Samsung Heavy Industries Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

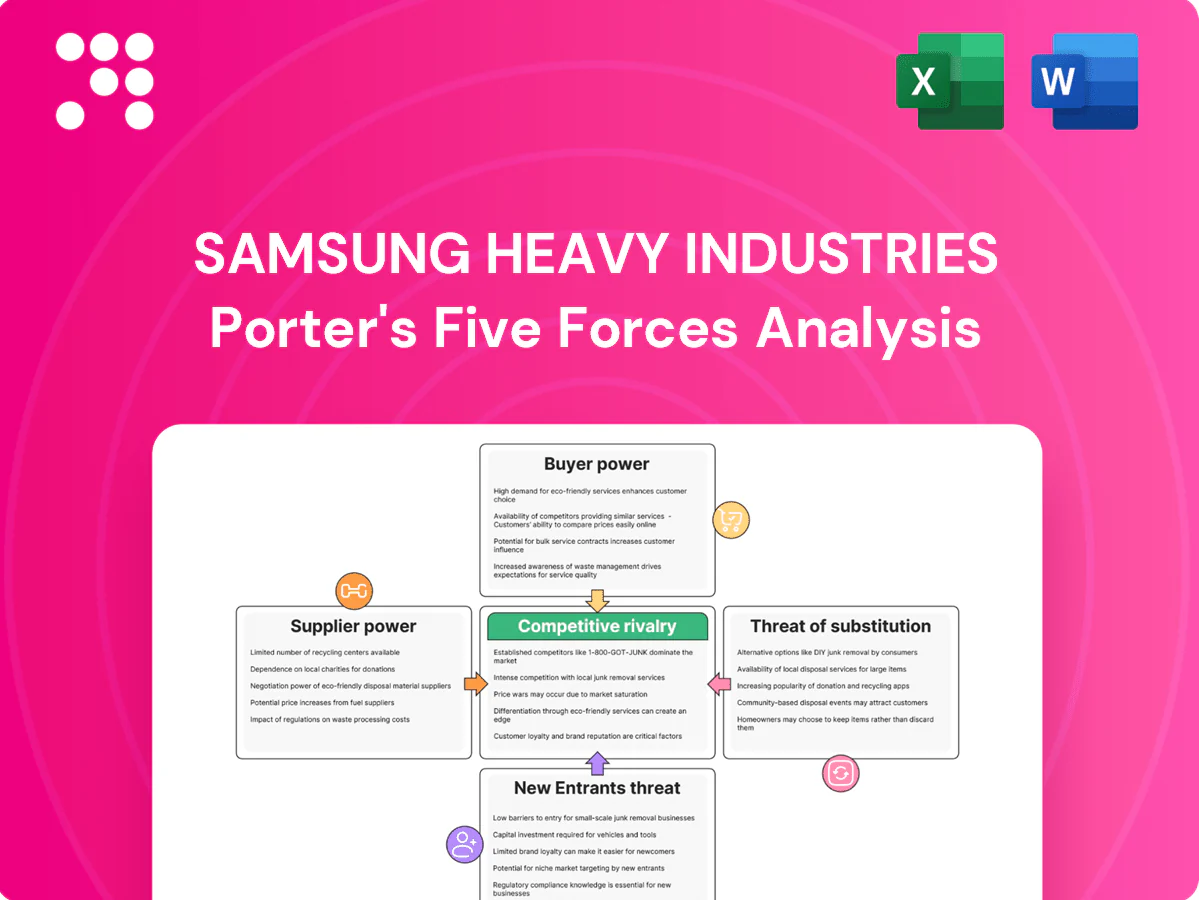

Samsung Heavy Industries faces high supplier power for specialized components, moderate buyer power among large shipowners, intense rivalry from global yards, low substitute threats, and medium new-entrant barriers due to capital intensity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Samsung Heavy Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

High-grade steel plate, LNG containment systems and propulsion components come from a narrow, certified supplier base—GTT controls roughly 60% of membrane LNG containment technology and the global LNG carrier fleet is about 650 vessels in 2024, concentrating leverage on suppliers.

That concentration raises supplier power over pricing and delivery terms, which can materially affect margins and schedules.

SHI uses multi-sourcing and long-term contracts to mitigate risk, but stringent specifications limit substitution and any disruption can ripple through large EPCIC schedules.

Technology licensors dependence

Dependence on LNG membrane licensors such as GTT—which holds roughly 70% of the membrane market—plus proprietary advanced engine designs forces SHI to meet licensor specs and pay royalties, raising supplier power. Delays or loss of licenses can render bids for high-value LNG carriers (typical newbuilds around $200–250 million) ineligible. SHI therefore pursues co-development and joint validation to reduce one-sided dependence.

Specialized equipment lead times

Winches (6–12 months), dynamic positioning systems (6–18 months), cryogenic systems (12–24 months) and topside modules (12–36 months) have long manufacturing cycles, allowing suppliers to demand front‑loaded payments and strict change controls. On mega‑projects schedule compression can raise costs by double‑digits. Early procurement and digital project planning (BIM/PLM) materially reduce schedule risk and premium spend.

Regional steel and logistics dynamics

Regional steel and logistics dynamics materially sway Samsung Heavy Industries cost baselines; in 2024 volatility in steel prices and freight disrupted project margins and scheduling. During upcycles regional mills with ship-grade certification such as POSCO and Nippon Steel gain negotiation leverage. SHI mitigates through hedging and long-term frame agreements, though strict shipbuilding specifications constrain supplier flexibility.

- 2024: certified mills (POSCO, Nippon Steel) hold leverage

- Hedging/frame agreements used to stabilize input costs

- Freight and steel volatility hit margins and schedules

- Specification constraints limit switchable sourcing

Automation and digital systems lock-in

- Vendor lock-in: integrated stacks

- After-sales leverage: lifecycle & interoperability

- Regulatory constraint: IMO MSC.428(98) & class rules

- SHI 2024: open-architecture pilots

High supplier concentration and long lead times fuel pricing leverage and delivery risk

Supplier concentration (GTT ~60% membrane, 2024 LNG fleet ~650 vessels) and certified steel mills (POSCO, Nippon Steel) give high bargaining power, pressuring prices and delivery terms.

Long lead times (winches 6–12m, DP 6–18m, cryo 12–24m) and proprietary tech raise switching costs and royalty exposure (LNG newbuilds $200–250M).

SHI mitigates via multi‑sourcing, hedging, long‑term contracts and open‑architecture pilots but supplier leverage remains material.

| Metric | 2024 |

|---|---|

| GTT share | ~60% |

| LNG fleet | ~650 vessels |

| Newbuild cost | $200–250M |

What is included in the product

Concise Porter's Five Forces analysis of Samsung Heavy Industries, highlighting competitive rivalry in shipbuilding and offshore engineering, supplier/buyer power, barriers deterring new entrants, and substitutes or disruptors affecting profitability.

One-sheet Porter’s Five Forces for Samsung Heavy Industries—visual radar of competitive pressure, customizable inputs for scenarios, copy-ready for decks and integrated dashboards.

Customers Bargaining Power

Concentrated, sophisticated buyers

Oil majors, NOCs and top liners place large, infrequent orders via competitive tenders, with technical teams imposing strict specs that heighten price and performance pressure; their volume and reputation stakes give them strong bargaining leverage. In 2024 SHI reported a roughly $7.5 billion backlog, which it leverages along with EPCIC integration and proven references to counter buyer power and win complex offshore contracts.

Project cyclicality and timing

Orders for SHI closely follow freight and LNG spreads and upstream FIDs, with global LNG FIDs reaching about 42 mtpa in 2024, shifting customer leverage across cycles.

In downturns buyers press for discounts and milestone protections, while 2024 yard slot tightening and >90% effective utilization in peak months reduced buyer bargaining power.

SHI manages vessel mix and a diversified backlog to soften cyclical swings and optimize negotiation leverage.

High switching but multi-yard strategies

Switching mid-project is costly, so buyers nonetheless pre-qualify 3–5 yards to retain options; framework agreements and repeat orders reduce switching, but competitive tenders periodically reset pricing. Performance guarantees and liquidated damages—commonly around 0.1% per day, capped near 10%—shift schedule and financial risk to builders. SHI leverages documented execution history and on-time delivery records to justify premium bids.

Customization and change orders

Complex FPSOs and LNG carriers require deep customization, and buyers frequently use design change orders to push down price and accelerate schedules; rigorous change control is essential to protect margins. SHI’s digital engineering reduces ambiguity and rework, narrowing negotiation levers for clients and preserving delivery timelines.

- Change orders used as bargaining chips

- Strict change control protects margins

- Digital engineering cuts rework and ambiguity

Financing and ESG conditions

Green financing and the Poseidon Principles, whose signatories represented over 70% of global ship finance in 2024, tie orders to emissions profiles and delivery risk, forcing buyers to require advanced fuels and digital efficiency without paying proportional premiums. SHI’s eco-ready designs strengthen its value proposition, but financing contingencies can still compress commercial terms.

Buyers have leverage; shipbuilder $7.5bn backlog, >90% utilization

Buyers wield strong leverage via infrequent large tenders, strict specs and change orders, but SHI’s $7.5bn 2024 backlog, >90% peak utilization and digital engineering plus eco-ready designs narrow buyer bargaining power; LNG FIDs ~42 mtpa and Poseidon Principles >70% of ship finance (2024) shift commercial terms; typical LD ~0.1%/day capped ~10%.

| Metric | 2024 |

|---|---|

| Backlog | $7.5bn |

| Peak utilization | >90% |

| LNG FIDs | ~42 mtpa |

| Poseidon Principles | >70% ship finance |

| LD rate | ~0.1%/day cap ~10% |

Full Version Awaits

Samsung Heavy Industries Porter's Five Forces Analysis

This preview shows the exact Samsung Heavy Industries Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally formatted document, ready to download and use the moment you buy. The contents include supplier, buyer, rivalry, substitution and entry force assessments with actionable insights.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Samsung Heavy Industries faces high supplier power for specialized components, moderate buyer power among large shipowners, intense rivalry from global yards, low substitute threats, and medium new-entrant barriers due to capital intensity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Samsung Heavy Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

High-grade steel plate, LNG containment systems and propulsion components come from a narrow, certified supplier base—GTT controls roughly 60% of membrane LNG containment technology and the global LNG carrier fleet is about 650 vessels in 2024, concentrating leverage on suppliers.

That concentration raises supplier power over pricing and delivery terms, which can materially affect margins and schedules.

SHI uses multi-sourcing and long-term contracts to mitigate risk, but stringent specifications limit substitution and any disruption can ripple through large EPCIC schedules.

Technology licensors dependence

Dependence on LNG membrane licensors such as GTT—which holds roughly 70% of the membrane market—plus proprietary advanced engine designs forces SHI to meet licensor specs and pay royalties, raising supplier power. Delays or loss of licenses can render bids for high-value LNG carriers (typical newbuilds around $200–250 million) ineligible. SHI therefore pursues co-development and joint validation to reduce one-sided dependence.

Specialized equipment lead times

Winches (6–12 months), dynamic positioning systems (6–18 months), cryogenic systems (12–24 months) and topside modules (12–36 months) have long manufacturing cycles, allowing suppliers to demand front‑loaded payments and strict change controls. On mega‑projects schedule compression can raise costs by double‑digits. Early procurement and digital project planning (BIM/PLM) materially reduce schedule risk and premium spend.

Regional steel and logistics dynamics

Regional steel and logistics dynamics materially sway Samsung Heavy Industries cost baselines; in 2024 volatility in steel prices and freight disrupted project margins and scheduling. During upcycles regional mills with ship-grade certification such as POSCO and Nippon Steel gain negotiation leverage. SHI mitigates through hedging and long-term frame agreements, though strict shipbuilding specifications constrain supplier flexibility.

- 2024: certified mills (POSCO, Nippon Steel) hold leverage

- Hedging/frame agreements used to stabilize input costs

- Freight and steel volatility hit margins and schedules

- Specification constraints limit switchable sourcing

Automation and digital systems lock-in

- Vendor lock-in: integrated stacks

- After-sales leverage: lifecycle & interoperability

- Regulatory constraint: IMO MSC.428(98) & class rules

- SHI 2024: open-architecture pilots

High supplier concentration and long lead times fuel pricing leverage and delivery risk

Supplier concentration (GTT ~60% membrane, 2024 LNG fleet ~650 vessels) and certified steel mills (POSCO, Nippon Steel) give high bargaining power, pressuring prices and delivery terms.

Long lead times (winches 6–12m, DP 6–18m, cryo 12–24m) and proprietary tech raise switching costs and royalty exposure (LNG newbuilds $200–250M).

SHI mitigates via multi‑sourcing, hedging, long‑term contracts and open‑architecture pilots but supplier leverage remains material.

| Metric | 2024 |

|---|---|

| GTT share | ~60% |

| LNG fleet | ~650 vessels |

| Newbuild cost | $200–250M |

What is included in the product

Concise Porter's Five Forces analysis of Samsung Heavy Industries, highlighting competitive rivalry in shipbuilding and offshore engineering, supplier/buyer power, barriers deterring new entrants, and substitutes or disruptors affecting profitability.

One-sheet Porter’s Five Forces for Samsung Heavy Industries—visual radar of competitive pressure, customizable inputs for scenarios, copy-ready for decks and integrated dashboards.

Customers Bargaining Power

Concentrated, sophisticated buyers

Oil majors, NOCs and top liners place large, infrequent orders via competitive tenders, with technical teams imposing strict specs that heighten price and performance pressure; their volume and reputation stakes give them strong bargaining leverage. In 2024 SHI reported a roughly $7.5 billion backlog, which it leverages along with EPCIC integration and proven references to counter buyer power and win complex offshore contracts.

Project cyclicality and timing

Orders for SHI closely follow freight and LNG spreads and upstream FIDs, with global LNG FIDs reaching about 42 mtpa in 2024, shifting customer leverage across cycles.

In downturns buyers press for discounts and milestone protections, while 2024 yard slot tightening and >90% effective utilization in peak months reduced buyer bargaining power.

SHI manages vessel mix and a diversified backlog to soften cyclical swings and optimize negotiation leverage.

High switching but multi-yard strategies

Switching mid-project is costly, so buyers nonetheless pre-qualify 3–5 yards to retain options; framework agreements and repeat orders reduce switching, but competitive tenders periodically reset pricing. Performance guarantees and liquidated damages—commonly around 0.1% per day, capped near 10%—shift schedule and financial risk to builders. SHI leverages documented execution history and on-time delivery records to justify premium bids.

Customization and change orders

Complex FPSOs and LNG carriers require deep customization, and buyers frequently use design change orders to push down price and accelerate schedules; rigorous change control is essential to protect margins. SHI’s digital engineering reduces ambiguity and rework, narrowing negotiation levers for clients and preserving delivery timelines.

- Change orders used as bargaining chips

- Strict change control protects margins

- Digital engineering cuts rework and ambiguity

Financing and ESG conditions

Green financing and the Poseidon Principles, whose signatories represented over 70% of global ship finance in 2024, tie orders to emissions profiles and delivery risk, forcing buyers to require advanced fuels and digital efficiency without paying proportional premiums. SHI’s eco-ready designs strengthen its value proposition, but financing contingencies can still compress commercial terms.

Buyers have leverage; shipbuilder $7.5bn backlog, >90% utilization

Buyers wield strong leverage via infrequent large tenders, strict specs and change orders, but SHI’s $7.5bn 2024 backlog, >90% peak utilization and digital engineering plus eco-ready designs narrow buyer bargaining power; LNG FIDs ~42 mtpa and Poseidon Principles >70% of ship finance (2024) shift commercial terms; typical LD ~0.1%/day capped ~10%.

| Metric | 2024 |

|---|---|

| Backlog | $7.5bn |

| Peak utilization | >90% |

| LNG FIDs | ~42 mtpa |

| Poseidon Principles | >70% ship finance |

| LD rate | ~0.1%/day cap ~10% |

Full Version Awaits

Samsung Heavy Industries Porter's Five Forces Analysis

This preview shows the exact Samsung Heavy Industries Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally formatted document, ready to download and use the moment you buy. The contents include supplier, buyer, rivalry, substitution and entry force assessments with actionable insights.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Samsung Heavy Industries faces high supplier power for specialized components, moderate buyer power among large shipowners, intense rivalry from global yards, low substitute threats, and medium new-entrant barriers due to capital intensity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Samsung Heavy Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

High-grade steel plate, LNG containment systems and propulsion components come from a narrow, certified supplier base—GTT controls roughly 60% of membrane LNG containment technology and the global LNG carrier fleet is about 650 vessels in 2024, concentrating leverage on suppliers.

That concentration raises supplier power over pricing and delivery terms, which can materially affect margins and schedules.

SHI uses multi-sourcing and long-term contracts to mitigate risk, but stringent specifications limit substitution and any disruption can ripple through large EPCIC schedules.

Technology licensors dependence

Dependence on LNG membrane licensors such as GTT—which holds roughly 70% of the membrane market—plus proprietary advanced engine designs forces SHI to meet licensor specs and pay royalties, raising supplier power. Delays or loss of licenses can render bids for high-value LNG carriers (typical newbuilds around $200–250 million) ineligible. SHI therefore pursues co-development and joint validation to reduce one-sided dependence.

Specialized equipment lead times

Winches (6–12 months), dynamic positioning systems (6–18 months), cryogenic systems (12–24 months) and topside modules (12–36 months) have long manufacturing cycles, allowing suppliers to demand front‑loaded payments and strict change controls. On mega‑projects schedule compression can raise costs by double‑digits. Early procurement and digital project planning (BIM/PLM) materially reduce schedule risk and premium spend.

Regional steel and logistics dynamics

Regional steel and logistics dynamics materially sway Samsung Heavy Industries cost baselines; in 2024 volatility in steel prices and freight disrupted project margins and scheduling. During upcycles regional mills with ship-grade certification such as POSCO and Nippon Steel gain negotiation leverage. SHI mitigates through hedging and long-term frame agreements, though strict shipbuilding specifications constrain supplier flexibility.

- 2024: certified mills (POSCO, Nippon Steel) hold leverage

- Hedging/frame agreements used to stabilize input costs

- Freight and steel volatility hit margins and schedules

- Specification constraints limit switchable sourcing

Automation and digital systems lock-in

- Vendor lock-in: integrated stacks

- After-sales leverage: lifecycle & interoperability

- Regulatory constraint: IMO MSC.428(98) & class rules

- SHI 2024: open-architecture pilots

High supplier concentration and long lead times fuel pricing leverage and delivery risk

Supplier concentration (GTT ~60% membrane, 2024 LNG fleet ~650 vessels) and certified steel mills (POSCO, Nippon Steel) give high bargaining power, pressuring prices and delivery terms.

Long lead times (winches 6–12m, DP 6–18m, cryo 12–24m) and proprietary tech raise switching costs and royalty exposure (LNG newbuilds $200–250M).

SHI mitigates via multi‑sourcing, hedging, long‑term contracts and open‑architecture pilots but supplier leverage remains material.

| Metric | 2024 |

|---|---|

| GTT share | ~60% |

| LNG fleet | ~650 vessels |

| Newbuild cost | $200–250M |

What is included in the product

Concise Porter's Five Forces analysis of Samsung Heavy Industries, highlighting competitive rivalry in shipbuilding and offshore engineering, supplier/buyer power, barriers deterring new entrants, and substitutes or disruptors affecting profitability.

One-sheet Porter’s Five Forces for Samsung Heavy Industries—visual radar of competitive pressure, customizable inputs for scenarios, copy-ready for decks and integrated dashboards.

Customers Bargaining Power

Concentrated, sophisticated buyers

Oil majors, NOCs and top liners place large, infrequent orders via competitive tenders, with technical teams imposing strict specs that heighten price and performance pressure; their volume and reputation stakes give them strong bargaining leverage. In 2024 SHI reported a roughly $7.5 billion backlog, which it leverages along with EPCIC integration and proven references to counter buyer power and win complex offshore contracts.

Project cyclicality and timing

Orders for SHI closely follow freight and LNG spreads and upstream FIDs, with global LNG FIDs reaching about 42 mtpa in 2024, shifting customer leverage across cycles.

In downturns buyers press for discounts and milestone protections, while 2024 yard slot tightening and >90% effective utilization in peak months reduced buyer bargaining power.

SHI manages vessel mix and a diversified backlog to soften cyclical swings and optimize negotiation leverage.

High switching but multi-yard strategies

Switching mid-project is costly, so buyers nonetheless pre-qualify 3–5 yards to retain options; framework agreements and repeat orders reduce switching, but competitive tenders periodically reset pricing. Performance guarantees and liquidated damages—commonly around 0.1% per day, capped near 10%—shift schedule and financial risk to builders. SHI leverages documented execution history and on-time delivery records to justify premium bids.

Customization and change orders

Complex FPSOs and LNG carriers require deep customization, and buyers frequently use design change orders to push down price and accelerate schedules; rigorous change control is essential to protect margins. SHI’s digital engineering reduces ambiguity and rework, narrowing negotiation levers for clients and preserving delivery timelines.

- Change orders used as bargaining chips

- Strict change control protects margins

- Digital engineering cuts rework and ambiguity

Financing and ESG conditions

Green financing and the Poseidon Principles, whose signatories represented over 70% of global ship finance in 2024, tie orders to emissions profiles and delivery risk, forcing buyers to require advanced fuels and digital efficiency without paying proportional premiums. SHI’s eco-ready designs strengthen its value proposition, but financing contingencies can still compress commercial terms.

Buyers have leverage; shipbuilder $7.5bn backlog, >90% utilization

Buyers wield strong leverage via infrequent large tenders, strict specs and change orders, but SHI’s $7.5bn 2024 backlog, >90% peak utilization and digital engineering plus eco-ready designs narrow buyer bargaining power; LNG FIDs ~42 mtpa and Poseidon Principles >70% of ship finance (2024) shift commercial terms; typical LD ~0.1%/day capped ~10%.

| Metric | 2024 |

|---|---|

| Backlog | $7.5bn |

| Peak utilization | >90% |

| LNG FIDs | ~42 mtpa |

| Poseidon Principles | >70% ship finance |

| LD rate | ~0.1%/day cap ~10% |

Full Version Awaits

Samsung Heavy Industries Porter's Five Forces Analysis

This preview shows the exact Samsung Heavy Industries Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally formatted document, ready to download and use the moment you buy. The contents include supplier, buyer, rivalry, substitution and entry force assessments with actionable insights.