Reliance Steel Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Reliance Steel faces varied pressures—from concentrated supplier relationships and cyclical steel demand to moderate buyer leverage and evolving substitution risks—impacting margins and growth prospects. This snapshot highlights strategic vulnerabilities and strengths but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Reliance Steel.

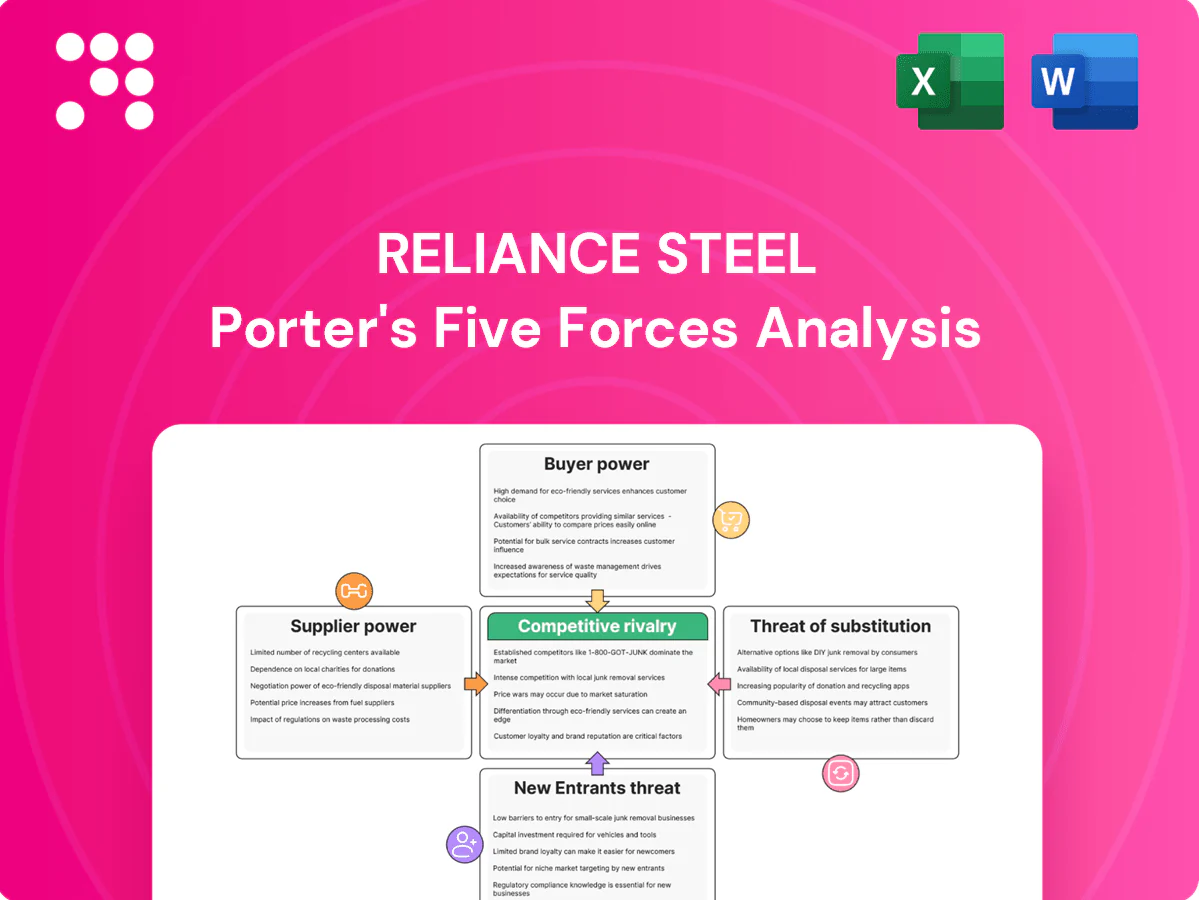

Suppliers Bargaining Power

Specialty mill concentration

In 2024 aerospace and high-spec alloys largely originate from a limited set of NADCAP and AS9100-qualified mills, concentrating supplier power and narrowing alternatives for Reliance. Maintaining approvals raises switching costs and can compress margins in tight markets. Reliance mitigates this by diversifying approved mills and using long-term supply agreements to stabilize access and pricing.

Scale-based purchasing leverage

Reliance Steel, with revenue of about $16.7 billion in FY2024 and 300+ service centers across 40 states and 12 countries, uses large volumes across metals and regions to secure price and allocation leverage. Aggregated buys, demand forecasting and vendor scorecards drive improved terms and rebates. In downcycles size wins better mill runs; in upcycles it secures priority allocation, partially offsetting supplier concentration.

Commodity price pass-through

In 2024 mill surcharges and base-price moves were largely passed through via indexed pricing, allowing Reliance Steel to neutralize much supplier pressure. Timing mismatches still create margin exposure on rapid spikes or drops, especially during volatile months. Active hedging programs and rapid inventory turnover reduced that risk. Overall, these pass-through mechanisms materially temper supplier bargaining power.

Logistics and energy exposure

Freight capacity constraints, port congestion and higher energy costs materially raise Reliance Steel’s effective inbound costs; carriers and utilities exert episodic supplier leverage during tight cycles. Multi-modal routing and a distributed plant footprint reduce single-node dependency, but port or fuel shocks can rapidly tighten supply and lift inbound landed costs.

- Freight capacity: episodic leverage

- Port congestion: increases lead times

- Energy prices: raise input and transport costs

- Mitigation: multimodal + distributed footprint

Quality and certification lock-ins

Certification bottlenecks raise supplier risk; $16.7B scale and indexed pricing mitigate

Supplier power is moderate: reliance on NADCAP/AS9100 mills and 6–18 month re-qualification windows raise concentration risk for aerospace/high-spec alloys, but indexed pass-through pricing and hedging offset base-price exposure. Scale (≈$16.7B revenue, ~320 service centers in 2024) and long-term agreements secure allocation and rebates, while freight/energy shocks create episodic leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Revenue | $16.7B | Purchasing leverage |

| Service centers | ≈320 | Negotiation credibility |

| Re-qualification | 6–18 months | Supplier stickiness |

What is included in the product

Tailored Porter's Five Forces assessment of Reliance Steel uncovers competitive intensity, buyer and supplier bargaining power, substitution risks, and entry barriers shaping profit margins. The analysis identifies disruptive threats, pricing pressures, and strategic defenses that protect Reliance Steel’s market position and informs investment and strategic decisions.

Concise one-sheet Porter's Five Forces for Reliance Steel—quickly highlights supplier/buyer power, competitive rivalry, substitutes, and entry threats to simplify strategic decisions and boardroom briefings.

Customers Bargaining Power

Diverse customer mix

Reliance serves aerospace, automotive, construction, energy and semiconductor customers and reports serving over 125,000 customers, reducing reliance on any single buyer.

This wide end-market spread limits concentration-driven bargaining power by preventing large-account dependence and allowing cyclical offsets to soften demand shocks between sectors.

Portfolio breadth and scale dampen price pressure from individual customers and support stronger margin negotiation across cycles.

Value-added processing

Cutting, precision sawing, machining and kitting embed service value beyond metal price, with value-added processing representing roughly 40% of service-center revenue and helping Reliance Steel capture $16.7 billion in FY2024 net sales. These services raise switching costs and reduce pure price shopping as customers lock in specifications and inventory routines. Tight tolerances and JIT delivery integrate into customer workflows, so buyers pay for reliability and processing consistency, not just commodity metal.

Large OEM negotiation

Large aerospace and auto OEMs demand aggressive pricing and strict SLAs, forcing Reliance Steel to compete on cost and service; Reliance Steel reported approximately $14.4 billion in net sales in 2023, underscoring scale but margin pressure. OEMs commonly dual-source to retain leverage, while multi-year agreements provide volume visibility yet compress margins. Meeting performance metrics and OTIF targets above 95% is critical to retain share.

Lead-time and availability

When mills are tight Reliance’s inventory breadth across over 300 service centers and roughly $3.6 billion in inventory (2024) reduces buyer power as availability often trumps price; in soft markets buyers secure discounts and flexible terms. Short lead-time fulfillment creates defensibility, and differentiated service levels counter pure price leverage.

- over 300 locations

- $3.6B inventory (2024)

- short lead times = defensibility

- service > price in tight markets

Spec and certification needs

End-use certifications and strict traceability—notably ISO 9001 and AS9100 in 2024—bind buyers to qualified distributors, making certified service centers like Reliance Steel preferred partners. Documentation accuracy and lot integrity are mandatory in regulated industries, lowering practical substitutability among service centers. Errors or mis-traceability create high buyer risk, favoring trusted, certified suppliers.

- Certifications: ISO 9001, AS9100

- Traceability: mandatory lot integrity

- Buyer risk: errors favor trusted partners

Scale + value-added services: >125,000 customers, $3.6B inventory, $16.7B sales

Reliance serves >125,000 customers across aerospace, auto, construction and energy, reducing buyer concentration and limiting single-customer leverage. Scale—300+ service centers, $3.6B inventory (2024) and FY2024 sales $16.7B—lets Reliance resist price pressure while value-added processing (~40% revenue) raises switching costs. OEMs still exert pressure via dual-sourcing and strict SLAs (OTIF >95%). Availability and certifications (ISO 9001, AS9100) further constrain buyer bargaining.

| Metric | Value |

|---|---|

| Customers | >125,000 |

| Service centers | 300+ |

| Inventory (2024) | $3.6B |

| FY2024 Net Sales | $16.7B |

| Value-added revenue | ~40% |

Preview Before You Purchase

Reliance Steel Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Reliance Steel you'll receive—no placeholders or mockups. The document is professionally written and fully formatted, ready for immediate download after purchase. What you see here is precisely what you get.

A Must-Have Tool for Decision-Makers

Reliance Steel faces varied pressures—from concentrated supplier relationships and cyclical steel demand to moderate buyer leverage and evolving substitution risks—impacting margins and growth prospects. This snapshot highlights strategic vulnerabilities and strengths but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Reliance Steel.

Suppliers Bargaining Power

Specialty mill concentration

In 2024 aerospace and high-spec alloys largely originate from a limited set of NADCAP and AS9100-qualified mills, concentrating supplier power and narrowing alternatives for Reliance. Maintaining approvals raises switching costs and can compress margins in tight markets. Reliance mitigates this by diversifying approved mills and using long-term supply agreements to stabilize access and pricing.

Scale-based purchasing leverage

Reliance Steel, with revenue of about $16.7 billion in FY2024 and 300+ service centers across 40 states and 12 countries, uses large volumes across metals and regions to secure price and allocation leverage. Aggregated buys, demand forecasting and vendor scorecards drive improved terms and rebates. In downcycles size wins better mill runs; in upcycles it secures priority allocation, partially offsetting supplier concentration.

Commodity price pass-through

In 2024 mill surcharges and base-price moves were largely passed through via indexed pricing, allowing Reliance Steel to neutralize much supplier pressure. Timing mismatches still create margin exposure on rapid spikes or drops, especially during volatile months. Active hedging programs and rapid inventory turnover reduced that risk. Overall, these pass-through mechanisms materially temper supplier bargaining power.

Logistics and energy exposure

Freight capacity constraints, port congestion and higher energy costs materially raise Reliance Steel’s effective inbound costs; carriers and utilities exert episodic supplier leverage during tight cycles. Multi-modal routing and a distributed plant footprint reduce single-node dependency, but port or fuel shocks can rapidly tighten supply and lift inbound landed costs.

- Freight capacity: episodic leverage

- Port congestion: increases lead times

- Energy prices: raise input and transport costs

- Mitigation: multimodal + distributed footprint

Quality and certification lock-ins

Certification bottlenecks raise supplier risk; $16.7B scale and indexed pricing mitigate

Supplier power is moderate: reliance on NADCAP/AS9100 mills and 6–18 month re-qualification windows raise concentration risk for aerospace/high-spec alloys, but indexed pass-through pricing and hedging offset base-price exposure. Scale (≈$16.7B revenue, ~320 service centers in 2024) and long-term agreements secure allocation and rebates, while freight/energy shocks create episodic leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Revenue | $16.7B | Purchasing leverage |

| Service centers | ≈320 | Negotiation credibility |

| Re-qualification | 6–18 months | Supplier stickiness |

What is included in the product

Tailored Porter's Five Forces assessment of Reliance Steel uncovers competitive intensity, buyer and supplier bargaining power, substitution risks, and entry barriers shaping profit margins. The analysis identifies disruptive threats, pricing pressures, and strategic defenses that protect Reliance Steel’s market position and informs investment and strategic decisions.

Concise one-sheet Porter's Five Forces for Reliance Steel—quickly highlights supplier/buyer power, competitive rivalry, substitutes, and entry threats to simplify strategic decisions and boardroom briefings.

Customers Bargaining Power

Diverse customer mix

Reliance serves aerospace, automotive, construction, energy and semiconductor customers and reports serving over 125,000 customers, reducing reliance on any single buyer.

This wide end-market spread limits concentration-driven bargaining power by preventing large-account dependence and allowing cyclical offsets to soften demand shocks between sectors.

Portfolio breadth and scale dampen price pressure from individual customers and support stronger margin negotiation across cycles.

Value-added processing

Cutting, precision sawing, machining and kitting embed service value beyond metal price, with value-added processing representing roughly 40% of service-center revenue and helping Reliance Steel capture $16.7 billion in FY2024 net sales. These services raise switching costs and reduce pure price shopping as customers lock in specifications and inventory routines. Tight tolerances and JIT delivery integrate into customer workflows, so buyers pay for reliability and processing consistency, not just commodity metal.

Large OEM negotiation

Large aerospace and auto OEMs demand aggressive pricing and strict SLAs, forcing Reliance Steel to compete on cost and service; Reliance Steel reported approximately $14.4 billion in net sales in 2023, underscoring scale but margin pressure. OEMs commonly dual-source to retain leverage, while multi-year agreements provide volume visibility yet compress margins. Meeting performance metrics and OTIF targets above 95% is critical to retain share.

Lead-time and availability

When mills are tight Reliance’s inventory breadth across over 300 service centers and roughly $3.6 billion in inventory (2024) reduces buyer power as availability often trumps price; in soft markets buyers secure discounts and flexible terms. Short lead-time fulfillment creates defensibility, and differentiated service levels counter pure price leverage.

- over 300 locations

- $3.6B inventory (2024)

- short lead times = defensibility

- service > price in tight markets

Spec and certification needs

End-use certifications and strict traceability—notably ISO 9001 and AS9100 in 2024—bind buyers to qualified distributors, making certified service centers like Reliance Steel preferred partners. Documentation accuracy and lot integrity are mandatory in regulated industries, lowering practical substitutability among service centers. Errors or mis-traceability create high buyer risk, favoring trusted, certified suppliers.

- Certifications: ISO 9001, AS9100

- Traceability: mandatory lot integrity

- Buyer risk: errors favor trusted partners

Scale + value-added services: >125,000 customers, $3.6B inventory, $16.7B sales

Reliance serves >125,000 customers across aerospace, auto, construction and energy, reducing buyer concentration and limiting single-customer leverage. Scale—300+ service centers, $3.6B inventory (2024) and FY2024 sales $16.7B—lets Reliance resist price pressure while value-added processing (~40% revenue) raises switching costs. OEMs still exert pressure via dual-sourcing and strict SLAs (OTIF >95%). Availability and certifications (ISO 9001, AS9100) further constrain buyer bargaining.

| Metric | Value |

|---|---|

| Customers | >125,000 |

| Service centers | 300+ |

| Inventory (2024) | $3.6B |

| FY2024 Net Sales | $16.7B |

| Value-added revenue | ~40% |

Preview Before You Purchase

Reliance Steel Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Reliance Steel you'll receive—no placeholders or mockups. The document is professionally written and fully formatted, ready for immediate download after purchase. What you see here is precisely what you get.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Reliance Steel faces varied pressures—from concentrated supplier relationships and cyclical steel demand to moderate buyer leverage and evolving substitution risks—impacting margins and growth prospects. This snapshot highlights strategic vulnerabilities and strengths but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Reliance Steel.

Suppliers Bargaining Power

Specialty mill concentration

In 2024 aerospace and high-spec alloys largely originate from a limited set of NADCAP and AS9100-qualified mills, concentrating supplier power and narrowing alternatives for Reliance. Maintaining approvals raises switching costs and can compress margins in tight markets. Reliance mitigates this by diversifying approved mills and using long-term supply agreements to stabilize access and pricing.

Scale-based purchasing leverage

Reliance Steel, with revenue of about $16.7 billion in FY2024 and 300+ service centers across 40 states and 12 countries, uses large volumes across metals and regions to secure price and allocation leverage. Aggregated buys, demand forecasting and vendor scorecards drive improved terms and rebates. In downcycles size wins better mill runs; in upcycles it secures priority allocation, partially offsetting supplier concentration.

Commodity price pass-through

In 2024 mill surcharges and base-price moves were largely passed through via indexed pricing, allowing Reliance Steel to neutralize much supplier pressure. Timing mismatches still create margin exposure on rapid spikes or drops, especially during volatile months. Active hedging programs and rapid inventory turnover reduced that risk. Overall, these pass-through mechanisms materially temper supplier bargaining power.

Logistics and energy exposure

Freight capacity constraints, port congestion and higher energy costs materially raise Reliance Steel’s effective inbound costs; carriers and utilities exert episodic supplier leverage during tight cycles. Multi-modal routing and a distributed plant footprint reduce single-node dependency, but port or fuel shocks can rapidly tighten supply and lift inbound landed costs.

- Freight capacity: episodic leverage

- Port congestion: increases lead times

- Energy prices: raise input and transport costs

- Mitigation: multimodal + distributed footprint

Quality and certification lock-ins

Certification bottlenecks raise supplier risk; $16.7B scale and indexed pricing mitigate

Supplier power is moderate: reliance on NADCAP/AS9100 mills and 6–18 month re-qualification windows raise concentration risk for aerospace/high-spec alloys, but indexed pass-through pricing and hedging offset base-price exposure. Scale (≈$16.7B revenue, ~320 service centers in 2024) and long-term agreements secure allocation and rebates, while freight/energy shocks create episodic leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Revenue | $16.7B | Purchasing leverage |

| Service centers | ≈320 | Negotiation credibility |

| Re-qualification | 6–18 months | Supplier stickiness |

What is included in the product

Tailored Porter's Five Forces assessment of Reliance Steel uncovers competitive intensity, buyer and supplier bargaining power, substitution risks, and entry barriers shaping profit margins. The analysis identifies disruptive threats, pricing pressures, and strategic defenses that protect Reliance Steel’s market position and informs investment and strategic decisions.

Concise one-sheet Porter's Five Forces for Reliance Steel—quickly highlights supplier/buyer power, competitive rivalry, substitutes, and entry threats to simplify strategic decisions and boardroom briefings.

Customers Bargaining Power

Diverse customer mix

Reliance serves aerospace, automotive, construction, energy and semiconductor customers and reports serving over 125,000 customers, reducing reliance on any single buyer.

This wide end-market spread limits concentration-driven bargaining power by preventing large-account dependence and allowing cyclical offsets to soften demand shocks between sectors.

Portfolio breadth and scale dampen price pressure from individual customers and support stronger margin negotiation across cycles.

Value-added processing

Cutting, precision sawing, machining and kitting embed service value beyond metal price, with value-added processing representing roughly 40% of service-center revenue and helping Reliance Steel capture $16.7 billion in FY2024 net sales. These services raise switching costs and reduce pure price shopping as customers lock in specifications and inventory routines. Tight tolerances and JIT delivery integrate into customer workflows, so buyers pay for reliability and processing consistency, not just commodity metal.

Large OEM negotiation

Large aerospace and auto OEMs demand aggressive pricing and strict SLAs, forcing Reliance Steel to compete on cost and service; Reliance Steel reported approximately $14.4 billion in net sales in 2023, underscoring scale but margin pressure. OEMs commonly dual-source to retain leverage, while multi-year agreements provide volume visibility yet compress margins. Meeting performance metrics and OTIF targets above 95% is critical to retain share.

Lead-time and availability

When mills are tight Reliance’s inventory breadth across over 300 service centers and roughly $3.6 billion in inventory (2024) reduces buyer power as availability often trumps price; in soft markets buyers secure discounts and flexible terms. Short lead-time fulfillment creates defensibility, and differentiated service levels counter pure price leverage.

- over 300 locations

- $3.6B inventory (2024)

- short lead times = defensibility

- service > price in tight markets

Spec and certification needs

End-use certifications and strict traceability—notably ISO 9001 and AS9100 in 2024—bind buyers to qualified distributors, making certified service centers like Reliance Steel preferred partners. Documentation accuracy and lot integrity are mandatory in regulated industries, lowering practical substitutability among service centers. Errors or mis-traceability create high buyer risk, favoring trusted, certified suppliers.

- Certifications: ISO 9001, AS9100

- Traceability: mandatory lot integrity

- Buyer risk: errors favor trusted partners

Scale + value-added services: >125,000 customers, $3.6B inventory, $16.7B sales

Reliance serves >125,000 customers across aerospace, auto, construction and energy, reducing buyer concentration and limiting single-customer leverage. Scale—300+ service centers, $3.6B inventory (2024) and FY2024 sales $16.7B—lets Reliance resist price pressure while value-added processing (~40% revenue) raises switching costs. OEMs still exert pressure via dual-sourcing and strict SLAs (OTIF >95%). Availability and certifications (ISO 9001, AS9100) further constrain buyer bargaining.

| Metric | Value |

|---|---|

| Customers | >125,000 |

| Service centers | 300+ |

| Inventory (2024) | $3.6B |

| FY2024 Net Sales | $16.7B |

| Value-added revenue | ~40% |

Preview Before You Purchase

Reliance Steel Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Reliance Steel you'll receive—no placeholders or mockups. The document is professionally written and fully formatted, ready for immediate download after purchase. What you see here is precisely what you get.