Samsung SDS Porter's Five Forces Analysis

From Overview to Strategy Blueprint

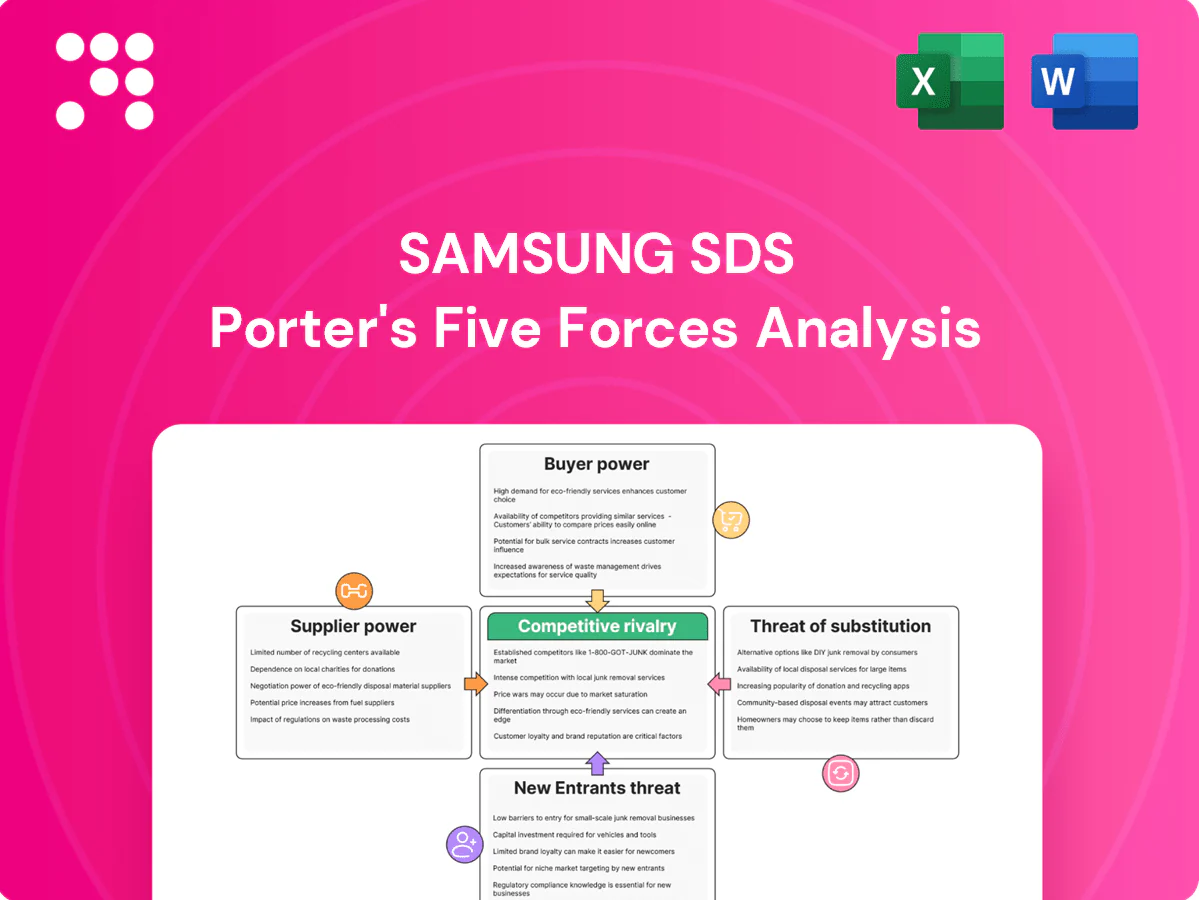

Samsung SDS faces intense competition from global cloud and IT services firms, moderate threat of new entrants due to scale and customer locks, supplier influence driven by proprietary tech partnerships, and rising substitute threats from hyperscalers—affecting margins and strategic options. Unlock the full Porter's Five Forces Analysis to explore these dynamics in depth.

Suppliers Bargaining Power

Dependence on hyperscale cloud partners

Partnerships with AWS, Microsoft Azure and Google Cloud (combined ~65% global IaaS share in 2024) plus Samsung Group infrastructure create interdependence in pricing, roadmap access and co-selling opportunities. Preferred partner tiers reduce supplier risk but concentrate bargaining leverage with a few platforms. Joint solution commitments can lock SDS into technical pathways and shifts in partner incentives or discounts can quickly compress margins.

Scarcity of specialized tech talent

Highly skilled engineers in cybersecurity, AI, and cloud architecture function as critical suppliers to Samsung SDS; ISC2 reported a global cybersecurity workforce gap of about 3.4 million in 2024, tightening talent supply. Tight labor markets pushed wage premiums for cloud/AI roles by double digits in many markets, giving talent strong bargaining power. Visa caps, compliance burdens and retention constraints amplify scarcity. SDS must invest in upskilling and employer branding to rebalance power.

Hardware and network vendors

Dependence on data center hardware, storage and network gear ties Samsung SDS to OEM pricing cycles and newer component lead times. Samsung Group scale and volume buying — leveraging over 280,000 employees and group-level procurement (2024) — helps negotiate better unit pricing and priority allocations. Major supply-chain shocks, however, can still spike costs or delay rollouts. Multi-vendor strategies dilute single-vendor leverage but increase integration and support complexity.

Software and cybersecurity ecosystems

Licenses from major software and security vendors raise Samsung SDS's costs and shape solution architectures; bundled enterprise agreements lower unit cost yet increase switching friction. Supplier leverage peaks during zero-day incidents where SLAs dictate remediation speed. Open-source alternatives (cybersecurity market ≈ $220B in 2024) reduce vendor power but require internal support capacity.

- License-driven cost structure

- Bundled deals = lower unit cost, higher lock-in

- SLA/zero-day response = critical supplier leverage

- Open-source tempers power, needs ops investment

Telecom and edge connectivity providers

Smart logistics and mobility depend on carriers and 5G/MEC partners for coverage and sub-10 ms latency; limited local carrier options (often 2–3 providers) increase supplier power. Long-term 3–5-year contracts stabilize service but reduce renegotiation. Private 5G deployments rose >30% in 2024, providing counter-leverage where feasible.

- Carrier concentration: 2–3 providers in many markets

- Contract tenor: typically 3–5 years

- Latency need: sub-10 ms for MEC use cases

- Private 5G growth: >30% YoY in 2024

Cloud + OEM deals concentrate risk; 3.4M cyber gap; private 5G >30%

Partnerships with AWS/Azure/GCP (~65% global IaaS share in 2024) and Samsung Group scale reduce supplier risk but concentrate leverage; talent gap (~3.4M cybersecurity shortage in 2024) raises wage pressure; OEM cycles and license costs (cybersecurity market ≈$220B in 2024) can compress margins; private 5G growth >30% in 2024 provides selective counter-leverage.

| Metric | 2024 |

|---|---|

| Global IaaS share (partners) | ~65% |

| Cybersecurity workforce gap | 3.4M |

| Cybersecurity market | $220B |

| Private 5G growth | >30% |

What is included in the product

Tailored Porter's Five Forces for Samsung SDS, uncovering key drivers of competition, customer and supplier influence, entry barriers, substitutes and disruptive threats, with strategic commentary for reports.

One-sheet Porter's Five Forces for Samsung SDS—quickly visualize supplier, buyer, entrant, substitute and rivalry pressures with a spider chart and customizable sliders to model scenarios; clean layout ready for decks and seamless Excel integration so non-finance teams can assess strategic pain points instantly.

Customers Bargaining Power

Large enterprise and public-sector clients

Large enterprise and public-sector clients drive aggressive RFPs and framework agreements that compress margins, with procurement teams demanding transparent SLAs and outcome-based fees; industry surveys show roughly 30% of enterprise deals now include outcome metrics. Scale deals concentrate revenue risk—top accounts can represent over 25% of IT services revenue—while references and certifications (ISO, SOC, cloud partner status) are table stakes to win.

High switching costs with modular exits

Deep systems integration at Samsung SDS raises switching costs for core workloads, while cloud-native patterns and APIs—with container use at roughly 92% in enterprise surveys—enable selective vendor substitution. Clients increasingly dual-source to pressure rates, and in a >$600B 2024 public cloud market renewal cycles become pivotal negotiation windows where pricing and scope are often reset.

Demand for measurable business outcomes

Buyers prioritize measurable outcomes—productivity, security posture, and logistics KPIs—over input metrics, with 2024 surveys showing a majority of enterprises favoring outcome-linked deals. Outcome-linked pricing shifts execution and performance risk to providers, increasing buyer leverage in negotiations. Clear baselines and access to operational data become contract flashpoints. Continuous optimization expectations extend well beyond initial delivery, driving longer-term SLAs and penalties.

Preference for standardized, interoperable solutions

Clients in 2024 increasingly demand standardized, interoperable solutions to avoid vendor lock-in and lower total lifecycle costs, which constrains premium pricing for proprietary stacks; compliance and data residency needs still drive customization but are becoming commoditized. Interoperability proofs and live integrations are decisive in deal closure, shifting negotiations toward measurable open-standard commitments.

- Clients: avoid lock-in

- Pricing: limits premium on proprietary stacks

- Compliance: customization commoditizing

- Sales: interoperability proofs close deals

Samsung Group affiliates as anchor customers

Samsung Group affiliation gives Samsung SDS stable, high-volume demand and co-innovation advantages, but tightens internal benchmarking as Group procurement disciplines pushed margins lower in exchange for volume; internal contracts reportedly made up about 40% of SDS revenue in 2024, setting a performance floor that external buyers expect to match. Overreliance on Group budgets concentrates risk if affiliate capex shifts, while success within the Group raises external customer expectations and bargaining leverage.

- Stable demand: ~40% revenue from affiliates (2024)

- Margin pressure: group procurement lowers pricing

- Benchmarking: internal success sets external expectations

- Concentration risk: dependent on affiliate budgets

Outcome-linked RFPs and cloud-native shift squeeze margins as top accounts, affiliates dominate

Buyers use aggressive RFPs and outcome-based fees (~30% of deals include outcome metrics) to compress margins; top accounts can exceed 25% of IT services revenue. Cloud-native patterns (container use ~92%) enable selective substitution; public cloud renewals in a >$600B 2024 market reset pricing. Samsung Group affiliates provided ~40% of SDS revenue in 2024, tightening internal benchmarking and pricing pressure.

| Metric | 2024 Value |

|---|---|

| Outcome-linked deals | ~30% |

| Top-account concentration | >25% |

| Container adoption | ~92% |

| Public cloud market | >$600B |

| Affiliate revenue | ~40% |

Full Version Awaits

Samsung SDS Porter's Five Forces Analysis

This preview shows the exact Samsung SDS Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final file you will get instantly.

From Overview to Strategy Blueprint

Samsung SDS faces intense competition from global cloud and IT services firms, moderate threat of new entrants due to scale and customer locks, supplier influence driven by proprietary tech partnerships, and rising substitute threats from hyperscalers—affecting margins and strategic options. Unlock the full Porter's Five Forces Analysis to explore these dynamics in depth.

Suppliers Bargaining Power

Dependence on hyperscale cloud partners

Partnerships with AWS, Microsoft Azure and Google Cloud (combined ~65% global IaaS share in 2024) plus Samsung Group infrastructure create interdependence in pricing, roadmap access and co-selling opportunities. Preferred partner tiers reduce supplier risk but concentrate bargaining leverage with a few platforms. Joint solution commitments can lock SDS into technical pathways and shifts in partner incentives or discounts can quickly compress margins.

Scarcity of specialized tech talent

Highly skilled engineers in cybersecurity, AI, and cloud architecture function as critical suppliers to Samsung SDS; ISC2 reported a global cybersecurity workforce gap of about 3.4 million in 2024, tightening talent supply. Tight labor markets pushed wage premiums for cloud/AI roles by double digits in many markets, giving talent strong bargaining power. Visa caps, compliance burdens and retention constraints amplify scarcity. SDS must invest in upskilling and employer branding to rebalance power.

Hardware and network vendors

Dependence on data center hardware, storage and network gear ties Samsung SDS to OEM pricing cycles and newer component lead times. Samsung Group scale and volume buying — leveraging over 280,000 employees and group-level procurement (2024) — helps negotiate better unit pricing and priority allocations. Major supply-chain shocks, however, can still spike costs or delay rollouts. Multi-vendor strategies dilute single-vendor leverage but increase integration and support complexity.

Software and cybersecurity ecosystems

Licenses from major software and security vendors raise Samsung SDS's costs and shape solution architectures; bundled enterprise agreements lower unit cost yet increase switching friction. Supplier leverage peaks during zero-day incidents where SLAs dictate remediation speed. Open-source alternatives (cybersecurity market ≈ $220B in 2024) reduce vendor power but require internal support capacity.

- License-driven cost structure

- Bundled deals = lower unit cost, higher lock-in

- SLA/zero-day response = critical supplier leverage

- Open-source tempers power, needs ops investment

Telecom and edge connectivity providers

Smart logistics and mobility depend on carriers and 5G/MEC partners for coverage and sub-10 ms latency; limited local carrier options (often 2–3 providers) increase supplier power. Long-term 3–5-year contracts stabilize service but reduce renegotiation. Private 5G deployments rose >30% in 2024, providing counter-leverage where feasible.

- Carrier concentration: 2–3 providers in many markets

- Contract tenor: typically 3–5 years

- Latency need: sub-10 ms for MEC use cases

- Private 5G growth: >30% YoY in 2024

Cloud + OEM deals concentrate risk; 3.4M cyber gap; private 5G >30%

Partnerships with AWS/Azure/GCP (~65% global IaaS share in 2024) and Samsung Group scale reduce supplier risk but concentrate leverage; talent gap (~3.4M cybersecurity shortage in 2024) raises wage pressure; OEM cycles and license costs (cybersecurity market ≈$220B in 2024) can compress margins; private 5G growth >30% in 2024 provides selective counter-leverage.

| Metric | 2024 |

|---|---|

| Global IaaS share (partners) | ~65% |

| Cybersecurity workforce gap | 3.4M |

| Cybersecurity market | $220B |

| Private 5G growth | >30% |

What is included in the product

Tailored Porter's Five Forces for Samsung SDS, uncovering key drivers of competition, customer and supplier influence, entry barriers, substitutes and disruptive threats, with strategic commentary for reports.

One-sheet Porter's Five Forces for Samsung SDS—quickly visualize supplier, buyer, entrant, substitute and rivalry pressures with a spider chart and customizable sliders to model scenarios; clean layout ready for decks and seamless Excel integration so non-finance teams can assess strategic pain points instantly.

Customers Bargaining Power

Large enterprise and public-sector clients

Large enterprise and public-sector clients drive aggressive RFPs and framework agreements that compress margins, with procurement teams demanding transparent SLAs and outcome-based fees; industry surveys show roughly 30% of enterprise deals now include outcome metrics. Scale deals concentrate revenue risk—top accounts can represent over 25% of IT services revenue—while references and certifications (ISO, SOC, cloud partner status) are table stakes to win.

High switching costs with modular exits

Deep systems integration at Samsung SDS raises switching costs for core workloads, while cloud-native patterns and APIs—with container use at roughly 92% in enterprise surveys—enable selective vendor substitution. Clients increasingly dual-source to pressure rates, and in a >$600B 2024 public cloud market renewal cycles become pivotal negotiation windows where pricing and scope are often reset.

Demand for measurable business outcomes

Buyers prioritize measurable outcomes—productivity, security posture, and logistics KPIs—over input metrics, with 2024 surveys showing a majority of enterprises favoring outcome-linked deals. Outcome-linked pricing shifts execution and performance risk to providers, increasing buyer leverage in negotiations. Clear baselines and access to operational data become contract flashpoints. Continuous optimization expectations extend well beyond initial delivery, driving longer-term SLAs and penalties.

Preference for standardized, interoperable solutions

Clients in 2024 increasingly demand standardized, interoperable solutions to avoid vendor lock-in and lower total lifecycle costs, which constrains premium pricing for proprietary stacks; compliance and data residency needs still drive customization but are becoming commoditized. Interoperability proofs and live integrations are decisive in deal closure, shifting negotiations toward measurable open-standard commitments.

- Clients: avoid lock-in

- Pricing: limits premium on proprietary stacks

- Compliance: customization commoditizing

- Sales: interoperability proofs close deals

Samsung Group affiliates as anchor customers

Samsung Group affiliation gives Samsung SDS stable, high-volume demand and co-innovation advantages, but tightens internal benchmarking as Group procurement disciplines pushed margins lower in exchange for volume; internal contracts reportedly made up about 40% of SDS revenue in 2024, setting a performance floor that external buyers expect to match. Overreliance on Group budgets concentrates risk if affiliate capex shifts, while success within the Group raises external customer expectations and bargaining leverage.

- Stable demand: ~40% revenue from affiliates (2024)

- Margin pressure: group procurement lowers pricing

- Benchmarking: internal success sets external expectations

- Concentration risk: dependent on affiliate budgets

Outcome-linked RFPs and cloud-native shift squeeze margins as top accounts, affiliates dominate

Buyers use aggressive RFPs and outcome-based fees (~30% of deals include outcome metrics) to compress margins; top accounts can exceed 25% of IT services revenue. Cloud-native patterns (container use ~92%) enable selective substitution; public cloud renewals in a >$600B 2024 market reset pricing. Samsung Group affiliates provided ~40% of SDS revenue in 2024, tightening internal benchmarking and pricing pressure.

| Metric | 2024 Value |

|---|---|

| Outcome-linked deals | ~30% |

| Top-account concentration | >25% |

| Container adoption | ~92% |

| Public cloud market | >$600B |

| Affiliate revenue | ~40% |

Full Version Awaits

Samsung SDS Porter's Five Forces Analysis

This preview shows the exact Samsung SDS Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final file you will get instantly.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Samsung SDS faces intense competition from global cloud and IT services firms, moderate threat of new entrants due to scale and customer locks, supplier influence driven by proprietary tech partnerships, and rising substitute threats from hyperscalers—affecting margins and strategic options. Unlock the full Porter's Five Forces Analysis to explore these dynamics in depth.

Suppliers Bargaining Power

Dependence on hyperscale cloud partners

Partnerships with AWS, Microsoft Azure and Google Cloud (combined ~65% global IaaS share in 2024) plus Samsung Group infrastructure create interdependence in pricing, roadmap access and co-selling opportunities. Preferred partner tiers reduce supplier risk but concentrate bargaining leverage with a few platforms. Joint solution commitments can lock SDS into technical pathways and shifts in partner incentives or discounts can quickly compress margins.

Scarcity of specialized tech talent

Highly skilled engineers in cybersecurity, AI, and cloud architecture function as critical suppliers to Samsung SDS; ISC2 reported a global cybersecurity workforce gap of about 3.4 million in 2024, tightening talent supply. Tight labor markets pushed wage premiums for cloud/AI roles by double digits in many markets, giving talent strong bargaining power. Visa caps, compliance burdens and retention constraints amplify scarcity. SDS must invest in upskilling and employer branding to rebalance power.

Hardware and network vendors

Dependence on data center hardware, storage and network gear ties Samsung SDS to OEM pricing cycles and newer component lead times. Samsung Group scale and volume buying — leveraging over 280,000 employees and group-level procurement (2024) — helps negotiate better unit pricing and priority allocations. Major supply-chain shocks, however, can still spike costs or delay rollouts. Multi-vendor strategies dilute single-vendor leverage but increase integration and support complexity.

Software and cybersecurity ecosystems

Licenses from major software and security vendors raise Samsung SDS's costs and shape solution architectures; bundled enterprise agreements lower unit cost yet increase switching friction. Supplier leverage peaks during zero-day incidents where SLAs dictate remediation speed. Open-source alternatives (cybersecurity market ≈ $220B in 2024) reduce vendor power but require internal support capacity.

- License-driven cost structure

- Bundled deals = lower unit cost, higher lock-in

- SLA/zero-day response = critical supplier leverage

- Open-source tempers power, needs ops investment

Telecom and edge connectivity providers

Smart logistics and mobility depend on carriers and 5G/MEC partners for coverage and sub-10 ms latency; limited local carrier options (often 2–3 providers) increase supplier power. Long-term 3–5-year contracts stabilize service but reduce renegotiation. Private 5G deployments rose >30% in 2024, providing counter-leverage where feasible.

- Carrier concentration: 2–3 providers in many markets

- Contract tenor: typically 3–5 years

- Latency need: sub-10 ms for MEC use cases

- Private 5G growth: >30% YoY in 2024

Cloud + OEM deals concentrate risk; 3.4M cyber gap; private 5G >30%

Partnerships with AWS/Azure/GCP (~65% global IaaS share in 2024) and Samsung Group scale reduce supplier risk but concentrate leverage; talent gap (~3.4M cybersecurity shortage in 2024) raises wage pressure; OEM cycles and license costs (cybersecurity market ≈$220B in 2024) can compress margins; private 5G growth >30% in 2024 provides selective counter-leverage.

| Metric | 2024 |

|---|---|

| Global IaaS share (partners) | ~65% |

| Cybersecurity workforce gap | 3.4M |

| Cybersecurity market | $220B |

| Private 5G growth | >30% |

What is included in the product

Tailored Porter's Five Forces for Samsung SDS, uncovering key drivers of competition, customer and supplier influence, entry barriers, substitutes and disruptive threats, with strategic commentary for reports.

One-sheet Porter's Five Forces for Samsung SDS—quickly visualize supplier, buyer, entrant, substitute and rivalry pressures with a spider chart and customizable sliders to model scenarios; clean layout ready for decks and seamless Excel integration so non-finance teams can assess strategic pain points instantly.

Customers Bargaining Power

Large enterprise and public-sector clients

Large enterprise and public-sector clients drive aggressive RFPs and framework agreements that compress margins, with procurement teams demanding transparent SLAs and outcome-based fees; industry surveys show roughly 30% of enterprise deals now include outcome metrics. Scale deals concentrate revenue risk—top accounts can represent over 25% of IT services revenue—while references and certifications (ISO, SOC, cloud partner status) are table stakes to win.

High switching costs with modular exits

Deep systems integration at Samsung SDS raises switching costs for core workloads, while cloud-native patterns and APIs—with container use at roughly 92% in enterprise surveys—enable selective vendor substitution. Clients increasingly dual-source to pressure rates, and in a >$600B 2024 public cloud market renewal cycles become pivotal negotiation windows where pricing and scope are often reset.

Demand for measurable business outcomes

Buyers prioritize measurable outcomes—productivity, security posture, and logistics KPIs—over input metrics, with 2024 surveys showing a majority of enterprises favoring outcome-linked deals. Outcome-linked pricing shifts execution and performance risk to providers, increasing buyer leverage in negotiations. Clear baselines and access to operational data become contract flashpoints. Continuous optimization expectations extend well beyond initial delivery, driving longer-term SLAs and penalties.

Preference for standardized, interoperable solutions

Clients in 2024 increasingly demand standardized, interoperable solutions to avoid vendor lock-in and lower total lifecycle costs, which constrains premium pricing for proprietary stacks; compliance and data residency needs still drive customization but are becoming commoditized. Interoperability proofs and live integrations are decisive in deal closure, shifting negotiations toward measurable open-standard commitments.

- Clients: avoid lock-in

- Pricing: limits premium on proprietary stacks

- Compliance: customization commoditizing

- Sales: interoperability proofs close deals

Samsung Group affiliates as anchor customers

Samsung Group affiliation gives Samsung SDS stable, high-volume demand and co-innovation advantages, but tightens internal benchmarking as Group procurement disciplines pushed margins lower in exchange for volume; internal contracts reportedly made up about 40% of SDS revenue in 2024, setting a performance floor that external buyers expect to match. Overreliance on Group budgets concentrates risk if affiliate capex shifts, while success within the Group raises external customer expectations and bargaining leverage.

- Stable demand: ~40% revenue from affiliates (2024)

- Margin pressure: group procurement lowers pricing

- Benchmarking: internal success sets external expectations

- Concentration risk: dependent on affiliate budgets

Outcome-linked RFPs and cloud-native shift squeeze margins as top accounts, affiliates dominate

Buyers use aggressive RFPs and outcome-based fees (~30% of deals include outcome metrics) to compress margins; top accounts can exceed 25% of IT services revenue. Cloud-native patterns (container use ~92%) enable selective substitution; public cloud renewals in a >$600B 2024 market reset pricing. Samsung Group affiliates provided ~40% of SDS revenue in 2024, tightening internal benchmarking and pricing pressure.

| Metric | 2024 Value |

|---|---|

| Outcome-linked deals | ~30% |

| Top-account concentration | >25% |

| Container adoption | ~92% |

| Public cloud market | >$600B |

| Affiliate revenue | ~40% |

Full Version Awaits

Samsung SDS Porter's Five Forces Analysis

This preview shows the exact Samsung SDS Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final file you will get instantly.