Sallie Mae Business Model Canvas

Business Model Canvas for a Major Student-Lending Firm: Strategy, Revenue & Risk Map

Unlock the full strategic blueprint behind Sallie Mae’s business model with our in-depth Business Model Canvas; it maps value propositions, revenue streams, partnerships, and cost structure to show how the company scales and manages risk. Ideal for investors, consultants, and founders seeking actionable insights and benchmarking tools. Download the complete Word and Excel files to analyze, adapt, and apply Sallie Mae’s proven strategies today.

Partnerships

Universities & Financial Aid Offices

Collaborate with schools to embed Sallie Mae private loan options into financial aid workflows, capturing students at key decision points and leveraging campus channels to reach over 7 million customers. Coordinate certification, disbursement, and enrollment verification to speed funding and reduce default risk. Support on-campus financial literacy programs; in 2024 Sallie Mae reported over $5B in private student loan originations, reinforcing campus partnerships.

Credit Bureaus & Data Providers

Partnerships with credit bureaus (Experian, TransUnion, Equifax report over 1 billion consumer records globally in 2024) provide Sallie Mae access to credit histories, income verification signals and alternative data for underwriting and improved risk segmentation.

These feeds enable ongoing performance monitoring, early delinquency detection and dynamic pricing to tighten loss forecasts.

Integration supports compliance with FCRA and ECOA reporting and fair lending requirements through auditable data trails.

Capital Markets & Securitization Partners

Sallie Mae partners with underwriters, trustees and institutional investors to securitize private education loan pools, and as of 2024 continues to diversify funding sources to optimize cost of capital and manage its balance sheet. The bank uses warehouse lines and whole-loan buyers to scale originations and transfer risk while maintaining liquidity. Ongoing investor relations and transparency practices support market access and pricing discipline in 2024.

Fintech & Servicing Technology Vendors

Regulators & Compliance Advisors

- Engage regulators

- Align disclosures & capital

- Audit & remediate with experts

Partnerships + credit APIs drive 7M+ users, $5B orig.

Key partnerships with 7M+ campus channels, credit bureaus, underwriters, fintech vendors and regulators drive originations, underwriting, funding and compliance; 2024 origins ~$5B. Credit bureau feeds and APIs enable dynamic pricing and early risk detection; DocuSign FY2024 revenue $2.57B supports e-signature scale. Securitization and investor relations diversify funding and manage capital cost.

| Partner | 2024 Metric |

|---|---|

| Campus channels | 7M+ customers |

| Private loans | $5B originations |

What is included in the product

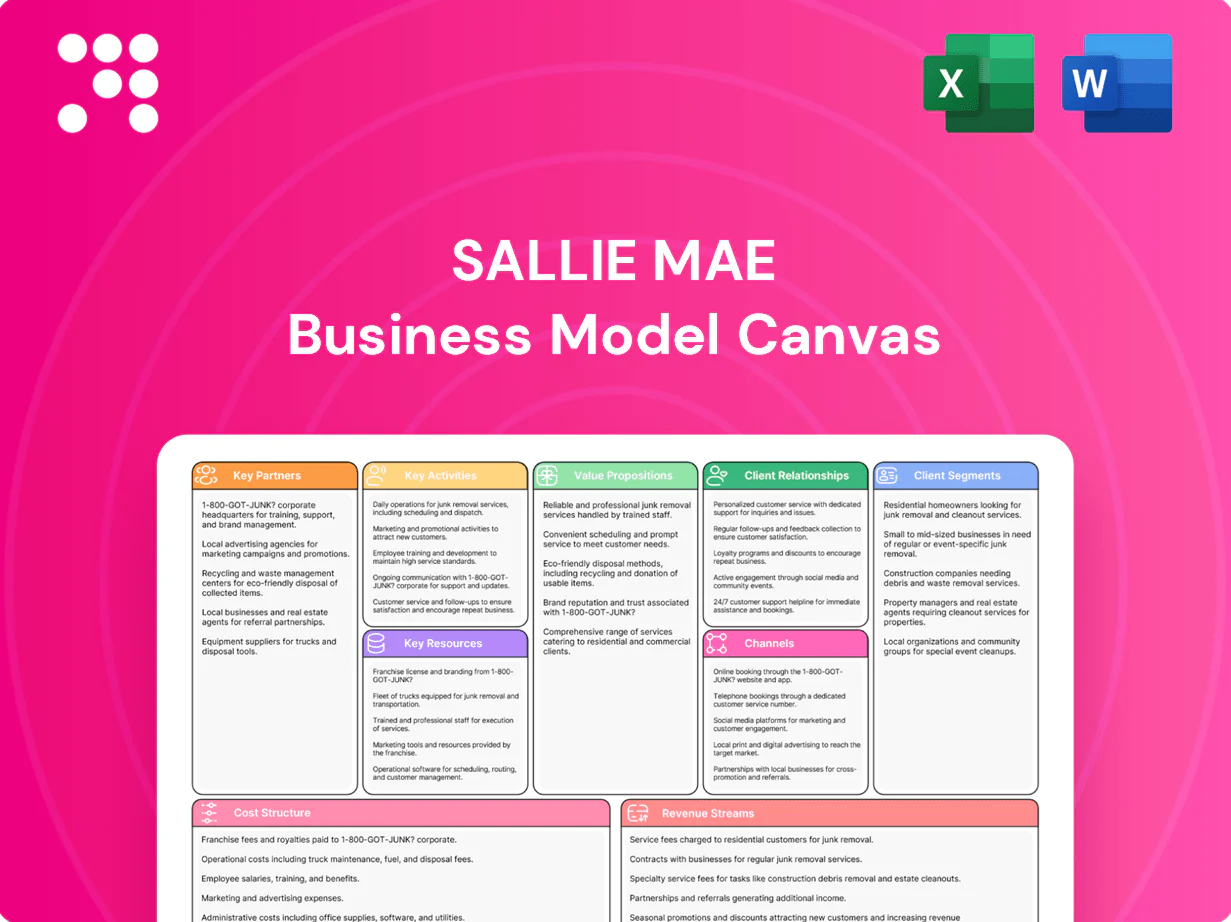

A comprehensive Sallie Mae Business Model Canvas aligned to the company’s student-lending strategy, covering customer segments, value propositions, channels, revenue streams, cost structure and partners across the 9 classic BMC blocks. Ideal for presentations and investor discussions, it includes narrative insights, competitive advantages and linked SWOT analysis to support strategic decisions and validation using real-world data.

High-level, shareable one-page canvas that distills Sallie Mae’s lending, servicing, and partnership model into editable cells to relieve analysis and presentation pain points.

Activities

Credit Underwriting & Pricing

Assess borrower and cosigner risk using bureau data and internal models, targeting loss rates consistent with SLM risk tolerance while referencing market conditions; in 2024 the Federal Reserve policy rate near 5.25–5.50% tightened funding costs and informed pricing. Price loans to reflect credit tier, term and market rates, balancing approval rates with portfolio quality and return targets. Continuously recalibrate cutoffs and APRs based on performance and bureau score migrations.

Loan Origination & Servicing

Streamline application, certification, and disbursement workflows to shorten origination time and improve underwriting accuracy. Manage billing, payments, escrow, and statements across accounts while handling deferment, forbearance, and cosigner release workflows. Drive digital self-service to lower costs—industry studies show self-service can cut servicing costs by up to 40%.

Funding & Securitization

Funding & Securitization sources include retail deposits and wholesale debt to support loan growth; in 2024 Sallie Mae leaned on bank deposits and covered ABS programs to diversify funding. The firm executed multiple ABS transactions and maintained investor reporting cadence for transparency. Treasury optimizes liquidity, capital and interest-rate exposures while hedging and laddering maturities to reduce reinvestment and rate risk.

Digital Product & CX Management

Optimize web/app funnels, prequalification flows, and instant-decision engines to shorten application time and improve approval clarity for Sallie Mae borrowers.

Run continuous A/B testing to lift conversion and reduce abandonment, reinforce accessibility standards and mobile-first features, and integrate calculators and educational content to boost informed conversions.

- funnel optimization

- A/B testing

- accessibility & mobile

- education tools & calculators

Risk, Compliance & Collections

Sallie Mae (SLM) monitors credit, fraud, operational and regulatory risks across its loan portfolio, which exceeds $40 billion, using centralized policies, recurring control testing and targeted training programs.

Collections teams manage early-stage delinquency and recovery strategies, applying predictive analytics and segmentation to reduce cure times and lower charge-offs.

- Risk tags: credit, fraud, ops, regulatory

- Controls: policies, training, testing

- Collections: early-stage focus, recovery playbooks

- Analytics: predictive models to cut charge-offs

Assess borrower risk, price loans; Fed 5.25–5.50%, portfolio >$40B

Assess borrower/cosigner risk with bureau data and internal models to price loans across credit tiers; 2024 Fed policy rate ~5.25–5.50% tightened funding and informed APRs. Streamline digital origination, servicing and collections to cut costs and charge-offs; self-service can lower servicing costs up to 40%. Fund via bank deposits and ABS, with treasury hedging liquidity and rate exposures for a >$40B loan portfolio.

| Metric | 2024 |

|---|---|

| Loan portfolio | >$40B |

| Fed policy rate | 5.25–5.50% |

| Servicing cost cut | up to 40% |

| Funding | Bank deposits + ABS |

Full Document Unlocks After Purchase

Business Model Canvas

The Sallie Mae Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the same content and layout you’ll receive after purchase. When you buy, you’ll download this identical, fully editable document in Word and Excel formats. No fillers, no surprises—ready to present or adapt.

Business Model Canvas for a Major Student-Lending Firm: Strategy, Revenue & Risk Map

Unlock the full strategic blueprint behind Sallie Mae’s business model with our in-depth Business Model Canvas; it maps value propositions, revenue streams, partnerships, and cost structure to show how the company scales and manages risk. Ideal for investors, consultants, and founders seeking actionable insights and benchmarking tools. Download the complete Word and Excel files to analyze, adapt, and apply Sallie Mae’s proven strategies today.

Partnerships

Universities & Financial Aid Offices

Collaborate with schools to embed Sallie Mae private loan options into financial aid workflows, capturing students at key decision points and leveraging campus channels to reach over 7 million customers. Coordinate certification, disbursement, and enrollment verification to speed funding and reduce default risk. Support on-campus financial literacy programs; in 2024 Sallie Mae reported over $5B in private student loan originations, reinforcing campus partnerships.

Credit Bureaus & Data Providers

Partnerships with credit bureaus (Experian, TransUnion, Equifax report over 1 billion consumer records globally in 2024) provide Sallie Mae access to credit histories, income verification signals and alternative data for underwriting and improved risk segmentation.

These feeds enable ongoing performance monitoring, early delinquency detection and dynamic pricing to tighten loss forecasts.

Integration supports compliance with FCRA and ECOA reporting and fair lending requirements through auditable data trails.

Capital Markets & Securitization Partners

Sallie Mae partners with underwriters, trustees and institutional investors to securitize private education loan pools, and as of 2024 continues to diversify funding sources to optimize cost of capital and manage its balance sheet. The bank uses warehouse lines and whole-loan buyers to scale originations and transfer risk while maintaining liquidity. Ongoing investor relations and transparency practices support market access and pricing discipline in 2024.

Fintech & Servicing Technology Vendors

Regulators & Compliance Advisors

- Engage regulators

- Align disclosures & capital

- Audit & remediate with experts

Partnerships + credit APIs drive 7M+ users, $5B orig.

Key partnerships with 7M+ campus channels, credit bureaus, underwriters, fintech vendors and regulators drive originations, underwriting, funding and compliance; 2024 origins ~$5B. Credit bureau feeds and APIs enable dynamic pricing and early risk detection; DocuSign FY2024 revenue $2.57B supports e-signature scale. Securitization and investor relations diversify funding and manage capital cost.

| Partner | 2024 Metric |

|---|---|

| Campus channels | 7M+ customers |

| Private loans | $5B originations |

What is included in the product

A comprehensive Sallie Mae Business Model Canvas aligned to the company’s student-lending strategy, covering customer segments, value propositions, channels, revenue streams, cost structure and partners across the 9 classic BMC blocks. Ideal for presentations and investor discussions, it includes narrative insights, competitive advantages and linked SWOT analysis to support strategic decisions and validation using real-world data.

High-level, shareable one-page canvas that distills Sallie Mae’s lending, servicing, and partnership model into editable cells to relieve analysis and presentation pain points.

Activities

Credit Underwriting & Pricing

Assess borrower and cosigner risk using bureau data and internal models, targeting loss rates consistent with SLM risk tolerance while referencing market conditions; in 2024 the Federal Reserve policy rate near 5.25–5.50% tightened funding costs and informed pricing. Price loans to reflect credit tier, term and market rates, balancing approval rates with portfolio quality and return targets. Continuously recalibrate cutoffs and APRs based on performance and bureau score migrations.

Loan Origination & Servicing

Streamline application, certification, and disbursement workflows to shorten origination time and improve underwriting accuracy. Manage billing, payments, escrow, and statements across accounts while handling deferment, forbearance, and cosigner release workflows. Drive digital self-service to lower costs—industry studies show self-service can cut servicing costs by up to 40%.

Funding & Securitization

Funding & Securitization sources include retail deposits and wholesale debt to support loan growth; in 2024 Sallie Mae leaned on bank deposits and covered ABS programs to diversify funding. The firm executed multiple ABS transactions and maintained investor reporting cadence for transparency. Treasury optimizes liquidity, capital and interest-rate exposures while hedging and laddering maturities to reduce reinvestment and rate risk.

Digital Product & CX Management

Optimize web/app funnels, prequalification flows, and instant-decision engines to shorten application time and improve approval clarity for Sallie Mae borrowers.

Run continuous A/B testing to lift conversion and reduce abandonment, reinforce accessibility standards and mobile-first features, and integrate calculators and educational content to boost informed conversions.

- funnel optimization

- A/B testing

- accessibility & mobile

- education tools & calculators

Risk, Compliance & Collections

Sallie Mae (SLM) monitors credit, fraud, operational and regulatory risks across its loan portfolio, which exceeds $40 billion, using centralized policies, recurring control testing and targeted training programs.

Collections teams manage early-stage delinquency and recovery strategies, applying predictive analytics and segmentation to reduce cure times and lower charge-offs.

- Risk tags: credit, fraud, ops, regulatory

- Controls: policies, training, testing

- Collections: early-stage focus, recovery playbooks

- Analytics: predictive models to cut charge-offs

Assess borrower risk, price loans; Fed 5.25–5.50%, portfolio >$40B

Assess borrower/cosigner risk with bureau data and internal models to price loans across credit tiers; 2024 Fed policy rate ~5.25–5.50% tightened funding and informed APRs. Streamline digital origination, servicing and collections to cut costs and charge-offs; self-service can lower servicing costs up to 40%. Fund via bank deposits and ABS, with treasury hedging liquidity and rate exposures for a >$40B loan portfolio.

| Metric | 2024 |

|---|---|

| Loan portfolio | >$40B |

| Fed policy rate | 5.25–5.50% |

| Servicing cost cut | up to 40% |

| Funding | Bank deposits + ABS |

Full Document Unlocks After Purchase

Business Model Canvas

The Sallie Mae Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the same content and layout you’ll receive after purchase. When you buy, you’ll download this identical, fully editable document in Word and Excel formats. No fillers, no surprises—ready to present or adapt.

Description

Business Model Canvas for a Major Student-Lending Firm: Strategy, Revenue & Risk Map

Unlock the full strategic blueprint behind Sallie Mae’s business model with our in-depth Business Model Canvas; it maps value propositions, revenue streams, partnerships, and cost structure to show how the company scales and manages risk. Ideal for investors, consultants, and founders seeking actionable insights and benchmarking tools. Download the complete Word and Excel files to analyze, adapt, and apply Sallie Mae’s proven strategies today.

Partnerships

Universities & Financial Aid Offices

Collaborate with schools to embed Sallie Mae private loan options into financial aid workflows, capturing students at key decision points and leveraging campus channels to reach over 7 million customers. Coordinate certification, disbursement, and enrollment verification to speed funding and reduce default risk. Support on-campus financial literacy programs; in 2024 Sallie Mae reported over $5B in private student loan originations, reinforcing campus partnerships.

Credit Bureaus & Data Providers

Partnerships with credit bureaus (Experian, TransUnion, Equifax report over 1 billion consumer records globally in 2024) provide Sallie Mae access to credit histories, income verification signals and alternative data for underwriting and improved risk segmentation.

These feeds enable ongoing performance monitoring, early delinquency detection and dynamic pricing to tighten loss forecasts.

Integration supports compliance with FCRA and ECOA reporting and fair lending requirements through auditable data trails.

Capital Markets & Securitization Partners

Sallie Mae partners with underwriters, trustees and institutional investors to securitize private education loan pools, and as of 2024 continues to diversify funding sources to optimize cost of capital and manage its balance sheet. The bank uses warehouse lines and whole-loan buyers to scale originations and transfer risk while maintaining liquidity. Ongoing investor relations and transparency practices support market access and pricing discipline in 2024.

Fintech & Servicing Technology Vendors

Regulators & Compliance Advisors

- Engage regulators

- Align disclosures & capital

- Audit & remediate with experts

Partnerships + credit APIs drive 7M+ users, $5B orig.

Key partnerships with 7M+ campus channels, credit bureaus, underwriters, fintech vendors and regulators drive originations, underwriting, funding and compliance; 2024 origins ~$5B. Credit bureau feeds and APIs enable dynamic pricing and early risk detection; DocuSign FY2024 revenue $2.57B supports e-signature scale. Securitization and investor relations diversify funding and manage capital cost.

| Partner | 2024 Metric |

|---|---|

| Campus channels | 7M+ customers |

| Private loans | $5B originations |

What is included in the product

A comprehensive Sallie Mae Business Model Canvas aligned to the company’s student-lending strategy, covering customer segments, value propositions, channels, revenue streams, cost structure and partners across the 9 classic BMC blocks. Ideal for presentations and investor discussions, it includes narrative insights, competitive advantages and linked SWOT analysis to support strategic decisions and validation using real-world data.

High-level, shareable one-page canvas that distills Sallie Mae’s lending, servicing, and partnership model into editable cells to relieve analysis and presentation pain points.

Activities

Credit Underwriting & Pricing

Assess borrower and cosigner risk using bureau data and internal models, targeting loss rates consistent with SLM risk tolerance while referencing market conditions; in 2024 the Federal Reserve policy rate near 5.25–5.50% tightened funding costs and informed pricing. Price loans to reflect credit tier, term and market rates, balancing approval rates with portfolio quality and return targets. Continuously recalibrate cutoffs and APRs based on performance and bureau score migrations.

Loan Origination & Servicing

Streamline application, certification, and disbursement workflows to shorten origination time and improve underwriting accuracy. Manage billing, payments, escrow, and statements across accounts while handling deferment, forbearance, and cosigner release workflows. Drive digital self-service to lower costs—industry studies show self-service can cut servicing costs by up to 40%.

Funding & Securitization

Funding & Securitization sources include retail deposits and wholesale debt to support loan growth; in 2024 Sallie Mae leaned on bank deposits and covered ABS programs to diversify funding. The firm executed multiple ABS transactions and maintained investor reporting cadence for transparency. Treasury optimizes liquidity, capital and interest-rate exposures while hedging and laddering maturities to reduce reinvestment and rate risk.

Digital Product & CX Management

Optimize web/app funnels, prequalification flows, and instant-decision engines to shorten application time and improve approval clarity for Sallie Mae borrowers.

Run continuous A/B testing to lift conversion and reduce abandonment, reinforce accessibility standards and mobile-first features, and integrate calculators and educational content to boost informed conversions.

- funnel optimization

- A/B testing

- accessibility & mobile

- education tools & calculators

Risk, Compliance & Collections

Sallie Mae (SLM) monitors credit, fraud, operational and regulatory risks across its loan portfolio, which exceeds $40 billion, using centralized policies, recurring control testing and targeted training programs.

Collections teams manage early-stage delinquency and recovery strategies, applying predictive analytics and segmentation to reduce cure times and lower charge-offs.

- Risk tags: credit, fraud, ops, regulatory

- Controls: policies, training, testing

- Collections: early-stage focus, recovery playbooks

- Analytics: predictive models to cut charge-offs

Assess borrower risk, price loans; Fed 5.25–5.50%, portfolio >$40B

Assess borrower/cosigner risk with bureau data and internal models to price loans across credit tiers; 2024 Fed policy rate ~5.25–5.50% tightened funding and informed APRs. Streamline digital origination, servicing and collections to cut costs and charge-offs; self-service can lower servicing costs up to 40%. Fund via bank deposits and ABS, with treasury hedging liquidity and rate exposures for a >$40B loan portfolio.

| Metric | 2024 |

|---|---|

| Loan portfolio | >$40B |

| Fed policy rate | 5.25–5.50% |

| Servicing cost cut | up to 40% |

| Funding | Bank deposits + ABS |

Full Document Unlocks After Purchase

Business Model Canvas

The Sallie Mae Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the same content and layout you’ll receive after purchase. When you buy, you’ll download this identical, fully editable document in Word and Excel formats. No fillers, no surprises—ready to present or adapt.