Beijing Sanyuan Foods Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

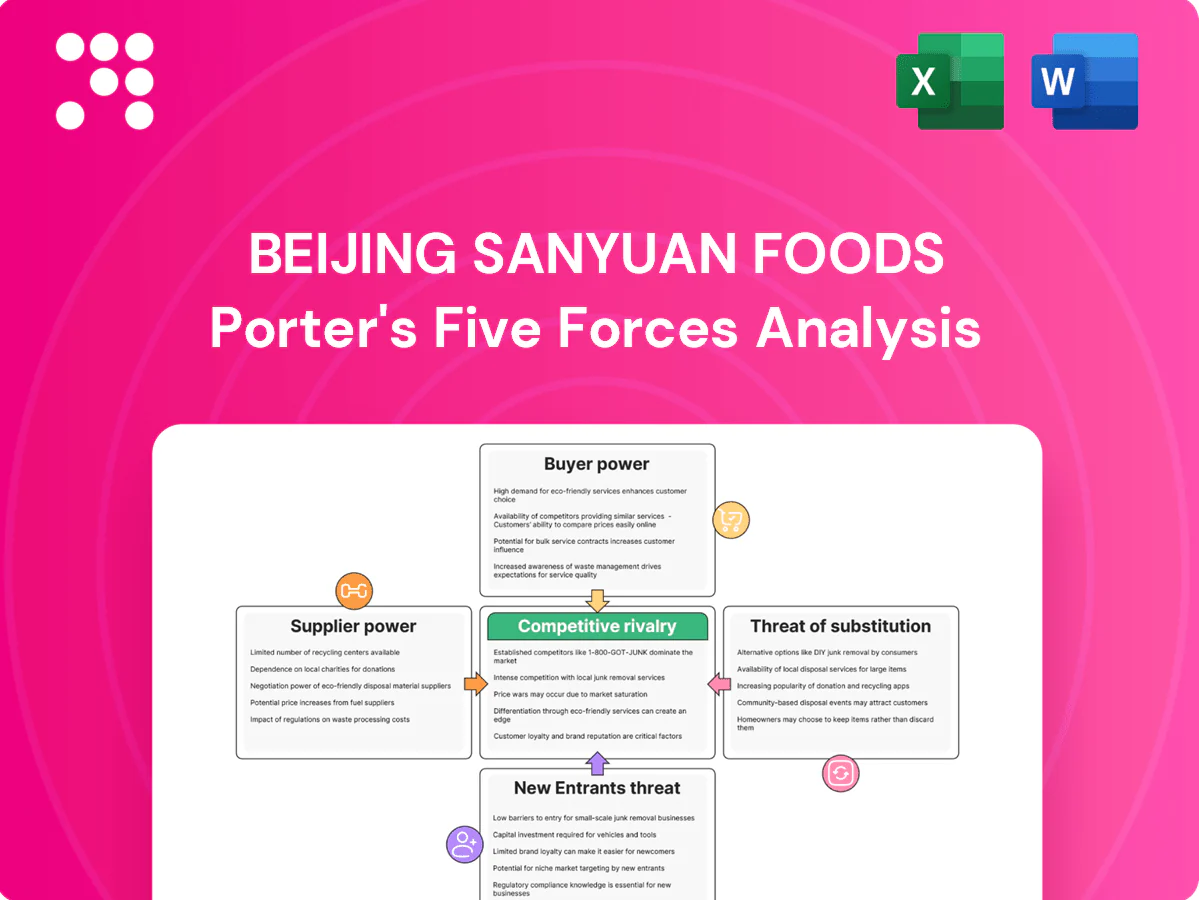

Beijing Sanyuan Foods faces moderate buyer power, intense rivalry among domestic dairy and packaged-food players, and growing substitute threats from plant-based and private-label brands, while supplier leverage is constrained by scale and regulatory oversight. Regulatory shifts and distribution costs add pressure but also create moats for compliant leaders. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sanyuan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw milk

Raw milk is the critical input and concentrated supply gives large-scale dairy farms and cooperatives leverage, with over 50% of China’s raw milk now sourced from large suppliers, elevating their bargaining power. Weather, feed-cost spikes and disease outbreaks have caused cyclical tightness and price swings—feed costs rose ~15–25% in 2022–24. Sanyuan tempers volatility through long-term contracts, partial vertical integration and proximity to Beijing, lowering transport and freshness risk.

Feed and inputs volatility

Feed grains, energy and additives cascade directly into raw milk costs, with feed often representing about 60% of dairy production costs and giving upstream agribusiness significant leverage during input-price spikes. Currency and commodity cycles in 2024 have rapidly shifted bargaining positions. Hedging and diversified sourcing mitigate but do not eliminate exposure. Procurement scale yields partial offset via stronger negotiated terms.

Specialty cultures & ingredients

Specialty probiotic strains, enzymes, cocoa and flavor houses are highly specialized and less interchangeable, with the top 5 global flavor houses holding about 60% market share in 2024, boosting supplier power over Beijing Sanyuan. IP-protected cultures and certification requirements (e.g., strain dossiers, GRAS/CFDA records) limit fast switching. Dual-sourcing and in-house R&D can reduce dependency and procurement risk by roughly 30%, while large yogurt volumes give Sanyuan negotiating leverage though niche inputs remain priced at a premium.

Packaging & cold chain

Packaging suppliers for Tetra Pak, HDPE and film are numerous, but tight specifications and multi-week lead times create procurement frictions for Beijing Sanyuan Foods; refrigerated logistics capacity tightens sharply in peak seasons, giving 3PLs leverage on spot rates. Long-term supplier and 3PL partnerships improve service levels and stabilize pricing. Owning segments of the cold chain—warehouses or fleets—reduces external supplier bargaining power and mitigates rate volatility.

Quality and compliance

Stringent Chinese dairy standards—heightened after the 2008 melamine crisis that sickened about 300,000 infants—raise the value of reliable, certified suppliers, enabling those with robust QA to command better pricing and contract terms.

Traceability mandates and mandatory audits increase near-term switching costs for buyers, while audits and digital traceability platforms (widely adopted across large processors) rebalance supplier power by boosting transparency and reducing information asymmetry.

- Certified-suppliers-premium

- Traceability-raises-switching-costs

- QA-enables-better-terms

- Audits-digital-traceability-increase-transparency

Dairy margins pressured by concentrated suppliers, 15-25% feed surge and flavor oligopoly

Beijing Sanyuan faces elevated supplier power: large farms supply >50% raw milk, feed accounts for ~60% of milk cost and rose 15–25% in 2022–24, and top‑5 flavor houses hold ~60% share—long contracts, partial vertical integration and cold‑chain ownership partly offset this pressure.

| Input | 2024 metric |

|---|---|

| Raw milk concentration | >50% from large suppliers |

| Feed cost share | ~60% of production cost |

| Feed cost change | +15–25% (2022–24) |

| Flavor house share | Top 5 ≈60% |

What is included in the product

Tailored Porter's Five Forces analysis for Beijing Sanyuan Foods that uncovers competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive risks and strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Beijing Sanyuan Foods — instantly visualize supplier/buyer pressure, rivalry, substitutes and entry threats with an editable spider chart and customizable scores, ready to drop into decks or dashboards for fast strategic decisions.

Customers Bargaining Power

Retailer concentration

National chains, convenience formats and e-commerce platforms (Alibaba + JD account for over 60% of online grocery sales in 2024) control shelf space and promotional calendars, forcing Beijing Sanyuan onto tough trade terms, returns policies and slotting fees. Their scale enables aggressive price/timing demands and private label expansion (private-label dairy roughly 10% penetration in modern trade). Strong Sanyuan brands and must-have SKUs partially offset this bargaining power.

Price-sensitive consumers

Milk and yogurt are frequent, low-involvement purchases with clear price anchors, and China’s retail dairy market was roughly US$60 billion in 2024, amplifying sensitivity to price moves. Low switching costs and heavy promotion cycles (weekend and festival discounts) mean consumers quickly shift brands, pressuring margins. Premium functional SKUs lower elasticity but require continuous R&D and marketing investment. Economic downturns increase trading-down risk and promotional dependence.

Digital comparison

E-commerce and social platforms let buyers compare prices and reviews instantly; over 1 billion mobile internet users in China (CNNIC 2024) amplify this transparency. Flash sales and livestreaming compress margins, with livestreaming GMV exceeding RMB1.5 trillion in 2024 (iMedia 2024). DTC channels can reclaim data and several percentage points of margin. Loyalty programs and subscriptions increase stickiness.

Foodservice and B2B

- bulk discounts: 5–10%

- typical monthly volume: 1–10 tonnes

- custom specs: raise dependency

- delivery reliability: key retention lever

Quality and safety expectations

Post-scandal Chinese consumers now prioritize safety and freshness, pushing buyers to favor brands with clear traceability; 2024 surveys report over 70% of urban consumers willing to pay premiums for traceable dairy, allowing firms like Beijing Sanyuan to reduce buyer power if certified; any safety lapse quickly triggers churn and restores bargaining leverage to customers.

- traceability premium: >70% willing to pay

- certifications: drive price resilience

- testing transparency: lowers churn risk

E-commerce squeeze 60% online grocery fuels margin pressure in China dairy

Retailers and e-commerce (Alibaba+JD ~60% online grocery 2024) exert strong trade leverage, squeezing margins; low switching costs and promotions keep consumer price sensitivity high in China’s ~US$60bn dairy market (2024). Livestreaming (GMV RMB1.5tr 2024) and >70% traceability premium shift power to informed buyers, while bulk buyers secure 5–10% discounts; DTC can recover ~3–5ppt margin.

| Metric | 2024 Value |

|---|---|

| Online grocery share (Alibaba+JD) | ~60% |

| China dairy market | ~US$60bn |

| Livestreaming GMV | RMB1.5tn |

| Traceability premium | >70% willing to pay |

| Bulk discounts | 5–10% |

| DTC margin recovery | ~3–5ppt |

Full Version Awaits

Beijing Sanyuan Foods Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Beijing Sanyuan Foods you'll receive after purchase, fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, with actionable insights and no placeholders. Instant download upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Beijing Sanyuan Foods faces moderate buyer power, intense rivalry among domestic dairy and packaged-food players, and growing substitute threats from plant-based and private-label brands, while supplier leverage is constrained by scale and regulatory oversight. Regulatory shifts and distribution costs add pressure but also create moats for compliant leaders. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sanyuan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw milk

Raw milk is the critical input and concentrated supply gives large-scale dairy farms and cooperatives leverage, with over 50% of China’s raw milk now sourced from large suppliers, elevating their bargaining power. Weather, feed-cost spikes and disease outbreaks have caused cyclical tightness and price swings—feed costs rose ~15–25% in 2022–24. Sanyuan tempers volatility through long-term contracts, partial vertical integration and proximity to Beijing, lowering transport and freshness risk.

Feed and inputs volatility

Feed grains, energy and additives cascade directly into raw milk costs, with feed often representing about 60% of dairy production costs and giving upstream agribusiness significant leverage during input-price spikes. Currency and commodity cycles in 2024 have rapidly shifted bargaining positions. Hedging and diversified sourcing mitigate but do not eliminate exposure. Procurement scale yields partial offset via stronger negotiated terms.

Specialty cultures & ingredients

Specialty probiotic strains, enzymes, cocoa and flavor houses are highly specialized and less interchangeable, with the top 5 global flavor houses holding about 60% market share in 2024, boosting supplier power over Beijing Sanyuan. IP-protected cultures and certification requirements (e.g., strain dossiers, GRAS/CFDA records) limit fast switching. Dual-sourcing and in-house R&D can reduce dependency and procurement risk by roughly 30%, while large yogurt volumes give Sanyuan negotiating leverage though niche inputs remain priced at a premium.

Packaging & cold chain

Packaging suppliers for Tetra Pak, HDPE and film are numerous, but tight specifications and multi-week lead times create procurement frictions for Beijing Sanyuan Foods; refrigerated logistics capacity tightens sharply in peak seasons, giving 3PLs leverage on spot rates. Long-term supplier and 3PL partnerships improve service levels and stabilize pricing. Owning segments of the cold chain—warehouses or fleets—reduces external supplier bargaining power and mitigates rate volatility.

Quality and compliance

Stringent Chinese dairy standards—heightened after the 2008 melamine crisis that sickened about 300,000 infants—raise the value of reliable, certified suppliers, enabling those with robust QA to command better pricing and contract terms.

Traceability mandates and mandatory audits increase near-term switching costs for buyers, while audits and digital traceability platforms (widely adopted across large processors) rebalance supplier power by boosting transparency and reducing information asymmetry.

- Certified-suppliers-premium

- Traceability-raises-switching-costs

- QA-enables-better-terms

- Audits-digital-traceability-increase-transparency

Dairy margins pressured by concentrated suppliers, 15-25% feed surge and flavor oligopoly

Beijing Sanyuan faces elevated supplier power: large farms supply >50% raw milk, feed accounts for ~60% of milk cost and rose 15–25% in 2022–24, and top‑5 flavor houses hold ~60% share—long contracts, partial vertical integration and cold‑chain ownership partly offset this pressure.

| Input | 2024 metric |

|---|---|

| Raw milk concentration | >50% from large suppliers |

| Feed cost share | ~60% of production cost |

| Feed cost change | +15–25% (2022–24) |

| Flavor house share | Top 5 ≈60% |

What is included in the product

Tailored Porter's Five Forces analysis for Beijing Sanyuan Foods that uncovers competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive risks and strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Beijing Sanyuan Foods — instantly visualize supplier/buyer pressure, rivalry, substitutes and entry threats with an editable spider chart and customizable scores, ready to drop into decks or dashboards for fast strategic decisions.

Customers Bargaining Power

Retailer concentration

National chains, convenience formats and e-commerce platforms (Alibaba + JD account for over 60% of online grocery sales in 2024) control shelf space and promotional calendars, forcing Beijing Sanyuan onto tough trade terms, returns policies and slotting fees. Their scale enables aggressive price/timing demands and private label expansion (private-label dairy roughly 10% penetration in modern trade). Strong Sanyuan brands and must-have SKUs partially offset this bargaining power.

Price-sensitive consumers

Milk and yogurt are frequent, low-involvement purchases with clear price anchors, and China’s retail dairy market was roughly US$60 billion in 2024, amplifying sensitivity to price moves. Low switching costs and heavy promotion cycles (weekend and festival discounts) mean consumers quickly shift brands, pressuring margins. Premium functional SKUs lower elasticity but require continuous R&D and marketing investment. Economic downturns increase trading-down risk and promotional dependence.

Digital comparison

E-commerce and social platforms let buyers compare prices and reviews instantly; over 1 billion mobile internet users in China (CNNIC 2024) amplify this transparency. Flash sales and livestreaming compress margins, with livestreaming GMV exceeding RMB1.5 trillion in 2024 (iMedia 2024). DTC channels can reclaim data and several percentage points of margin. Loyalty programs and subscriptions increase stickiness.

Foodservice and B2B

- bulk discounts: 5–10%

- typical monthly volume: 1–10 tonnes

- custom specs: raise dependency

- delivery reliability: key retention lever

Quality and safety expectations

Post-scandal Chinese consumers now prioritize safety and freshness, pushing buyers to favor brands with clear traceability; 2024 surveys report over 70% of urban consumers willing to pay premiums for traceable dairy, allowing firms like Beijing Sanyuan to reduce buyer power if certified; any safety lapse quickly triggers churn and restores bargaining leverage to customers.

- traceability premium: >70% willing to pay

- certifications: drive price resilience

- testing transparency: lowers churn risk

E-commerce squeeze 60% online grocery fuels margin pressure in China dairy

Retailers and e-commerce (Alibaba+JD ~60% online grocery 2024) exert strong trade leverage, squeezing margins; low switching costs and promotions keep consumer price sensitivity high in China’s ~US$60bn dairy market (2024). Livestreaming (GMV RMB1.5tr 2024) and >70% traceability premium shift power to informed buyers, while bulk buyers secure 5–10% discounts; DTC can recover ~3–5ppt margin.

| Metric | 2024 Value |

|---|---|

| Online grocery share (Alibaba+JD) | ~60% |

| China dairy market | ~US$60bn |

| Livestreaming GMV | RMB1.5tn |

| Traceability premium | >70% willing to pay |

| Bulk discounts | 5–10% |

| DTC margin recovery | ~3–5ppt |

Full Version Awaits

Beijing Sanyuan Foods Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Beijing Sanyuan Foods you'll receive after purchase, fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, with actionable insights and no placeholders. Instant download upon payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Beijing Sanyuan Foods faces moderate buyer power, intense rivalry among domestic dairy and packaged-food players, and growing substitute threats from plant-based and private-label brands, while supplier leverage is constrained by scale and regulatory oversight. Regulatory shifts and distribution costs add pressure but also create moats for compliant leaders. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sanyuan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw milk

Raw milk is the critical input and concentrated supply gives large-scale dairy farms and cooperatives leverage, with over 50% of China’s raw milk now sourced from large suppliers, elevating their bargaining power. Weather, feed-cost spikes and disease outbreaks have caused cyclical tightness and price swings—feed costs rose ~15–25% in 2022–24. Sanyuan tempers volatility through long-term contracts, partial vertical integration and proximity to Beijing, lowering transport and freshness risk.

Feed and inputs volatility

Feed grains, energy and additives cascade directly into raw milk costs, with feed often representing about 60% of dairy production costs and giving upstream agribusiness significant leverage during input-price spikes. Currency and commodity cycles in 2024 have rapidly shifted bargaining positions. Hedging and diversified sourcing mitigate but do not eliminate exposure. Procurement scale yields partial offset via stronger negotiated terms.

Specialty cultures & ingredients

Specialty probiotic strains, enzymes, cocoa and flavor houses are highly specialized and less interchangeable, with the top 5 global flavor houses holding about 60% market share in 2024, boosting supplier power over Beijing Sanyuan. IP-protected cultures and certification requirements (e.g., strain dossiers, GRAS/CFDA records) limit fast switching. Dual-sourcing and in-house R&D can reduce dependency and procurement risk by roughly 30%, while large yogurt volumes give Sanyuan negotiating leverage though niche inputs remain priced at a premium.

Packaging & cold chain

Packaging suppliers for Tetra Pak, HDPE and film are numerous, but tight specifications and multi-week lead times create procurement frictions for Beijing Sanyuan Foods; refrigerated logistics capacity tightens sharply in peak seasons, giving 3PLs leverage on spot rates. Long-term supplier and 3PL partnerships improve service levels and stabilize pricing. Owning segments of the cold chain—warehouses or fleets—reduces external supplier bargaining power and mitigates rate volatility.

Quality and compliance

Stringent Chinese dairy standards—heightened after the 2008 melamine crisis that sickened about 300,000 infants—raise the value of reliable, certified suppliers, enabling those with robust QA to command better pricing and contract terms.

Traceability mandates and mandatory audits increase near-term switching costs for buyers, while audits and digital traceability platforms (widely adopted across large processors) rebalance supplier power by boosting transparency and reducing information asymmetry.

- Certified-suppliers-premium

- Traceability-raises-switching-costs

- QA-enables-better-terms

- Audits-digital-traceability-increase-transparency

Dairy margins pressured by concentrated suppliers, 15-25% feed surge and flavor oligopoly

Beijing Sanyuan faces elevated supplier power: large farms supply >50% raw milk, feed accounts for ~60% of milk cost and rose 15–25% in 2022–24, and top‑5 flavor houses hold ~60% share—long contracts, partial vertical integration and cold‑chain ownership partly offset this pressure.

| Input | 2024 metric |

|---|---|

| Raw milk concentration | >50% from large suppliers |

| Feed cost share | ~60% of production cost |

| Feed cost change | +15–25% (2022–24) |

| Flavor house share | Top 5 ≈60% |

What is included in the product

Tailored Porter's Five Forces analysis for Beijing Sanyuan Foods that uncovers competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive risks and strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Beijing Sanyuan Foods — instantly visualize supplier/buyer pressure, rivalry, substitutes and entry threats with an editable spider chart and customizable scores, ready to drop into decks or dashboards for fast strategic decisions.

Customers Bargaining Power

Retailer concentration

National chains, convenience formats and e-commerce platforms (Alibaba + JD account for over 60% of online grocery sales in 2024) control shelf space and promotional calendars, forcing Beijing Sanyuan onto tough trade terms, returns policies and slotting fees. Their scale enables aggressive price/timing demands and private label expansion (private-label dairy roughly 10% penetration in modern trade). Strong Sanyuan brands and must-have SKUs partially offset this bargaining power.

Price-sensitive consumers

Milk and yogurt are frequent, low-involvement purchases with clear price anchors, and China’s retail dairy market was roughly US$60 billion in 2024, amplifying sensitivity to price moves. Low switching costs and heavy promotion cycles (weekend and festival discounts) mean consumers quickly shift brands, pressuring margins. Premium functional SKUs lower elasticity but require continuous R&D and marketing investment. Economic downturns increase trading-down risk and promotional dependence.

Digital comparison

E-commerce and social platforms let buyers compare prices and reviews instantly; over 1 billion mobile internet users in China (CNNIC 2024) amplify this transparency. Flash sales and livestreaming compress margins, with livestreaming GMV exceeding RMB1.5 trillion in 2024 (iMedia 2024). DTC channels can reclaim data and several percentage points of margin. Loyalty programs and subscriptions increase stickiness.

Foodservice and B2B

- bulk discounts: 5–10%

- typical monthly volume: 1–10 tonnes

- custom specs: raise dependency

- delivery reliability: key retention lever

Quality and safety expectations

Post-scandal Chinese consumers now prioritize safety and freshness, pushing buyers to favor brands with clear traceability; 2024 surveys report over 70% of urban consumers willing to pay premiums for traceable dairy, allowing firms like Beijing Sanyuan to reduce buyer power if certified; any safety lapse quickly triggers churn and restores bargaining leverage to customers.

- traceability premium: >70% willing to pay

- certifications: drive price resilience

- testing transparency: lowers churn risk

E-commerce squeeze 60% online grocery fuels margin pressure in China dairy

Retailers and e-commerce (Alibaba+JD ~60% online grocery 2024) exert strong trade leverage, squeezing margins; low switching costs and promotions keep consumer price sensitivity high in China’s ~US$60bn dairy market (2024). Livestreaming (GMV RMB1.5tr 2024) and >70% traceability premium shift power to informed buyers, while bulk buyers secure 5–10% discounts; DTC can recover ~3–5ppt margin.

| Metric | 2024 Value |

|---|---|

| Online grocery share (Alibaba+JD) | ~60% |

| China dairy market | ~US$60bn |

| Livestreaming GMV | RMB1.5tn |

| Traceability premium | >70% willing to pay |

| Bulk discounts | 5–10% |

| DTC margin recovery | ~3–5ppt |

Full Version Awaits

Beijing Sanyuan Foods Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Beijing Sanyuan Foods you'll receive after purchase, fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, with actionable insights and no placeholders. Instant download upon payment.