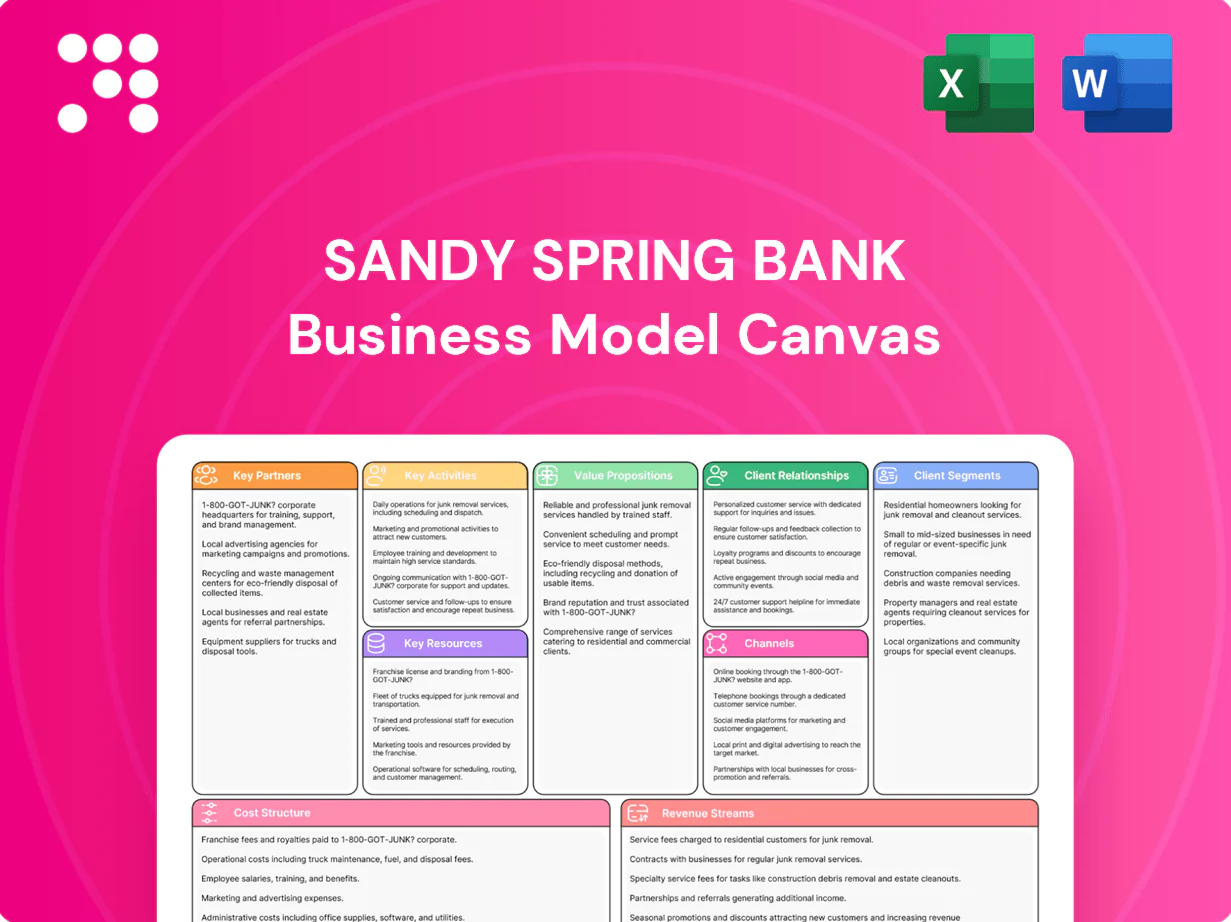

Sandy Spring Bank Business Model Canvas

Business Model Canvas for a regional community bank: value, deposits, and digital scale

Unlock the full strategic blueprint behind Sandy Spring Bank's business model. This in-depth Business Model Canvas reveals how the bank creates value, captures deposits and lending margins, and scales through partnerships and digital channels. Ideal for investors, advisors, and entrepreneurs—download the complete, editable Canvas to apply these insights to your strategy.

Partnerships

Core banking and fintech providers

Core banking and fintech partners provide Sandy Spring Bank with core processing, digital banking, payments rails and fraud detection tools, supporting customer-facing services and back-office reconciliation. Service-level agreements commonly guarantee 99.9%+ uptime and adherence to PCI DSS and SOC 2 controls, enabling secure, scalable operations and rapid feature rollout. Co-development partnerships shorten time-to-market and control costs while meeting regulatory-grade integrations.

Payment networks and card processors

Visa and Mastercard, plus ACH and The Clearing House RTP, power Sandy Spring Bank card and transfer rails, with U.S. ACH moving about $76.5 trillion across roughly 33 billion payments in 2023 and RTP enabling real‑time, 24/7 settlement. Card processors provide acceptance, clearing, settlement and dispute resolution, expanding merchant and consumer utility. Interchange (commonly 1–3%) and transaction reliability drive client satisfaction.

Mortgage investors and brokers

Secondary market partners such as agencies and investors provide liquidity—agents guarantee roughly 70% of U.S. single-family originations—enabling Sandy Spring to convert loans to securities and redeploy capital. Broker relationships expand origination reach and product variety, feeding both retail originations and correspondent channels. Selling versus servicing decisions and whole-loan sales optimize balance-sheet capacity, while pipeline hedging and delivery commitments limit rate and basis risk.

Wealth custodians and asset managers

Custodians safeguard client assets and streamline reporting while asset managers supply diversified products from ETFs to SMAs and alternatives, enabling scalable portfolio construction. Open-architecture platforms enhance client fit and risk-adjusted returns by broadening investable options and easing rebalancing. Revenue-sharing agreements and rigorous due diligence keep incentives aligned and control counterparty risk.

- Custodians: asset safety, reporting

- Managers: ETFs, SMAs, alternatives

- Open-architecture: improved fit

- Alignment: revenue-sharing, due diligence

Community organizations and regulators

Community nonprofits, chambers, and housing agencies help Sandy Spring Bank extend outreach, financial education, and affordable housing support; collaboration strengthens CRA performance and local loan originations. Regulators including the FDIC and Federal Reserve guide safety, soundness, and compliance while transparent engagement builds trust and operating stability. Sandy Spring Bancorp reported about $13 billion in assets in 2024.

- Community partners: outreach, education, housing

- Regulators: safety, compliance, CRA guidance

- Impact: stronger inclusion, stable operations

99.9% SLA fintech-core stack accelerates PCI/SOC2 payments: ACH $76.5T, RTP, 1–3% interchange

Core banking and fintech partners deliver processing, digital channels, payments rails and fraud tools with 99.9%+ SLA, PCI DSS and SOC 2 compliance, shortening time-to-market. Visa/Mastercard, ACH ($76.5T, ~33B payments in 2023) and RTP enable card/real-time rails; interchange ~1–3%. Agencies/backing cover ~70% of US single-family originations, aiding liquidity; Sandy Spring Bancorp assets ~$13B (2024).

| Partner | Role | Key metric |

|---|---|---|

| Core/Fintech | Processing, digital, fraud | 99.9%+ SLA, PCI/SOC2 |

| Card/Rails | Payments, clearing | ACH $76.5T (2023), 1–3% interchange |

| Agencies/Investors | Liquidity, secondary market | ~70% guarantee on SF originations |

| Community/Regulators | Outreach, compliance | $13B assets (2024) |

What is included in the product

A comprehensive Business Model Canvas for Sandy Spring Bank detailing customer segments, channels, value propositions, revenue streams, key resources and partners across the 9 BMC blocks, reflecting real-world retail and commercial banking operations; ideal for presentations, investor discussions and strategic analysis with linked SWOT and competitive-advantage insights.

Condenses Sandy Spring Bank’s strategy into a digestible one-page snapshot with editable cells, saving hours of formatting and enabling teams to quickly identify core components, adapt to regulatory or product shifts, and collaborate on solutions to customer and operational pain points.

Activities

Deposit gathering and liquidity management

Design and price deposit products to attract stable, low-cost core funding while using cash, FHLB lines and liquid securities to maintain day-to-day and contingency liquidity. Execute asset-liability management to balance duration and interest-rate risk across the balance sheet, running scenario-driven gap and stress tests. Continuously monitor deposit and loan flows to protect net interest margin and operational resilience.

Lending origination, underwriting, and servicing

Sandy Spring Bank generates commercial, consumer, and mortgage loans while performing rigorous credit analysis, collateral evaluation, and risk-based pricing. The bank services portfolios with payment processing, loan modifications, and workout strategies to preserve asset quality. It enforces credit policy discipline across cycles to limit charge-offs and support capital stability.

Wealth management and fiduciary services

Advise clients on investments, trusts and estates through Sandy Spring Bank (SASR), aligning portfolios to goals and risk tolerance while integrating retirement, tax and generational transfer planning. Construct diversified portfolios and model scenarios to meet target outcomes. Ongoing reviews maintain performance and regulatory compliance across Maryland, D.C. and Virginia.

Risk, compliance, and cybersecurity

Sandy Spring Bank operates robust BSA/AML, KYC, and fair lending programs, conducts stress tests and model validation, and enforces vendor oversight to meet regulatory standards; in 2023 U.S. fraud losses reported to the FBI IC3 totaled about 10.3 billion dollars, underscoring the need for strong controls. The bank monitors threats, hardens defenses with layered controls, trains staff, and performs continuous audits to close gaps.

- Program scope: BSA/AML, KYC, fair lending

- Controls: layered defenses, continuous monitoring

- Testing: stress tests, model validation

- Governance: vendor oversight, training, audits

Digital product development and client support

Digital product development focuses on enhancing mobile, online, and API experiences for Sandy Spring Bank, while client support resolves issues through contact centers and relationship managers to maintain service quality.

Analytics personalize offers and identify churn signals, driving targeted retention actions; NPS is tracked regularly to guide rapid feature iteration and prioritization.

- Enhance mobile/online/API UX

- Contact centers + RMs resolve issues

- Use analytics to personalize and reduce churn

- Measure NPS and iterate fast

Low-cost deposits, ALM, strict underwriting; IC3 fraud losses $10.3B

Design and price deposits to secure low‑cost core funding and manage liquidity via cash, FHLB lines and securities; execute ALM with scenario gap and stress tests. Originate and service commercial, consumer and mortgage loans with strict credit underwriting and workouts to protect asset quality. Develop digital channels, analytics and advisory services to improve NPS and reduce churn; reinforce BSA/AML controls—2023 FBI IC3 losses $10.3B.

| Metric | Value |

|---|---|

| FBI IC3 fraud losses (2023) | $10.3B |

Full Document Unlocks After Purchase

Business Model Canvas

The document you’re previewing is the actual Sandy Spring Bank Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact, fully formatted file—ready to edit, present, and apply. No surprises: the preview equals the final deliverable in full.

Business Model Canvas for a regional community bank: value, deposits, and digital scale

Unlock the full strategic blueprint behind Sandy Spring Bank's business model. This in-depth Business Model Canvas reveals how the bank creates value, captures deposits and lending margins, and scales through partnerships and digital channels. Ideal for investors, advisors, and entrepreneurs—download the complete, editable Canvas to apply these insights to your strategy.

Partnerships

Core banking and fintech providers

Core banking and fintech partners provide Sandy Spring Bank with core processing, digital banking, payments rails and fraud detection tools, supporting customer-facing services and back-office reconciliation. Service-level agreements commonly guarantee 99.9%+ uptime and adherence to PCI DSS and SOC 2 controls, enabling secure, scalable operations and rapid feature rollout. Co-development partnerships shorten time-to-market and control costs while meeting regulatory-grade integrations.

Payment networks and card processors

Visa and Mastercard, plus ACH and The Clearing House RTP, power Sandy Spring Bank card and transfer rails, with U.S. ACH moving about $76.5 trillion across roughly 33 billion payments in 2023 and RTP enabling real‑time, 24/7 settlement. Card processors provide acceptance, clearing, settlement and dispute resolution, expanding merchant and consumer utility. Interchange (commonly 1–3%) and transaction reliability drive client satisfaction.

Mortgage investors and brokers

Secondary market partners such as agencies and investors provide liquidity—agents guarantee roughly 70% of U.S. single-family originations—enabling Sandy Spring to convert loans to securities and redeploy capital. Broker relationships expand origination reach and product variety, feeding both retail originations and correspondent channels. Selling versus servicing decisions and whole-loan sales optimize balance-sheet capacity, while pipeline hedging and delivery commitments limit rate and basis risk.

Wealth custodians and asset managers

Custodians safeguard client assets and streamline reporting while asset managers supply diversified products from ETFs to SMAs and alternatives, enabling scalable portfolio construction. Open-architecture platforms enhance client fit and risk-adjusted returns by broadening investable options and easing rebalancing. Revenue-sharing agreements and rigorous due diligence keep incentives aligned and control counterparty risk.

- Custodians: asset safety, reporting

- Managers: ETFs, SMAs, alternatives

- Open-architecture: improved fit

- Alignment: revenue-sharing, due diligence

Community organizations and regulators

Community nonprofits, chambers, and housing agencies help Sandy Spring Bank extend outreach, financial education, and affordable housing support; collaboration strengthens CRA performance and local loan originations. Regulators including the FDIC and Federal Reserve guide safety, soundness, and compliance while transparent engagement builds trust and operating stability. Sandy Spring Bancorp reported about $13 billion in assets in 2024.

- Community partners: outreach, education, housing

- Regulators: safety, compliance, CRA guidance

- Impact: stronger inclusion, stable operations

99.9% SLA fintech-core stack accelerates PCI/SOC2 payments: ACH $76.5T, RTP, 1–3% interchange

Core banking and fintech partners deliver processing, digital channels, payments rails and fraud tools with 99.9%+ SLA, PCI DSS and SOC 2 compliance, shortening time-to-market. Visa/Mastercard, ACH ($76.5T, ~33B payments in 2023) and RTP enable card/real-time rails; interchange ~1–3%. Agencies/backing cover ~70% of US single-family originations, aiding liquidity; Sandy Spring Bancorp assets ~$13B (2024).

| Partner | Role | Key metric |

|---|---|---|

| Core/Fintech | Processing, digital, fraud | 99.9%+ SLA, PCI/SOC2 |

| Card/Rails | Payments, clearing | ACH $76.5T (2023), 1–3% interchange |

| Agencies/Investors | Liquidity, secondary market | ~70% guarantee on SF originations |

| Community/Regulators | Outreach, compliance | $13B assets (2024) |

What is included in the product

A comprehensive Business Model Canvas for Sandy Spring Bank detailing customer segments, channels, value propositions, revenue streams, key resources and partners across the 9 BMC blocks, reflecting real-world retail and commercial banking operations; ideal for presentations, investor discussions and strategic analysis with linked SWOT and competitive-advantage insights.

Condenses Sandy Spring Bank’s strategy into a digestible one-page snapshot with editable cells, saving hours of formatting and enabling teams to quickly identify core components, adapt to regulatory or product shifts, and collaborate on solutions to customer and operational pain points.

Activities

Deposit gathering and liquidity management

Design and price deposit products to attract stable, low-cost core funding while using cash, FHLB lines and liquid securities to maintain day-to-day and contingency liquidity. Execute asset-liability management to balance duration and interest-rate risk across the balance sheet, running scenario-driven gap and stress tests. Continuously monitor deposit and loan flows to protect net interest margin and operational resilience.

Lending origination, underwriting, and servicing

Sandy Spring Bank generates commercial, consumer, and mortgage loans while performing rigorous credit analysis, collateral evaluation, and risk-based pricing. The bank services portfolios with payment processing, loan modifications, and workout strategies to preserve asset quality. It enforces credit policy discipline across cycles to limit charge-offs and support capital stability.

Wealth management and fiduciary services

Advise clients on investments, trusts and estates through Sandy Spring Bank (SASR), aligning portfolios to goals and risk tolerance while integrating retirement, tax and generational transfer planning. Construct diversified portfolios and model scenarios to meet target outcomes. Ongoing reviews maintain performance and regulatory compliance across Maryland, D.C. and Virginia.

Risk, compliance, and cybersecurity

Sandy Spring Bank operates robust BSA/AML, KYC, and fair lending programs, conducts stress tests and model validation, and enforces vendor oversight to meet regulatory standards; in 2023 U.S. fraud losses reported to the FBI IC3 totaled about 10.3 billion dollars, underscoring the need for strong controls. The bank monitors threats, hardens defenses with layered controls, trains staff, and performs continuous audits to close gaps.

- Program scope: BSA/AML, KYC, fair lending

- Controls: layered defenses, continuous monitoring

- Testing: stress tests, model validation

- Governance: vendor oversight, training, audits

Digital product development and client support

Digital product development focuses on enhancing mobile, online, and API experiences for Sandy Spring Bank, while client support resolves issues through contact centers and relationship managers to maintain service quality.

Analytics personalize offers and identify churn signals, driving targeted retention actions; NPS is tracked regularly to guide rapid feature iteration and prioritization.

- Enhance mobile/online/API UX

- Contact centers + RMs resolve issues

- Use analytics to personalize and reduce churn

- Measure NPS and iterate fast

Low-cost deposits, ALM, strict underwriting; IC3 fraud losses $10.3B

Design and price deposits to secure low‑cost core funding and manage liquidity via cash, FHLB lines and securities; execute ALM with scenario gap and stress tests. Originate and service commercial, consumer and mortgage loans with strict credit underwriting and workouts to protect asset quality. Develop digital channels, analytics and advisory services to improve NPS and reduce churn; reinforce BSA/AML controls—2023 FBI IC3 losses $10.3B.

| Metric | Value |

|---|---|

| FBI IC3 fraud losses (2023) | $10.3B |

Full Document Unlocks After Purchase

Business Model Canvas

The document you’re previewing is the actual Sandy Spring Bank Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact, fully formatted file—ready to edit, present, and apply. No surprises: the preview equals the final deliverable in full.

Description

Business Model Canvas for a regional community bank: value, deposits, and digital scale

Unlock the full strategic blueprint behind Sandy Spring Bank's business model. This in-depth Business Model Canvas reveals how the bank creates value, captures deposits and lending margins, and scales through partnerships and digital channels. Ideal for investors, advisors, and entrepreneurs—download the complete, editable Canvas to apply these insights to your strategy.

Partnerships

Core banking and fintech providers

Core banking and fintech partners provide Sandy Spring Bank with core processing, digital banking, payments rails and fraud detection tools, supporting customer-facing services and back-office reconciliation. Service-level agreements commonly guarantee 99.9%+ uptime and adherence to PCI DSS and SOC 2 controls, enabling secure, scalable operations and rapid feature rollout. Co-development partnerships shorten time-to-market and control costs while meeting regulatory-grade integrations.

Payment networks and card processors

Visa and Mastercard, plus ACH and The Clearing House RTP, power Sandy Spring Bank card and transfer rails, with U.S. ACH moving about $76.5 trillion across roughly 33 billion payments in 2023 and RTP enabling real‑time, 24/7 settlement. Card processors provide acceptance, clearing, settlement and dispute resolution, expanding merchant and consumer utility. Interchange (commonly 1–3%) and transaction reliability drive client satisfaction.

Mortgage investors and brokers

Secondary market partners such as agencies and investors provide liquidity—agents guarantee roughly 70% of U.S. single-family originations—enabling Sandy Spring to convert loans to securities and redeploy capital. Broker relationships expand origination reach and product variety, feeding both retail originations and correspondent channels. Selling versus servicing decisions and whole-loan sales optimize balance-sheet capacity, while pipeline hedging and delivery commitments limit rate and basis risk.

Wealth custodians and asset managers

Custodians safeguard client assets and streamline reporting while asset managers supply diversified products from ETFs to SMAs and alternatives, enabling scalable portfolio construction. Open-architecture platforms enhance client fit and risk-adjusted returns by broadening investable options and easing rebalancing. Revenue-sharing agreements and rigorous due diligence keep incentives aligned and control counterparty risk.

- Custodians: asset safety, reporting

- Managers: ETFs, SMAs, alternatives

- Open-architecture: improved fit

- Alignment: revenue-sharing, due diligence

Community organizations and regulators

Community nonprofits, chambers, and housing agencies help Sandy Spring Bank extend outreach, financial education, and affordable housing support; collaboration strengthens CRA performance and local loan originations. Regulators including the FDIC and Federal Reserve guide safety, soundness, and compliance while transparent engagement builds trust and operating stability. Sandy Spring Bancorp reported about $13 billion in assets in 2024.

- Community partners: outreach, education, housing

- Regulators: safety, compliance, CRA guidance

- Impact: stronger inclusion, stable operations

99.9% SLA fintech-core stack accelerates PCI/SOC2 payments: ACH $76.5T, RTP, 1–3% interchange

Core banking and fintech partners deliver processing, digital channels, payments rails and fraud tools with 99.9%+ SLA, PCI DSS and SOC 2 compliance, shortening time-to-market. Visa/Mastercard, ACH ($76.5T, ~33B payments in 2023) and RTP enable card/real-time rails; interchange ~1–3%. Agencies/backing cover ~70% of US single-family originations, aiding liquidity; Sandy Spring Bancorp assets ~$13B (2024).

| Partner | Role | Key metric |

|---|---|---|

| Core/Fintech | Processing, digital, fraud | 99.9%+ SLA, PCI/SOC2 |

| Card/Rails | Payments, clearing | ACH $76.5T (2023), 1–3% interchange |

| Agencies/Investors | Liquidity, secondary market | ~70% guarantee on SF originations |

| Community/Regulators | Outreach, compliance | $13B assets (2024) |

What is included in the product

A comprehensive Business Model Canvas for Sandy Spring Bank detailing customer segments, channels, value propositions, revenue streams, key resources and partners across the 9 BMC blocks, reflecting real-world retail and commercial banking operations; ideal for presentations, investor discussions and strategic analysis with linked SWOT and competitive-advantage insights.

Condenses Sandy Spring Bank’s strategy into a digestible one-page snapshot with editable cells, saving hours of formatting and enabling teams to quickly identify core components, adapt to regulatory or product shifts, and collaborate on solutions to customer and operational pain points.

Activities

Deposit gathering and liquidity management

Design and price deposit products to attract stable, low-cost core funding while using cash, FHLB lines and liquid securities to maintain day-to-day and contingency liquidity. Execute asset-liability management to balance duration and interest-rate risk across the balance sheet, running scenario-driven gap and stress tests. Continuously monitor deposit and loan flows to protect net interest margin and operational resilience.

Lending origination, underwriting, and servicing

Sandy Spring Bank generates commercial, consumer, and mortgage loans while performing rigorous credit analysis, collateral evaluation, and risk-based pricing. The bank services portfolios with payment processing, loan modifications, and workout strategies to preserve asset quality. It enforces credit policy discipline across cycles to limit charge-offs and support capital stability.

Wealth management and fiduciary services

Advise clients on investments, trusts and estates through Sandy Spring Bank (SASR), aligning portfolios to goals and risk tolerance while integrating retirement, tax and generational transfer planning. Construct diversified portfolios and model scenarios to meet target outcomes. Ongoing reviews maintain performance and regulatory compliance across Maryland, D.C. and Virginia.

Risk, compliance, and cybersecurity

Sandy Spring Bank operates robust BSA/AML, KYC, and fair lending programs, conducts stress tests and model validation, and enforces vendor oversight to meet regulatory standards; in 2023 U.S. fraud losses reported to the FBI IC3 totaled about 10.3 billion dollars, underscoring the need for strong controls. The bank monitors threats, hardens defenses with layered controls, trains staff, and performs continuous audits to close gaps.

- Program scope: BSA/AML, KYC, fair lending

- Controls: layered defenses, continuous monitoring

- Testing: stress tests, model validation

- Governance: vendor oversight, training, audits

Digital product development and client support

Digital product development focuses on enhancing mobile, online, and API experiences for Sandy Spring Bank, while client support resolves issues through contact centers and relationship managers to maintain service quality.

Analytics personalize offers and identify churn signals, driving targeted retention actions; NPS is tracked regularly to guide rapid feature iteration and prioritization.

- Enhance mobile/online/API UX

- Contact centers + RMs resolve issues

- Use analytics to personalize and reduce churn

- Measure NPS and iterate fast

Low-cost deposits, ALM, strict underwriting; IC3 fraud losses $10.3B

Design and price deposits to secure low‑cost core funding and manage liquidity via cash, FHLB lines and securities; execute ALM with scenario gap and stress tests. Originate and service commercial, consumer and mortgage loans with strict credit underwriting and workouts to protect asset quality. Develop digital channels, analytics and advisory services to improve NPS and reduce churn; reinforce BSA/AML controls—2023 FBI IC3 losses $10.3B.

| Metric | Value |

|---|---|

| FBI IC3 fraud losses (2023) | $10.3B |

Full Document Unlocks After Purchase

Business Model Canvas

The document you’re previewing is the actual Sandy Spring Bank Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact, fully formatted file—ready to edit, present, and apply. No surprises: the preview equals the final deliverable in full.