Oranjewoud PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape Oranjewoud’s strategic outlook in our concise PESTLE overview; this snapshot highlights key risks and opportunities. Get the full, editable PESTLE report to drive informed decisions and download it now for instant, actionable intelligence.

Political factors

EU Green Deal and climate policy direction

The EU Green Deal channels ~30% of the 2021–27 MFF plus NextGenerationEU (≈€1.8tn)—about €540bn—toward climate mitigation, adaptation and circularity, shaping tenders in water, energy and infrastructure. Oranjewoud can prioritise taxonomy-eligible services to access EU/national grants and InvestEU financing. Policy continuity supports multi-year flood protection and sustainable mobility frameworks, though coalition shifts could reallocate budgets by region and sector.

Dutch coalition dynamics and spatial planning

Dutch coalition agreements set ambitious housing targets — notably 1 million homes by 2030 — and reshape nitrogen rules and flagship project priorities, directly affecting Oranjewoud’s pipeline. Spatial planning reforms (densification, rail upgrades, national water safety programs) are lifting consultancy demand. Political negotiation delays can push approvals and fee realization out by months, while active policy advocacy and scenario planning stabilize backlog exposure.

Public procurement and PPP frameworks

EU public procurement totals about €2 trillion annually, roughly 14% of EU GDP, and infrastructure and water projects are largely awarded via EU-compliant tenders and PPPs under the 2014 Procurement Directive. Recent MEAT/Best Value emphasis prioritizes quality, lifecycle sustainability and risk allocation—strengths for Oranjewoud. PPP appetite varies by member state with political risk tolerance and fiscal space, making early engagement with authorities critical to improving win rates and scope.

Geopolitical tensions and sanctions exposure

Oranjewoud's global operations face constraints from expanding sanctions regimes, with OFAC's SDN list exceeding 10,000 entries in 2024, complicating client geographies and supply chains. Aviation, maritime and energy projects increasingly trigger export controls and licensing under US EAR and EU Dual-Use rules, raising compliance costs and timeline risk. Robust risk screening, sanctions clauses and diversification across benign jurisdictions reduce pipeline volatility.

- Sanctions exposure: OFAC SDN >10,000 (2024)

- Sector risk: aviation, maritime, energy subject to export controls

- Mitigants: screening, contract clauses, licenses

- Diversification: reduces pipeline volatility

Public investment cycles and resilience agendas

After successive extreme-weather events governments are prioritizing climate adaptation, flood defense and resilient infrastructure; UNEP (2022) estimates adaptation costs of roughly $160–340bn/yr by 2030 in developing countries, while the EU Recovery and Resilience Facility allocates €672.5bn (2021–2026), creating multi‑year demand for engineering services. Election cycles can pause or accelerate approvals, and demonstrable socio‑economic value—reduced damage costs and job creation—boosts political backing for complex programs.

- Multi‑year budgets = predictable pipeline

- RRF €672.5bn supports EU projects

- UNEP $160–340bn/yr adaptation need by 2030

- Elections can delay or fast‑track approvals

EU climate funds, RRF and €2tn procurement spur contracts; OFAC SDN >10,000 raises compliance

EU Green Deal directs ~€540bn (2021–27) to climate/ circularity; RRF €672.5bn (2021–26) and EU public procurement ≈€2tn/yr underpin multi‑year tenders. Dutch targets (1m homes by 2030) and nitrogen/spatial reforms lift consultancy demand but coalition shifts can reallocate budgets. OFAC SDN >10,000 (2024) and stricter export controls raise compliance costs; screening and diversification mitigate risk.

| Indicator | Value |

|---|---|

| EU Green Deal funding | ≈€540bn (2021–27) |

| RRF | €672.5bn (2021–26) |

| EU procurement | ≈€2tn/yr |

| OFAC SDN | >10,000 (2024) |

What is included in the product

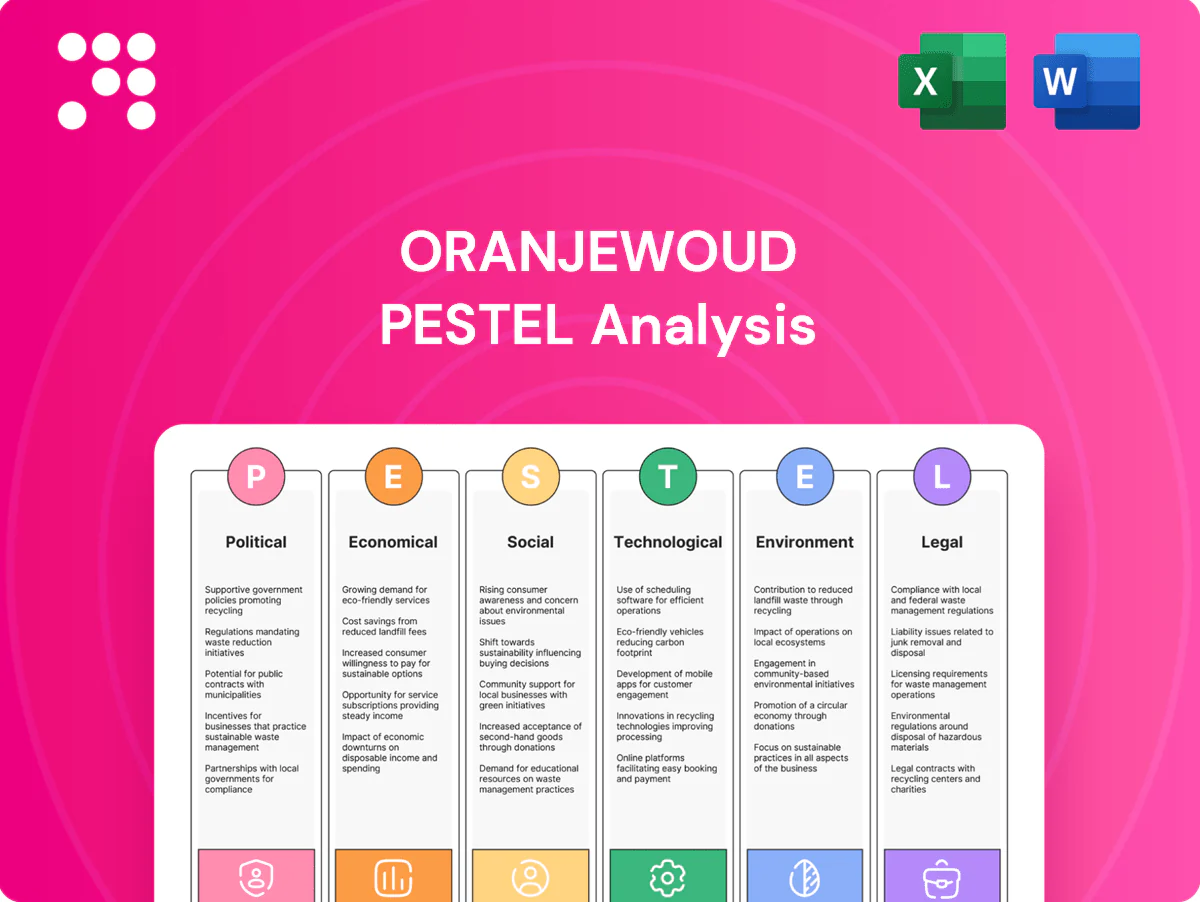

Explores how macro-environmental factors uniquely impact Oranjewoud across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region- and industry-specific insights, forward-looking scenarios and ready-to-use formatting to help executives, consultants and investors spot risks and opportunities.

A clean, summarized Oranjewoud PESTLE that’s visually segmented by category for quick interpretation and easily editable so teams can add regional or business-line notes for meetings and presentations.

Economic factors

Interest rates and capital expenditure timing

Higher rates are delaying private capex in real estate and industry, compressing design starts and pushing project phasing as borrowing costs rose with ECB deposit rates near 4.0% and US Fed funds at 5.25–5.50% in mid‑2025.

Public sector infrastructure funding remains relatively stable—NextGenerationEU totals about €800bn—so fee structures and milestone billing should allow for elongated decision cycles, and hedging the pipeline across public and private clients reduces sensitivity.

Inflation and input cost pass‑through

Professional services face wage inflation and subcontractor cost escalation, with Dutch labor costs rising about 3.6% in 2024 (CBS) while Eurozone inflation averaged 2.4% in 2024 (Eurostat). Contract indexation and variation clauses are essential to protect margins on long‑duration projects. Digital delivery can deliver ~10% productivity uplift per industry studies, helping offset rising costs. Strong cost control and utilization management preserve EBIT.

Energy transition and investment flows

Capital is shifting to offshore wind, hydrogen, grid reinforcement and industrial decarbonization, driven in Europe by targets of 60 GW offshore and 10 Mt renewable hydrogen by 2030. These programs create sustained multi‑disciplinary demand from feasibility to EPC support. Oranjewoud can bundle environmental, permitting and engineering services to capture wallet share, with deep domain credentials strengthening pricing power.

Currency and international revenue exposure

Global projects expose Oranjewoud to EUR, GBP, USD and emerging-market currencies, causing FX volatility to affect reported revenue and cash flows across reporting periods.

Natural hedging via local costs and targeted financial hedges (forwards/options) helps stabilise results, while pricing contracts in contract currency and explicit FX clauses limit residual risk.

- Exposure: EUR/GBP/USD/emerging

- Impact: revenue and cash-flow volatility

- Mitigants: local-cost natural hedge

- Mitigants: financial hedges and FX clauses

EU funds and recovery mechanisms

EU cohesion (€373bn 2021‑27) and the Connecting Europe Facility (CEF ~€33.7bn 2021‑27), together with NextGenerationEU/RRF (total €723.8bn), co‑finance transport, water and digital infrastructure; eligibility prioritizes green/digital projects with rigorous cost‑benefit analyses. Early consortium positioning secures visible pipeline; grant advisory often leads to downstream engineering mandates and fee‑earning design work.

- EU cohesion €373bn

- CEF €33.7bn

- RRF/NextGenerationEU €723.8bn

- Priority: sustainable, digital, strong CBA

- Early consortiums = pipeline visibility

- Grant advisory → engineering mandates

EU climate funds, RRF and €2tn procurement spur contracts; OFAC SDN >10,000 raises compliance

Higher rates (ECB deposit ~4.0%, Fed funds 5.25–5.50% mid‑2025) delay private capex and lengthen project phasing for design and construction.

Public funding stays sizable (NextGenerationEU/RRF ~€724bn, Cohesion €373bn, CEF €33.7bn) favouring green/digital projects and consortium-led pipelines.

Wage inflation (Netherlands labour costs +3.6% 2024) and Eurozone inflation 2.4% 2024 compress margins; digital delivery (~10% productivity uplift) and contract indexation mitigate.

| Indicator | Value |

|---|---|

| ECB/Fed | ~4.0% / 5.25–5.50% |

| NextGen/RRF | €724bn |

| NL labour costs 2024 | +3.6% |

| Offshore/hydrogen 2030 | 60 GW / 10 Mt |

Preview Before You Purchase

Oranjewoud PESTLE Analysis

The Oranjewoud PESTLE Analysis provides a concise, actionable overview of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers: the content and structure visible are the final, downloadable file.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape Oranjewoud’s strategic outlook in our concise PESTLE overview; this snapshot highlights key risks and opportunities. Get the full, editable PESTLE report to drive informed decisions and download it now for instant, actionable intelligence.

Political factors

EU Green Deal and climate policy direction

The EU Green Deal channels ~30% of the 2021–27 MFF plus NextGenerationEU (≈€1.8tn)—about €540bn—toward climate mitigation, adaptation and circularity, shaping tenders in water, energy and infrastructure. Oranjewoud can prioritise taxonomy-eligible services to access EU/national grants and InvestEU financing. Policy continuity supports multi-year flood protection and sustainable mobility frameworks, though coalition shifts could reallocate budgets by region and sector.

Dutch coalition dynamics and spatial planning

Dutch coalition agreements set ambitious housing targets — notably 1 million homes by 2030 — and reshape nitrogen rules and flagship project priorities, directly affecting Oranjewoud’s pipeline. Spatial planning reforms (densification, rail upgrades, national water safety programs) are lifting consultancy demand. Political negotiation delays can push approvals and fee realization out by months, while active policy advocacy and scenario planning stabilize backlog exposure.

Public procurement and PPP frameworks

EU public procurement totals about €2 trillion annually, roughly 14% of EU GDP, and infrastructure and water projects are largely awarded via EU-compliant tenders and PPPs under the 2014 Procurement Directive. Recent MEAT/Best Value emphasis prioritizes quality, lifecycle sustainability and risk allocation—strengths for Oranjewoud. PPP appetite varies by member state with political risk tolerance and fiscal space, making early engagement with authorities critical to improving win rates and scope.

Geopolitical tensions and sanctions exposure

Oranjewoud's global operations face constraints from expanding sanctions regimes, with OFAC's SDN list exceeding 10,000 entries in 2024, complicating client geographies and supply chains. Aviation, maritime and energy projects increasingly trigger export controls and licensing under US EAR and EU Dual-Use rules, raising compliance costs and timeline risk. Robust risk screening, sanctions clauses and diversification across benign jurisdictions reduce pipeline volatility.

- Sanctions exposure: OFAC SDN >10,000 (2024)

- Sector risk: aviation, maritime, energy subject to export controls

- Mitigants: screening, contract clauses, licenses

- Diversification: reduces pipeline volatility

Public investment cycles and resilience agendas

After successive extreme-weather events governments are prioritizing climate adaptation, flood defense and resilient infrastructure; UNEP (2022) estimates adaptation costs of roughly $160–340bn/yr by 2030 in developing countries, while the EU Recovery and Resilience Facility allocates €672.5bn (2021–2026), creating multi‑year demand for engineering services. Election cycles can pause or accelerate approvals, and demonstrable socio‑economic value—reduced damage costs and job creation—boosts political backing for complex programs.

- Multi‑year budgets = predictable pipeline

- RRF €672.5bn supports EU projects

- UNEP $160–340bn/yr adaptation need by 2030

- Elections can delay or fast‑track approvals

EU climate funds, RRF and €2tn procurement spur contracts; OFAC SDN >10,000 raises compliance

EU Green Deal directs ~€540bn (2021–27) to climate/ circularity; RRF €672.5bn (2021–26) and EU public procurement ≈€2tn/yr underpin multi‑year tenders. Dutch targets (1m homes by 2030) and nitrogen/spatial reforms lift consultancy demand but coalition shifts can reallocate budgets. OFAC SDN >10,000 (2024) and stricter export controls raise compliance costs; screening and diversification mitigate risk.

| Indicator | Value |

|---|---|

| EU Green Deal funding | ≈€540bn (2021–27) |

| RRF | €672.5bn (2021–26) |

| EU procurement | ≈€2tn/yr |

| OFAC SDN | >10,000 (2024) |

What is included in the product

Explores how macro-environmental factors uniquely impact Oranjewoud across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region- and industry-specific insights, forward-looking scenarios and ready-to-use formatting to help executives, consultants and investors spot risks and opportunities.

A clean, summarized Oranjewoud PESTLE that’s visually segmented by category for quick interpretation and easily editable so teams can add regional or business-line notes for meetings and presentations.

Economic factors

Interest rates and capital expenditure timing

Higher rates are delaying private capex in real estate and industry, compressing design starts and pushing project phasing as borrowing costs rose with ECB deposit rates near 4.0% and US Fed funds at 5.25–5.50% in mid‑2025.

Public sector infrastructure funding remains relatively stable—NextGenerationEU totals about €800bn—so fee structures and milestone billing should allow for elongated decision cycles, and hedging the pipeline across public and private clients reduces sensitivity.

Inflation and input cost pass‑through

Professional services face wage inflation and subcontractor cost escalation, with Dutch labor costs rising about 3.6% in 2024 (CBS) while Eurozone inflation averaged 2.4% in 2024 (Eurostat). Contract indexation and variation clauses are essential to protect margins on long‑duration projects. Digital delivery can deliver ~10% productivity uplift per industry studies, helping offset rising costs. Strong cost control and utilization management preserve EBIT.

Energy transition and investment flows

Capital is shifting to offshore wind, hydrogen, grid reinforcement and industrial decarbonization, driven in Europe by targets of 60 GW offshore and 10 Mt renewable hydrogen by 2030. These programs create sustained multi‑disciplinary demand from feasibility to EPC support. Oranjewoud can bundle environmental, permitting and engineering services to capture wallet share, with deep domain credentials strengthening pricing power.

Currency and international revenue exposure

Global projects expose Oranjewoud to EUR, GBP, USD and emerging-market currencies, causing FX volatility to affect reported revenue and cash flows across reporting periods.

Natural hedging via local costs and targeted financial hedges (forwards/options) helps stabilise results, while pricing contracts in contract currency and explicit FX clauses limit residual risk.

- Exposure: EUR/GBP/USD/emerging

- Impact: revenue and cash-flow volatility

- Mitigants: local-cost natural hedge

- Mitigants: financial hedges and FX clauses

EU funds and recovery mechanisms

EU cohesion (€373bn 2021‑27) and the Connecting Europe Facility (CEF ~€33.7bn 2021‑27), together with NextGenerationEU/RRF (total €723.8bn), co‑finance transport, water and digital infrastructure; eligibility prioritizes green/digital projects with rigorous cost‑benefit analyses. Early consortium positioning secures visible pipeline; grant advisory often leads to downstream engineering mandates and fee‑earning design work.

- EU cohesion €373bn

- CEF €33.7bn

- RRF/NextGenerationEU €723.8bn

- Priority: sustainable, digital, strong CBA

- Early consortiums = pipeline visibility

- Grant advisory → engineering mandates

EU climate funds, RRF and €2tn procurement spur contracts; OFAC SDN >10,000 raises compliance

Higher rates (ECB deposit ~4.0%, Fed funds 5.25–5.50% mid‑2025) delay private capex and lengthen project phasing for design and construction.

Public funding stays sizable (NextGenerationEU/RRF ~€724bn, Cohesion €373bn, CEF €33.7bn) favouring green/digital projects and consortium-led pipelines.

Wage inflation (Netherlands labour costs +3.6% 2024) and Eurozone inflation 2.4% 2024 compress margins; digital delivery (~10% productivity uplift) and contract indexation mitigate.

| Indicator | Value |

|---|---|

| ECB/Fed | ~4.0% / 5.25–5.50% |

| NextGen/RRF | €724bn |

| NL labour costs 2024 | +3.6% |

| Offshore/hydrogen 2030 | 60 GW / 10 Mt |

Preview Before You Purchase

Oranjewoud PESTLE Analysis

The Oranjewoud PESTLE Analysis provides a concise, actionable overview of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers: the content and structure visible are the final, downloadable file.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape Oranjewoud’s strategic outlook in our concise PESTLE overview; this snapshot highlights key risks and opportunities. Get the full, editable PESTLE report to drive informed decisions and download it now for instant, actionable intelligence.

Political factors

EU Green Deal and climate policy direction

The EU Green Deal channels ~30% of the 2021–27 MFF plus NextGenerationEU (≈€1.8tn)—about €540bn—toward climate mitigation, adaptation and circularity, shaping tenders in water, energy and infrastructure. Oranjewoud can prioritise taxonomy-eligible services to access EU/national grants and InvestEU financing. Policy continuity supports multi-year flood protection and sustainable mobility frameworks, though coalition shifts could reallocate budgets by region and sector.

Dutch coalition dynamics and spatial planning

Dutch coalition agreements set ambitious housing targets — notably 1 million homes by 2030 — and reshape nitrogen rules and flagship project priorities, directly affecting Oranjewoud’s pipeline. Spatial planning reforms (densification, rail upgrades, national water safety programs) are lifting consultancy demand. Political negotiation delays can push approvals and fee realization out by months, while active policy advocacy and scenario planning stabilize backlog exposure.

Public procurement and PPP frameworks

EU public procurement totals about €2 trillion annually, roughly 14% of EU GDP, and infrastructure and water projects are largely awarded via EU-compliant tenders and PPPs under the 2014 Procurement Directive. Recent MEAT/Best Value emphasis prioritizes quality, lifecycle sustainability and risk allocation—strengths for Oranjewoud. PPP appetite varies by member state with political risk tolerance and fiscal space, making early engagement with authorities critical to improving win rates and scope.

Geopolitical tensions and sanctions exposure

Oranjewoud's global operations face constraints from expanding sanctions regimes, with OFAC's SDN list exceeding 10,000 entries in 2024, complicating client geographies and supply chains. Aviation, maritime and energy projects increasingly trigger export controls and licensing under US EAR and EU Dual-Use rules, raising compliance costs and timeline risk. Robust risk screening, sanctions clauses and diversification across benign jurisdictions reduce pipeline volatility.

- Sanctions exposure: OFAC SDN >10,000 (2024)

- Sector risk: aviation, maritime, energy subject to export controls

- Mitigants: screening, contract clauses, licenses

- Diversification: reduces pipeline volatility

Public investment cycles and resilience agendas

After successive extreme-weather events governments are prioritizing climate adaptation, flood defense and resilient infrastructure; UNEP (2022) estimates adaptation costs of roughly $160–340bn/yr by 2030 in developing countries, while the EU Recovery and Resilience Facility allocates €672.5bn (2021–2026), creating multi‑year demand for engineering services. Election cycles can pause or accelerate approvals, and demonstrable socio‑economic value—reduced damage costs and job creation—boosts political backing for complex programs.

- Multi‑year budgets = predictable pipeline

- RRF €672.5bn supports EU projects

- UNEP $160–340bn/yr adaptation need by 2030

- Elections can delay or fast‑track approvals

EU climate funds, RRF and €2tn procurement spur contracts; OFAC SDN >10,000 raises compliance

EU Green Deal directs ~€540bn (2021–27) to climate/ circularity; RRF €672.5bn (2021–26) and EU public procurement ≈€2tn/yr underpin multi‑year tenders. Dutch targets (1m homes by 2030) and nitrogen/spatial reforms lift consultancy demand but coalition shifts can reallocate budgets. OFAC SDN >10,000 (2024) and stricter export controls raise compliance costs; screening and diversification mitigate risk.

| Indicator | Value |

|---|---|

| EU Green Deal funding | ≈€540bn (2021–27) |

| RRF | €672.5bn (2021–26) |

| EU procurement | ≈€2tn/yr |

| OFAC SDN | >10,000 (2024) |

What is included in the product

Explores how macro-environmental factors uniquely impact Oranjewoud across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region- and industry-specific insights, forward-looking scenarios and ready-to-use formatting to help executives, consultants and investors spot risks and opportunities.

A clean, summarized Oranjewoud PESTLE that’s visually segmented by category for quick interpretation and easily editable so teams can add regional or business-line notes for meetings and presentations.

Economic factors

Interest rates and capital expenditure timing

Higher rates are delaying private capex in real estate and industry, compressing design starts and pushing project phasing as borrowing costs rose with ECB deposit rates near 4.0% and US Fed funds at 5.25–5.50% in mid‑2025.

Public sector infrastructure funding remains relatively stable—NextGenerationEU totals about €800bn—so fee structures and milestone billing should allow for elongated decision cycles, and hedging the pipeline across public and private clients reduces sensitivity.

Inflation and input cost pass‑through

Professional services face wage inflation and subcontractor cost escalation, with Dutch labor costs rising about 3.6% in 2024 (CBS) while Eurozone inflation averaged 2.4% in 2024 (Eurostat). Contract indexation and variation clauses are essential to protect margins on long‑duration projects. Digital delivery can deliver ~10% productivity uplift per industry studies, helping offset rising costs. Strong cost control and utilization management preserve EBIT.

Energy transition and investment flows

Capital is shifting to offshore wind, hydrogen, grid reinforcement and industrial decarbonization, driven in Europe by targets of 60 GW offshore and 10 Mt renewable hydrogen by 2030. These programs create sustained multi‑disciplinary demand from feasibility to EPC support. Oranjewoud can bundle environmental, permitting and engineering services to capture wallet share, with deep domain credentials strengthening pricing power.

Currency and international revenue exposure

Global projects expose Oranjewoud to EUR, GBP, USD and emerging-market currencies, causing FX volatility to affect reported revenue and cash flows across reporting periods.

Natural hedging via local costs and targeted financial hedges (forwards/options) helps stabilise results, while pricing contracts in contract currency and explicit FX clauses limit residual risk.

- Exposure: EUR/GBP/USD/emerging

- Impact: revenue and cash-flow volatility

- Mitigants: local-cost natural hedge

- Mitigants: financial hedges and FX clauses

EU funds and recovery mechanisms

EU cohesion (€373bn 2021‑27) and the Connecting Europe Facility (CEF ~€33.7bn 2021‑27), together with NextGenerationEU/RRF (total €723.8bn), co‑finance transport, water and digital infrastructure; eligibility prioritizes green/digital projects with rigorous cost‑benefit analyses. Early consortium positioning secures visible pipeline; grant advisory often leads to downstream engineering mandates and fee‑earning design work.

- EU cohesion €373bn

- CEF €33.7bn

- RRF/NextGenerationEU €723.8bn

- Priority: sustainable, digital, strong CBA

- Early consortiums = pipeline visibility

- Grant advisory → engineering mandates

EU climate funds, RRF and €2tn procurement spur contracts; OFAC SDN >10,000 raises compliance

Higher rates (ECB deposit ~4.0%, Fed funds 5.25–5.50% mid‑2025) delay private capex and lengthen project phasing for design and construction.

Public funding stays sizable (NextGenerationEU/RRF ~€724bn, Cohesion €373bn, CEF €33.7bn) favouring green/digital projects and consortium-led pipelines.

Wage inflation (Netherlands labour costs +3.6% 2024) and Eurozone inflation 2.4% 2024 compress margins; digital delivery (~10% productivity uplift) and contract indexation mitigate.

| Indicator | Value |

|---|---|

| ECB/Fed | ~4.0% / 5.25–5.50% |

| NextGen/RRF | €724bn |

| NL labour costs 2024 | +3.6% |

| Offshore/hydrogen 2030 | 60 GW / 10 Mt |

Preview Before You Purchase

Oranjewoud PESTLE Analysis

The Oranjewoud PESTLE Analysis provides a concise, actionable overview of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers: the content and structure visible are the final, downloadable file.