RTX Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

RTX faces complex competitive dynamics—high buyer expectations, concentrated supplier relationships, and evolving substitute threats driven by tech shifts. Our snapshot highlights key pressures on margins and innovation priorities. The full Porter's Five Forces analysis decodes each force with ratings and strategic implications to inform smarter investment and strategy decisions.

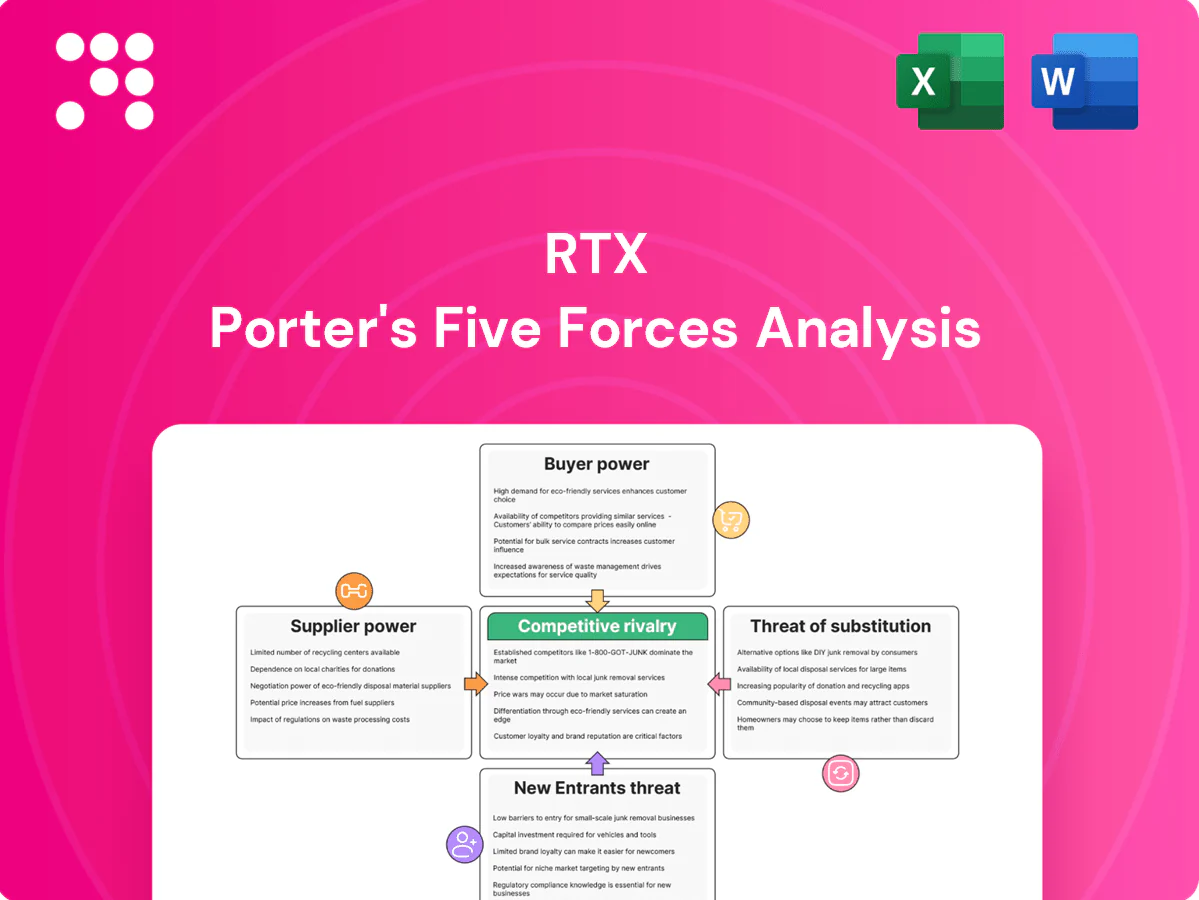

Suppliers Bargaining Power

Concentrated critical materials

RTX depends on limited suppliers for titanium, advanced alloys, rare-earth magnets and high-temp composites; China controls roughly 80% of rare-earth processing capacity (2023–24) and Russia remains a key source for titanium feedstock, raising supplier leverage and geopolitical risk. Disruptions can delay engine castings, avionics and missile components by months to over a year. Dual-sourcing reduces risk but is often infeasible for flight-critical parts.

Specialized aero components

Specialized aero castings, forgings, microelectronics and sensors are concentrated among a few qualified suppliers, creating high supplier power and limited alternatives. Qualification and requalification cycles typically span 12–24 months and often incur multi‑million‑dollar costs, raising switching barriers. Suppliers with proprietary processes therefore command stronger commercial terms, and RTX offsets risk via long‑term agreements and supplier development programs.

Certification and quality lock-in

Certification embeds specific supplier parts into Type Certificates and defense specs, so replacing a vendor often triggers FAA/EASA recertification that commonly takes 12–36 months and can incur tens to hundreds of millions of dollars in program costs. This creates structural supplier stickiness and bargaining power for approved vendors. It lengthens negotiation cycles and forces higher safety-stock and longer lead-time inventory policies for OEMs.

Capacity and lead-time constraints

Engines and defense systems rely on long-lead items with typical lead times of 6–36 months, and tight capacity in castings, chips and energetic materials gives suppliers pricing latitude; chip lead times remained >20 weeks in 2024, stressing availability during backlog recovery cycles.

- Long lead: 6–36 months

- Chips: >20 weeks in 2024

- High capacity utilization → pricing power

- RTX must early-buy and share volume visibility

Compliance and cyber requirements

Compliance regimes—ITAR, DFARS and 2024-era cybersecurity standards (NIST SP 800-171/CMMC 2.0 implementation)—shrink the qualified supplier pool for RTX, raising supplier leverage on sensitive programs. Smaller vendors often pass certification and remediation costs to primes, and non-compliance risk forces RTX to pay premiums for vetted suppliers. This dynamic elevates supplier power in classified and defense-critical work.

- ITAR/DFARS: restrict foreign/small vendor access

- CMMC/NIST 2024: increases vetting costs

- Vetted suppliers: command price premiums

Supplier concentration, long lead times and recertification drive premiums and inventory

RTX relies on few qualified suppliers for titanium, alloys and rare‑earth magnets (China ~80% processing 2023–24), giving suppliers strong leverage; dual‑sourcing often infeasible. Certification/ITAR/CMMC raises switching costs (recert 12–36 months) and forces premiums. Long leads (6–36 months) and chip lead times >20 weeks in 2024 drive early buys and higher inventory.

| Item | Metric | Impact |

|---|---|---|

| Rare‑earth | China ~80% (2023–24) | High supplier power |

| Recertification | 12–36 months | Switching cost |

| Lead times | 6–36 months | Inventory/premiums |

| Chips | >20 weeks (2024) | Availability risk |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry threats specific to RTX, detailing disruptive substitutes and strategic barriers that protect incumbents while highlighting risks to market share and profitability.

A concise, one-sheet RTX Porter's Five Forces summary that highlights supplier/buyer power, competitive rivalry, substitution and entry threats—instantly pinpointing strategic pain points and where to focus mitigation and investment decisions.

Customers Bargaining Power

Concentrated government buyers

US DoD and allied governments are extremely concentrated buyers—US DoD FY2024 budget ~ $858 billion and NATO members’ combined defense spending exceeds $1.2 trillion—driving competitive tenders that push hard on price, IP, and performance. Budget cycles, congressional audits, and program reviews increase margin pressure and contract renegotiations. Mission criticality and multiyear programs (often 5–20 years) limit abrupt price cuts, preserving predictable long-term revenue.

Commercial OEM leverage

In 2024 Boeing and Airbus retained over 90% combined share of large commercial jet platforms, giving them outsized bargaining power over avionics and subsystem suppliers like RTX. Linefit slots are commonly secured through aggressive upfront pricing and performance guarantees tied to certification and delivery milestones. Once a supplier achieves linefit, growing lifetime installed base and aftermarket spares/MRO demand steadily reduce buyer leverage. Upfront concessions are thus traded for durable, high-margin installed-base revenue streams.

Airlines and MRO dynamics

Airlines exert strong pressure for cost-effective maintenance and firm availability, driving RTX into power-by-the-hour and uptime SLA deals that transfer operational risk to the supplier while securing recurring revenue; the global commercial MRO market was about $93 billion in 2024, underlining contract scale. Independent MROs and PMA parts trimmed OEM leverage but safety, certification and reliability requirements keep switching costs high.

High switching costs and lock-in

Engines and defense systems require decades-long integration, training and tooling, with MRO and sustainment contracts commonly running 20+ years, creating high sunk costs that make mid-program vendor switches costly and risky.

Embedded software, data ecosystems and proprietary diagnostics further deepen lock-in, reducing buyer leverage once a platform and supplier are selected.

- Long-term MRO: 20+ years

- High sunk costs: tooling, training, certification

- Software/data lock-in: proprietary diagnostics and updates

- Result: reduced buyer bargaining power post-selection

Performance and availability focus

Buyers prioritize mission readiness, fuel efficiency and lifecycle cost, and superior performance can justify RTX premium pricing while reducing total cost of ownership; in 2024 global defence spending was about 2.3 trillion, keeping pressure on availability and capability. Penalties for delays and AOG events rebalance bargaining power episodically, and data-driven support services improve sortie rates and defend margin by lowering downtime and warranty costs.

- Buyers: mission readiness, lifecycle cost

- Pricing: performance enables premium

- Risk: AOG/delay penalties shift power

- Defense: data services protect margins

Defense buyers and jet duopoly lock long-term MRO and sustainment revenue

US DoD (FY2024 ~$858B) and NATO (> $1.2T) concentrate buying power, driving tough price/IP terms; Boeing+Airsbus hold >90% large-jet share, pressuring linefit pricing. Long MRO/sustainment (20+ years), high sunk costs and software lock-in reduce buyer leverage post-selection; global defense $2.3T and MRO ~$93B sustain recurring revenue and margin defense.

| Metric | 2024 Value |

|---|---|

| US DoD budget | $858B |

| NATO defense spend | >$1.2T |

| Global defense | $2.3T |

| Commercial MRO | $93B |

What You See Is What You Get

RTX Porter's Five Forces Analysis

This Porter's Five Forces analysis of RTX is the exact document you're previewing—fully formatted and ready for immediate download after purchase. It provides a comprehensive assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to RTX. No placeholders or samples—what you see is what you get, instantly accessible once you buy.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

RTX faces complex competitive dynamics—high buyer expectations, concentrated supplier relationships, and evolving substitute threats driven by tech shifts. Our snapshot highlights key pressures on margins and innovation priorities. The full Porter's Five Forces analysis decodes each force with ratings and strategic implications to inform smarter investment and strategy decisions.

Suppliers Bargaining Power

Concentrated critical materials

RTX depends on limited suppliers for titanium, advanced alloys, rare-earth magnets and high-temp composites; China controls roughly 80% of rare-earth processing capacity (2023–24) and Russia remains a key source for titanium feedstock, raising supplier leverage and geopolitical risk. Disruptions can delay engine castings, avionics and missile components by months to over a year. Dual-sourcing reduces risk but is often infeasible for flight-critical parts.

Specialized aero components

Specialized aero castings, forgings, microelectronics and sensors are concentrated among a few qualified suppliers, creating high supplier power and limited alternatives. Qualification and requalification cycles typically span 12–24 months and often incur multi‑million‑dollar costs, raising switching barriers. Suppliers with proprietary processes therefore command stronger commercial terms, and RTX offsets risk via long‑term agreements and supplier development programs.

Certification and quality lock-in

Certification embeds specific supplier parts into Type Certificates and defense specs, so replacing a vendor often triggers FAA/EASA recertification that commonly takes 12–36 months and can incur tens to hundreds of millions of dollars in program costs. This creates structural supplier stickiness and bargaining power for approved vendors. It lengthens negotiation cycles and forces higher safety-stock and longer lead-time inventory policies for OEMs.

Capacity and lead-time constraints

Engines and defense systems rely on long-lead items with typical lead times of 6–36 months, and tight capacity in castings, chips and energetic materials gives suppliers pricing latitude; chip lead times remained >20 weeks in 2024, stressing availability during backlog recovery cycles.

- Long lead: 6–36 months

- Chips: >20 weeks in 2024

- High capacity utilization → pricing power

- RTX must early-buy and share volume visibility

Compliance and cyber requirements

Compliance regimes—ITAR, DFARS and 2024-era cybersecurity standards (NIST SP 800-171/CMMC 2.0 implementation)—shrink the qualified supplier pool for RTX, raising supplier leverage on sensitive programs. Smaller vendors often pass certification and remediation costs to primes, and non-compliance risk forces RTX to pay premiums for vetted suppliers. This dynamic elevates supplier power in classified and defense-critical work.

- ITAR/DFARS: restrict foreign/small vendor access

- CMMC/NIST 2024: increases vetting costs

- Vetted suppliers: command price premiums

Supplier concentration, long lead times and recertification drive premiums and inventory

RTX relies on few qualified suppliers for titanium, alloys and rare‑earth magnets (China ~80% processing 2023–24), giving suppliers strong leverage; dual‑sourcing often infeasible. Certification/ITAR/CMMC raises switching costs (recert 12–36 months) and forces premiums. Long leads (6–36 months) and chip lead times >20 weeks in 2024 drive early buys and higher inventory.

| Item | Metric | Impact |

|---|---|---|

| Rare‑earth | China ~80% (2023–24) | High supplier power |

| Recertification | 12–36 months | Switching cost |

| Lead times | 6–36 months | Inventory/premiums |

| Chips | >20 weeks (2024) | Availability risk |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry threats specific to RTX, detailing disruptive substitutes and strategic barriers that protect incumbents while highlighting risks to market share and profitability.

A concise, one-sheet RTX Porter's Five Forces summary that highlights supplier/buyer power, competitive rivalry, substitution and entry threats—instantly pinpointing strategic pain points and where to focus mitigation and investment decisions.

Customers Bargaining Power

Concentrated government buyers

US DoD and allied governments are extremely concentrated buyers—US DoD FY2024 budget ~ $858 billion and NATO members’ combined defense spending exceeds $1.2 trillion—driving competitive tenders that push hard on price, IP, and performance. Budget cycles, congressional audits, and program reviews increase margin pressure and contract renegotiations. Mission criticality and multiyear programs (often 5–20 years) limit abrupt price cuts, preserving predictable long-term revenue.

Commercial OEM leverage

In 2024 Boeing and Airbus retained over 90% combined share of large commercial jet platforms, giving them outsized bargaining power over avionics and subsystem suppliers like RTX. Linefit slots are commonly secured through aggressive upfront pricing and performance guarantees tied to certification and delivery milestones. Once a supplier achieves linefit, growing lifetime installed base and aftermarket spares/MRO demand steadily reduce buyer leverage. Upfront concessions are thus traded for durable, high-margin installed-base revenue streams.

Airlines and MRO dynamics

Airlines exert strong pressure for cost-effective maintenance and firm availability, driving RTX into power-by-the-hour and uptime SLA deals that transfer operational risk to the supplier while securing recurring revenue; the global commercial MRO market was about $93 billion in 2024, underlining contract scale. Independent MROs and PMA parts trimmed OEM leverage but safety, certification and reliability requirements keep switching costs high.

High switching costs and lock-in

Engines and defense systems require decades-long integration, training and tooling, with MRO and sustainment contracts commonly running 20+ years, creating high sunk costs that make mid-program vendor switches costly and risky.

Embedded software, data ecosystems and proprietary diagnostics further deepen lock-in, reducing buyer leverage once a platform and supplier are selected.

- Long-term MRO: 20+ years

- High sunk costs: tooling, training, certification

- Software/data lock-in: proprietary diagnostics and updates

- Result: reduced buyer bargaining power post-selection

Performance and availability focus

Buyers prioritize mission readiness, fuel efficiency and lifecycle cost, and superior performance can justify RTX premium pricing while reducing total cost of ownership; in 2024 global defence spending was about 2.3 trillion, keeping pressure on availability and capability. Penalties for delays and AOG events rebalance bargaining power episodically, and data-driven support services improve sortie rates and defend margin by lowering downtime and warranty costs.

- Buyers: mission readiness, lifecycle cost

- Pricing: performance enables premium

- Risk: AOG/delay penalties shift power

- Defense: data services protect margins

Defense buyers and jet duopoly lock long-term MRO and sustainment revenue

US DoD (FY2024 ~$858B) and NATO (> $1.2T) concentrate buying power, driving tough price/IP terms; Boeing+Airsbus hold >90% large-jet share, pressuring linefit pricing. Long MRO/sustainment (20+ years), high sunk costs and software lock-in reduce buyer leverage post-selection; global defense $2.3T and MRO ~$93B sustain recurring revenue and margin defense.

| Metric | 2024 Value |

|---|---|

| US DoD budget | $858B |

| NATO defense spend | >$1.2T |

| Global defense | $2.3T |

| Commercial MRO | $93B |

What You See Is What You Get

RTX Porter's Five Forces Analysis

This Porter's Five Forces analysis of RTX is the exact document you're previewing—fully formatted and ready for immediate download after purchase. It provides a comprehensive assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to RTX. No placeholders or samples—what you see is what you get, instantly accessible once you buy.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

RTX faces complex competitive dynamics—high buyer expectations, concentrated supplier relationships, and evolving substitute threats driven by tech shifts. Our snapshot highlights key pressures on margins and innovation priorities. The full Porter's Five Forces analysis decodes each force with ratings and strategic implications to inform smarter investment and strategy decisions.

Suppliers Bargaining Power

Concentrated critical materials

RTX depends on limited suppliers for titanium, advanced alloys, rare-earth magnets and high-temp composites; China controls roughly 80% of rare-earth processing capacity (2023–24) and Russia remains a key source for titanium feedstock, raising supplier leverage and geopolitical risk. Disruptions can delay engine castings, avionics and missile components by months to over a year. Dual-sourcing reduces risk but is often infeasible for flight-critical parts.

Specialized aero components

Specialized aero castings, forgings, microelectronics and sensors are concentrated among a few qualified suppliers, creating high supplier power and limited alternatives. Qualification and requalification cycles typically span 12–24 months and often incur multi‑million‑dollar costs, raising switching barriers. Suppliers with proprietary processes therefore command stronger commercial terms, and RTX offsets risk via long‑term agreements and supplier development programs.

Certification and quality lock-in

Certification embeds specific supplier parts into Type Certificates and defense specs, so replacing a vendor often triggers FAA/EASA recertification that commonly takes 12–36 months and can incur tens to hundreds of millions of dollars in program costs. This creates structural supplier stickiness and bargaining power for approved vendors. It lengthens negotiation cycles and forces higher safety-stock and longer lead-time inventory policies for OEMs.

Capacity and lead-time constraints

Engines and defense systems rely on long-lead items with typical lead times of 6–36 months, and tight capacity in castings, chips and energetic materials gives suppliers pricing latitude; chip lead times remained >20 weeks in 2024, stressing availability during backlog recovery cycles.

- Long lead: 6–36 months

- Chips: >20 weeks in 2024

- High capacity utilization → pricing power

- RTX must early-buy and share volume visibility

Compliance and cyber requirements

Compliance regimes—ITAR, DFARS and 2024-era cybersecurity standards (NIST SP 800-171/CMMC 2.0 implementation)—shrink the qualified supplier pool for RTX, raising supplier leverage on sensitive programs. Smaller vendors often pass certification and remediation costs to primes, and non-compliance risk forces RTX to pay premiums for vetted suppliers. This dynamic elevates supplier power in classified and defense-critical work.

- ITAR/DFARS: restrict foreign/small vendor access

- CMMC/NIST 2024: increases vetting costs

- Vetted suppliers: command price premiums

Supplier concentration, long lead times and recertification drive premiums and inventory

RTX relies on few qualified suppliers for titanium, alloys and rare‑earth magnets (China ~80% processing 2023–24), giving suppliers strong leverage; dual‑sourcing often infeasible. Certification/ITAR/CMMC raises switching costs (recert 12–36 months) and forces premiums. Long leads (6–36 months) and chip lead times >20 weeks in 2024 drive early buys and higher inventory.

| Item | Metric | Impact |

|---|---|---|

| Rare‑earth | China ~80% (2023–24) | High supplier power |

| Recertification | 12–36 months | Switching cost |

| Lead times | 6–36 months | Inventory/premiums |

| Chips | >20 weeks (2024) | Availability risk |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry threats specific to RTX, detailing disruptive substitutes and strategic barriers that protect incumbents while highlighting risks to market share and profitability.

A concise, one-sheet RTX Porter's Five Forces summary that highlights supplier/buyer power, competitive rivalry, substitution and entry threats—instantly pinpointing strategic pain points and where to focus mitigation and investment decisions.

Customers Bargaining Power

Concentrated government buyers

US DoD and allied governments are extremely concentrated buyers—US DoD FY2024 budget ~ $858 billion and NATO members’ combined defense spending exceeds $1.2 trillion—driving competitive tenders that push hard on price, IP, and performance. Budget cycles, congressional audits, and program reviews increase margin pressure and contract renegotiations. Mission criticality and multiyear programs (often 5–20 years) limit abrupt price cuts, preserving predictable long-term revenue.

Commercial OEM leverage

In 2024 Boeing and Airbus retained over 90% combined share of large commercial jet platforms, giving them outsized bargaining power over avionics and subsystem suppliers like RTX. Linefit slots are commonly secured through aggressive upfront pricing and performance guarantees tied to certification and delivery milestones. Once a supplier achieves linefit, growing lifetime installed base and aftermarket spares/MRO demand steadily reduce buyer leverage. Upfront concessions are thus traded for durable, high-margin installed-base revenue streams.

Airlines and MRO dynamics

Airlines exert strong pressure for cost-effective maintenance and firm availability, driving RTX into power-by-the-hour and uptime SLA deals that transfer operational risk to the supplier while securing recurring revenue; the global commercial MRO market was about $93 billion in 2024, underlining contract scale. Independent MROs and PMA parts trimmed OEM leverage but safety, certification and reliability requirements keep switching costs high.

High switching costs and lock-in

Engines and defense systems require decades-long integration, training and tooling, with MRO and sustainment contracts commonly running 20+ years, creating high sunk costs that make mid-program vendor switches costly and risky.

Embedded software, data ecosystems and proprietary diagnostics further deepen lock-in, reducing buyer leverage once a platform and supplier are selected.

- Long-term MRO: 20+ years

- High sunk costs: tooling, training, certification

- Software/data lock-in: proprietary diagnostics and updates

- Result: reduced buyer bargaining power post-selection

Performance and availability focus

Buyers prioritize mission readiness, fuel efficiency and lifecycle cost, and superior performance can justify RTX premium pricing while reducing total cost of ownership; in 2024 global defence spending was about 2.3 trillion, keeping pressure on availability and capability. Penalties for delays and AOG events rebalance bargaining power episodically, and data-driven support services improve sortie rates and defend margin by lowering downtime and warranty costs.

- Buyers: mission readiness, lifecycle cost

- Pricing: performance enables premium

- Risk: AOG/delay penalties shift power

- Defense: data services protect margins

Defense buyers and jet duopoly lock long-term MRO and sustainment revenue

US DoD (FY2024 ~$858B) and NATO (> $1.2T) concentrate buying power, driving tough price/IP terms; Boeing+Airsbus hold >90% large-jet share, pressuring linefit pricing. Long MRO/sustainment (20+ years), high sunk costs and software lock-in reduce buyer leverage post-selection; global defense $2.3T and MRO ~$93B sustain recurring revenue and margin defense.

| Metric | 2024 Value |

|---|---|

| US DoD budget | $858B |

| NATO defense spend | >$1.2T |

| Global defense | $2.3T |

| Commercial MRO | $93B |

What You See Is What You Get

RTX Porter's Five Forces Analysis

This Porter's Five Forces analysis of RTX is the exact document you're previewing—fully formatted and ready for immediate download after purchase. It provides a comprehensive assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to RTX. No placeholders or samples—what you see is what you get, instantly accessible once you buy.