Ryerson Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

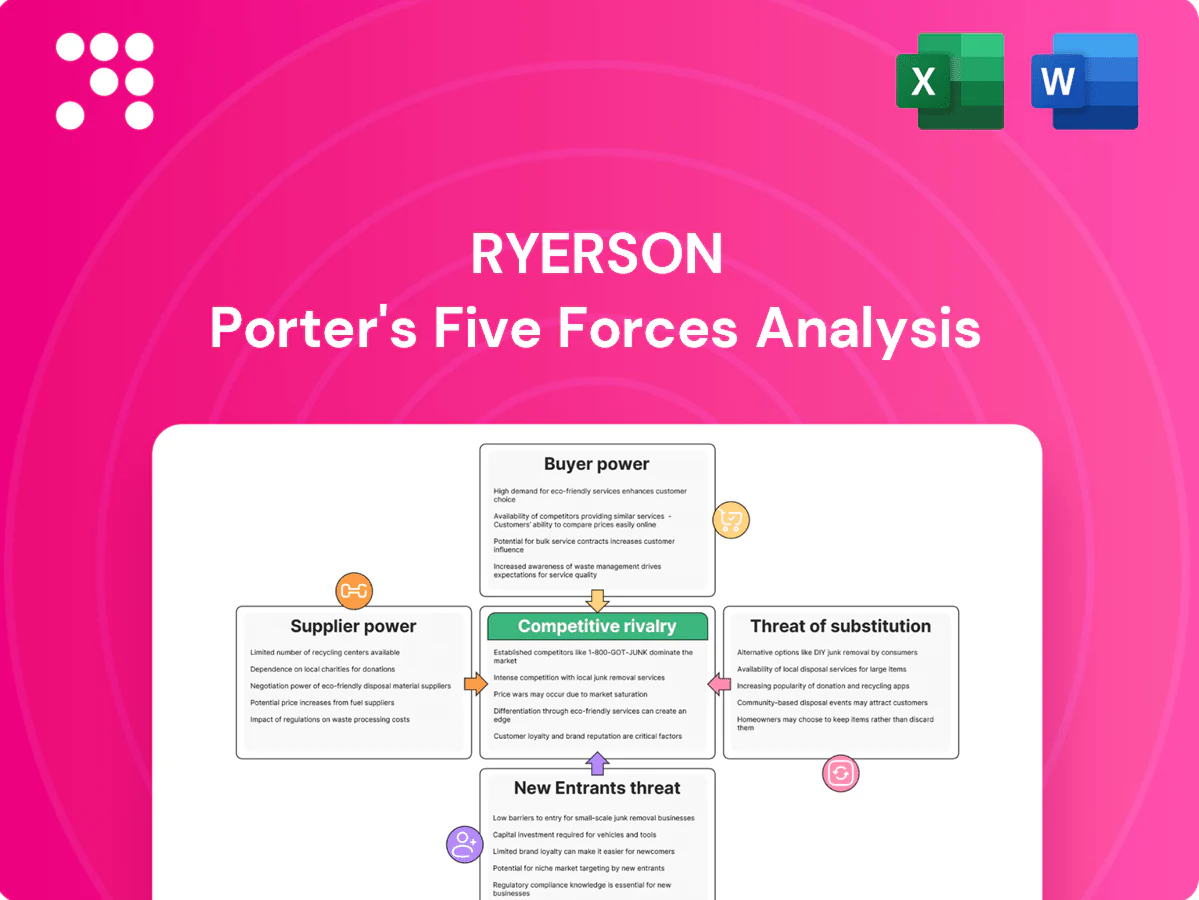

Ryerson’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, substitute threats, entry barriers, and rival intensity to reveal where competitive vulnerability and opportunity lie; the concise findings point to strategic levers for margin protection and growth. This brief only scratches the surface—purchase the full report for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated upstream metal producers

In 2024 global crude steel production remained highly concentrated, with China supplying more than half of world tonnage and the largest mills controlling regional allocations and pricing. Aluminum smelters are likewise clustered among a handful of producers, giving upstream suppliers leverage over premiums and lead times. Ryerson’s broad product mix reduces single-grade exposure, but critical grades often remain single- or few-sourced. Long-term contracts and multi-mill sourcing lower but do not eliminate supplier power during tight cycles.

Input price volatility and surcharges

Commodity price swings and mill surcharges (fuel, alloy) in 2024 compressed margins when pass-through to customers lagged, and Ryerson’s published pricing mechanisms and tighter inventory discipline mitigated but did not eliminate timing mismatches. Suppliers in 2024 occasionally enforced price floors or allocation during tight supply windows. Hedging reduced headline volatility but introduced basis and timing risks that persisted across quarters.

Quality specs and certifications

Quality specs and certifications drive supplier power in automotive, energy and aerospace where AS9100, ISO 9001 and Nadcap approvals (as of 2024) narrow qualified vendors and raise switching friction. Mills holding proprietary specs or OEM approvals secure pricing leverage. Ryerson’s approved supplier roster reduces single-supplier dependency but approval cycles slow substitution. Nonconformance risks increase the effective cost of pushing back on terms.

Logistics and lead-time constraints

Freight capacity squeeze, import controls and the continued 25% Section 232 steel tariff in 2024 tighten supply channels, letting mills use delivery schedules and minimums to pressure service-center margins; Ryerson’s broad branch network and mixed-mode logistics mitigate but cannot fully offset systemic lead-time and capacity limits, and regional steel shortages raise local supplier clout.

- Freight capacity: tight in 2024

- Tariffs: 25% Section 232 on steel

- Mills leverage: delivery schedules & minimums

- Ryerson: network softens but not eliminates risk

- Regional shortages boost supplier bargaining

Value-added coil/plate availability

Access to wider coils, plate, and specialty alloys is concentrated among a handful of mills that can bundle favorable and scarce items to shape negotiations; Ryerson’s purchasing scale secures improved allocation during constrained periods but scarcity of certain high-grade alloys maintains elevated supplier power.

- Supplier concentration

- Bundling leverage

- Ryerson scale improves allocation

- Scarce grades sustain supplier power

Supplier leverage tightens as China >50% steel and 25% tariffs squeeze margins

Supplier power in 2024 remained high: China supplied >50% of crude steel, a few mills and smelters controlled allocations, and scarce alloy grades were few-sourced. Ryerson’s multi-mill sourcing and long-term contracts blunt but do not remove leverage; timing mismatches from mill surcharges compressed margins. Trade policy and logistics tightened channels—Section 232 steel tariff at 25% amplified local supplier clout.

| Metric | 2024 |

|---|---|

| China share of crude steel | >50% |

| Section 232 steel tariff | 25% |

| Freight | Capacity tight |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Ryerson, uncovering competitive intensity, supplier and buyer power, and barriers to entry. Highlights disruptive threats, substitutes, and strategic levers to protect market share and pricing power.

One-sheet Ryerson Porter's Five Forces summary that instantly clarifies competitive pressure—perfect for rapid decision-making and cleanly copyable into pitch decks or board slides.

Customers Bargaining Power

Fragmented base but powerful OEMs

Ryerson serves a fragmented SME base that limits individual buyer leverage, but large OEMs in transportation, heavy equipment and energy exert strong negotiating power; industry estimates place the US metal distribution market near $110 billion in 2024, concentrating bargaining with top OEMs. Big accounts routinely demand volume discounts and strict SLAs, and losing a major customer can materially shift sales mix and depress plant utilization.

High price transparency on commodities

In 2024 spot indices from Fastmarkets, Platts and MetalMiner and published surcharges enable easy benchmarking, and buyers can solicit multiple quotes within hours, compressing negotiation and pressuring margins. Ryerson competes on total delivered cost—not just base price—by pricing transport, inventory and surcharge mixes. Transparent markets amplify buyer leverage in oversupplied periods, worsening margin pressure.

Low switching costs for basic products

For standard grades and dimensions alternatives are plentiful and customers can re-source with minimal qualification effort; global crude steel production was about 1.8 billion tonnes in 2024, underscoring broad supplier capacity. Ryerson raises switching costs via downstream processing integration, kitting, and vendor-managed inventory programs. Ultimately, service-level reliability — on-time fills and order accuracy — becomes the primary stickiness factor.

Value-added services dampen leverage

Cutting, slitting, blanking and JIT programs embed Ryerson into customer workflows, making it a logistics and processing partner rather than a commodity supplier. Tailored inventory and staggered release schedules demonstrably reduce customers’ working capital needs and curb pure price-driven switching. Operational integration and near-real-time performance data via EDI links strengthen retention and raise switching costs.

- Service integration: processing + JIT

- Working capital: tailored inventory

- Retention: EDI + performance data

Demand cyclicality sharpens buyer tactics

Demand cyclicality sharpens buyer tactics: in 2024 downturns customers consolidated spend and ran auctions more frequently, increasing lead-time slack and elevating negotiation pressure; in upcycles buyers accepted pass-throughs to secure supply. Ryerson’s diversified contract mix (fixed, index-linked, spot) smooths but does not eliminate cyclic impacts on margins.

- 2024: auction-driven price resets rose notably

- Lead-time slack amplified bargaining leverage

- Pass-throughs more accepted in tight supply

- Contract mix reduces but doesn’t nullify cyclicity

Buyers' leverage compresses metal margins; distributors use processing, JIT and VMI to defend

Buyers have strong leverage: US metal distribution ~ $110B in 2024 and large OEMs concentrate spend, pressing for discounts and SLAs. Transparent spot indices (Fastmarkets/Platts/MetalMiner) and 1.8bn t crude steel supply in 2024 enable rapid re-sourcing, compressing margins. Ryerson offsets via processing, JIT and VMI to raise switching costs and protect utilization.

| Metric | 2024 |

|---|---|

| US market size | $110B |

| Global crude steel | 1.8bn t |

| Indices | Fastmarkets/Platts/MetalMiner |

Full Version Awaits

Ryerson Porter's Five Forces Analysis

This preview shows the Ryerson Porter’s Five Forces Analysis exactly as delivered upon purchase—no mockups, no placeholders. The file is the full, professionally formatted analysis you’ll receive instantly after payment. It’s ready for download and immediate use in presentations, reports, or strategic planning. What you see here is precisely what you’ll get.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Ryerson’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, substitute threats, entry barriers, and rival intensity to reveal where competitive vulnerability and opportunity lie; the concise findings point to strategic levers for margin protection and growth. This brief only scratches the surface—purchase the full report for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated upstream metal producers

In 2024 global crude steel production remained highly concentrated, with China supplying more than half of world tonnage and the largest mills controlling regional allocations and pricing. Aluminum smelters are likewise clustered among a handful of producers, giving upstream suppliers leverage over premiums and lead times. Ryerson’s broad product mix reduces single-grade exposure, but critical grades often remain single- or few-sourced. Long-term contracts and multi-mill sourcing lower but do not eliminate supplier power during tight cycles.

Input price volatility and surcharges

Commodity price swings and mill surcharges (fuel, alloy) in 2024 compressed margins when pass-through to customers lagged, and Ryerson’s published pricing mechanisms and tighter inventory discipline mitigated but did not eliminate timing mismatches. Suppliers in 2024 occasionally enforced price floors or allocation during tight supply windows. Hedging reduced headline volatility but introduced basis and timing risks that persisted across quarters.

Quality specs and certifications

Quality specs and certifications drive supplier power in automotive, energy and aerospace where AS9100, ISO 9001 and Nadcap approvals (as of 2024) narrow qualified vendors and raise switching friction. Mills holding proprietary specs or OEM approvals secure pricing leverage. Ryerson’s approved supplier roster reduces single-supplier dependency but approval cycles slow substitution. Nonconformance risks increase the effective cost of pushing back on terms.

Logistics and lead-time constraints

Freight capacity squeeze, import controls and the continued 25% Section 232 steel tariff in 2024 tighten supply channels, letting mills use delivery schedules and minimums to pressure service-center margins; Ryerson’s broad branch network and mixed-mode logistics mitigate but cannot fully offset systemic lead-time and capacity limits, and regional steel shortages raise local supplier clout.

- Freight capacity: tight in 2024

- Tariffs: 25% Section 232 on steel

- Mills leverage: delivery schedules & minimums

- Ryerson: network softens but not eliminates risk

- Regional shortages boost supplier bargaining

Value-added coil/plate availability

Access to wider coils, plate, and specialty alloys is concentrated among a handful of mills that can bundle favorable and scarce items to shape negotiations; Ryerson’s purchasing scale secures improved allocation during constrained periods but scarcity of certain high-grade alloys maintains elevated supplier power.

- Supplier concentration

- Bundling leverage

- Ryerson scale improves allocation

- Scarce grades sustain supplier power

Supplier leverage tightens as China >50% steel and 25% tariffs squeeze margins

Supplier power in 2024 remained high: China supplied >50% of crude steel, a few mills and smelters controlled allocations, and scarce alloy grades were few-sourced. Ryerson’s multi-mill sourcing and long-term contracts blunt but do not remove leverage; timing mismatches from mill surcharges compressed margins. Trade policy and logistics tightened channels—Section 232 steel tariff at 25% amplified local supplier clout.

| Metric | 2024 |

|---|---|

| China share of crude steel | >50% |

| Section 232 steel tariff | 25% |

| Freight | Capacity tight |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Ryerson, uncovering competitive intensity, supplier and buyer power, and barriers to entry. Highlights disruptive threats, substitutes, and strategic levers to protect market share and pricing power.

One-sheet Ryerson Porter's Five Forces summary that instantly clarifies competitive pressure—perfect for rapid decision-making and cleanly copyable into pitch decks or board slides.

Customers Bargaining Power

Fragmented base but powerful OEMs

Ryerson serves a fragmented SME base that limits individual buyer leverage, but large OEMs in transportation, heavy equipment and energy exert strong negotiating power; industry estimates place the US metal distribution market near $110 billion in 2024, concentrating bargaining with top OEMs. Big accounts routinely demand volume discounts and strict SLAs, and losing a major customer can materially shift sales mix and depress plant utilization.

High price transparency on commodities

In 2024 spot indices from Fastmarkets, Platts and MetalMiner and published surcharges enable easy benchmarking, and buyers can solicit multiple quotes within hours, compressing negotiation and pressuring margins. Ryerson competes on total delivered cost—not just base price—by pricing transport, inventory and surcharge mixes. Transparent markets amplify buyer leverage in oversupplied periods, worsening margin pressure.

Low switching costs for basic products

For standard grades and dimensions alternatives are plentiful and customers can re-source with minimal qualification effort; global crude steel production was about 1.8 billion tonnes in 2024, underscoring broad supplier capacity. Ryerson raises switching costs via downstream processing integration, kitting, and vendor-managed inventory programs. Ultimately, service-level reliability — on-time fills and order accuracy — becomes the primary stickiness factor.

Value-added services dampen leverage

Cutting, slitting, blanking and JIT programs embed Ryerson into customer workflows, making it a logistics and processing partner rather than a commodity supplier. Tailored inventory and staggered release schedules demonstrably reduce customers’ working capital needs and curb pure price-driven switching. Operational integration and near-real-time performance data via EDI links strengthen retention and raise switching costs.

- Service integration: processing + JIT

- Working capital: tailored inventory

- Retention: EDI + performance data

Demand cyclicality sharpens buyer tactics

Demand cyclicality sharpens buyer tactics: in 2024 downturns customers consolidated spend and ran auctions more frequently, increasing lead-time slack and elevating negotiation pressure; in upcycles buyers accepted pass-throughs to secure supply. Ryerson’s diversified contract mix (fixed, index-linked, spot) smooths but does not eliminate cyclic impacts on margins.

- 2024: auction-driven price resets rose notably

- Lead-time slack amplified bargaining leverage

- Pass-throughs more accepted in tight supply

- Contract mix reduces but doesn’t nullify cyclicity

Buyers' leverage compresses metal margins; distributors use processing, JIT and VMI to defend

Buyers have strong leverage: US metal distribution ~ $110B in 2024 and large OEMs concentrate spend, pressing for discounts and SLAs. Transparent spot indices (Fastmarkets/Platts/MetalMiner) and 1.8bn t crude steel supply in 2024 enable rapid re-sourcing, compressing margins. Ryerson offsets via processing, JIT and VMI to raise switching costs and protect utilization.

| Metric | 2024 |

|---|---|

| US market size | $110B |

| Global crude steel | 1.8bn t |

| Indices | Fastmarkets/Platts/MetalMiner |

Full Version Awaits

Ryerson Porter's Five Forces Analysis

This preview shows the Ryerson Porter’s Five Forces Analysis exactly as delivered upon purchase—no mockups, no placeholders. The file is the full, professionally formatted analysis you’ll receive instantly after payment. It’s ready for download and immediate use in presentations, reports, or strategic planning. What you see here is precisely what you’ll get.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Ryerson’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, substitute threats, entry barriers, and rival intensity to reveal where competitive vulnerability and opportunity lie; the concise findings point to strategic levers for margin protection and growth. This brief only scratches the surface—purchase the full report for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated upstream metal producers

In 2024 global crude steel production remained highly concentrated, with China supplying more than half of world tonnage and the largest mills controlling regional allocations and pricing. Aluminum smelters are likewise clustered among a handful of producers, giving upstream suppliers leverage over premiums and lead times. Ryerson’s broad product mix reduces single-grade exposure, but critical grades often remain single- or few-sourced. Long-term contracts and multi-mill sourcing lower but do not eliminate supplier power during tight cycles.

Input price volatility and surcharges

Commodity price swings and mill surcharges (fuel, alloy) in 2024 compressed margins when pass-through to customers lagged, and Ryerson’s published pricing mechanisms and tighter inventory discipline mitigated but did not eliminate timing mismatches. Suppliers in 2024 occasionally enforced price floors or allocation during tight supply windows. Hedging reduced headline volatility but introduced basis and timing risks that persisted across quarters.

Quality specs and certifications

Quality specs and certifications drive supplier power in automotive, energy and aerospace where AS9100, ISO 9001 and Nadcap approvals (as of 2024) narrow qualified vendors and raise switching friction. Mills holding proprietary specs or OEM approvals secure pricing leverage. Ryerson’s approved supplier roster reduces single-supplier dependency but approval cycles slow substitution. Nonconformance risks increase the effective cost of pushing back on terms.

Logistics and lead-time constraints

Freight capacity squeeze, import controls and the continued 25% Section 232 steel tariff in 2024 tighten supply channels, letting mills use delivery schedules and minimums to pressure service-center margins; Ryerson’s broad branch network and mixed-mode logistics mitigate but cannot fully offset systemic lead-time and capacity limits, and regional steel shortages raise local supplier clout.

- Freight capacity: tight in 2024

- Tariffs: 25% Section 232 on steel

- Mills leverage: delivery schedules & minimums

- Ryerson: network softens but not eliminates risk

- Regional shortages boost supplier bargaining

Value-added coil/plate availability

Access to wider coils, plate, and specialty alloys is concentrated among a handful of mills that can bundle favorable and scarce items to shape negotiations; Ryerson’s purchasing scale secures improved allocation during constrained periods but scarcity of certain high-grade alloys maintains elevated supplier power.

- Supplier concentration

- Bundling leverage

- Ryerson scale improves allocation

- Scarce grades sustain supplier power

Supplier leverage tightens as China >50% steel and 25% tariffs squeeze margins

Supplier power in 2024 remained high: China supplied >50% of crude steel, a few mills and smelters controlled allocations, and scarce alloy grades were few-sourced. Ryerson’s multi-mill sourcing and long-term contracts blunt but do not remove leverage; timing mismatches from mill surcharges compressed margins. Trade policy and logistics tightened channels—Section 232 steel tariff at 25% amplified local supplier clout.

| Metric | 2024 |

|---|---|

| China share of crude steel | >50% |

| Section 232 steel tariff | 25% |

| Freight | Capacity tight |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Ryerson, uncovering competitive intensity, supplier and buyer power, and barriers to entry. Highlights disruptive threats, substitutes, and strategic levers to protect market share and pricing power.

One-sheet Ryerson Porter's Five Forces summary that instantly clarifies competitive pressure—perfect for rapid decision-making and cleanly copyable into pitch decks or board slides.

Customers Bargaining Power

Fragmented base but powerful OEMs

Ryerson serves a fragmented SME base that limits individual buyer leverage, but large OEMs in transportation, heavy equipment and energy exert strong negotiating power; industry estimates place the US metal distribution market near $110 billion in 2024, concentrating bargaining with top OEMs. Big accounts routinely demand volume discounts and strict SLAs, and losing a major customer can materially shift sales mix and depress plant utilization.

High price transparency on commodities

In 2024 spot indices from Fastmarkets, Platts and MetalMiner and published surcharges enable easy benchmarking, and buyers can solicit multiple quotes within hours, compressing negotiation and pressuring margins. Ryerson competes on total delivered cost—not just base price—by pricing transport, inventory and surcharge mixes. Transparent markets amplify buyer leverage in oversupplied periods, worsening margin pressure.

Low switching costs for basic products

For standard grades and dimensions alternatives are plentiful and customers can re-source with minimal qualification effort; global crude steel production was about 1.8 billion tonnes in 2024, underscoring broad supplier capacity. Ryerson raises switching costs via downstream processing integration, kitting, and vendor-managed inventory programs. Ultimately, service-level reliability — on-time fills and order accuracy — becomes the primary stickiness factor.

Value-added services dampen leverage

Cutting, slitting, blanking and JIT programs embed Ryerson into customer workflows, making it a logistics and processing partner rather than a commodity supplier. Tailored inventory and staggered release schedules demonstrably reduce customers’ working capital needs and curb pure price-driven switching. Operational integration and near-real-time performance data via EDI links strengthen retention and raise switching costs.

- Service integration: processing + JIT

- Working capital: tailored inventory

- Retention: EDI + performance data

Demand cyclicality sharpens buyer tactics

Demand cyclicality sharpens buyer tactics: in 2024 downturns customers consolidated spend and ran auctions more frequently, increasing lead-time slack and elevating negotiation pressure; in upcycles buyers accepted pass-throughs to secure supply. Ryerson’s diversified contract mix (fixed, index-linked, spot) smooths but does not eliminate cyclic impacts on margins.

- 2024: auction-driven price resets rose notably

- Lead-time slack amplified bargaining leverage

- Pass-throughs more accepted in tight supply

- Contract mix reduces but doesn’t nullify cyclicity

Buyers' leverage compresses metal margins; distributors use processing, JIT and VMI to defend

Buyers have strong leverage: US metal distribution ~ $110B in 2024 and large OEMs concentrate spend, pressing for discounts and SLAs. Transparent spot indices (Fastmarkets/Platts/MetalMiner) and 1.8bn t crude steel supply in 2024 enable rapid re-sourcing, compressing margins. Ryerson offsets via processing, JIT and VMI to raise switching costs and protect utilization.

| Metric | 2024 |

|---|---|

| US market size | $110B |

| Global crude steel | 1.8bn t |

| Indices | Fastmarkets/Platts/MetalMiner |

Full Version Awaits

Ryerson Porter's Five Forces Analysis

This preview shows the Ryerson Porter’s Five Forces Analysis exactly as delivered upon purchase—no mockups, no placeholders. The file is the full, professionally formatted analysis you’ll receive instantly after payment. It’s ready for download and immediate use in presentations, reports, or strategic planning. What you see here is precisely what you’ll get.