SAKURA Internet Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

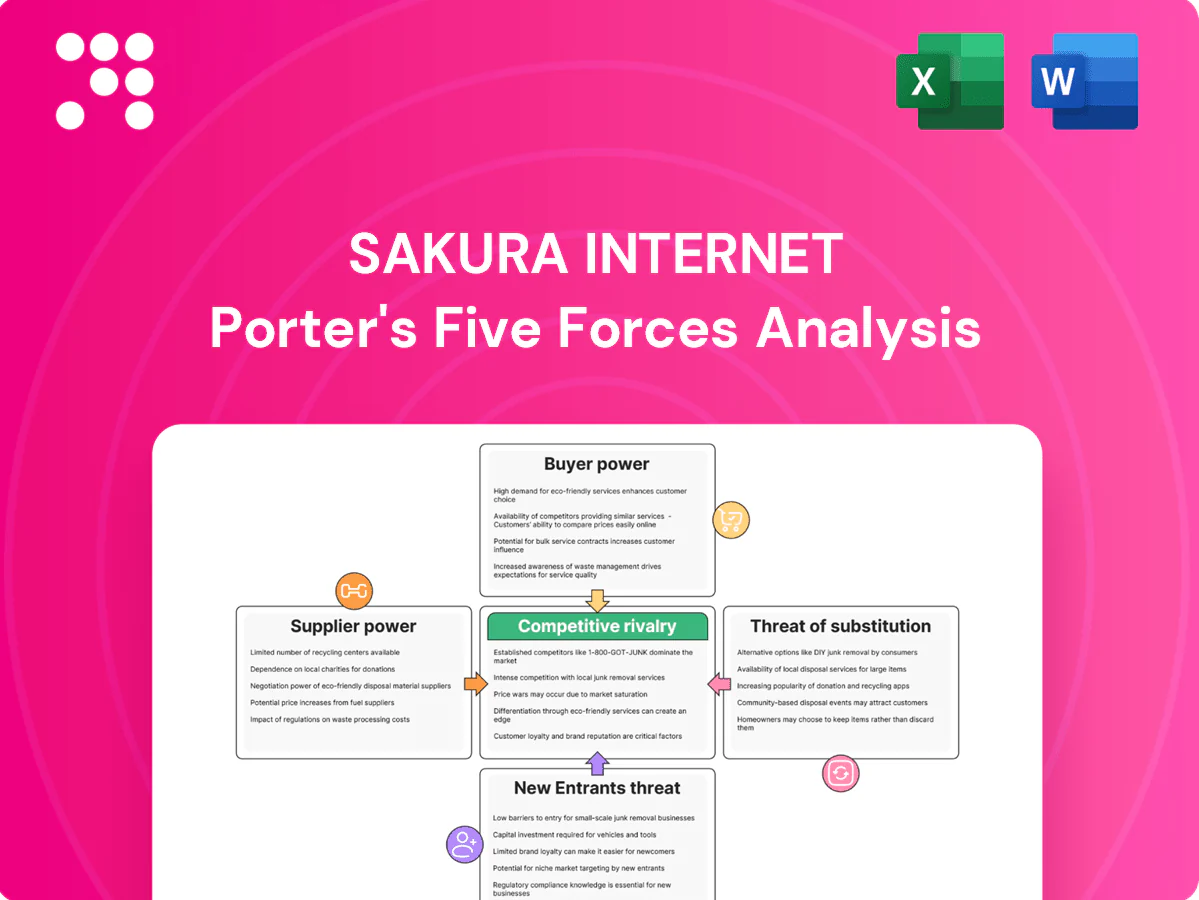

SAKURA Internet faces moderate supplier leverage due to specialized data-center hardware and high switching costs, while buyer power is tempered by enterprise contracts and differentiated services. Competitive rivalry is intense from cloud giants and local ISPs, and threat of entrants remains low given capital intensity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SAKURA Internet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Power, network, and land concentration

Energy utilities and major carriers (NTT group, KDDI, SoftBank) are concentrated suppliers in Japan, with NTT holding over 70% of the fixed-line fiber market in 2024, giving telcos pricing and SLA leverage due to limited right-of-way and substation access. Scarce urban land—Tokyo 23‑ward density ~15,000/km2—and seismic-grade site requirements raise site costs and reduce locational flexibility. SAKURA mitigates this via multi-site design and regional diversification.

Hardware and chip vendor dependence

Server OEMs are concentrated—Dell, HPE and Lenovo held roughly 53% of server revenue in 2023—and CPU/GPU supply is dominated by Intel/AMD/NVIDIA, creating months-to-quarters lead times and periodic shortages that pressure margins and capacity planning. Specialty parts for high-density and liquid cooling further limit suppliers. Qualifying multi-vendor stacks and open hardware (OCP, disaggregated designs) reduces lock-in and procurement risk.

Network transit and peering terms

Tier-1/2 carriers and IX operators (notably JPIX and JPNAP) set transit costs and interconnection quality, directly shaping SAKURA’s unit economics. Changes in peering policies or port pricing can materially alter performance costs and margin on hosting and cloud services. Tokyo and Osaka are dense peering hubs with JPIX/JPNAP connecting hundreds of networks, partially offsetting carrier leverage. SAKURA (TYO:3778) maintains its own backbone and IX presence, strengthening its negotiating position.

Software licensing and OSS ecosystems

Proprietary virtualization, database and security licenses commonly impose per-core or per-socket costs ranging from thousands to tens of thousands of dollars per socket annually; open-source software (OSS) cuts license fees but shifts dependence to community roadmaps and internal support capability. Vendor audits remain a material compliance risk with frequent multi‑hundred‑thousand to multi‑million dollar adjustments reported. A hybrid stack is the prevailing 2024 response to balance cost control and operational reliability.

- Per-core/socket fees: high and variable

- OSS: lower fees, higher internal support need

- Vendor audits: measurable financial risk

- Hybrid stack: ~60%+ enterprise adoption in 2024

Construction and cooling vendors

Construction and cooling vendors hold moderate-to-high supplier power for SAKURA due to a small pool of Japan-standard specialized EPCs, modular data-center builders and HVAC suppliers; lead times for chillers, generators and batteries stretched to roughly 3–9 months in 2024, delaying rollouts and tying up project liquidity. Material price volatility has driven local capex overruns, while framework agreements and pre-procurement materially reduce supply risk and schedule exposure.

- supplier concentration: limited specialized vendors

- lead times: chillers/generators/batteries ~3–9 months (2024)

- risk: material price spikes → capex overruns

- mitigation: framework agreements, pre-procurement

Concentrated suppliers, high license fees and 3-9 month lead times raise datacenter capex risk

Suppliers exert moderate-to-high power: NTT controls >70% of fixed-line fiber (2024) and carriers/IXs set transit pricing; Dell/HPE/Lenovo held ~53% server revenue (2023) while Intel/AMD/NVIDIA dominate CPUs/GPUs. License fees cost thousands–tens thousands $/socket/yr; chillers/gens/batteries lead times 3–9 months (2024), raising capex risk. SAKURA uses multi-vendor stacks, hybrid licensing and own backbone to mitigate.

| Item | Metric/2024 |

|---|---|

| NTT fiber share | >70% |

| Server OEMs (2023) | 53% |

| License cost | $k–$10k+/socket/yr |

| Cooling lead time | 3–9 months |

What is included in the product

Tailored Porter's Five Forces analysis for SAKURA Internet, uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptors—actionable insights for strategy and investor materials.

A clear, one-sheet summary of SAKURA Internet's Five Forces—perfect for quick strategic decisions and investor decks. Swap in your own data and instantly visualize competitive pressure with a radar chart for boardroom-ready insights.

Customers Bargaining Power

Commoditized IaaS pricing

Compute, storage and bandwidth are highly transparent and comparable across providers; 2024 global cloud market shares were AWS 31%, Microsoft 24%, Google 11% (Synergy Research Group), enabling buyers to benchmark unit costs and demand discounts. This compresses margins and shifts competition to total cost of ownership. Bundled services and reserved pricing (Savings Plans/Reserved Instances discounts up to 72%) can defend ARPU.

Enterprise and public-sector negotiating clout

Enterprise and public-sector deals drive concentrated revenue for SAKURA Internet as buyers use RFPs to extract tailored SLAs, compliance attestations and integration support; Japan public cloud spending rose to about ¥2.0 trillion in 2024, up ~18.5% (IDC), intensifying procurement leverage. This RFP-driven demand raises concession pressure on pricing and service levels, though multi-year contracts still lock in volume stability and predictable cash flow.

Switching costs vs data gravity

Data migration and refactoring create friction but are increasingly manageable with tooling and professional services; 2024 Flexera data shows 92% of enterprises pursue multi-cloud, reducing dependence on one vendor. Egress fees (AWS data transfer out to internet ~0.09 USD/GB for first 10 TB) and cross-region latency (tens of ms) raise effective switching costs. Proactive migration support helps retain accounts.

Performance and locality sensitivity

Japan-based users prioritize low latency, domestic data residency, and Japanese-language support, so where these are critical buyer power is moderated because local alternatives like SAKURA Internet (as of 2024 operating multiple Japan data centers) remain limited; for generic workloads buyer power rises as global hyperscalers expand. Local compliance and language support often act as tie-breakers in procurement.

- low-latency sensitivity

- domestic-residency strength

- language/compliance tie-breaker

- global options boost buyer power

Demand volatility in SMEs

SME customers are highly price-sensitive and churn-prone with bursty usage patterns, intensifying buyer power; SMEs account for 99.7% of Japanese firms (METI, 2024), so this segment drives volume-sensitive pricing. Monthly shopping for rates and promos amplifies switching; self-service onboarding and exits reduce switching friction, while sticky value-adds and predictable bundles can stabilize retention.

- Price-sensitive: monthly rate shoppers

- Churn-prone: bursty usage spikes

- Low friction: self-service exits

- Mitigation: sticky add-ons, predictable bundles

Price transparency compresses margins; Japan cloud spend ¥2.0T

Customers have high price transparency (AWS 31%, Microsoft 24%, Google 11% in 2024, Synergy) and strong leverage, compressing margins; enterprise RFPs and Japan public cloud spend ~¥2.0T (+18.5% in 2024, IDC) intensify concession pressure. Multi-cloud adoption (92% enterprises, Flexera 2024) and SME price-sensitivity (99.7% of firms, METI 2024) raise churn risk, while domestic low-latency/residency needs (SAKURA Japan data centers, 2024) moderate power.

| Metric | 2024 Value |

|---|---|

| Global cloud share (AWS/MS/Google) | 31% / 24% / 11% |

| Japan public cloud spend | ¥2.0T (+18.5%) |

| Enterprises multi-cloud | 92% |

| SME share of firms (Japan) | 99.7% |

| AWS egress fee (first 10 TB) | ~0.09 USD/GB |

Same Document Delivered

SAKURA Internet Porter's Five Forces Analysis

This preview shows the exact SAKURA Internet Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the final deliverable, identical to the file you will get.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

SAKURA Internet faces moderate supplier leverage due to specialized data-center hardware and high switching costs, while buyer power is tempered by enterprise contracts and differentiated services. Competitive rivalry is intense from cloud giants and local ISPs, and threat of entrants remains low given capital intensity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SAKURA Internet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Power, network, and land concentration

Energy utilities and major carriers (NTT group, KDDI, SoftBank) are concentrated suppliers in Japan, with NTT holding over 70% of the fixed-line fiber market in 2024, giving telcos pricing and SLA leverage due to limited right-of-way and substation access. Scarce urban land—Tokyo 23‑ward density ~15,000/km2—and seismic-grade site requirements raise site costs and reduce locational flexibility. SAKURA mitigates this via multi-site design and regional diversification.

Hardware and chip vendor dependence

Server OEMs are concentrated—Dell, HPE and Lenovo held roughly 53% of server revenue in 2023—and CPU/GPU supply is dominated by Intel/AMD/NVIDIA, creating months-to-quarters lead times and periodic shortages that pressure margins and capacity planning. Specialty parts for high-density and liquid cooling further limit suppliers. Qualifying multi-vendor stacks and open hardware (OCP, disaggregated designs) reduces lock-in and procurement risk.

Network transit and peering terms

Tier-1/2 carriers and IX operators (notably JPIX and JPNAP) set transit costs and interconnection quality, directly shaping SAKURA’s unit economics. Changes in peering policies or port pricing can materially alter performance costs and margin on hosting and cloud services. Tokyo and Osaka are dense peering hubs with JPIX/JPNAP connecting hundreds of networks, partially offsetting carrier leverage. SAKURA (TYO:3778) maintains its own backbone and IX presence, strengthening its negotiating position.

Software licensing and OSS ecosystems

Proprietary virtualization, database and security licenses commonly impose per-core or per-socket costs ranging from thousands to tens of thousands of dollars per socket annually; open-source software (OSS) cuts license fees but shifts dependence to community roadmaps and internal support capability. Vendor audits remain a material compliance risk with frequent multi‑hundred‑thousand to multi‑million dollar adjustments reported. A hybrid stack is the prevailing 2024 response to balance cost control and operational reliability.

- Per-core/socket fees: high and variable

- OSS: lower fees, higher internal support need

- Vendor audits: measurable financial risk

- Hybrid stack: ~60%+ enterprise adoption in 2024

Construction and cooling vendors

Construction and cooling vendors hold moderate-to-high supplier power for SAKURA due to a small pool of Japan-standard specialized EPCs, modular data-center builders and HVAC suppliers; lead times for chillers, generators and batteries stretched to roughly 3–9 months in 2024, delaying rollouts and tying up project liquidity. Material price volatility has driven local capex overruns, while framework agreements and pre-procurement materially reduce supply risk and schedule exposure.

- supplier concentration: limited specialized vendors

- lead times: chillers/generators/batteries ~3–9 months (2024)

- risk: material price spikes → capex overruns

- mitigation: framework agreements, pre-procurement

Concentrated suppliers, high license fees and 3-9 month lead times raise datacenter capex risk

Suppliers exert moderate-to-high power: NTT controls >70% of fixed-line fiber (2024) and carriers/IXs set transit pricing; Dell/HPE/Lenovo held ~53% server revenue (2023) while Intel/AMD/NVIDIA dominate CPUs/GPUs. License fees cost thousands–tens thousands $/socket/yr; chillers/gens/batteries lead times 3–9 months (2024), raising capex risk. SAKURA uses multi-vendor stacks, hybrid licensing and own backbone to mitigate.

| Item | Metric/2024 |

|---|---|

| NTT fiber share | >70% |

| Server OEMs (2023) | 53% |

| License cost | $k–$10k+/socket/yr |

| Cooling lead time | 3–9 months |

What is included in the product

Tailored Porter's Five Forces analysis for SAKURA Internet, uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptors—actionable insights for strategy and investor materials.

A clear, one-sheet summary of SAKURA Internet's Five Forces—perfect for quick strategic decisions and investor decks. Swap in your own data and instantly visualize competitive pressure with a radar chart for boardroom-ready insights.

Customers Bargaining Power

Commoditized IaaS pricing

Compute, storage and bandwidth are highly transparent and comparable across providers; 2024 global cloud market shares were AWS 31%, Microsoft 24%, Google 11% (Synergy Research Group), enabling buyers to benchmark unit costs and demand discounts. This compresses margins and shifts competition to total cost of ownership. Bundled services and reserved pricing (Savings Plans/Reserved Instances discounts up to 72%) can defend ARPU.

Enterprise and public-sector negotiating clout

Enterprise and public-sector deals drive concentrated revenue for SAKURA Internet as buyers use RFPs to extract tailored SLAs, compliance attestations and integration support; Japan public cloud spending rose to about ¥2.0 trillion in 2024, up ~18.5% (IDC), intensifying procurement leverage. This RFP-driven demand raises concession pressure on pricing and service levels, though multi-year contracts still lock in volume stability and predictable cash flow.

Switching costs vs data gravity

Data migration and refactoring create friction but are increasingly manageable with tooling and professional services; 2024 Flexera data shows 92% of enterprises pursue multi-cloud, reducing dependence on one vendor. Egress fees (AWS data transfer out to internet ~0.09 USD/GB for first 10 TB) and cross-region latency (tens of ms) raise effective switching costs. Proactive migration support helps retain accounts.

Performance and locality sensitivity

Japan-based users prioritize low latency, domestic data residency, and Japanese-language support, so where these are critical buyer power is moderated because local alternatives like SAKURA Internet (as of 2024 operating multiple Japan data centers) remain limited; for generic workloads buyer power rises as global hyperscalers expand. Local compliance and language support often act as tie-breakers in procurement.

- low-latency sensitivity

- domestic-residency strength

- language/compliance tie-breaker

- global options boost buyer power

Demand volatility in SMEs

SME customers are highly price-sensitive and churn-prone with bursty usage patterns, intensifying buyer power; SMEs account for 99.7% of Japanese firms (METI, 2024), so this segment drives volume-sensitive pricing. Monthly shopping for rates and promos amplifies switching; self-service onboarding and exits reduce switching friction, while sticky value-adds and predictable bundles can stabilize retention.

- Price-sensitive: monthly rate shoppers

- Churn-prone: bursty usage spikes

- Low friction: self-service exits

- Mitigation: sticky add-ons, predictable bundles

Price transparency compresses margins; Japan cloud spend ¥2.0T

Customers have high price transparency (AWS 31%, Microsoft 24%, Google 11% in 2024, Synergy) and strong leverage, compressing margins; enterprise RFPs and Japan public cloud spend ~¥2.0T (+18.5% in 2024, IDC) intensify concession pressure. Multi-cloud adoption (92% enterprises, Flexera 2024) and SME price-sensitivity (99.7% of firms, METI 2024) raise churn risk, while domestic low-latency/residency needs (SAKURA Japan data centers, 2024) moderate power.

| Metric | 2024 Value |

|---|---|

| Global cloud share (AWS/MS/Google) | 31% / 24% / 11% |

| Japan public cloud spend | ¥2.0T (+18.5%) |

| Enterprises multi-cloud | 92% |

| SME share of firms (Japan) | 99.7% |

| AWS egress fee (first 10 TB) | ~0.09 USD/GB |

Same Document Delivered

SAKURA Internet Porter's Five Forces Analysis

This preview shows the exact SAKURA Internet Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the final deliverable, identical to the file you will get.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

SAKURA Internet faces moderate supplier leverage due to specialized data-center hardware and high switching costs, while buyer power is tempered by enterprise contracts and differentiated services. Competitive rivalry is intense from cloud giants and local ISPs, and threat of entrants remains low given capital intensity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SAKURA Internet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Power, network, and land concentration

Energy utilities and major carriers (NTT group, KDDI, SoftBank) are concentrated suppliers in Japan, with NTT holding over 70% of the fixed-line fiber market in 2024, giving telcos pricing and SLA leverage due to limited right-of-way and substation access. Scarce urban land—Tokyo 23‑ward density ~15,000/km2—and seismic-grade site requirements raise site costs and reduce locational flexibility. SAKURA mitigates this via multi-site design and regional diversification.

Hardware and chip vendor dependence

Server OEMs are concentrated—Dell, HPE and Lenovo held roughly 53% of server revenue in 2023—and CPU/GPU supply is dominated by Intel/AMD/NVIDIA, creating months-to-quarters lead times and periodic shortages that pressure margins and capacity planning. Specialty parts for high-density and liquid cooling further limit suppliers. Qualifying multi-vendor stacks and open hardware (OCP, disaggregated designs) reduces lock-in and procurement risk.

Network transit and peering terms

Tier-1/2 carriers and IX operators (notably JPIX and JPNAP) set transit costs and interconnection quality, directly shaping SAKURA’s unit economics. Changes in peering policies or port pricing can materially alter performance costs and margin on hosting and cloud services. Tokyo and Osaka are dense peering hubs with JPIX/JPNAP connecting hundreds of networks, partially offsetting carrier leverage. SAKURA (TYO:3778) maintains its own backbone and IX presence, strengthening its negotiating position.

Software licensing and OSS ecosystems

Proprietary virtualization, database and security licenses commonly impose per-core or per-socket costs ranging from thousands to tens of thousands of dollars per socket annually; open-source software (OSS) cuts license fees but shifts dependence to community roadmaps and internal support capability. Vendor audits remain a material compliance risk with frequent multi‑hundred‑thousand to multi‑million dollar adjustments reported. A hybrid stack is the prevailing 2024 response to balance cost control and operational reliability.

- Per-core/socket fees: high and variable

- OSS: lower fees, higher internal support need

- Vendor audits: measurable financial risk

- Hybrid stack: ~60%+ enterprise adoption in 2024

Construction and cooling vendors

Construction and cooling vendors hold moderate-to-high supplier power for SAKURA due to a small pool of Japan-standard specialized EPCs, modular data-center builders and HVAC suppliers; lead times for chillers, generators and batteries stretched to roughly 3–9 months in 2024, delaying rollouts and tying up project liquidity. Material price volatility has driven local capex overruns, while framework agreements and pre-procurement materially reduce supply risk and schedule exposure.

- supplier concentration: limited specialized vendors

- lead times: chillers/generators/batteries ~3–9 months (2024)

- risk: material price spikes → capex overruns

- mitigation: framework agreements, pre-procurement

Concentrated suppliers, high license fees and 3-9 month lead times raise datacenter capex risk

Suppliers exert moderate-to-high power: NTT controls >70% of fixed-line fiber (2024) and carriers/IXs set transit pricing; Dell/HPE/Lenovo held ~53% server revenue (2023) while Intel/AMD/NVIDIA dominate CPUs/GPUs. License fees cost thousands–tens thousands $/socket/yr; chillers/gens/batteries lead times 3–9 months (2024), raising capex risk. SAKURA uses multi-vendor stacks, hybrid licensing and own backbone to mitigate.

| Item | Metric/2024 |

|---|---|

| NTT fiber share | >70% |

| Server OEMs (2023) | 53% |

| License cost | $k–$10k+/socket/yr |

| Cooling lead time | 3–9 months |

What is included in the product

Tailored Porter's Five Forces analysis for SAKURA Internet, uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptors—actionable insights for strategy and investor materials.

A clear, one-sheet summary of SAKURA Internet's Five Forces—perfect for quick strategic decisions and investor decks. Swap in your own data and instantly visualize competitive pressure with a radar chart for boardroom-ready insights.

Customers Bargaining Power

Commoditized IaaS pricing

Compute, storage and bandwidth are highly transparent and comparable across providers; 2024 global cloud market shares were AWS 31%, Microsoft 24%, Google 11% (Synergy Research Group), enabling buyers to benchmark unit costs and demand discounts. This compresses margins and shifts competition to total cost of ownership. Bundled services and reserved pricing (Savings Plans/Reserved Instances discounts up to 72%) can defend ARPU.

Enterprise and public-sector negotiating clout

Enterprise and public-sector deals drive concentrated revenue for SAKURA Internet as buyers use RFPs to extract tailored SLAs, compliance attestations and integration support; Japan public cloud spending rose to about ¥2.0 trillion in 2024, up ~18.5% (IDC), intensifying procurement leverage. This RFP-driven demand raises concession pressure on pricing and service levels, though multi-year contracts still lock in volume stability and predictable cash flow.

Switching costs vs data gravity

Data migration and refactoring create friction but are increasingly manageable with tooling and professional services; 2024 Flexera data shows 92% of enterprises pursue multi-cloud, reducing dependence on one vendor. Egress fees (AWS data transfer out to internet ~0.09 USD/GB for first 10 TB) and cross-region latency (tens of ms) raise effective switching costs. Proactive migration support helps retain accounts.

Performance and locality sensitivity

Japan-based users prioritize low latency, domestic data residency, and Japanese-language support, so where these are critical buyer power is moderated because local alternatives like SAKURA Internet (as of 2024 operating multiple Japan data centers) remain limited; for generic workloads buyer power rises as global hyperscalers expand. Local compliance and language support often act as tie-breakers in procurement.

- low-latency sensitivity

- domestic-residency strength

- language/compliance tie-breaker

- global options boost buyer power

Demand volatility in SMEs

SME customers are highly price-sensitive and churn-prone with bursty usage patterns, intensifying buyer power; SMEs account for 99.7% of Japanese firms (METI, 2024), so this segment drives volume-sensitive pricing. Monthly shopping for rates and promos amplifies switching; self-service onboarding and exits reduce switching friction, while sticky value-adds and predictable bundles can stabilize retention.

- Price-sensitive: monthly rate shoppers

- Churn-prone: bursty usage spikes

- Low friction: self-service exits

- Mitigation: sticky add-ons, predictable bundles

Price transparency compresses margins; Japan cloud spend ¥2.0T

Customers have high price transparency (AWS 31%, Microsoft 24%, Google 11% in 2024, Synergy) and strong leverage, compressing margins; enterprise RFPs and Japan public cloud spend ~¥2.0T (+18.5% in 2024, IDC) intensify concession pressure. Multi-cloud adoption (92% enterprises, Flexera 2024) and SME price-sensitivity (99.7% of firms, METI 2024) raise churn risk, while domestic low-latency/residency needs (SAKURA Japan data centers, 2024) moderate power.

| Metric | 2024 Value |

|---|---|

| Global cloud share (AWS/MS/Google) | 31% / 24% / 11% |

| Japan public cloud spend | ¥2.0T (+18.5%) |

| Enterprises multi-cloud | 92% |

| SME share of firms (Japan) | 99.7% |

| AWS egress fee (first 10 TB) | ~0.09 USD/GB |

Same Document Delivered

SAKURA Internet Porter's Five Forces Analysis

This preview shows the exact SAKURA Internet Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the final deliverable, identical to the file you will get.