Rumo SWOT Analysis

Your Strategic Toolkit Starts Here

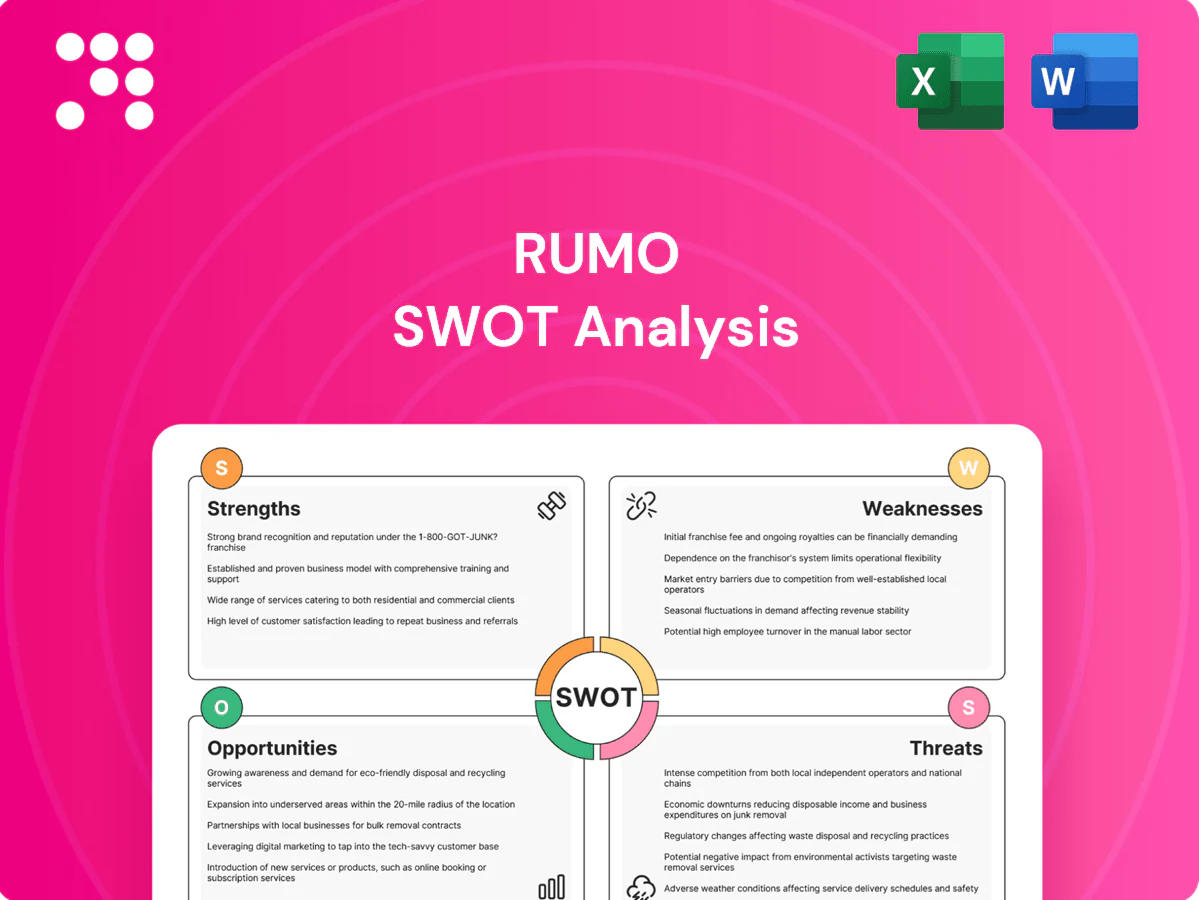

Rumo’s SWOT reveals a dominant Brazilian rail network and strong agribusiness exposure as key strengths, offset by regulatory risk and asset concentration as weaknesses. Opportunities include export growth, intermodal expansion, and digital logistics, while threats stem from commodity cycles, road competition, and policy shifts. Want the full strategic picture with editable Word and Excel deliverables? Purchase the complete SWOT for research-ready insights and action plans.

Strengths

Extensive rail network scale

Rumo's extensive contiguous rail footprint exceeds 12,000 km, linking Mato Grosso, Paraná and other producing regions to export ports such as Santos and Paranaguá. High corridor density and long corridor lengths give deep reach into Brazil's agribusiness heartland (Mato Grosso accounts for roughly 30% of national soy). Scale drives higher asset utilization and service frequency, creating strong barriers to entry and pricing power in bulk logistics.

Integrated logistics (rail, ports, warehousing)

Rumo’s integrated logistics platform—anchored on a rail network of over 12,000 km and linked ports and warehousing—cuts handoff frictions and lowers total landed cost by consolidating door-to-door flows for shippers. Close coordination between terminals, yards and storage smooths scheduling and reduces dwell times, improving throughput and turn-times. Integration increases customer stickiness and enables deeper, longer-term contracts.

Cost advantage for bulk commodities

Rail offers a 3–4x energy efficiency advantage over trucking and carries much higher payloads, yielding roughly 50–70% lower per-ton-km costs for long-haul grains, sugar, ethanol and industrial goods. That lower logistics cost improves exporters’ competitiveness at major Brazilian ports such as Santos and Paranaguá by reducing inland haul share of FOB costs. The cost edge supports volume resilience and capacity to absorb peak harvest surges without proportionate unit-cost increases.

Long-term concessions and contracts

Long-term concessions and take-or-pay shipper contracts give Rumo high volume visibility by locking minimum freight volumes and defining tariff frameworks, which underpins predictable utilization of its rail network.

These contract structures translate into stable cash flows and stronger debt-service capacity, supporting capital expenditure for network expansion and rolling stock.

Regulatory-backed concession frameworks provide operating continuity and tariff adjustment mechanisms, reducing revenue volatility across cycles.

- Volume visibility via take-or-pay contracts

- Stable cash flow → enhanced financing capacity for capex

- Regulatory concession protections

- Lower revenue volatility across cycles

Strategic positioning in export corridors

Rumo’s strategic positioning along Brazil’s main soy, corn and sugar export corridors aligns terminals and services with key industrial clusters and provides gateway access to major ports and intermodal terminals, enabling higher scheduling reliability and differentiated premium service tiers that capture time-sensitive shippers.

Rail >12,000 km links Mato Grosso soy to ports; 3–4x energy, 50–70% lower cost

Rumo operates a contiguous rail network >12,000 km connecting Mato Grosso (≈30% of Brazil’s soy) to ports, creating high corridor density and pricing power. Integrated terminals, yards and storage lower total landed cost and increase customer stickiness via long-term take-or-pay contracts. Rail offers 3–4x energy efficiency and ~50–70% lower per-ton-km for long-haul bulk, supporting volume resilience and stable cash flows.

| Metric | Value |

|---|---|

| Network length | >12,000 km |

| Mato Grosso soy share | ≈30% |

| Energy efficiency (rail vs truck) | 3–4x |

| Per-ton-km cost advantage | ~50–70% |

What is included in the product

Provides a concise strategic overview of Rumo’s internal strengths and weaknesses and external opportunities and threats, mapping key growth drivers, operational gaps, competitive position and risks shaping its future.

Provides a clear, visual SWOT layout for Rumo to quickly identify operational bottlenecks and align mitigation strategies across teams.

Weaknesses

High capital intensity and leverage

Recurring high-cost needs for track renewal, double-tracking, rolling stock and signaling drive Rumo’s capital expenditure (capex) — 2024 capex was about BRL 4.1 billion — while net debt of roughly BRL 29.4 billion at end-2024 makes the company sensitive to interest-rate swings and refinancing costs. Large projects have long payback horizons (often 7–15 years) and meaningful execution risk, increasing the chance of cost overruns. These dynamics compress free cash flow flexibility, limiting dividend and opportunistic investment capacity during periods of elevated rates or weak volumes.

Corridor concentration risk

Rumo's network concentration along key agribusiness corridors—notably the Mato Grosso to coastal terminals—creates dependence on those routes to move the bulk of grain flows across its about 12,300 km system. This links performance directly to regional harvest outcomes (Brazil's 2024 soy crop was about 160 million tonnes) and local disruptions like floods, strikes or track incidents. Limited presence in northern or alternative export arcs in some segments reduces diversification. Corridor concentration can therefore amplify operational shocks and revenue volatility.

Commodity volume seasonality

Rumo faces pronounced peak-and-trough patterns tied to Brazil's harvest cycles, with the main soybean harvest concentrated in Feb–Apr and the safrinha corn season in Oct–Jan. These peaks strain planning for crews, wagons and terminal capacity, requiring surge logistics and temporary hires. Off-peak months can leave assets underutilized, increasing per-ton costs. Seasonality amplifies earnings volatility and working capital swings as receivables and inventory rise around harvests.

Regulatory and concession dependencies

Rumo depends on concession renewals (typically 30-year terms) and tariff oversight by ANTT/ANTAQ, with contractual minimum investment obligations that constrain cash flow and require capital deployment.

Regulatory approvals for works and tariffs can take months to years, delaying projects; compliance and expanded reporting raise operating costs and administrative burden.

Rule changes or tariff rebalancing materially risk return profiles and IRR on long-lived rail assets.

- Concession length: ~30 years

- Regulators: ANTT, ANTAQ

- Approval delays: months–years

- Higher compliance/reporting costs

Legacy infrastructure bottlenecks

Rumo's legacy network, roughly 12,000 km as of 2024, contains extensive single-track stretches, speed-limited segments and aging bridges that constrain throughput and punctuality on key corridors. These bottlenecks raise maintenance intensity and outage risk, driving higher O&M and derailment-related costs. Service reliability erosion feeds cost creep and limits volume growth potential.

- Scale: ≈12,000 km (2024)

- Constraint: single-track/speed limits reduce capacity

- Risk: aging bridges → higher outage/maintenance

- Impact: reliability decline → rising O&M costs

High capex and heavy debt constrain rail network amid Mato Grosso seasonality and single-track limits

High capex (BRL 4.1bn in 2024) and net debt (~BRL 29.4bn end-2024) limit cash flexibility and heighten refinancing/interest-rate risk; major projects have 7–15 year paybacks and execution risk. Network concentration on Mato Grosso export corridors and strong seasonality (soy Feb–Apr, safrinha Oct–Jan) amplify volume volatility. Extensive single-track stretches (~12,300 km) and aging assets constrain capacity and raise O&M/outage costs.

| Metric | Value |

|---|---|

| 2024 capex | BRL 4.1bn |

| Net debt (end-2024) | BRL 29.4bn |

| Network length (2024) | ≈12,300 km |

| Concession term | ≈30 years |

| Peak months | Feb–Apr; Oct–Jan |

Full Version Awaits

Rumo SWOT Analysis

This is the actual Rumo SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. The file is structured, actionable, and ready for immediate use after checkout.

Your Strategic Toolkit Starts Here

Rumo’s SWOT reveals a dominant Brazilian rail network and strong agribusiness exposure as key strengths, offset by regulatory risk and asset concentration as weaknesses. Opportunities include export growth, intermodal expansion, and digital logistics, while threats stem from commodity cycles, road competition, and policy shifts. Want the full strategic picture with editable Word and Excel deliverables? Purchase the complete SWOT for research-ready insights and action plans.

Strengths

Extensive rail network scale

Rumo's extensive contiguous rail footprint exceeds 12,000 km, linking Mato Grosso, Paraná and other producing regions to export ports such as Santos and Paranaguá. High corridor density and long corridor lengths give deep reach into Brazil's agribusiness heartland (Mato Grosso accounts for roughly 30% of national soy). Scale drives higher asset utilization and service frequency, creating strong barriers to entry and pricing power in bulk logistics.

Integrated logistics (rail, ports, warehousing)

Rumo’s integrated logistics platform—anchored on a rail network of over 12,000 km and linked ports and warehousing—cuts handoff frictions and lowers total landed cost by consolidating door-to-door flows for shippers. Close coordination between terminals, yards and storage smooths scheduling and reduces dwell times, improving throughput and turn-times. Integration increases customer stickiness and enables deeper, longer-term contracts.

Cost advantage for bulk commodities

Rail offers a 3–4x energy efficiency advantage over trucking and carries much higher payloads, yielding roughly 50–70% lower per-ton-km costs for long-haul grains, sugar, ethanol and industrial goods. That lower logistics cost improves exporters’ competitiveness at major Brazilian ports such as Santos and Paranaguá by reducing inland haul share of FOB costs. The cost edge supports volume resilience and capacity to absorb peak harvest surges without proportionate unit-cost increases.

Long-term concessions and contracts

Long-term concessions and take-or-pay shipper contracts give Rumo high volume visibility by locking minimum freight volumes and defining tariff frameworks, which underpins predictable utilization of its rail network.

These contract structures translate into stable cash flows and stronger debt-service capacity, supporting capital expenditure for network expansion and rolling stock.

Regulatory-backed concession frameworks provide operating continuity and tariff adjustment mechanisms, reducing revenue volatility across cycles.

- Volume visibility via take-or-pay contracts

- Stable cash flow → enhanced financing capacity for capex

- Regulatory concession protections

- Lower revenue volatility across cycles

Strategic positioning in export corridors

Rumo’s strategic positioning along Brazil’s main soy, corn and sugar export corridors aligns terminals and services with key industrial clusters and provides gateway access to major ports and intermodal terminals, enabling higher scheduling reliability and differentiated premium service tiers that capture time-sensitive shippers.

Rail >12,000 km links Mato Grosso soy to ports; 3–4x energy, 50–70% lower cost

Rumo operates a contiguous rail network >12,000 km connecting Mato Grosso (≈30% of Brazil’s soy) to ports, creating high corridor density and pricing power. Integrated terminals, yards and storage lower total landed cost and increase customer stickiness via long-term take-or-pay contracts. Rail offers 3–4x energy efficiency and ~50–70% lower per-ton-km for long-haul bulk, supporting volume resilience and stable cash flows.

| Metric | Value |

|---|---|

| Network length | >12,000 km |

| Mato Grosso soy share | ≈30% |

| Energy efficiency (rail vs truck) | 3–4x |

| Per-ton-km cost advantage | ~50–70% |

What is included in the product

Provides a concise strategic overview of Rumo’s internal strengths and weaknesses and external opportunities and threats, mapping key growth drivers, operational gaps, competitive position and risks shaping its future.

Provides a clear, visual SWOT layout for Rumo to quickly identify operational bottlenecks and align mitigation strategies across teams.

Weaknesses

High capital intensity and leverage

Recurring high-cost needs for track renewal, double-tracking, rolling stock and signaling drive Rumo’s capital expenditure (capex) — 2024 capex was about BRL 4.1 billion — while net debt of roughly BRL 29.4 billion at end-2024 makes the company sensitive to interest-rate swings and refinancing costs. Large projects have long payback horizons (often 7–15 years) and meaningful execution risk, increasing the chance of cost overruns. These dynamics compress free cash flow flexibility, limiting dividend and opportunistic investment capacity during periods of elevated rates or weak volumes.

Corridor concentration risk

Rumo's network concentration along key agribusiness corridors—notably the Mato Grosso to coastal terminals—creates dependence on those routes to move the bulk of grain flows across its about 12,300 km system. This links performance directly to regional harvest outcomes (Brazil's 2024 soy crop was about 160 million tonnes) and local disruptions like floods, strikes or track incidents. Limited presence in northern or alternative export arcs in some segments reduces diversification. Corridor concentration can therefore amplify operational shocks and revenue volatility.

Commodity volume seasonality

Rumo faces pronounced peak-and-trough patterns tied to Brazil's harvest cycles, with the main soybean harvest concentrated in Feb–Apr and the safrinha corn season in Oct–Jan. These peaks strain planning for crews, wagons and terminal capacity, requiring surge logistics and temporary hires. Off-peak months can leave assets underutilized, increasing per-ton costs. Seasonality amplifies earnings volatility and working capital swings as receivables and inventory rise around harvests.

Regulatory and concession dependencies

Rumo depends on concession renewals (typically 30-year terms) and tariff oversight by ANTT/ANTAQ, with contractual minimum investment obligations that constrain cash flow and require capital deployment.

Regulatory approvals for works and tariffs can take months to years, delaying projects; compliance and expanded reporting raise operating costs and administrative burden.

Rule changes or tariff rebalancing materially risk return profiles and IRR on long-lived rail assets.

- Concession length: ~30 years

- Regulators: ANTT, ANTAQ

- Approval delays: months–years

- Higher compliance/reporting costs

Legacy infrastructure bottlenecks

Rumo's legacy network, roughly 12,000 km as of 2024, contains extensive single-track stretches, speed-limited segments and aging bridges that constrain throughput and punctuality on key corridors. These bottlenecks raise maintenance intensity and outage risk, driving higher O&M and derailment-related costs. Service reliability erosion feeds cost creep and limits volume growth potential.

- Scale: ≈12,000 km (2024)

- Constraint: single-track/speed limits reduce capacity

- Risk: aging bridges → higher outage/maintenance

- Impact: reliability decline → rising O&M costs

High capex and heavy debt constrain rail network amid Mato Grosso seasonality and single-track limits

High capex (BRL 4.1bn in 2024) and net debt (~BRL 29.4bn end-2024) limit cash flexibility and heighten refinancing/interest-rate risk; major projects have 7–15 year paybacks and execution risk. Network concentration on Mato Grosso export corridors and strong seasonality (soy Feb–Apr, safrinha Oct–Jan) amplify volume volatility. Extensive single-track stretches (~12,300 km) and aging assets constrain capacity and raise O&M/outage costs.

| Metric | Value |

|---|---|

| 2024 capex | BRL 4.1bn |

| Net debt (end-2024) | BRL 29.4bn |

| Network length (2024) | ≈12,300 km |

| Concession term | ≈30 years |

| Peak months | Feb–Apr; Oct–Jan |

Full Version Awaits

Rumo SWOT Analysis

This is the actual Rumo SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. The file is structured, actionable, and ready for immediate use after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

Rumo’s SWOT reveals a dominant Brazilian rail network and strong agribusiness exposure as key strengths, offset by regulatory risk and asset concentration as weaknesses. Opportunities include export growth, intermodal expansion, and digital logistics, while threats stem from commodity cycles, road competition, and policy shifts. Want the full strategic picture with editable Word and Excel deliverables? Purchase the complete SWOT for research-ready insights and action plans.

Strengths

Extensive rail network scale

Rumo's extensive contiguous rail footprint exceeds 12,000 km, linking Mato Grosso, Paraná and other producing regions to export ports such as Santos and Paranaguá. High corridor density and long corridor lengths give deep reach into Brazil's agribusiness heartland (Mato Grosso accounts for roughly 30% of national soy). Scale drives higher asset utilization and service frequency, creating strong barriers to entry and pricing power in bulk logistics.

Integrated logistics (rail, ports, warehousing)

Rumo’s integrated logistics platform—anchored on a rail network of over 12,000 km and linked ports and warehousing—cuts handoff frictions and lowers total landed cost by consolidating door-to-door flows for shippers. Close coordination between terminals, yards and storage smooths scheduling and reduces dwell times, improving throughput and turn-times. Integration increases customer stickiness and enables deeper, longer-term contracts.

Cost advantage for bulk commodities

Rail offers a 3–4x energy efficiency advantage over trucking and carries much higher payloads, yielding roughly 50–70% lower per-ton-km costs for long-haul grains, sugar, ethanol and industrial goods. That lower logistics cost improves exporters’ competitiveness at major Brazilian ports such as Santos and Paranaguá by reducing inland haul share of FOB costs. The cost edge supports volume resilience and capacity to absorb peak harvest surges without proportionate unit-cost increases.

Long-term concessions and contracts

Long-term concessions and take-or-pay shipper contracts give Rumo high volume visibility by locking minimum freight volumes and defining tariff frameworks, which underpins predictable utilization of its rail network.

These contract structures translate into stable cash flows and stronger debt-service capacity, supporting capital expenditure for network expansion and rolling stock.

Regulatory-backed concession frameworks provide operating continuity and tariff adjustment mechanisms, reducing revenue volatility across cycles.

- Volume visibility via take-or-pay contracts

- Stable cash flow → enhanced financing capacity for capex

- Regulatory concession protections

- Lower revenue volatility across cycles

Strategic positioning in export corridors

Rumo’s strategic positioning along Brazil’s main soy, corn and sugar export corridors aligns terminals and services with key industrial clusters and provides gateway access to major ports and intermodal terminals, enabling higher scheduling reliability and differentiated premium service tiers that capture time-sensitive shippers.

Rail >12,000 km links Mato Grosso soy to ports; 3–4x energy, 50–70% lower cost

Rumo operates a contiguous rail network >12,000 km connecting Mato Grosso (≈30% of Brazil’s soy) to ports, creating high corridor density and pricing power. Integrated terminals, yards and storage lower total landed cost and increase customer stickiness via long-term take-or-pay contracts. Rail offers 3–4x energy efficiency and ~50–70% lower per-ton-km for long-haul bulk, supporting volume resilience and stable cash flows.

| Metric | Value |

|---|---|

| Network length | >12,000 km |

| Mato Grosso soy share | ≈30% |

| Energy efficiency (rail vs truck) | 3–4x |

| Per-ton-km cost advantage | ~50–70% |

What is included in the product

Provides a concise strategic overview of Rumo’s internal strengths and weaknesses and external opportunities and threats, mapping key growth drivers, operational gaps, competitive position and risks shaping its future.

Provides a clear, visual SWOT layout for Rumo to quickly identify operational bottlenecks and align mitigation strategies across teams.

Weaknesses

High capital intensity and leverage

Recurring high-cost needs for track renewal, double-tracking, rolling stock and signaling drive Rumo’s capital expenditure (capex) — 2024 capex was about BRL 4.1 billion — while net debt of roughly BRL 29.4 billion at end-2024 makes the company sensitive to interest-rate swings and refinancing costs. Large projects have long payback horizons (often 7–15 years) and meaningful execution risk, increasing the chance of cost overruns. These dynamics compress free cash flow flexibility, limiting dividend and opportunistic investment capacity during periods of elevated rates or weak volumes.

Corridor concentration risk

Rumo's network concentration along key agribusiness corridors—notably the Mato Grosso to coastal terminals—creates dependence on those routes to move the bulk of grain flows across its about 12,300 km system. This links performance directly to regional harvest outcomes (Brazil's 2024 soy crop was about 160 million tonnes) and local disruptions like floods, strikes or track incidents. Limited presence in northern or alternative export arcs in some segments reduces diversification. Corridor concentration can therefore amplify operational shocks and revenue volatility.

Commodity volume seasonality

Rumo faces pronounced peak-and-trough patterns tied to Brazil's harvest cycles, with the main soybean harvest concentrated in Feb–Apr and the safrinha corn season in Oct–Jan. These peaks strain planning for crews, wagons and terminal capacity, requiring surge logistics and temporary hires. Off-peak months can leave assets underutilized, increasing per-ton costs. Seasonality amplifies earnings volatility and working capital swings as receivables and inventory rise around harvests.

Regulatory and concession dependencies

Rumo depends on concession renewals (typically 30-year terms) and tariff oversight by ANTT/ANTAQ, with contractual minimum investment obligations that constrain cash flow and require capital deployment.

Regulatory approvals for works and tariffs can take months to years, delaying projects; compliance and expanded reporting raise operating costs and administrative burden.

Rule changes or tariff rebalancing materially risk return profiles and IRR on long-lived rail assets.

- Concession length: ~30 years

- Regulators: ANTT, ANTAQ

- Approval delays: months–years

- Higher compliance/reporting costs

Legacy infrastructure bottlenecks

Rumo's legacy network, roughly 12,000 km as of 2024, contains extensive single-track stretches, speed-limited segments and aging bridges that constrain throughput and punctuality on key corridors. These bottlenecks raise maintenance intensity and outage risk, driving higher O&M and derailment-related costs. Service reliability erosion feeds cost creep and limits volume growth potential.

- Scale: ≈12,000 km (2024)

- Constraint: single-track/speed limits reduce capacity

- Risk: aging bridges → higher outage/maintenance

- Impact: reliability decline → rising O&M costs

High capex and heavy debt constrain rail network amid Mato Grosso seasonality and single-track limits

High capex (BRL 4.1bn in 2024) and net debt (~BRL 29.4bn end-2024) limit cash flexibility and heighten refinancing/interest-rate risk; major projects have 7–15 year paybacks and execution risk. Network concentration on Mato Grosso export corridors and strong seasonality (soy Feb–Apr, safrinha Oct–Jan) amplify volume volatility. Extensive single-track stretches (~12,300 km) and aging assets constrain capacity and raise O&M/outage costs.

| Metric | Value |

|---|---|

| 2024 capex | BRL 4.1bn |

| Net debt (end-2024) | BRL 29.4bn |

| Network length (2024) | ≈12,300 km |

| Concession term | ≈30 years |

| Peak months | Feb–Apr; Oct–Jan |

Full Version Awaits

Rumo SWOT Analysis

This is the actual Rumo SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. The file is structured, actionable, and ready for immediate use after checkout.