Samsung Life Insurance Business Model Canvas

Insurance Business Model Canvas: Strategic blueprint for trust, growth, and profit

Unlock Samsung Life Insurance’s strategic blueprint with a concise Business Model Canvas that maps its customer segments, value propositions, revenue streams, key partnerships, and cost structure. This snapshot reveals how the firm scales trust and profitability in a competitive market. Ideal for investors, consultants, and executives seeking actionable insights—download the full, editable Canvas to benchmark strategy and drive decisions.

Partnerships

Global reinsurers

Global reinsurers absorb peak risks to stabilize Samsung Life’s loss ratios across cycles, protecting solvency and smoothing earnings for Korea’s largest life insurer. They supply advanced pricing insights and catastrophe-modeling support to refine underwriting and reduce tail volatility. Long-term treaties enable capital efficiency under regulatory and accounting regimes and support sustainable growth. Co-innovation with reinsurers accelerates market entry for parametric and cyber risk products.

Hospitals and health networks

Provider partnerships with hospitals and health networks enable cashless claims and on-site medical assessments, shortening adjudication times by up to 30% and improving customer experience in 2024.

Agreements secure preferred pricing and integrated wellness and preventive-care pathways, supporting cost control and retention while lowering claims leakage by similar margins.

Data-sharing under explicit consent feeds richer clinical inputs into underwriting models, improving risk selection and pricing accuracy in 2024.

Banks and financial distributors

Bancassurance expands Samsung Life’s reach to retail and corporate clients at scale; bancassurance supplies roughly one-third of life premiums in Asia (Swiss Re 2024). Embedded insurance at point-of-banking boosts conversion and lowers CAC through streamlined onboarding. Joint campaigns bundle savings, loans and protection to increase wallet share, while revenue-sharing aligns bank-insurer incentives for sustained cross-sell.

Samsung ecosystem partners

Technology and data vendors

Samsung Life, Korea's largest life insurer, relies on core admin, analytics and cloud providers to scale operations and boost resilience; in 2024 it advanced cloud-first migration to improve uptime. AI-driven underwriting and fraud detection speed issuance and reduce claims leakage, while cybersecurity partners enforce compliance with Korea's Personal Information Protection Act; APIs enable rapid channel integration.

- Core vendors: scalability/resilience

- AI: underwriting/fraud/service automation

- Cybersecurity: policyholder data protection

- APIs: faster channel integration

Reinsurers steady solvency; providers cut adjudication 30%; device reach 1.4B/200M/100M

Reinsurers stabilize solvency and tail risk via long-term treaties and co-innovation. Provider networks enable cashless care, cutting adjudication times up to 30% (2024). Bancassurance drives scale (~33% of life premiums in Asia, Swiss Re 2024); Samsung ecosystem (1.4B devices; Samsung Health 200M; Samsung Pay 100M) fuels distribution and data integration.

| Partner | Role | 2024 metric |

|---|---|---|

| Reinsurers | Risk/capital | — |

| Providers | Claims speed | Adjudication −30% |

| Bancassurance | Distribution | ~33% premiums |

| Samsung ecosystem | Digital reach | 1.4B/200M/100M |

What is included in the product

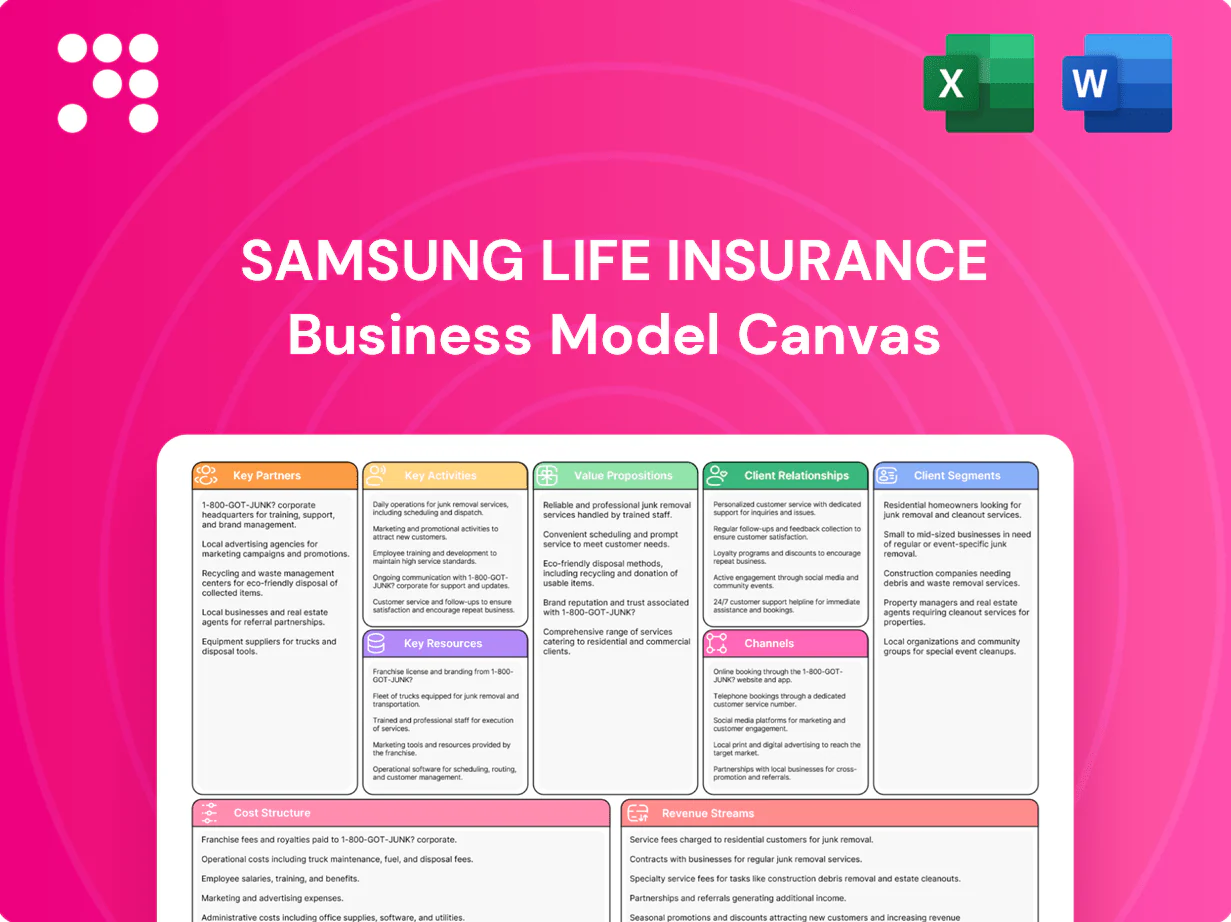

A comprehensive Business Model Canvas for Samsung Life Insurance outlining customer segments, channels, value propositions, revenue streams, key resources, partners, activities, cost structure and distribution strategy, with competitive advantages and linked SWOT insights. Ideal for presentations, investor discussions and strategic decision-making.

High-level view of Samsung Life Insurance’s business model with editable cells to quickly pinpoint pain-relieving elements—tailored protection products, streamlined digital claims, and integrated wealth-management services for seamless customer solutions.

Activities

Underwriting and pricing

Risk selection balances protection needs with portfolio profitability, supporting Samsung Life’s position as South Korea’s largest insurer with assets over 300 trillion KRW. Actuarial models calibrate mortality, morbidity and lapse assumptions using vendor and internal longevity studies. Continuous monitoring of experience and capital metrics sharpens pricing adequacy. Rules engines and AI speed decisions and ensure consistent outcomes across volumes.

Investment management

Managing Samsung Life's general account (≈KRW 338 trillion AUM in 2024) optimizes yield within defined risk appetite and ALM limits; active allocation targets spread pickup while respecting capital constraints. Duration matching (duration gap kept near 1–2 years) protects solvency against rate shifts. Multi-asset strategies diversify credit and market risk across bonds, alternatives and equities. ESG and stewardship policies guide long-term alignment with liabilities.

Distribution and sales enablement

Training, tools, and commission incentives boost agent and partner productivity, supporting Samsung Life, South Korea's largest life insurer by assets in 2024. Digital quoting and e-signature compress the sales cycle, enabling faster policy issuance and higher conversion rates. Segmented marketing funnels nurture leads across retail and bancassurance channels. Performance analytics continuously refines channel mix and shortens CAC payback.

Claims and policy administration

Straight-through processing accelerates simple claims and endorsements, cutting cycle times and enabling near-instant payouts for routine cases.

Clear SLAs and triage models boost customer satisfaction through predictable response times and prioritized handling for complex claims.

Robust fraud controls, regular audits and self-service portals reduce loss ratios, lower operational load and minimize manual errors.

- STP: faster routine claims

- SLA: predictable responses

- Fraud controls: protect loss ratios

- Self-service: lower ops load

Compliance and risk management

Robust governance at Samsung Life ensures regulatory adherence and policyholder protection through board-level compliance and internal audit functions. ORSA, annual stress tests and active capital management maintain solvency in line with Korea's risk-based capital requirement (>100%). Strong data privacy and cyber controls protect customer information, while vendor and model risk frameworks ensure third-party and model integrity.

- Governance: board compliance & internal audit

- Solvency: ORSA, stress tests, capital planning (RBC >100%)

- Data security: privacy, cyber controls

- Risk frameworks: vendor & model risk management

Risk selection, AI pricing and digital sales drive profits for insurer with KRW 338T, RBC >100%

Risk selection and pricing sustain profitability for Samsung Life (total assets ≈KRW 338 trillion in 2024) using actuarial models, AI rules engines and experience monitoring. General account management (AUM ≈KRW 338T) targets spread with duration gap ~1–2 years across bonds, alternatives and equities. Digital sales, STP claims and agent incentives shorten cycles and raise conversion. Governance enforces ORSA, stress tests and RBC >100%.

| Metric | 2024 Value |

|---|---|

| Total assets / AUM | ≈KRW 338 trillion |

| Duration gap | ~1–2 years |

| Solvency (RBC) | >100% |

Full Version Awaits

Business Model Canvas

The Samsung Life Insurance Business Model Canvas previewed here is the actual deliverable, not a mockup or marketing sample. When you complete your purchase you’ll receive this exact document with all content and layout intact. The files are provided ready-to-edit and downloadable in Word and Excel formats.

Insurance Business Model Canvas: Strategic blueprint for trust, growth, and profit

Unlock Samsung Life Insurance’s strategic blueprint with a concise Business Model Canvas that maps its customer segments, value propositions, revenue streams, key partnerships, and cost structure. This snapshot reveals how the firm scales trust and profitability in a competitive market. Ideal for investors, consultants, and executives seeking actionable insights—download the full, editable Canvas to benchmark strategy and drive decisions.

Partnerships

Global reinsurers

Global reinsurers absorb peak risks to stabilize Samsung Life’s loss ratios across cycles, protecting solvency and smoothing earnings for Korea’s largest life insurer. They supply advanced pricing insights and catastrophe-modeling support to refine underwriting and reduce tail volatility. Long-term treaties enable capital efficiency under regulatory and accounting regimes and support sustainable growth. Co-innovation with reinsurers accelerates market entry for parametric and cyber risk products.

Hospitals and health networks

Provider partnerships with hospitals and health networks enable cashless claims and on-site medical assessments, shortening adjudication times by up to 30% and improving customer experience in 2024.

Agreements secure preferred pricing and integrated wellness and preventive-care pathways, supporting cost control and retention while lowering claims leakage by similar margins.

Data-sharing under explicit consent feeds richer clinical inputs into underwriting models, improving risk selection and pricing accuracy in 2024.

Banks and financial distributors

Bancassurance expands Samsung Life’s reach to retail and corporate clients at scale; bancassurance supplies roughly one-third of life premiums in Asia (Swiss Re 2024). Embedded insurance at point-of-banking boosts conversion and lowers CAC through streamlined onboarding. Joint campaigns bundle savings, loans and protection to increase wallet share, while revenue-sharing aligns bank-insurer incentives for sustained cross-sell.

Samsung ecosystem partners

Technology and data vendors

Samsung Life, Korea's largest life insurer, relies on core admin, analytics and cloud providers to scale operations and boost resilience; in 2024 it advanced cloud-first migration to improve uptime. AI-driven underwriting and fraud detection speed issuance and reduce claims leakage, while cybersecurity partners enforce compliance with Korea's Personal Information Protection Act; APIs enable rapid channel integration.

- Core vendors: scalability/resilience

- AI: underwriting/fraud/service automation

- Cybersecurity: policyholder data protection

- APIs: faster channel integration

Reinsurers steady solvency; providers cut adjudication 30%; device reach 1.4B/200M/100M

Reinsurers stabilize solvency and tail risk via long-term treaties and co-innovation. Provider networks enable cashless care, cutting adjudication times up to 30% (2024). Bancassurance drives scale (~33% of life premiums in Asia, Swiss Re 2024); Samsung ecosystem (1.4B devices; Samsung Health 200M; Samsung Pay 100M) fuels distribution and data integration.

| Partner | Role | 2024 metric |

|---|---|---|

| Reinsurers | Risk/capital | — |

| Providers | Claims speed | Adjudication −30% |

| Bancassurance | Distribution | ~33% premiums |

| Samsung ecosystem | Digital reach | 1.4B/200M/100M |

What is included in the product

A comprehensive Business Model Canvas for Samsung Life Insurance outlining customer segments, channels, value propositions, revenue streams, key resources, partners, activities, cost structure and distribution strategy, with competitive advantages and linked SWOT insights. Ideal for presentations, investor discussions and strategic decision-making.

High-level view of Samsung Life Insurance’s business model with editable cells to quickly pinpoint pain-relieving elements—tailored protection products, streamlined digital claims, and integrated wealth-management services for seamless customer solutions.

Activities

Underwriting and pricing

Risk selection balances protection needs with portfolio profitability, supporting Samsung Life’s position as South Korea’s largest insurer with assets over 300 trillion KRW. Actuarial models calibrate mortality, morbidity and lapse assumptions using vendor and internal longevity studies. Continuous monitoring of experience and capital metrics sharpens pricing adequacy. Rules engines and AI speed decisions and ensure consistent outcomes across volumes.

Investment management

Managing Samsung Life's general account (≈KRW 338 trillion AUM in 2024) optimizes yield within defined risk appetite and ALM limits; active allocation targets spread pickup while respecting capital constraints. Duration matching (duration gap kept near 1–2 years) protects solvency against rate shifts. Multi-asset strategies diversify credit and market risk across bonds, alternatives and equities. ESG and stewardship policies guide long-term alignment with liabilities.

Distribution and sales enablement

Training, tools, and commission incentives boost agent and partner productivity, supporting Samsung Life, South Korea's largest life insurer by assets in 2024. Digital quoting and e-signature compress the sales cycle, enabling faster policy issuance and higher conversion rates. Segmented marketing funnels nurture leads across retail and bancassurance channels. Performance analytics continuously refines channel mix and shortens CAC payback.

Claims and policy administration

Straight-through processing accelerates simple claims and endorsements, cutting cycle times and enabling near-instant payouts for routine cases.

Clear SLAs and triage models boost customer satisfaction through predictable response times and prioritized handling for complex claims.

Robust fraud controls, regular audits and self-service portals reduce loss ratios, lower operational load and minimize manual errors.

- STP: faster routine claims

- SLA: predictable responses

- Fraud controls: protect loss ratios

- Self-service: lower ops load

Compliance and risk management

Robust governance at Samsung Life ensures regulatory adherence and policyholder protection through board-level compliance and internal audit functions. ORSA, annual stress tests and active capital management maintain solvency in line with Korea's risk-based capital requirement (>100%). Strong data privacy and cyber controls protect customer information, while vendor and model risk frameworks ensure third-party and model integrity.

- Governance: board compliance & internal audit

- Solvency: ORSA, stress tests, capital planning (RBC >100%)

- Data security: privacy, cyber controls

- Risk frameworks: vendor & model risk management

Risk selection, AI pricing and digital sales drive profits for insurer with KRW 338T, RBC >100%

Risk selection and pricing sustain profitability for Samsung Life (total assets ≈KRW 338 trillion in 2024) using actuarial models, AI rules engines and experience monitoring. General account management (AUM ≈KRW 338T) targets spread with duration gap ~1–2 years across bonds, alternatives and equities. Digital sales, STP claims and agent incentives shorten cycles and raise conversion. Governance enforces ORSA, stress tests and RBC >100%.

| Metric | 2024 Value |

|---|---|

| Total assets / AUM | ≈KRW 338 trillion |

| Duration gap | ~1–2 years |

| Solvency (RBC) | >100% |

Full Version Awaits

Business Model Canvas

The Samsung Life Insurance Business Model Canvas previewed here is the actual deliverable, not a mockup or marketing sample. When you complete your purchase you’ll receive this exact document with all content and layout intact. The files are provided ready-to-edit and downloadable in Word and Excel formats.

Original: $10.00

-65%$10.00

$3.50Description

Insurance Business Model Canvas: Strategic blueprint for trust, growth, and profit

Unlock Samsung Life Insurance’s strategic blueprint with a concise Business Model Canvas that maps its customer segments, value propositions, revenue streams, key partnerships, and cost structure. This snapshot reveals how the firm scales trust and profitability in a competitive market. Ideal for investors, consultants, and executives seeking actionable insights—download the full, editable Canvas to benchmark strategy and drive decisions.

Partnerships

Global reinsurers

Global reinsurers absorb peak risks to stabilize Samsung Life’s loss ratios across cycles, protecting solvency and smoothing earnings for Korea’s largest life insurer. They supply advanced pricing insights and catastrophe-modeling support to refine underwriting and reduce tail volatility. Long-term treaties enable capital efficiency under regulatory and accounting regimes and support sustainable growth. Co-innovation with reinsurers accelerates market entry for parametric and cyber risk products.

Hospitals and health networks

Provider partnerships with hospitals and health networks enable cashless claims and on-site medical assessments, shortening adjudication times by up to 30% and improving customer experience in 2024.

Agreements secure preferred pricing and integrated wellness and preventive-care pathways, supporting cost control and retention while lowering claims leakage by similar margins.

Data-sharing under explicit consent feeds richer clinical inputs into underwriting models, improving risk selection and pricing accuracy in 2024.

Banks and financial distributors

Bancassurance expands Samsung Life’s reach to retail and corporate clients at scale; bancassurance supplies roughly one-third of life premiums in Asia (Swiss Re 2024). Embedded insurance at point-of-banking boosts conversion and lowers CAC through streamlined onboarding. Joint campaigns bundle savings, loans and protection to increase wallet share, while revenue-sharing aligns bank-insurer incentives for sustained cross-sell.

Samsung ecosystem partners

Technology and data vendors

Samsung Life, Korea's largest life insurer, relies on core admin, analytics and cloud providers to scale operations and boost resilience; in 2024 it advanced cloud-first migration to improve uptime. AI-driven underwriting and fraud detection speed issuance and reduce claims leakage, while cybersecurity partners enforce compliance with Korea's Personal Information Protection Act; APIs enable rapid channel integration.

- Core vendors: scalability/resilience

- AI: underwriting/fraud/service automation

- Cybersecurity: policyholder data protection

- APIs: faster channel integration

Reinsurers steady solvency; providers cut adjudication 30%; device reach 1.4B/200M/100M

Reinsurers stabilize solvency and tail risk via long-term treaties and co-innovation. Provider networks enable cashless care, cutting adjudication times up to 30% (2024). Bancassurance drives scale (~33% of life premiums in Asia, Swiss Re 2024); Samsung ecosystem (1.4B devices; Samsung Health 200M; Samsung Pay 100M) fuels distribution and data integration.

| Partner | Role | 2024 metric |

|---|---|---|

| Reinsurers | Risk/capital | — |

| Providers | Claims speed | Adjudication −30% |

| Bancassurance | Distribution | ~33% premiums |

| Samsung ecosystem | Digital reach | 1.4B/200M/100M |

What is included in the product

A comprehensive Business Model Canvas for Samsung Life Insurance outlining customer segments, channels, value propositions, revenue streams, key resources, partners, activities, cost structure and distribution strategy, with competitive advantages and linked SWOT insights. Ideal for presentations, investor discussions and strategic decision-making.

High-level view of Samsung Life Insurance’s business model with editable cells to quickly pinpoint pain-relieving elements—tailored protection products, streamlined digital claims, and integrated wealth-management services for seamless customer solutions.

Activities

Underwriting and pricing

Risk selection balances protection needs with portfolio profitability, supporting Samsung Life’s position as South Korea’s largest insurer with assets over 300 trillion KRW. Actuarial models calibrate mortality, morbidity and lapse assumptions using vendor and internal longevity studies. Continuous monitoring of experience and capital metrics sharpens pricing adequacy. Rules engines and AI speed decisions and ensure consistent outcomes across volumes.

Investment management

Managing Samsung Life's general account (≈KRW 338 trillion AUM in 2024) optimizes yield within defined risk appetite and ALM limits; active allocation targets spread pickup while respecting capital constraints. Duration matching (duration gap kept near 1–2 years) protects solvency against rate shifts. Multi-asset strategies diversify credit and market risk across bonds, alternatives and equities. ESG and stewardship policies guide long-term alignment with liabilities.

Distribution and sales enablement

Training, tools, and commission incentives boost agent and partner productivity, supporting Samsung Life, South Korea's largest life insurer by assets in 2024. Digital quoting and e-signature compress the sales cycle, enabling faster policy issuance and higher conversion rates. Segmented marketing funnels nurture leads across retail and bancassurance channels. Performance analytics continuously refines channel mix and shortens CAC payback.

Claims and policy administration

Straight-through processing accelerates simple claims and endorsements, cutting cycle times and enabling near-instant payouts for routine cases.

Clear SLAs and triage models boost customer satisfaction through predictable response times and prioritized handling for complex claims.

Robust fraud controls, regular audits and self-service portals reduce loss ratios, lower operational load and minimize manual errors.

- STP: faster routine claims

- SLA: predictable responses

- Fraud controls: protect loss ratios

- Self-service: lower ops load

Compliance and risk management

Robust governance at Samsung Life ensures regulatory adherence and policyholder protection through board-level compliance and internal audit functions. ORSA, annual stress tests and active capital management maintain solvency in line with Korea's risk-based capital requirement (>100%). Strong data privacy and cyber controls protect customer information, while vendor and model risk frameworks ensure third-party and model integrity.

- Governance: board compliance & internal audit

- Solvency: ORSA, stress tests, capital planning (RBC >100%)

- Data security: privacy, cyber controls

- Risk frameworks: vendor & model risk management

Risk selection, AI pricing and digital sales drive profits for insurer with KRW 338T, RBC >100%

Risk selection and pricing sustain profitability for Samsung Life (total assets ≈KRW 338 trillion in 2024) using actuarial models, AI rules engines and experience monitoring. General account management (AUM ≈KRW 338T) targets spread with duration gap ~1–2 years across bonds, alternatives and equities. Digital sales, STP claims and agent incentives shorten cycles and raise conversion. Governance enforces ORSA, stress tests and RBC >100%.

| Metric | 2024 Value |

|---|---|

| Total assets / AUM | ≈KRW 338 trillion |

| Duration gap | ~1–2 years |

| Solvency (RBC) | >100% |

Full Version Awaits

Business Model Canvas

The Samsung Life Insurance Business Model Canvas previewed here is the actual deliverable, not a mockup or marketing sample. When you complete your purchase you’ll receive this exact document with all content and layout intact. The files are provided ready-to-edit and downloadable in Word and Excel formats.