SAP Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

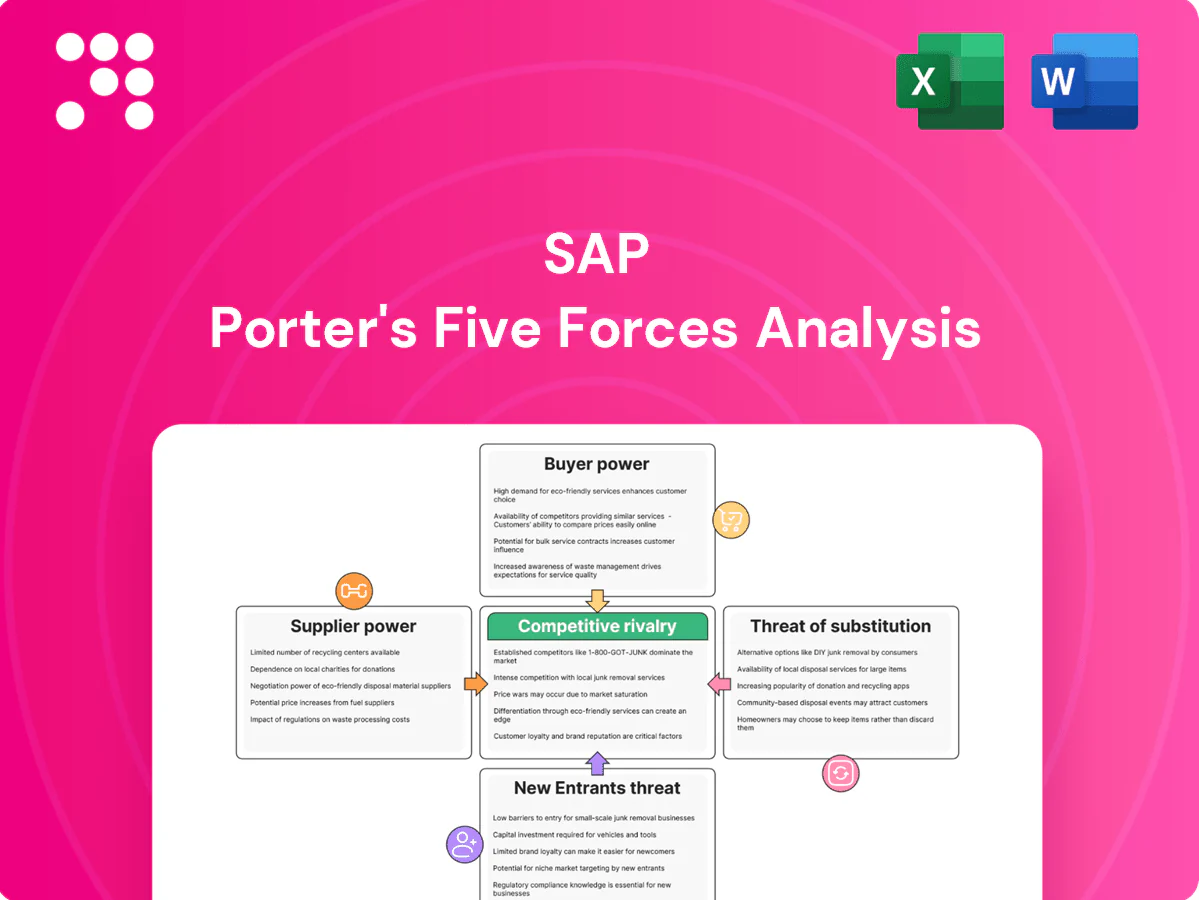

SAP’s Porter's Five Forces snapshot highlights strong buyer expectations, high supplier specialization, intense rivalry among enterprise software firms, moderate threat from cloud-native entrants, and evolving substitute pressures from niche SaaS. This brief overview signals where strategic risk and opportunity lie for SAP. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Dependence on hyperscalers

SAP’s cloud delivery leverages major IaaS providers for compute, storage and networking, concentrating negotiation power among hyperscalers: Gartner 2024 IaaS/PaaS shares show AWS ~34%, Microsoft Azure ~23% and Google Cloud ~11%, creating pricing and capacity asymmetries. Multi‑cloud deployments reduce lock‑in but add orchestration complexity and switching frictions. Outages and egress fees at hyperscalers can quickly translate into upstream cost pressure for SAP and its customers.

Specialized talent and partners

Skilled engineers, AI specialists and security experts are scarce and often command premium wages—senior AI/security engineers in the US frequently exceed $200,000 total comp in 2024. SAP depends on a global partner ecosystem of over 21,000 partners, so partner availability directly affects delivery timelines. Wage inflation and partner margin increases pressure services costs, while retention programs and partner certification tracks help moderate supplier power.

Core technology stack inputs

While SAP HANA cuts dependence on third‑party DBMS, suppliers of chips, middleware and open‑source libraries still exert influence; hardware supply cycles and licensing shifts can materially affect TCO and performance. Vendor roadmaps — e.g., CPU/accelerator changes from major foundries such as TSMC (≈55% global foundry share in 2024) — shape SAP optimization priorities and timing. Strategic sourcing and in‑house optimization notably reduce this exposure.

Data center colocation and network

Regional colocation providers and carriers determine latency and compliance for SAP workloads, and in regulated markets certified facilities are noticeably scarcer, increasing supplier leverage; long-term colocation and network contracts lock in capacity but reduce deployment flexibility while edge and private cloud alternatives diversify supply and raise integration overheads.

- Regional certified sites concentrate power

- Long-term contracts = capacity security but less agility

- Edge/private cloud lower single-supplier risk, raise integration costs

Regulatory and compliance services

Regulatory and compliance service providers—audit, localization, and compliance content vendors—directly slow SAP time-to-market across jurisdictions; as of 2024 reliance on timely external updates increased due to faster rule changes. Premium certification and content services command higher fees, while investing in internal regulatory expertise partially offsets supplier dependence and reduces update lag.

- 2024: increased reliance on third-party updates

- Audit/localization impact: delays in multi-jurisdiction rollouts

- Premium content: higher pricing power

- Internal expertise: partial mitigation

Hyperscaler concentration, talent scarcity and foundry dominance raise supplier risk

Hyperscaler concentration (AWS 34%, Azure 23%, GCP 11% in 2024) gives suppliers pricing/capacity leverage. Talent scarcity (senior AI/security comps > $200k in US, 2024) and 21,000+ partner reliance increase service cost and delivery risk. Foundry shifts (TSMC ≈55% share, 2024) and regional colocation scarcity amplify hardware and compliance supply power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Hyperscalers | AWS34%/Azure23%/GCP11% | Price/capacity risk |

| Talent | Senior comps >$200k | Higher Opex |

| Foundries | TSMC ≈55% | Hardware constraint |

| Partners | 21,000+ | Delivery dependency |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for SAP, uncovering competitive drivers, supplier and buyer influence on pricing, and barriers protecting incumbents. Highlights emerging threats, substitutes, and entry risks with strategic commentary for reports and presentations.

SAP-tailored Porter's Five Forces one-sheet that simplifies competitive pressure into a customizable radar chart—quickly assess supplier/buyer power, threats, and rivalry, then drop it into decks or dashboards for fast, board-ready decisions.

Customers Bargaining Power

Large enterprise procurement clout

Large global enterprises leverage procurement clout to demand volume discounts and bespoke contract terms, especially as the enterprise software market reached about $620 billion in 2024 (Statista 2024). Competitive bake-offs among Oracle, Microsoft and SAP raise buyer leverage, while long sales cycles push vendors toward pricing and service concessions. Referenceability and logo value further tilt negotiations in buyers' favor.

High switching costs yet rising optionality

Process re-engineering, data migration, and retraining make moving off SAP costly and time-consuming, anchoring customer dependence despite rising options. Modular SaaS offerings and open APIs now permit selective replacement of modules, enabling progressive decoupling such as swapping CRM or HCM and boosting buyer leverage at the edge. Multi-vendor estates further strengthen negotiation postures by creating credible alternative sourcing.

Outcome-based expectations

Buyers demand measurable ROI, uptime of 99.9% and security assurances, increasingly tying payments to outcomes in 2024. SLAs with financial penalties and defined success metrics raise supplier accountability and are standard in large deals. Value-realization services and proof-of-value pilots serve as negotiation levers; failure to demonstrate outcomes often results in price pressure or customer churn.

SMB price sensitivity

SMB price sensitivity drives demand for affordability and rapid time-to-value; 2024 surveys show median SMB SaaS contracts around 12 months and average SMB churn near 30%, increasing price-driven switching.

Smaller customers can pivot fast to lighter suites or point solutions, pressuring SAP to offer modular, lower-cost tiers and faster onboarding.

- short contracts = higher bargaining agility

- tiered packaging critical to capture elastic demand

Compliance and data residency demands

Buyers push modular outcome SaaS as $620B market tightens pricing

Customers wield strong leverage: enterprise procurement secures discounts in a $620B enterprise software market (Statista 2024); SAP cloud revenue €13.4B in 2024. Modular SaaS, open APIs, SMB churn ~30% and 99.9% SLA/outcome demands raise price pressure and drive modular, outcome-based contracts.

| Metric | Value | Source |

|---|---|---|

| Enterprise SW market | $620B | Statista 2024 |

| SAP cloud revenue | €13.4B | SAP 2024 |

| SMB churn | ~30% | 2024 surveys |

| Buyer SLA demand | 99.9% uptime | 2024 market deals |

Preview the Actual Deliverable

SAP Porter's Five Forces Analysis

This SAP Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to SAP's market position. This preview is the exact document you will receive after purchase—fully formatted and ready for immediate download. No placeholders or samples; the content shown is the final, professionally written deliverable for your use.

A Must-Have Tool for Decision-Makers

SAP’s Porter's Five Forces snapshot highlights strong buyer expectations, high supplier specialization, intense rivalry among enterprise software firms, moderate threat from cloud-native entrants, and evolving substitute pressures from niche SaaS. This brief overview signals where strategic risk and opportunity lie for SAP. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Dependence on hyperscalers

SAP’s cloud delivery leverages major IaaS providers for compute, storage and networking, concentrating negotiation power among hyperscalers: Gartner 2024 IaaS/PaaS shares show AWS ~34%, Microsoft Azure ~23% and Google Cloud ~11%, creating pricing and capacity asymmetries. Multi‑cloud deployments reduce lock‑in but add orchestration complexity and switching frictions. Outages and egress fees at hyperscalers can quickly translate into upstream cost pressure for SAP and its customers.

Specialized talent and partners

Skilled engineers, AI specialists and security experts are scarce and often command premium wages—senior AI/security engineers in the US frequently exceed $200,000 total comp in 2024. SAP depends on a global partner ecosystem of over 21,000 partners, so partner availability directly affects delivery timelines. Wage inflation and partner margin increases pressure services costs, while retention programs and partner certification tracks help moderate supplier power.

Core technology stack inputs

While SAP HANA cuts dependence on third‑party DBMS, suppliers of chips, middleware and open‑source libraries still exert influence; hardware supply cycles and licensing shifts can materially affect TCO and performance. Vendor roadmaps — e.g., CPU/accelerator changes from major foundries such as TSMC (≈55% global foundry share in 2024) — shape SAP optimization priorities and timing. Strategic sourcing and in‑house optimization notably reduce this exposure.

Data center colocation and network

Regional colocation providers and carriers determine latency and compliance for SAP workloads, and in regulated markets certified facilities are noticeably scarcer, increasing supplier leverage; long-term colocation and network contracts lock in capacity but reduce deployment flexibility while edge and private cloud alternatives diversify supply and raise integration overheads.

- Regional certified sites concentrate power

- Long-term contracts = capacity security but less agility

- Edge/private cloud lower single-supplier risk, raise integration costs

Regulatory and compliance services

Regulatory and compliance service providers—audit, localization, and compliance content vendors—directly slow SAP time-to-market across jurisdictions; as of 2024 reliance on timely external updates increased due to faster rule changes. Premium certification and content services command higher fees, while investing in internal regulatory expertise partially offsets supplier dependence and reduces update lag.

- 2024: increased reliance on third-party updates

- Audit/localization impact: delays in multi-jurisdiction rollouts

- Premium content: higher pricing power

- Internal expertise: partial mitigation

Hyperscaler concentration, talent scarcity and foundry dominance raise supplier risk

Hyperscaler concentration (AWS 34%, Azure 23%, GCP 11% in 2024) gives suppliers pricing/capacity leverage. Talent scarcity (senior AI/security comps > $200k in US, 2024) and 21,000+ partner reliance increase service cost and delivery risk. Foundry shifts (TSMC ≈55% share, 2024) and regional colocation scarcity amplify hardware and compliance supply power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Hyperscalers | AWS34%/Azure23%/GCP11% | Price/capacity risk |

| Talent | Senior comps >$200k | Higher Opex |

| Foundries | TSMC ≈55% | Hardware constraint |

| Partners | 21,000+ | Delivery dependency |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for SAP, uncovering competitive drivers, supplier and buyer influence on pricing, and barriers protecting incumbents. Highlights emerging threats, substitutes, and entry risks with strategic commentary for reports and presentations.

SAP-tailored Porter's Five Forces one-sheet that simplifies competitive pressure into a customizable radar chart—quickly assess supplier/buyer power, threats, and rivalry, then drop it into decks or dashboards for fast, board-ready decisions.

Customers Bargaining Power

Large enterprise procurement clout

Large global enterprises leverage procurement clout to demand volume discounts and bespoke contract terms, especially as the enterprise software market reached about $620 billion in 2024 (Statista 2024). Competitive bake-offs among Oracle, Microsoft and SAP raise buyer leverage, while long sales cycles push vendors toward pricing and service concessions. Referenceability and logo value further tilt negotiations in buyers' favor.

High switching costs yet rising optionality

Process re-engineering, data migration, and retraining make moving off SAP costly and time-consuming, anchoring customer dependence despite rising options. Modular SaaS offerings and open APIs now permit selective replacement of modules, enabling progressive decoupling such as swapping CRM or HCM and boosting buyer leverage at the edge. Multi-vendor estates further strengthen negotiation postures by creating credible alternative sourcing.

Outcome-based expectations

Buyers demand measurable ROI, uptime of 99.9% and security assurances, increasingly tying payments to outcomes in 2024. SLAs with financial penalties and defined success metrics raise supplier accountability and are standard in large deals. Value-realization services and proof-of-value pilots serve as negotiation levers; failure to demonstrate outcomes often results in price pressure or customer churn.

SMB price sensitivity

SMB price sensitivity drives demand for affordability and rapid time-to-value; 2024 surveys show median SMB SaaS contracts around 12 months and average SMB churn near 30%, increasing price-driven switching.

Smaller customers can pivot fast to lighter suites or point solutions, pressuring SAP to offer modular, lower-cost tiers and faster onboarding.

- short contracts = higher bargaining agility

- tiered packaging critical to capture elastic demand

Compliance and data residency demands

Buyers push modular outcome SaaS as $620B market tightens pricing

Customers wield strong leverage: enterprise procurement secures discounts in a $620B enterprise software market (Statista 2024); SAP cloud revenue €13.4B in 2024. Modular SaaS, open APIs, SMB churn ~30% and 99.9% SLA/outcome demands raise price pressure and drive modular, outcome-based contracts.

| Metric | Value | Source |

|---|---|---|

| Enterprise SW market | $620B | Statista 2024 |

| SAP cloud revenue | €13.4B | SAP 2024 |

| SMB churn | ~30% | 2024 surveys |

| Buyer SLA demand | 99.9% uptime | 2024 market deals |

Preview the Actual Deliverable

SAP Porter's Five Forces Analysis

This SAP Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to SAP's market position. This preview is the exact document you will receive after purchase—fully formatted and ready for immediate download. No placeholders or samples; the content shown is the final, professionally written deliverable for your use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

SAP’s Porter's Five Forces snapshot highlights strong buyer expectations, high supplier specialization, intense rivalry among enterprise software firms, moderate threat from cloud-native entrants, and evolving substitute pressures from niche SaaS. This brief overview signals where strategic risk and opportunity lie for SAP. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Dependence on hyperscalers

SAP’s cloud delivery leverages major IaaS providers for compute, storage and networking, concentrating negotiation power among hyperscalers: Gartner 2024 IaaS/PaaS shares show AWS ~34%, Microsoft Azure ~23% and Google Cloud ~11%, creating pricing and capacity asymmetries. Multi‑cloud deployments reduce lock‑in but add orchestration complexity and switching frictions. Outages and egress fees at hyperscalers can quickly translate into upstream cost pressure for SAP and its customers.

Specialized talent and partners

Skilled engineers, AI specialists and security experts are scarce and often command premium wages—senior AI/security engineers in the US frequently exceed $200,000 total comp in 2024. SAP depends on a global partner ecosystem of over 21,000 partners, so partner availability directly affects delivery timelines. Wage inflation and partner margin increases pressure services costs, while retention programs and partner certification tracks help moderate supplier power.

Core technology stack inputs

While SAP HANA cuts dependence on third‑party DBMS, suppliers of chips, middleware and open‑source libraries still exert influence; hardware supply cycles and licensing shifts can materially affect TCO and performance. Vendor roadmaps — e.g., CPU/accelerator changes from major foundries such as TSMC (≈55% global foundry share in 2024) — shape SAP optimization priorities and timing. Strategic sourcing and in‑house optimization notably reduce this exposure.

Data center colocation and network

Regional colocation providers and carriers determine latency and compliance for SAP workloads, and in regulated markets certified facilities are noticeably scarcer, increasing supplier leverage; long-term colocation and network contracts lock in capacity but reduce deployment flexibility while edge and private cloud alternatives diversify supply and raise integration overheads.

- Regional certified sites concentrate power

- Long-term contracts = capacity security but less agility

- Edge/private cloud lower single-supplier risk, raise integration costs

Regulatory and compliance services

Regulatory and compliance service providers—audit, localization, and compliance content vendors—directly slow SAP time-to-market across jurisdictions; as of 2024 reliance on timely external updates increased due to faster rule changes. Premium certification and content services command higher fees, while investing in internal regulatory expertise partially offsets supplier dependence and reduces update lag.

- 2024: increased reliance on third-party updates

- Audit/localization impact: delays in multi-jurisdiction rollouts

- Premium content: higher pricing power

- Internal expertise: partial mitigation

Hyperscaler concentration, talent scarcity and foundry dominance raise supplier risk

Hyperscaler concentration (AWS 34%, Azure 23%, GCP 11% in 2024) gives suppliers pricing/capacity leverage. Talent scarcity (senior AI/security comps > $200k in US, 2024) and 21,000+ partner reliance increase service cost and delivery risk. Foundry shifts (TSMC ≈55% share, 2024) and regional colocation scarcity amplify hardware and compliance supply power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Hyperscalers | AWS34%/Azure23%/GCP11% | Price/capacity risk |

| Talent | Senior comps >$200k | Higher Opex |

| Foundries | TSMC ≈55% | Hardware constraint |

| Partners | 21,000+ | Delivery dependency |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for SAP, uncovering competitive drivers, supplier and buyer influence on pricing, and barriers protecting incumbents. Highlights emerging threats, substitutes, and entry risks with strategic commentary for reports and presentations.

SAP-tailored Porter's Five Forces one-sheet that simplifies competitive pressure into a customizable radar chart—quickly assess supplier/buyer power, threats, and rivalry, then drop it into decks or dashboards for fast, board-ready decisions.

Customers Bargaining Power

Large enterprise procurement clout

Large global enterprises leverage procurement clout to demand volume discounts and bespoke contract terms, especially as the enterprise software market reached about $620 billion in 2024 (Statista 2024). Competitive bake-offs among Oracle, Microsoft and SAP raise buyer leverage, while long sales cycles push vendors toward pricing and service concessions. Referenceability and logo value further tilt negotiations in buyers' favor.

High switching costs yet rising optionality

Process re-engineering, data migration, and retraining make moving off SAP costly and time-consuming, anchoring customer dependence despite rising options. Modular SaaS offerings and open APIs now permit selective replacement of modules, enabling progressive decoupling such as swapping CRM or HCM and boosting buyer leverage at the edge. Multi-vendor estates further strengthen negotiation postures by creating credible alternative sourcing.

Outcome-based expectations

Buyers demand measurable ROI, uptime of 99.9% and security assurances, increasingly tying payments to outcomes in 2024. SLAs with financial penalties and defined success metrics raise supplier accountability and are standard in large deals. Value-realization services and proof-of-value pilots serve as negotiation levers; failure to demonstrate outcomes often results in price pressure or customer churn.

SMB price sensitivity

SMB price sensitivity drives demand for affordability and rapid time-to-value; 2024 surveys show median SMB SaaS contracts around 12 months and average SMB churn near 30%, increasing price-driven switching.

Smaller customers can pivot fast to lighter suites or point solutions, pressuring SAP to offer modular, lower-cost tiers and faster onboarding.

- short contracts = higher bargaining agility

- tiered packaging critical to capture elastic demand

Compliance and data residency demands

Buyers push modular outcome SaaS as $620B market tightens pricing

Customers wield strong leverage: enterprise procurement secures discounts in a $620B enterprise software market (Statista 2024); SAP cloud revenue €13.4B in 2024. Modular SaaS, open APIs, SMB churn ~30% and 99.9% SLA/outcome demands raise price pressure and drive modular, outcome-based contracts.

| Metric | Value | Source |

|---|---|---|

| Enterprise SW market | $620B | Statista 2024 |

| SAP cloud revenue | €13.4B | SAP 2024 |

| SMB churn | ~30% | 2024 surveys |

| Buyer SLA demand | 99.9% uptime | 2024 market deals |

Preview the Actual Deliverable

SAP Porter's Five Forces Analysis

This SAP Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to SAP's market position. This preview is the exact document you will receive after purchase—fully formatted and ready for immediate download. No placeholders or samples; the content shown is the final, professionally written deliverable for your use.