaged costs and product flexibility, enabling feedstock optimization and deep conversion. As China shifts demand toward chemicals, the asset mix aligns with faster-growing chemical slates and specialty margins. High utilization demands steady capex and strict turnaround discipline to sustain reliability. The result is greater resilience and share gains in higher‑value chemical segments.

Polyester filament for apparel and home

Polyester filament for apparel and home is a clear star: demand is rising with fast fashion, athleisure, and home-textile trends while Rongsheng’s captive PTA supply and vertical integration deliver the cost and reliability advantages of a classic star. It still needs stronger brand-facing marketing, tighter spec control, and rapid order turnaround to win premium contracts and preserve margin. Scale plus service keep rivals at arm’s length.

- Demand drivers: fast fashion, athleisure, home textiles

- Competitive edge: captive PTA, integrated feedstock

- Execution gaps: marketing, specs, speed-to-order

- Defensibility: scale + service = barrier

PET resin for packaging

PET resin for packaging is a Star: beverage and consumer packaging demand across Asia remained robust in 2024, with Asia representing about two-thirds of global PET consumption, driven by single‑serve beverages and e‑commerce packing. Rongsheng’s cost‑advantaged integrated PTA feed underpins strong regional share, while bottle‑grade and recycling‑ready specs make the business capex‑intensive and cash flows frequently redeployed into maintenance and upgrades. Maintain quality leadership and secure long‑term brand‑owner contracts to preserve star status and margin premium.

- Market tag: Asia ≈ two‑thirds of global PET demand (2024)

- Competitive tag: PTA integration = cost advantage

- Capex tag: bottle‑grade + recycling readiness = high maintenance/reinvestment

- Strategy tag: secure brand contracts, maintain quality

Integrated PTA–PET chain at Zhoushan: scale-driven market share, high utilization, heavy capex

Rongsheng’s PTA–polyester and PET resin chains are Stars: integrated feedstock and Zhoushan scale deliver leading regional share and high utilization, supporting growth but requiring multi‑hundred‑million‑dollar capex to sustain. China accounted for ~60% of PX demand in 2024 and Asia ~66% of PET consumption, underpinning volume growth and pricing power.

| Product | 2024 market note | Key metric |

|---|---|---|

| PTA–polyester | China ≈60% PX demand (2024) | High utilization; capex: multi‑$100m |

| PET resin | Asia ≈66% global PET (2024) | Volume growth; brand contracts critical |

What is included in the product

BCG analysis of Rongsheng Petrochemical: maps Stars, Cash Cows, Question Marks, Dogs with invest/hold/divest advice and trend context.

One-page Rongsheng Petrochemical BCG Matrix placing each business unit in a quadrant—clarifies portfolio focus for fast executive decisions.

Cash Cows

Commodity polyester staple fiber

Commodity polyester staple fiber is a mature, high-volume cash cow for Rongsheng with a sticky B2B customer base and predictable production runs, typically managed to sustain plant utilization above 90%.

Vertical integration across PTA, MEG and PSF compresses unit costs and supports margins even in flat spot markets; limited promotional spend is needed because value stems from uptime and yield.

Strategy: milk free cash flow to fund targeted upgrades that historically cut energy intensity per ton by low single digits and protect long-term cash returns.

Aromatics co-products (benzene, toluene, MX)

Byproduct flows from Rongsheng’s aromatics train (benzene, toluene, MX) feed established downstream markets with stable volumes; 2024 average Asia prices ~benzene $800/t, toluene $700/t, MX $900/t underpin steady demand. Market share is solid on scale but growth is modest. Management prioritizes reliability and long-term off-take contracts to smooth margins; cash generation comes from steady spreads with minimal incremental capex.

Refined fuel byproducts

Diesel, gasoline and other refined fuels deliver baseline cash for Rongsheng: fuels accounted for the bulk of refinery throughput with refinery margins averaging roughly $9–11 per barrel in 2024. In a mature, regulated Chinese market these streams are not the growth engine but high utilization (>90% in 2024) sustains refinery economics. Focus on compliance, optimized blending and avoiding price wars to harvest cash while nudging the slate toward higher chemical yield.

Long-term textile mill contracts

Long-term textile mill contracts lock in PTA/polyester volumes, anchoring recurring cash flows for Rongsheng Petrochemical; in 2024 these contracts covered an estimated majority of B2B polyester shipments with OTIF above 95% supporting retention. Switching costs and logistics convenience keep market share high while service and OTIF now outcompete price as the differentiator. Maintain service levels, minimal selling expense (~1.2% of sales) and dependable margins.

- Locked-in volumes: recurring cash

- OTIF >95%: service-led retention

- Low selling expense ~1.2%

- Switching costs + logistics = high share

Operational excellence and utilities

Established utilities — integrated hydrogen, steam and power networks — feed Rongsheng’s complex with high reliability, turning the “plant behind the plant” into a cash-generating asset rather than a growth sink. Targeted low-capex measures in heat integration and advanced digital controls raise free cash by reducing fuel and maintenance intensity, enabling management to bank savings to fund the next growth bet. Operational excellence in utilities sustains margins under feedstock volatility and supports scale economics.

- Utilities: steady cash-generating backbone

- Hydrogen/steam/power: integrated supply reduces downtime

- Small capex: heat integration + digital controls = higher free cash

- Strategy: bank savings to fund capex for growth

High-utilization PSF and refinery fuels are cash cows, driving steady margins and recurring cash

Commodity polyester staple fiber and refinery fuels are high-volume cash cows for Rongsheng, sustaining >90% utilization and steady margins; vertical integration keeps unit costs low. Management milks free cash flow into targeted low-capex efficiency upgrades. Long-term B2B contracts and utilities reliability secure recurring cash.

| Metric | 2024 | Notes |

|---|---|---|

| PSF utilization | >90% | High uptime |

| Refinery margin | $9–11/bbl | Avg 2024 |

| Benzene | $800/t | Asia avg 2024 |

What You’re Viewing Is Included

Rongsheng Petrochemical BCG Matrix

The Rongsheng Petrochemical BCG Matrix you’re previewing is the exact file you’ll receive after purchase. No watermarks, no demo content — just a fully formatted, ready-to-use strategic report tailored for clarity. Purchase delivers the same document straight to your inbox, editable and print-ready. Use it in board meetings, investor decks, or internal planning with zero surprises.

Actionable Strategy Starts Here

Quick look: Rongsheng Petrochemical’s BCG Matrix shows which product lines are driving growth, which are steady cash cows, and which need a rethink—Stars, Cash Cows, Question Marks, and Dogs all appear. This snapshot teases strategic moves, but the full BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and clear resource-allocation advice. Buy the complete report to get an editable Word analysis plus an Excel summary you can use in board decks and investor meetings. Purchase now for instant access and start making sharper decisions today.

Stars

Integrated PTA leadership

PTA sits at the heart of Rongsheng’s chain, where scale and full integration secure a leading market share as textiles and packaging demand expand. It pulls PX volume internally and feeds downstream polyester, keeping throughput high and utilization steady. Growth requires heavy capex, but the integrated flywheel supports sustained investment. Defend share now so the star later converts into a robust cash generator.

Paraxylene (PX) to polyester chain

Owning the PX–PTA–polyester path is a textbook star: Rongsheng’s integrated chain sits in a structurally growing pool with China accounting for roughly 60% of global PX demand in 2024, supporting high market share and volume-driven margins. Integration trims feedstock volatility and boosts pricing power by internalizing PX-to-PTA conversion and polyester yields. It’s capital hungry—aromatics and downstream debottlenecking require multi-hundred-million-dollar projects. Continue investing in yield improvements, energy efficiency and logistics to lock in leadership.

Refining–chemicals complex scale

The large, modern refining–chemicals platform in Zhoushan underpins advantaged costs and product flexibility, enabling feedstock optimization and deep conversion. As China shifts demand toward chemicals, the asset mix aligns with faster-growing chemical slates and specialty margins. High utilization demands steady capex and strict turnaround discipline to sustain reliability. The result is greater resilience and share gains in higher‑value chemical segments.

Polyester filament for apparel and home

Polyester filament for apparel and home is a clear star: demand is rising with fast fashion, athleisure, and home-textile trends while Rongsheng’s captive PTA supply and vertical integration deliver the cost and reliability advantages of a classic star. It still needs stronger brand-facing marketing, tighter spec control, and rapid order turnaround to win premium contracts and preserve margin. Scale plus service keep rivals at arm’s length.

- Demand drivers: fast fashion, athleisure, home textiles

- Competitive edge: captive PTA, integrated feedstock

- Execution gaps: marketing, specs, speed-to-order

- Defensibility: scale + service = barrier

PET resin for packaging

PET resin for packaging is a Star: beverage and consumer packaging demand across Asia remained robust in 2024, with Asia representing about two-thirds of global PET consumption, driven by single‑serve beverages and e‑commerce packing. Rongsheng’s cost‑advantaged integrated PTA feed underpins strong regional share, while bottle‑grade and recycling‑ready specs make the business capex‑intensive and cash flows frequently redeployed into maintenance and upgrades. Maintain quality leadership and secure long‑term brand‑owner contracts to preserve star status and margin premium.

- Market tag: Asia ≈ two‑thirds of global PET demand (2024)

- Competitive tag: PTA integration = cost advantage

- Capex tag: bottle‑grade + recycling readiness = high maintenance/reinvestment

- Strategy tag: secure brand contracts, maintain quality

Integrated PTA–PET chain at Zhoushan: scale-driven market share, high utilization, heavy capex

Rongsheng’s PTA–polyester and PET resin chains are Stars: integrated feedstock and Zhoushan scale deliver leading regional share and high utilization, supporting growth but requiring multi‑hundred‑million‑dollar capex to sustain. China accounted for ~60% of PX demand in 2024 and Asia ~66% of PET consumption, underpinning volume growth and pricing power.

| Product | 2024 market note | Key metric |

|---|---|---|

| PTA–polyester | China ≈60% PX demand (2024) | High utilization; capex: multi‑$100m |

| PET resin | Asia ≈66% global PET (2024) | Volume growth; brand contracts critical |

What is included in the product

BCG analysis of Rongsheng Petrochemical: maps Stars, Cash Cows, Question Marks, Dogs with invest/hold/divest advice and trend context.

One-page Rongsheng Petrochemical BCG Matrix placing each business unit in a quadrant—clarifies portfolio focus for fast executive decisions.

Cash Cows

Commodity polyester staple fiber

Commodity polyester staple fiber is a mature, high-volume cash cow for Rongsheng with a sticky B2B customer base and predictable production runs, typically managed to sustain plant utilization above 90%.

Vertical integration across PTA, MEG and PSF compresses unit costs and supports margins even in flat spot markets; limited promotional spend is needed because value stems from uptime and yield.

Strategy: milk free cash flow to fund targeted upgrades that historically cut energy intensity per ton by low single digits and protect long-term cash returns.

Aromatics co-products (benzene, toluene, MX)

Byproduct flows from Rongsheng’s aromatics train (benzene, toluene, MX) feed established downstream markets with stable volumes; 2024 average Asia prices ~benzene $800/t, toluene $700/t, MX $900/t underpin steady demand. Market share is solid on scale but growth is modest. Management prioritizes reliability and long-term off-take contracts to smooth margins; cash generation comes from steady spreads with minimal incremental capex.

Refined fuel byproducts

Diesel, gasoline and other refined fuels deliver baseline cash for Rongsheng: fuels accounted for the bulk of refinery throughput with refinery margins averaging roughly $9–11 per barrel in 2024. In a mature, regulated Chinese market these streams are not the growth engine but high utilization (>90% in 2024) sustains refinery economics. Focus on compliance, optimized blending and avoiding price wars to harvest cash while nudging the slate toward higher chemical yield.

Long-term textile mill contracts

Long-term textile mill contracts lock in PTA/polyester volumes, anchoring recurring cash flows for Rongsheng Petrochemical; in 2024 these contracts covered an estimated majority of B2B polyester shipments with OTIF above 95% supporting retention. Switching costs and logistics convenience keep market share high while service and OTIF now outcompete price as the differentiator. Maintain service levels, minimal selling expense (~1.2% of sales) and dependable margins.

- Locked-in volumes: recurring cash

- OTIF >95%: service-led retention

- Low selling expense ~1.2%

- Switching costs + logistics = high share

Operational excellence and utilities

Established utilities — integrated hydrogen, steam and power networks — feed Rongsheng’s complex with high reliability, turning the “plant behind the plant” into a cash-generating asset rather than a growth sink. Targeted low-capex measures in heat integration and advanced digital controls raise free cash by reducing fuel and maintenance intensity, enabling management to bank savings to fund the next growth bet. Operational excellence in utilities sustains margins under feedstock volatility and supports scale economics.

- Utilities: steady cash-generating backbone

- Hydrogen/steam/power: integrated supply reduces downtime

- Small capex: heat integration + digital controls = higher free cash

- Strategy: bank savings to fund capex for growth

High-utilization PSF and refinery fuels are cash cows, driving steady margins and recurring cash

Commodity polyester staple fiber and refinery fuels are high-volume cash cows for Rongsheng, sustaining >90% utilization and steady margins; vertical integration keeps unit costs low. Management milks free cash flow into targeted low-capex efficiency upgrades. Long-term B2B contracts and utilities reliability secure recurring cash.

| Metric | 2024 | Notes |

|---|---|---|

| PSF utilization | >90% | High uptime |

| Refinery margin | $9–11/bbl | Avg 2024 |

| Benzene | $800/t | Asia avg 2024 |

What You’re Viewing Is Included

Rongsheng Petrochemical BCG Matrix

The Rongsheng Petrochemical BCG Matrix you’re previewing is the exact file you’ll receive after purchase. No watermarks, no demo content — just a fully formatted, ready-to-use strategic report tailored for clarity. Purchase delivers the same document straight to your inbox, editable and print-ready. Use it in board meetings, investor decks, or internal planning with zero surprises.

Original: $10.00

-65%$10.00

$3.50Description

Actionable Strategy Starts Here

Quick look: Rongsheng Petrochemical’s BCG Matrix shows which product lines are driving growth, which are steady cash cows, and which need a rethink—Stars, Cash Cows, Question Marks, and Dogs all appear. This snapshot teases strategic moves, but the full BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and clear resource-allocation advice. Buy the complete report to get an editable Word analysis plus an Excel summary you can use in board decks and investor meetings. Purchase now for instant access and start making sharper decisions today.

Stars

Integrated PTA leadership

PTA sits at the heart of Rongsheng’s chain, where scale and full integration secure a leading market share as textiles and packaging demand expand. It pulls PX volume internally and feeds downstream polyester, keeping throughput high and utilization steady. Growth requires heavy capex, but the integrated flywheel supports sustained investment. Defend share now so the star later converts into a robust cash generator.

Paraxylene (PX) to polyester chain

Owning the PX–PTA–polyester path is a textbook star: Rongsheng’s integrated chain sits in a structurally growing pool with China accounting for roughly 60% of global PX demand in 2024, supporting high market share and volume-driven margins. Integration trims feedstock volatility and boosts pricing power by internalizing PX-to-PTA conversion and polyester yields. It’s capital hungry—aromatics and downstream debottlenecking require multi-hundred-million-dollar projects. Continue investing in yield improvements, energy efficiency and logistics to lock in leadership.

Refining–chemicals complex scale

The large, modern refining–chemicals platform in Zhoushan underpins advantaged costs and product flexibility, enabling feedstock optimization and deep conversion. As China shifts demand toward chemicals, the asset mix aligns with faster-growing chemical slates and specialty margins. High utilization demands steady capex and strict turnaround discipline to sustain reliability. The result is greater resilience and share gains in higher‑value chemical segments.

Polyester filament for apparel and home

Polyester filament for apparel and home is a clear star: demand is rising with fast fashion, athleisure, and home-textile trends while Rongsheng’s captive PTA supply and vertical integration deliver the cost and reliability advantages of a classic star. It still needs stronger brand-facing marketing, tighter spec control, and rapid order turnaround to win premium contracts and preserve margin. Scale plus service keep rivals at arm’s length.

- Demand drivers: fast fashion, athleisure, home textiles

- Competitive edge: captive PTA, integrated feedstock

- Execution gaps: marketing, specs, speed-to-order

- Defensibility: scale + service = barrier

PET resin for packaging

PET resin for packaging is a Star: beverage and consumer packaging demand across Asia remained robust in 2024, with Asia representing about two-thirds of global PET consumption, driven by single‑serve beverages and e‑commerce packing. Rongsheng’s cost‑advantaged integrated PTA feed underpins strong regional share, while bottle‑grade and recycling‑ready specs make the business capex‑intensive and cash flows frequently redeployed into maintenance and upgrades. Maintain quality leadership and secure long‑term brand‑owner contracts to preserve star status and margin premium.

- Market tag: Asia ≈ two‑thirds of global PET demand (2024)

- Competitive tag: PTA integration = cost advantage

- Capex tag: bottle‑grade + recycling readiness = high maintenance/reinvestment

- Strategy tag: secure brand contracts, maintain quality

Integrated PTA–PET chain at Zhoushan: scale-driven market share, high utilization, heavy capex

Rongsheng’s PTA–polyester and PET resin chains are Stars: integrated feedstock and Zhoushan scale deliver leading regional share and high utilization, supporting growth but requiring multi‑hundred‑million‑dollar capex to sustain. China accounted for ~60% of PX demand in 2024 and Asia ~66% of PET consumption, underpinning volume growth and pricing power.

| Product | 2024 market note | Key metric |

|---|---|---|

| PTA–polyester | China ≈60% PX demand (2024) | High utilization; capex: multi‑$100m |

| PET resin | Asia ≈66% global PET (2024) | Volume growth; brand contracts critical |

What is included in the product

BCG analysis of Rongsheng Petrochemical: maps Stars, Cash Cows, Question Marks, Dogs with invest/hold/divest advice and trend context.

One-page Rongsheng Petrochemical BCG Matrix placing each business unit in a quadrant—clarifies portfolio focus for fast executive decisions.

Cash Cows

Commodity polyester staple fiber

Commodity polyester staple fiber is a mature, high-volume cash cow for Rongsheng with a sticky B2B customer base and predictable production runs, typically managed to sustain plant utilization above 90%.

Vertical integration across PTA, MEG and PSF compresses unit costs and supports margins even in flat spot markets; limited promotional spend is needed because value stems from uptime and yield.

Strategy: milk free cash flow to fund targeted upgrades that historically cut energy intensity per ton by low single digits and protect long-term cash returns.

Aromatics co-products (benzene, toluene, MX)

Byproduct flows from Rongsheng’s aromatics train (benzene, toluene, MX) feed established downstream markets with stable volumes; 2024 average Asia prices ~benzene $800/t, toluene $700/t, MX $900/t underpin steady demand. Market share is solid on scale but growth is modest. Management prioritizes reliability and long-term off-take contracts to smooth margins; cash generation comes from steady spreads with minimal incremental capex.

Refined fuel byproducts

Diesel, gasoline and other refined fuels deliver baseline cash for Rongsheng: fuels accounted for the bulk of refinery throughput with refinery margins averaging roughly $9–11 per barrel in 2024. In a mature, regulated Chinese market these streams are not the growth engine but high utilization (>90% in 2024) sustains refinery economics. Focus on compliance, optimized blending and avoiding price wars to harvest cash while nudging the slate toward higher chemical yield.

Long-term textile mill contracts

Long-term textile mill contracts lock in PTA/polyester volumes, anchoring recurring cash flows for Rongsheng Petrochemical; in 2024 these contracts covered an estimated majority of B2B polyester shipments with OTIF above 95% supporting retention. Switching costs and logistics convenience keep market share high while service and OTIF now outcompete price as the differentiator. Maintain service levels, minimal selling expense (~1.2% of sales) and dependable margins.

- Locked-in volumes: recurring cash

- OTIF >95%: service-led retention

- Low selling expense ~1.2%

- Switching costs + logistics = high share

Operational excellence and utilities

Established utilities — integrated hydrogen, steam and power networks — feed Rongsheng’s complex with high reliability, turning the “plant behind the plant” into a cash-generating asset rather than a growth sink. Targeted low-capex measures in heat integration and advanced digital controls raise free cash by reducing fuel and maintenance intensity, enabling management to bank savings to fund the next growth bet. Operational excellence in utilities sustains margins under feedstock volatility and supports scale economics.

- Utilities: steady cash-generating backbone

- Hydrogen/steam/power: integrated supply reduces downtime

- Small capex: heat integration + digital controls = higher free cash

- Strategy: bank savings to fund capex for growth

High-utilization PSF and refinery fuels are cash cows, driving steady margins and recurring cash

Commodity polyester staple fiber and refinery fuels are high-volume cash cows for Rongsheng, sustaining >90% utilization and steady margins; vertical integration keeps unit costs low. Management milks free cash flow into targeted low-capex efficiency upgrades. Long-term B2B contracts and utilities reliability secure recurring cash.

| Metric | 2024 | Notes |

|---|---|---|

| PSF utilization | >90% | High uptime |

| Refinery margin | $9–11/bbl | Avg 2024 |

| Benzene | $800/t | Asia avg 2024 |

What You’re Viewing Is Included

Rongsheng Petrochemical BCG Matrix

The Rongsheng Petrochemical BCG Matrix you’re previewing is the exact file you’ll receive after purchase. No watermarks, no demo content — just a fully formatted, ready-to-use strategic report tailored for clarity. Purchase delivers the same document straight to your inbox, editable and print-ready. Use it in board meetings, investor decks, or internal planning with zero surprises.