Ross Stores Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Ross Stores faces intense price competition and high buyer sensitivity, moderate supplier influence, low threat of scale-driven entrants, and meaningful substitute pressure from online retailers; strategic positioning and cost discipline are key. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ross’s competitive dynamics and drive smarter decisions.

Suppliers Bargaining Power

Fragmented brand supplier base

The off-price supply pool spans thousands of brands, manufacturers and importers, limiting any single vendor’s leverage. Ross routinely plays vendors against each other to secure favorable pricing and timing, reducing supplier hold-up risk. This fragmentation enables rapid assortment refresh and high SKU turnover without dependency on a few labels. The breadth of sources supports consistent margin resilience.

Vendor need to clear excess

Brands rely on off-price channels to monetize overstocks, canceled orders, and packaway inventory, a structural need that weakens supplier bargaining power. Ross’s scale — operating over 2,200 stores in 2024 — and predictable clearance cadence make it a preferred off-loader. Vendors routinely accept lower margins for speed, confidentiality, and brand protection, prioritizing inventory turn over higher wholesale pricing.

Scale and flexible buying

Ross’s scale—operating over 1,500 off-price stores—and opportunistic buying allow take-all deals at steep discounts, forcing suppliers to accept lower margins to move volume. Volume commitments and rapid decision cycles increase Ross’s leverage, while ability to cherry-pick styles, sizes, and regions concentrates selling pressure on suppliers. In 2023 Ross reported annual net sales exceeding $15 billion, underscoring buying clout and compelling aggressive supplier pricing to turn inventory quickly.

Low switching costs

Low switching costs let Ross shift orders across vendors, categories, and regions with minimal friction, and in 2024 multi-sourcing further diluted supplier leverage over pricing and terms. Vendor scorecards and strict compliance standards commoditize supply, while the threat of losing Ross’s sizeable off-price demand forces suppliers to conform on cost and lead times.

- Multi-sourcing reduces supplier share

- Scorecards standardize compliance

- Demand loss risk enforces concessions

Premium brand scarcity pockets

Access to coveted in-season designer labels is often constrained, creating localized supplier power as some brands tightly gate off-price distribution to protect brand image. Ross mitigates this through long-standing vendor relationships and strict confidentiality measures, but 2024 scarcity episodes still force higher purchase costs or volume limits in key categories.

- Localized scarcity raises supplier leverage

- Brand gating limits off-price supply

- Ross relies on long-term ties/confidentiality

- 2024 shortages increased category cost/limited inventory

Scale mutes supplier power but 2024 scarcity raised costs and cut designer supply

Supplier power is muted by a fragmented off-price supply base and Ross’s scale (about 2,200 stores in 2024), enabling aggressive sourcing, low switching costs, and vendor concessions; Ross reported net sales >$15B in 2023. Localized brand gating and 2024 scarcity episodes nonetheless pushed up costs and limited access to key designer labels.

| Metric | Value |

|---|---|

| Stores (2024) | ~2,200 |

| Net sales (2023) | >$15B |

| 2024 scarcity | Increased category costs / limited supply |

What is included in the product

Tailored Porter's Five Forces analysis for Ross Stores, uncovering competitive intensity, buyer/supplier power, threat of entrants and substitutes, plus disruptive risks and strategic levers that shape its pricing and profitability.

Clear one-sheet Porter's Five Forces for Ross Stores that highlights competitive pressures and supplier/buyer leverage—perfect for quick strategic decisions; customizable pressure levels and radar visualization make it easy to model scenarios and copy straight into slides.

Customers Bargaining Power

High price sensitivity

Ross targets value-focused shoppers who compare across discount formats; with roughly 2,200 stores in 2024, small price gaps can quickly shift traffic to TJX, Burlington or mass merchants. Frequent promotions elsewhere heighten expectations and train shoppers to seek deals. Ross must sustain visible bargains and compelling in-store markdowns to defend trip frequency and basket size amid high price sensitivity.

Low switching costs

Low switching costs mean shoppers can jump between off-price, mass and e-commerce channels easily; US e-commerce penetration reached about 18% in 2024, increasing alternative access. Ross had roughly 2,200 stores in 2024, so convenience and proximity often drive visits rather than loyalty. There are no contracts or bespoke products to lock customers in, and any assortment miss risks immediate defection to competitors.

Treasure-hunt dampens comparability

Ross's treasure-hunt model — with unique, fast-turn assortments — reduces SKU-to-SKU price comparisons and narrows direct buyer power at the item level, supporting margin resilience; Ross operated about 2,200 stores in 2024 and reported roughly $18.2 billion in fiscal 2024 net sales. Perceived discovery value often offsets limited services, encouraging one-time purchases despite lower service levels. Repeat behavior still hinges on overall value perception and price-to-quality trade-offs.

Limited online presence influence

Ross’s minimal e-commerce keeps price transparency lower than pure-play online rivals, preserving a treasure-hunt in-store experience that retains foot traffic but cedes digital convenience. Shoppers still use mobile to benchmark prices, so buyer leverage is curbed but not eliminated; Ross operated over 2,200 stores in 2024.

- Limited e‑commerce reduces price transparency

- Store-only treasure‑hunt retains traffic

- Mobile benchmarking sustains buyer leverage

- Over 2,200 stores in 2024

Macro elasticity of demand

Macro elasticity favors Ross: during downturns consumers trade down into off-price, lifting traffic, while expansions see some trade-up that modestly increases buyer power. US CPI eased from a 2022 peak near 8% to about 3.4% in 2024, heightening price scrutiny during inflation spikes and driving basket optimization. Clear value communication and SKU/mix management remain critical to defend margins and frequency.

- Off-price demand rises in recessions: traffic boost

- Expansions: partial trade-up, modest buyer power gain

- 2024 CPI ~3.4%: increases price sensitivity

- Priority: value messaging and assortment/mix control

Treasure-hunt off-price wins despite high switching power; 18% e-commerce

Customers have high bargaining power due to low switching costs and 18% US e‑commerce penetration in 2024, but Ross’s treasure‑hunt model and limited online presence curb item‑level price comparisons. Ross operated ~2,200 stores and reported $18.2B net sales in fiscal 2024; CPI ~3.4% in 2024 raises price sensitivity. Value perception drives repeat visits more than loyalty.

| Metric | 2024 |

|---|---|

| Stores | ~2,200 |

| Net sales | $18.2B |

| US e‑commerce | ~18% |

| CPI | ~3.4% |

What You See Is What You Get

Ross Stores Porter's Five Forces Analysis

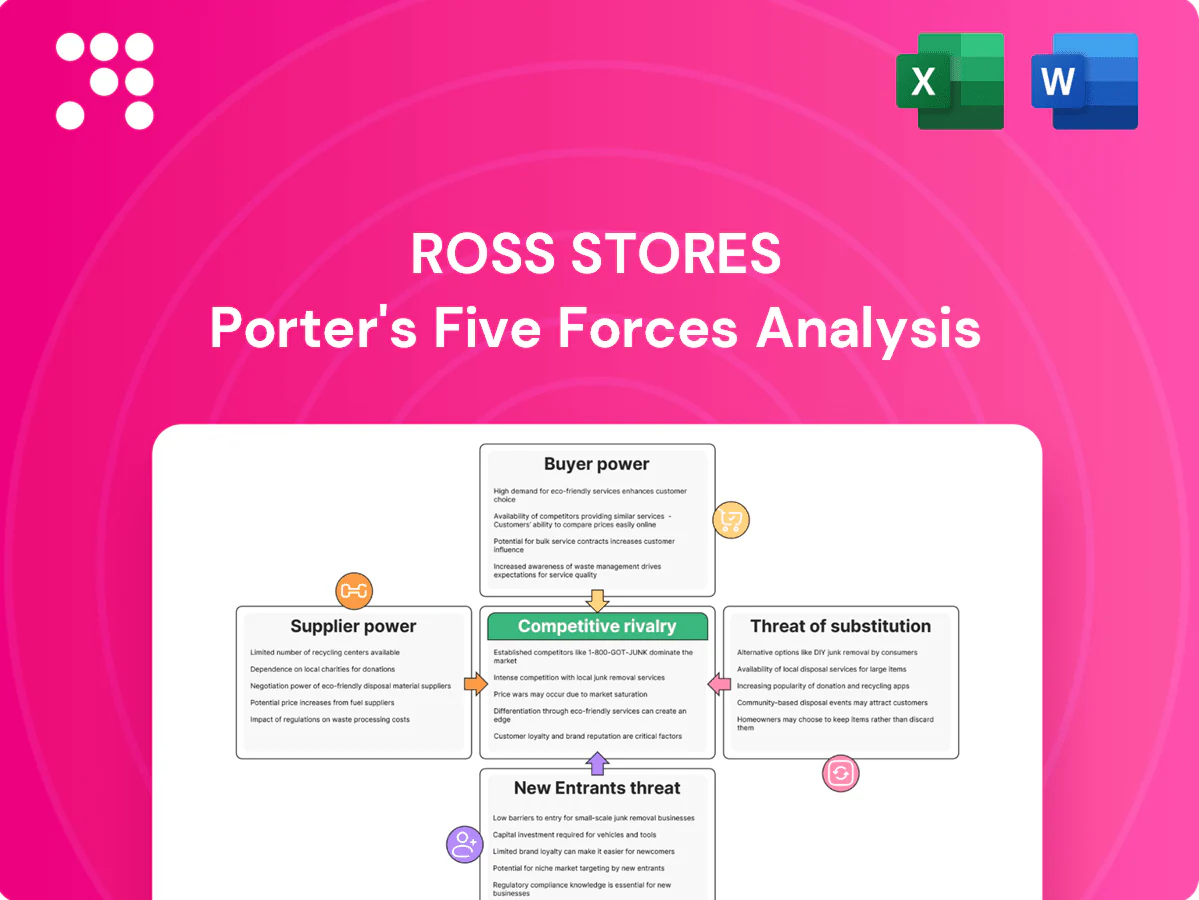

This Ross Stores Porter's Five Forces analysis assesses competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and industry dynamics to inform strategy and valuation. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

Don't Miss the Bigger Picture

Ross Stores faces intense price competition and high buyer sensitivity, moderate supplier influence, low threat of scale-driven entrants, and meaningful substitute pressure from online retailers; strategic positioning and cost discipline are key. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ross’s competitive dynamics and drive smarter decisions.

Suppliers Bargaining Power

Fragmented brand supplier base

The off-price supply pool spans thousands of brands, manufacturers and importers, limiting any single vendor’s leverage. Ross routinely plays vendors against each other to secure favorable pricing and timing, reducing supplier hold-up risk. This fragmentation enables rapid assortment refresh and high SKU turnover without dependency on a few labels. The breadth of sources supports consistent margin resilience.

Vendor need to clear excess

Brands rely on off-price channels to monetize overstocks, canceled orders, and packaway inventory, a structural need that weakens supplier bargaining power. Ross’s scale — operating over 2,200 stores in 2024 — and predictable clearance cadence make it a preferred off-loader. Vendors routinely accept lower margins for speed, confidentiality, and brand protection, prioritizing inventory turn over higher wholesale pricing.

Scale and flexible buying

Ross’s scale—operating over 1,500 off-price stores—and opportunistic buying allow take-all deals at steep discounts, forcing suppliers to accept lower margins to move volume. Volume commitments and rapid decision cycles increase Ross’s leverage, while ability to cherry-pick styles, sizes, and regions concentrates selling pressure on suppliers. In 2023 Ross reported annual net sales exceeding $15 billion, underscoring buying clout and compelling aggressive supplier pricing to turn inventory quickly.

Low switching costs

Low switching costs let Ross shift orders across vendors, categories, and regions with minimal friction, and in 2024 multi-sourcing further diluted supplier leverage over pricing and terms. Vendor scorecards and strict compliance standards commoditize supply, while the threat of losing Ross’s sizeable off-price demand forces suppliers to conform on cost and lead times.

- Multi-sourcing reduces supplier share

- Scorecards standardize compliance

- Demand loss risk enforces concessions

Premium brand scarcity pockets

Access to coveted in-season designer labels is often constrained, creating localized supplier power as some brands tightly gate off-price distribution to protect brand image. Ross mitigates this through long-standing vendor relationships and strict confidentiality measures, but 2024 scarcity episodes still force higher purchase costs or volume limits in key categories.

- Localized scarcity raises supplier leverage

- Brand gating limits off-price supply

- Ross relies on long-term ties/confidentiality

- 2024 shortages increased category cost/limited inventory

Scale mutes supplier power but 2024 scarcity raised costs and cut designer supply

Supplier power is muted by a fragmented off-price supply base and Ross’s scale (about 2,200 stores in 2024), enabling aggressive sourcing, low switching costs, and vendor concessions; Ross reported net sales >$15B in 2023. Localized brand gating and 2024 scarcity episodes nonetheless pushed up costs and limited access to key designer labels.

| Metric | Value |

|---|---|

| Stores (2024) | ~2,200 |

| Net sales (2023) | >$15B |

| 2024 scarcity | Increased category costs / limited supply |

What is included in the product

Tailored Porter's Five Forces analysis for Ross Stores, uncovering competitive intensity, buyer/supplier power, threat of entrants and substitutes, plus disruptive risks and strategic levers that shape its pricing and profitability.

Clear one-sheet Porter's Five Forces for Ross Stores that highlights competitive pressures and supplier/buyer leverage—perfect for quick strategic decisions; customizable pressure levels and radar visualization make it easy to model scenarios and copy straight into slides.

Customers Bargaining Power

High price sensitivity

Ross targets value-focused shoppers who compare across discount formats; with roughly 2,200 stores in 2024, small price gaps can quickly shift traffic to TJX, Burlington or mass merchants. Frequent promotions elsewhere heighten expectations and train shoppers to seek deals. Ross must sustain visible bargains and compelling in-store markdowns to defend trip frequency and basket size amid high price sensitivity.

Low switching costs

Low switching costs mean shoppers can jump between off-price, mass and e-commerce channels easily; US e-commerce penetration reached about 18% in 2024, increasing alternative access. Ross had roughly 2,200 stores in 2024, so convenience and proximity often drive visits rather than loyalty. There are no contracts or bespoke products to lock customers in, and any assortment miss risks immediate defection to competitors.

Treasure-hunt dampens comparability

Ross's treasure-hunt model — with unique, fast-turn assortments — reduces SKU-to-SKU price comparisons and narrows direct buyer power at the item level, supporting margin resilience; Ross operated about 2,200 stores in 2024 and reported roughly $18.2 billion in fiscal 2024 net sales. Perceived discovery value often offsets limited services, encouraging one-time purchases despite lower service levels. Repeat behavior still hinges on overall value perception and price-to-quality trade-offs.

Limited online presence influence

Ross’s minimal e-commerce keeps price transparency lower than pure-play online rivals, preserving a treasure-hunt in-store experience that retains foot traffic but cedes digital convenience. Shoppers still use mobile to benchmark prices, so buyer leverage is curbed but not eliminated; Ross operated over 2,200 stores in 2024.

- Limited e‑commerce reduces price transparency

- Store-only treasure‑hunt retains traffic

- Mobile benchmarking sustains buyer leverage

- Over 2,200 stores in 2024

Macro elasticity of demand

Macro elasticity favors Ross: during downturns consumers trade down into off-price, lifting traffic, while expansions see some trade-up that modestly increases buyer power. US CPI eased from a 2022 peak near 8% to about 3.4% in 2024, heightening price scrutiny during inflation spikes and driving basket optimization. Clear value communication and SKU/mix management remain critical to defend margins and frequency.

- Off-price demand rises in recessions: traffic boost

- Expansions: partial trade-up, modest buyer power gain

- 2024 CPI ~3.4%: increases price sensitivity

- Priority: value messaging and assortment/mix control

Treasure-hunt off-price wins despite high switching power; 18% e-commerce

Customers have high bargaining power due to low switching costs and 18% US e‑commerce penetration in 2024, but Ross’s treasure‑hunt model and limited online presence curb item‑level price comparisons. Ross operated ~2,200 stores and reported $18.2B net sales in fiscal 2024; CPI ~3.4% in 2024 raises price sensitivity. Value perception drives repeat visits more than loyalty.

| Metric | 2024 |

|---|---|

| Stores | ~2,200 |

| Net sales | $18.2B |

| US e‑commerce | ~18% |

| CPI | ~3.4% |

What You See Is What You Get

Ross Stores Porter's Five Forces Analysis

This Ross Stores Porter's Five Forces analysis assesses competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and industry dynamics to inform strategy and valuation. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Ross Stores faces intense price competition and high buyer sensitivity, moderate supplier influence, low threat of scale-driven entrants, and meaningful substitute pressure from online retailers; strategic positioning and cost discipline are key. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ross’s competitive dynamics and drive smarter decisions.

Suppliers Bargaining Power

Fragmented brand supplier base

The off-price supply pool spans thousands of brands, manufacturers and importers, limiting any single vendor’s leverage. Ross routinely plays vendors against each other to secure favorable pricing and timing, reducing supplier hold-up risk. This fragmentation enables rapid assortment refresh and high SKU turnover without dependency on a few labels. The breadth of sources supports consistent margin resilience.

Vendor need to clear excess

Brands rely on off-price channels to monetize overstocks, canceled orders, and packaway inventory, a structural need that weakens supplier bargaining power. Ross’s scale — operating over 2,200 stores in 2024 — and predictable clearance cadence make it a preferred off-loader. Vendors routinely accept lower margins for speed, confidentiality, and brand protection, prioritizing inventory turn over higher wholesale pricing.

Scale and flexible buying

Ross’s scale—operating over 1,500 off-price stores—and opportunistic buying allow take-all deals at steep discounts, forcing suppliers to accept lower margins to move volume. Volume commitments and rapid decision cycles increase Ross’s leverage, while ability to cherry-pick styles, sizes, and regions concentrates selling pressure on suppliers. In 2023 Ross reported annual net sales exceeding $15 billion, underscoring buying clout and compelling aggressive supplier pricing to turn inventory quickly.

Low switching costs

Low switching costs let Ross shift orders across vendors, categories, and regions with minimal friction, and in 2024 multi-sourcing further diluted supplier leverage over pricing and terms. Vendor scorecards and strict compliance standards commoditize supply, while the threat of losing Ross’s sizeable off-price demand forces suppliers to conform on cost and lead times.

- Multi-sourcing reduces supplier share

- Scorecards standardize compliance

- Demand loss risk enforces concessions

Premium brand scarcity pockets

Access to coveted in-season designer labels is often constrained, creating localized supplier power as some brands tightly gate off-price distribution to protect brand image. Ross mitigates this through long-standing vendor relationships and strict confidentiality measures, but 2024 scarcity episodes still force higher purchase costs or volume limits in key categories.

- Localized scarcity raises supplier leverage

- Brand gating limits off-price supply

- Ross relies on long-term ties/confidentiality

- 2024 shortages increased category cost/limited inventory

Scale mutes supplier power but 2024 scarcity raised costs and cut designer supply

Supplier power is muted by a fragmented off-price supply base and Ross’s scale (about 2,200 stores in 2024), enabling aggressive sourcing, low switching costs, and vendor concessions; Ross reported net sales >$15B in 2023. Localized brand gating and 2024 scarcity episodes nonetheless pushed up costs and limited access to key designer labels.

| Metric | Value |

|---|---|

| Stores (2024) | ~2,200 |

| Net sales (2023) | >$15B |

| 2024 scarcity | Increased category costs / limited supply |

What is included in the product

Tailored Porter's Five Forces analysis for Ross Stores, uncovering competitive intensity, buyer/supplier power, threat of entrants and substitutes, plus disruptive risks and strategic levers that shape its pricing and profitability.

Clear one-sheet Porter's Five Forces for Ross Stores that highlights competitive pressures and supplier/buyer leverage—perfect for quick strategic decisions; customizable pressure levels and radar visualization make it easy to model scenarios and copy straight into slides.

Customers Bargaining Power

High price sensitivity

Ross targets value-focused shoppers who compare across discount formats; with roughly 2,200 stores in 2024, small price gaps can quickly shift traffic to TJX, Burlington or mass merchants. Frequent promotions elsewhere heighten expectations and train shoppers to seek deals. Ross must sustain visible bargains and compelling in-store markdowns to defend trip frequency and basket size amid high price sensitivity.

Low switching costs

Low switching costs mean shoppers can jump between off-price, mass and e-commerce channels easily; US e-commerce penetration reached about 18% in 2024, increasing alternative access. Ross had roughly 2,200 stores in 2024, so convenience and proximity often drive visits rather than loyalty. There are no contracts or bespoke products to lock customers in, and any assortment miss risks immediate defection to competitors.

Treasure-hunt dampens comparability

Ross's treasure-hunt model — with unique, fast-turn assortments — reduces SKU-to-SKU price comparisons and narrows direct buyer power at the item level, supporting margin resilience; Ross operated about 2,200 stores in 2024 and reported roughly $18.2 billion in fiscal 2024 net sales. Perceived discovery value often offsets limited services, encouraging one-time purchases despite lower service levels. Repeat behavior still hinges on overall value perception and price-to-quality trade-offs.

Limited online presence influence

Ross’s minimal e-commerce keeps price transparency lower than pure-play online rivals, preserving a treasure-hunt in-store experience that retains foot traffic but cedes digital convenience. Shoppers still use mobile to benchmark prices, so buyer leverage is curbed but not eliminated; Ross operated over 2,200 stores in 2024.

- Limited e‑commerce reduces price transparency

- Store-only treasure‑hunt retains traffic

- Mobile benchmarking sustains buyer leverage

- Over 2,200 stores in 2024

Macro elasticity of demand

Macro elasticity favors Ross: during downturns consumers trade down into off-price, lifting traffic, while expansions see some trade-up that modestly increases buyer power. US CPI eased from a 2022 peak near 8% to about 3.4% in 2024, heightening price scrutiny during inflation spikes and driving basket optimization. Clear value communication and SKU/mix management remain critical to defend margins and frequency.

- Off-price demand rises in recessions: traffic boost

- Expansions: partial trade-up, modest buyer power gain

- 2024 CPI ~3.4%: increases price sensitivity

- Priority: value messaging and assortment/mix control

Treasure-hunt off-price wins despite high switching power; 18% e-commerce

Customers have high bargaining power due to low switching costs and 18% US e‑commerce penetration in 2024, but Ross’s treasure‑hunt model and limited online presence curb item‑level price comparisons. Ross operated ~2,200 stores and reported $18.2B net sales in fiscal 2024; CPI ~3.4% in 2024 raises price sensitivity. Value perception drives repeat visits more than loyalty.

| Metric | 2024 |

|---|---|

| Stores | ~2,200 |

| Net sales | $18.2B |

| US e‑commerce | ~18% |

| CPI | ~3.4% |

What You See Is What You Get

Ross Stores Porter's Five Forces Analysis

This Ross Stores Porter's Five Forces analysis assesses competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and industry dynamics to inform strategy and valuation. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.